VA Loan Appraisal Requirements: MPRs, Fees & Timeline 2026

A VA loan can get you into a home with no down payment and no private mortgage insurance, but the property itself still has to pass inspection. VA loan appraisal requirements exist to protect both you and the lender by confirming the home meets minimum safety and livability standards. If the property falls short, your closing can stall or fall apart entirely.

The appraisal isn't just about value. VA appraisers evaluate the home against a specific set of Minimum Property Requirements (MPRs) that cover everything from the roof to the water supply. Knowing what they look for, and what triggers a failure, gives you a real advantage before you're under contract. Understanding the fees and timeline upfront also helps you plan without surprises.

With over 25 years of lending experience and more than $150 million in funded loans, I've guided hundreds of veterans and active-duty service members through this exact process. At David Roa, VA loans are one of our core residential mortgage products, and I've seen firsthand what causes delays and how to avoid them. This guide breaks down the MPRs, costs, and timeline you need to know heading into your 2026 VA purchase.

Why VA appraisals matter for buyers and sellers

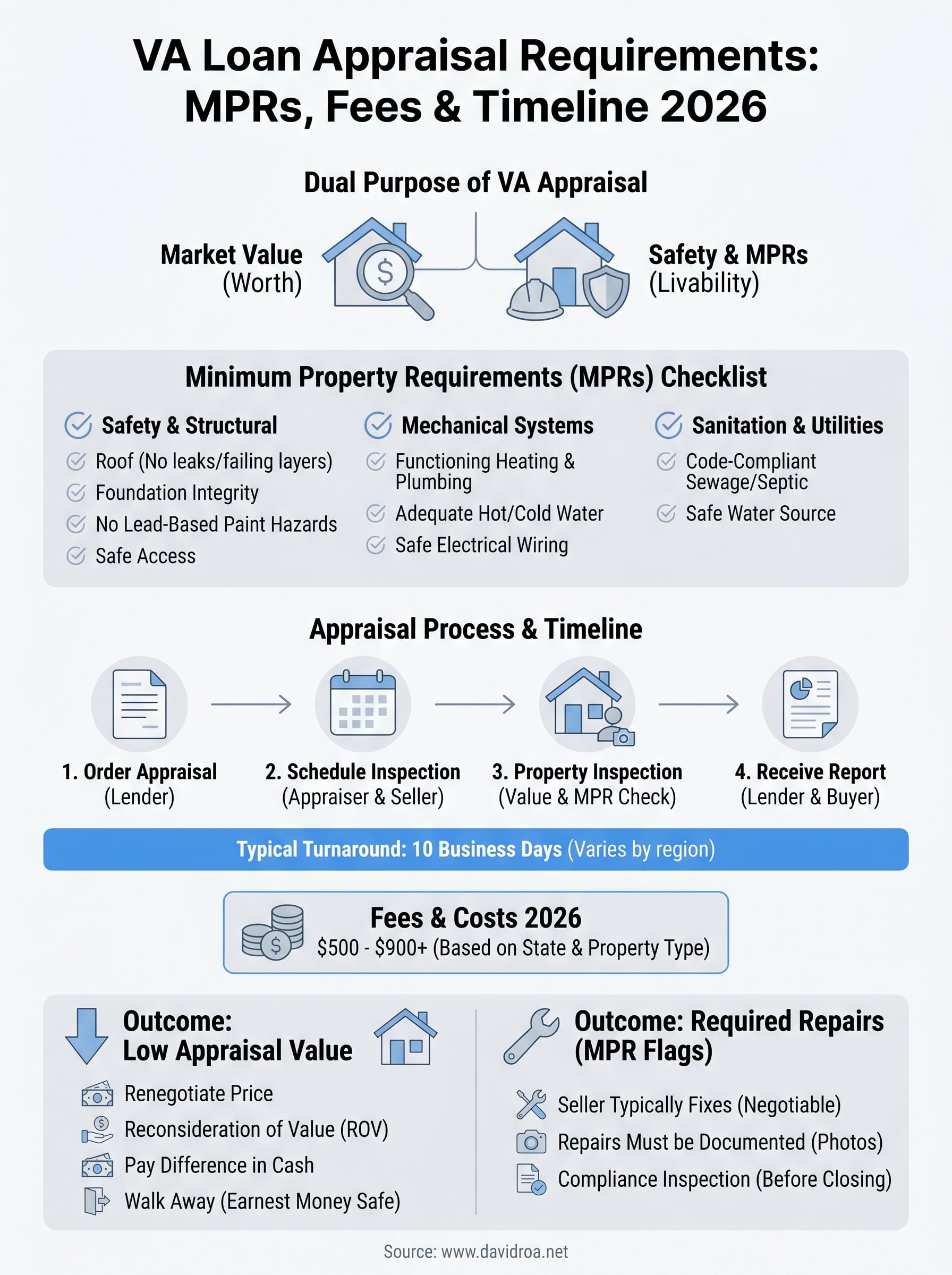

The VA appraisal does two things at once: it tells the lender what the home is worth, and it tells both you and the VA that the property is safe enough to live in. Most conventional appraisals stop at value. VA loan appraisal requirements go further by layering in Minimum Property Requirements that the appraiser checks alongside market comparables. That dual purpose is what sets VA appraisals apart, and it's also why they sometimes create friction that buyers and sellers don't expect.

What the appraisal means for you as a buyer

As a buyer, the VA appraisal is one of the strongest protections you have in the transaction. If the appraised value comes in below the purchase price, you are not required to pay the difference out of pocket just because the seller wants more. You can renegotiate, walk away, or use a Reconsideration of Value request to challenge the number with supporting data. That protection sits in your corner from the moment the appraisal is ordered.

The MPR side of the appraisal protects you differently. A conventional loan might close on a home with a failing roof or faulty electrical, and the buyer discovers those problems later. With a VA appraisal, the appraiser flags those issues before closing, which means you're less likely to move into a property that needs immediate expensive repairs. That's not a bureaucratic hurdle; it's a filter that works in your favor.

If the VA appraisal flags a safety issue, the lender cannot close the loan until the seller addresses it, which gives you real leverage at the negotiating table.

What the appraisal means for sellers

Sellers who haven't worked with VA buyers before often assume the process is more complicated than it needs to be. The truth is that a home in good structural condition with working systems, safe access, and adequate utilities will pass without issue. Problems only arise when the property has deferred maintenance or code violations that would concern any reasonable buyer.

