Apply For FHA Loan Online: Steps, Docs & Timeline In 2026

You can apply for an FHA loan online without ever stepping into a bank branch, and in 2026, the process is more streamlined than most people expect. But "easy to start" doesn't mean "impossible to mess up." Missing a single document or misunderstanding an eligibility requirement can stall your approval for weeks.

That's where having the right guidance matters. At David Roa, we've helped borrowers secure FHA financing as part of over $150 million in funded loans across more than 25 years in the lending business. We work with first-time buyers, ITIN holders, and everyone in between, so we've seen what trips people up and what moves the needle.

This guide breaks down the exact steps to complete your FHA application online, the documents you'll need ready before you start, and a realistic timeline from application to closing. Whether you're buying your first home or exploring FHA options you didn't know existed (like 203k renovation loans), you'll walk away knowing exactly what to do next.

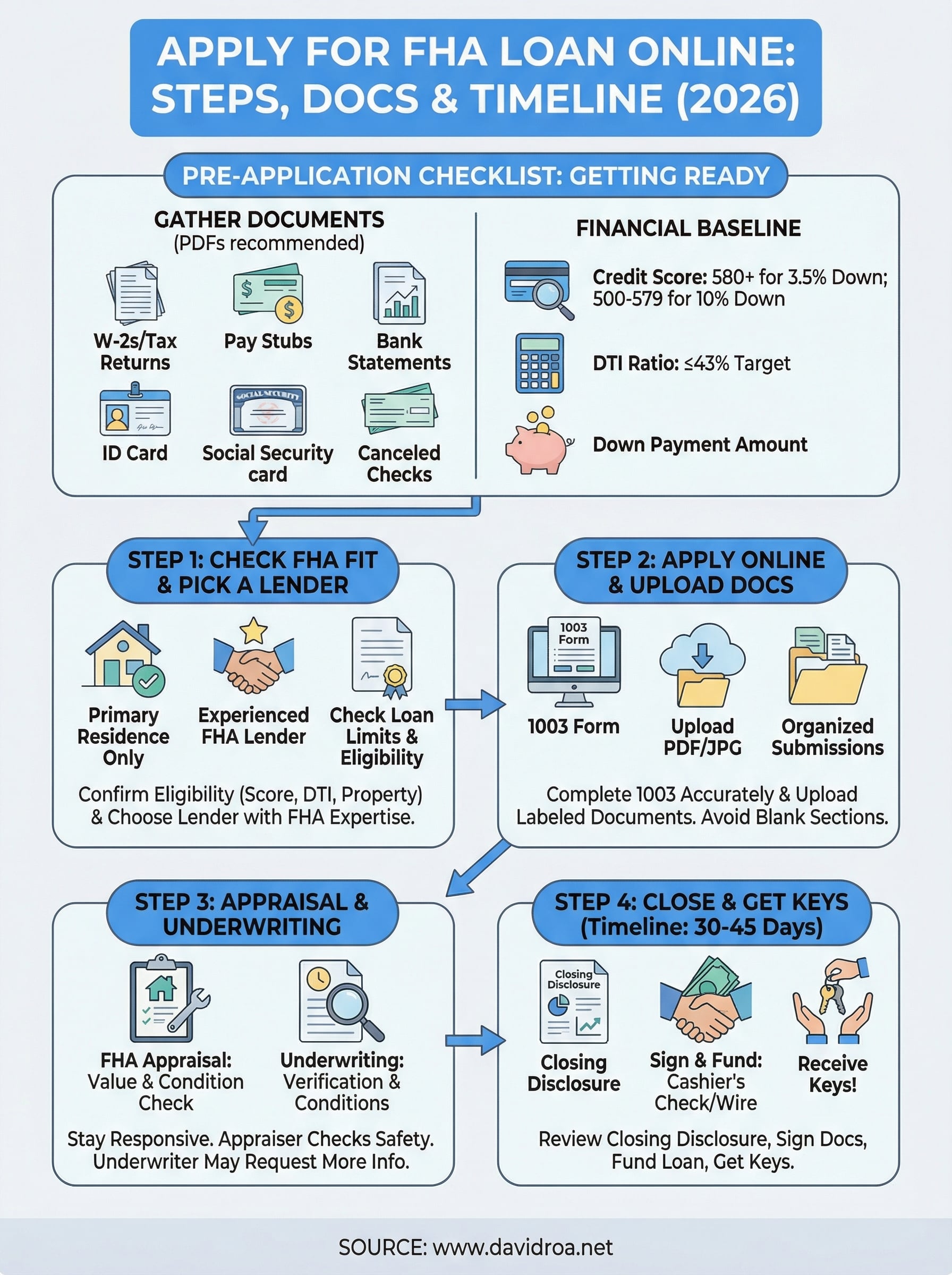

What you need before you apply online

Getting organized before you apply for an FHA loan online saves you from the most common delay: scrambling for paperwork after a lender already asks for it. Lenders pull your credit, verify your income, and confirm your available assets within the first few days of submission, so having everything ready upfront keeps your file moving without unnecessary gaps.

Your financial baseline

Before you touch an application, confirm three numbers: your credit score, your debt-to-income (DTI) ratio, and your down payment amount. FHA loans require a minimum 580 credit score for the standard 3.5% down payment option. If your score falls between 500 and 579, you'll need 10% down instead. Your DTI ratio should sit at or below 43% in most cases, though some lenders will stretch higher with compensating factors like strong cash reserves.

A credit score of 580 or above unlocks the most favorable FHA terms, so pull your report before you start comparing lenders.