Sellers benefit from knowing the MPR checklist before they list. A pre-listing inspection that mirrors VA standards can prevent surprises once a buyer's appraiser arrives. When the appraiser does flag repairs, the seller can choose to complete them, negotiate a price reduction, or decline. The deal doesn't automatically die, but time pressure increases because VA loans have strict closing timelines that don't leave room for extended back-and-forth over repairs. The faster a seller can respond to repair requests, the better the odds of reaching the closing table without complications.

How the VA appraisal process works step by step

Once your offer is accepted and your loan application is underway, the VA appraisal process begins automatically. Your lender submits the request through the VA's ordering system, and the VA assigns a licensed appraiser from its approved panel for that geographic area. The VA controls that assignment directly, not your lender, which keeps the appraisal independent from outside pressure by any party in the transaction.

Ordering the appraisal

Your lender initiates the order, and the VA system selects an approved appraiser in the property's region. You typically pay the appraisal fee at or before this stage. Once assigned, the appraiser contacts the listing agent or seller to schedule the physical inspection at a mutually available time. Delays in seller availability at this step are one of the most common reasons the overall timeline stretches.

The property inspection

The appraiser visits the home in person and works through two separate evaluations at the same time: they assess market value by comparing the home to recent similar sales in the area, and they check the property against VA Minimum Property Requirements. This dual evaluation is what makes va loan appraisal requirements different from a standard appraisal. The appraiser documents any conditions that could affect safety, structural soundness, or livability with photographs and written notes in the report.

The VA appraiser is assigned by and works for the VA, not for you or your lender, which is why neither party can simply override the report without going through a formal review process.

Receiving the appraisal report

After the inspection, the appraiser submits the completed report to your lender, who is then required to give you a copy within a few business days. The report lists the appraised value and identifies any required repairs or conditions that must be resolved before your loan can close. From there, you and your lender coordinate with the seller to address those items before moving forward.

VA Minimum Property Requirements checklist for 2026

VA Minimum Property Requirements cover the conditions the VA considers non-negotiable for any property securing a VA loan. These aren't arbitrary standards; they reflect the VA's commitment to ensuring veterans don't purchase homes with hidden hazards or structural deficiencies that put their investment at risk. When va loan appraisal requirements include MPRs, the appraiser isn't hunting for cosmetic flaws. They're checking whether the home is safe, structurally sound, and sanitary enough for occupancy.

Safety and structural standards

The appraiser will flag any condition that creates an immediate risk to occupants. This covers the roof, foundation, and overall structural integrity of the home. A roof with active leaks or more than one failing layer will require repair or replacement before your loan can close. The property must also have safe pedestrian access from a public or private road, maintained year-round.

The VA requires that the property be free of lead-based paint hazards, particularly in homes built before 1978, which the appraiser must document during the inspection.

Items the appraiser checks under safety and structure:

- Roof condition and estimated remaining life

- Foundation integrity with no significant settling or cracking

- No evidence of termite damage or active infestation

- Safe electrical systems with no exposed wiring

- Lead-based paint hazards in pre-1978 homes

Mechanical systems and utilities

Your home must have functioning heating, plumbing, and electrical systems that serve every room in the house. A wood-burning stove alone does not satisfy the heating requirement unless local climate conditions make it a reasonable primary source. Plumbing must supply adequate hot and cold running water, and the water source must be safe whether it comes from a municipal line or a private well.

Sewage disposal must be operational and code-compliant before closing. If your property uses a septic system, the appraiser will note it in the report, and your lender may require a separate inspection to confirm it's functioning correctly. These mechanical checks protect your long-term investment, not just the VA's interest in the collateral.

VA appraisal fees and timeline in 2026

Understanding what you'll pay and how long you'll wait helps you build a realistic closing schedule from the start. The VA sets maximum allowable fees for appraisals by state and property type, which caps how much appraisers can charge. The VA publishes and updates these limits periodically, so your lender can confirm the exact fee for your region before the order is placed.

What the VA appraisal costs in 2026

VA appraisal fees in 2026 range from roughly $500 to over $900, depending on your state and the type of property being evaluated. Single-family homes in most markets fall between $600 and $800. Rural properties and multi-unit homes tend to cost more because the appraiser spends more time on-site and works with a smaller pool of comparable sales.

The VA publishes its official fee schedule by state, and your lender must disclose the appraisal fee to you before you pay it.

You pay the appraisal fee directly, and it is typically non-refundable even if the loan does not close. Factor this into your upfront cost planning alongside your home inspection fee and any earnest money you've already committed.

How long the VA appraisal takes

The VA assigns target completion timelines that appraisers in each region must follow, and in most markets the full appraisal wraps up within 10 business days of the property inspection. High demand in competitive markets or rural areas with fewer VA-approved appraisers can push that window closer to two to three weeks, which your expected closing date needs to absorb.

Staying on schedule with va loan appraisal requirements also depends on seller cooperation. If the seller delays scheduling the inspection, your entire closing timeline shifts right along with it. Confirm access availability with the listing agent before your lender submits the appraisal order to avoid that common and entirely preventable delay.

What happens if the appraisal is low or flags repairs

A low appraisal or a list of required repairs doesn't automatically kill your deal, but it does require you to act quickly and strategically. Understanding your options under va loan appraisal requirements before this situation occurs puts you in a much stronger position when the report lands.

When the appraised value comes in low

If the appraiser values the home below your agreed purchase price, you have four realistic paths forward. You can renegotiate the purchase price down to the appraised value, which many sellers accept when they understand the VA's rules. You can submit a Reconsideration of Value request through your lender, providing the appraiser with stronger comparable sales data that supports a higher number. You can pay the difference between the appraised value and the purchase price out of pocket, though that defeats much of the financial benefit of a VA loan. Finally, you can walk away and keep your earnest money, since the VA appraisal contingency gives you that exit.

A Reconsideration of Value does not guarantee a different outcome, but it is worth pursuing if you have solid comparable sales data that the appraiser may have missed.

When the appraiser flags required repairs

Required repairs fall into two categories: those the appraiser lists as mandatory before closing, and those they note as recommended but not blocking. Mandatory repairs must be completed and documented with photos before your loan can close. Typically, the seller handles these costs, but you can negotiate who pays or split the cost if the seller refuses to cover everything.

Your lender will order a compliance inspection once repairs are complete to confirm the work meets the standard outlined in the report. That inspection carries its own fee, usually between $100 and $150, and the turnaround is generally faster than the original appraisal. Build that extra step into your closing timeline so the schedule doesn't slip at the final stage.

Key takeaways

VA loan appraisal requirements cover two things every buyer needs to understand before going under contract: market value and Minimum Property Requirements. The appraisal protects you by flagging safety and structural issues before closing, and it gives you real leverage to renegotiate if the value comes in below the purchase price. Fees range between $500 and $900 depending on your state, and most appraisals wrap up within 10 business days of the physical property inspection.

When the report flags repairs or delivers a low value, you have options. A Reconsideration of Value request lets you challenge the number with stronger comparable sales data, and mandatory repairs must be completed and documented before your loan can close. Knowing these rules before you make an offer puts you in a stronger position than most buyers.

Ready to move forward with your VA benefit? Connect with a VA loan specialist at David Roa to walk through the process and close with confidence.