Documents to gather in advance

Lenders ask for the same core set of documents regardless of which online platform you use. Pull these together before you open the application:

- Two years of W-2s or tax returns (self-employed borrowers need two full years of complete returns with all schedules)

- 30 days of recent pay stubs

- Two to three months of bank statements for every account you plan to use for the down payment or closing costs

- A copy of your government-issued ID

- Your Social Security number or ITIN if you're applying through an ITIN program

- 12 months of canceled rent checks or your landlord's contact information if you currently rent

Scan each document and save it as a PDF before you start the application. Most online portals accept PDF, JPG, and PNG, but PDF keeps multi-page documents clean and reduces upload errors.

Step 1. Check FHA fit and pick a lender

Before you apply for an FHA loan online, confirm FHA is actually the right product for your situation. FHA loans are government-backed mortgages built for borrowers with lower credit scores or smaller down payments, but they carry mandatory mortgage insurance premiums (MIP) that add to your monthly payment. If your score is above 720 and you have 20% down, a conventional loan might cost you less over the life of the loan.

Confirm your FHA eligibility

Run through each item below before you contact a lender. A quick self-check prevents application delays later and helps you walk into any conversation knowing your exact financial position.

- Credit score: 580 or above for 3.5% down; 500-579 for 10% down

- DTI ratio: 43% or below in most cases

- Property type: Must be your primary residence, not a rental or vacation home

- Loan limits: Check your county's 2026 FHA loan ceiling at HUD.gov

FHA does not fund investment properties, so if you're buying a rental, ask about DSCR or hard money alternatives instead.

Pick the right lender

Not every lender handles FHA files with the same speed or flexibility. Look for a licensed mortgage broker with a direct track record in FHA closings rather than a general lender who lists FHA as one product among dozens.

Your lender's familiarity with FHA guidelines directly affects how fast your file moves through underwriting, so experience here is not a minor detail.

Step 2. Apply online and upload your documents

Once you've selected your lender, you'll access their online portal to complete the Uniform Residential Loan Application, known as the 1003 form. Most lenders use a proprietary system, but the data they ask for is standard across all FHA applications.

Complete the 1003 accurately

The 1003 covers your personal information, employment history, income, assets, and the property details. Fill every field completely. Leaving a section blank forces an underwriter to send a conditions letter requesting clarification, which adds days to your timeline.

Double-check your employer's address and exact start date before submitting. Small errors in employment history are one of the most common causes of early underwriting flags.

Upload your documents in the right format

When you apply for an FHA loan online, the document upload step is where most delays occur. Label each file clearly before uploading, using a format like:

LastName_W2_2024.pdfLastName_BankStatement_Jan2026.pdfLastName_PayStub_March2026.pdf

Labeled files move through the lender's processing queue faster, and organized submissions reduce the back-and-forth with your loan processor by a significant margin.

Step 3. Navigate appraisal and underwriting

After you apply for an FHA loan online and your file is submitted, the lender orders an FHA appraisal and sends your application to underwriting. These two processes run close together, and both require you to stay responsive. A delayed response to an underwriter's question can push your closing date back by a week or more.

The FHA Appraisal

An FHA appraiser evaluates both market value and property condition. Unlike conventional appraisals, the FHA version checks for health and safety issues, meaning a cracked foundation, missing handrails, or peeling paint on older homes can trigger required repairs before closing. If the appraiser flags a repair, your seller must complete it, or you'll need to negotiate a price reduction or escrow holdback.

If the appraisal comes in below the purchase price, you can renegotiate with the seller, pay the difference in cash, or walk away without losing your deposit.

What Underwriters Review

Your underwriter verifies every document you uploaded and checks that your file meets all FHA guidelines. Keep your phone and email accessible during this stage. Common conditions include a letter of explanation for large deposits, updated bank statements, or proof of employment if your closing date extends beyond 60 days from your original pay stub.

Step 4. Close the loan and get the keys

Once underwriting clears your file, your lender issues a clear to close, which means your loan is fully approved and a closing date gets scheduled. At this point, the hardest work is behind you. Your job now is to review your final documents carefully and show up prepared.

Review Your Closing Disclosure

Your lender sends a Closing Disclosure at least three business days before closing. Read every line and compare it against your Loan Estimate from early in the process. Confirm that your interest rate, loan amount, and closing costs match what you agreed to. If any number shifted without explanation, contact your lender immediately before the three-day window closes.

Flag any fee that wasn't on your original Loan Estimate so your lender can explain or correct it before you sign.

What Happens at the Closing Table

You'll sign a stack of documents and bring a certified or cashier's check for your remaining closing costs and down payment. Wire transfers are also common, but confirm the exact amount with your title company the day before. After signatures, your lender funds the loan, the title company records the deed, and you receive your keys. The entire process from when you first apply for an FHA loan online to this moment typically runs 30 to 45 days.

Next Steps

You now have everything you need to apply for an FHA loan online with confidence. Gather your documents in advance, confirm your credit score and DTI ratio, and choose a lender with proven FHA experience before you touch the application. Those three steps alone eliminate the delays that slow most borrowers down.

From there, the process follows a predictable path: submit a complete 1003, respond quickly to underwriting conditions, and review your Closing Disclosure carefully before you sign. Most borrowers close in 30 to 45 days when their file is clean from the start.

Working with an experienced mortgage broker makes a real difference, especially if your situation involves an ITIN, self-employment income, or a renovation loan. If you're ready to move forward, connect with David Roa and get guidance from a lender with over 25 years of FHA closings behind him.