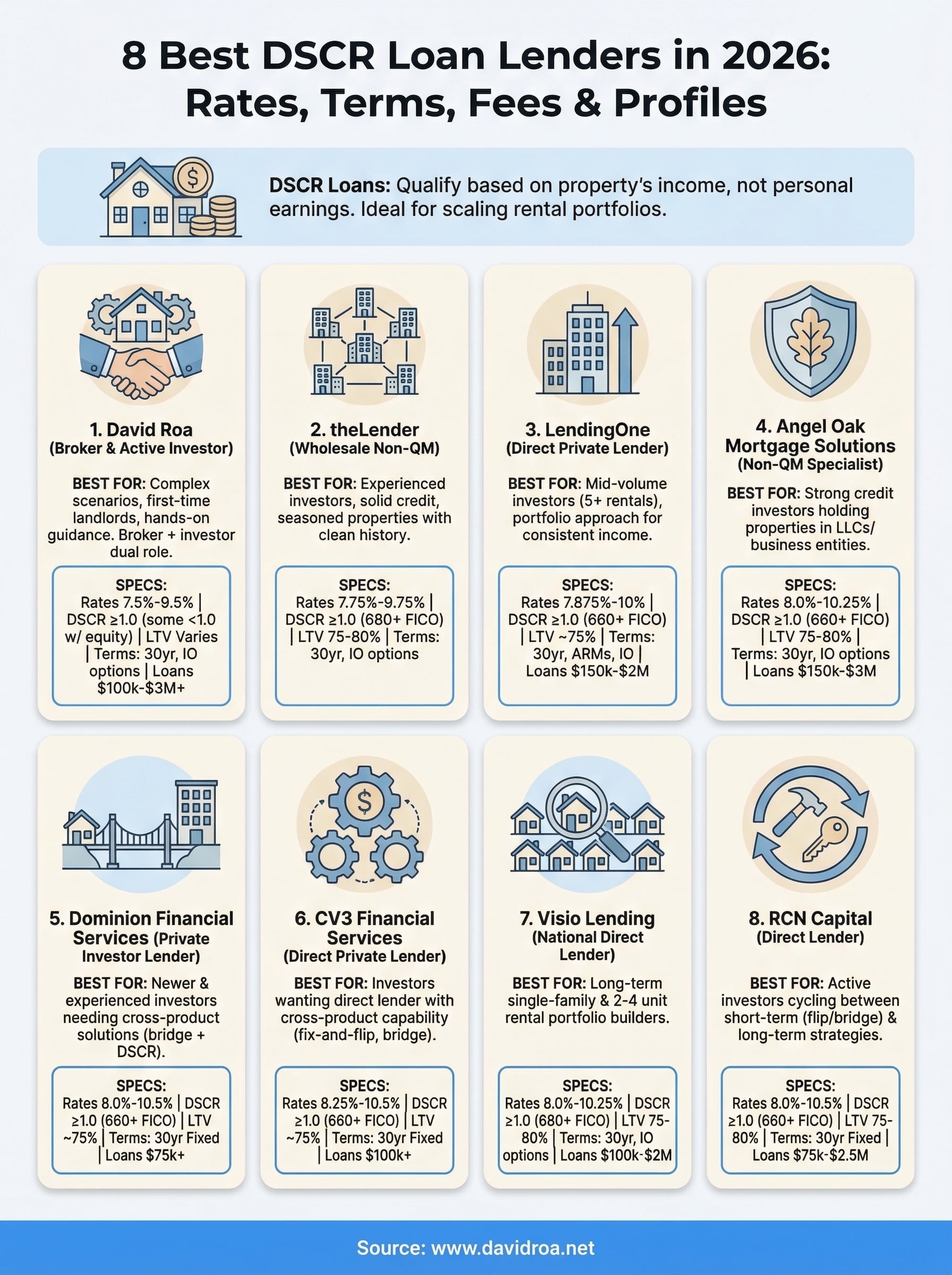

8 Best DSCR Loan Lenders in 2026: Rates, Terms, Fees

DSCR loans let real estate investors qualify based on a property's income rather than their own, which makes them one of the most practical tools for scaling a rental portfolio. But not all lenders structure these loans the same way. Rates, leverage, prepayment penalties, and minimum DSCR ratios vary widely from one lender to the next, and picking the wrong one can cost you tens of thousands over the life of a loan. That's why finding the best DSCR loan lenders matters just as much as finding the right property.

Having originated DSCR loans for investors across the country over a 25-plus-year career, with more than $150 million funded, I've seen firsthand how much the lender impacts a deal's profitability. At David Roa, we work with many of the lenders featured here on a daily basis and actively invest in real estate ourselves, so this isn't a list assembled from a distance. It's built from direct experience closing these loans.

Below, I break down eight top DSCR lenders for 2026, comparing their rates, terms, fees, and ideal borrower profiles. Whether you're financing your first rental or adding your twentieth, this guide gives you the side-by-side detail you need to make a confident choice.

1. David Roa

When searching for the best DSCR loan lenders, working with a broker who also operates as an active investor gives you a fundamentally different experience. At David Roa, you get more than a loan officer processing paperwork. You get a 25-plus-year veteran who has personally flipped properties, manages a restaurant, and has funded over $150 million in loans across residential and commercial transactions.

What David Roa offers for DSCR borrowers

David Roa provides DSCR loans for single-family rentals, multi-unit properties, and mixed-use assets through a broad network of wholesale lenders. Because the business operates as a broker, you access multiple loan programs and can shop for competitive pricing without walking into a single bank. The focus is on matching your specific deal to the right lender rather than forcing you into one product.

Best fit for David Roa

This option works best for investors who carry complex scenarios: ITIN holders, first-time landlords, or experienced buyers who want hands-on guidance through the process. If you prefer working with someone who understands what it's like to sit on both sides of a transaction, David Roa's dual background as a broker and active real estate investor is a clear advantage over a typical retail loan officer.

Working with someone who has personally closed investment deals means your loan structure gets reviewed with the actual performance of the property in mind, not just the checkbox items on a loan application.

Rates, fees, and terms to expect

DSCR loan rates through David Roa typically run 7.5% to 9.5% depending on credit score, LTV, and property type as of early 2026. Loan amounts range from $100,000 to over $3 million, with 30-year terms available including interest-only options on select programs. Prepayment penalties vary by lender, so always confirm the step-down structure before you sign.

Underwriting focus and DSCR requirements

The underwriting process centers on the property's rental income relative to its monthly debt obligation. A minimum DSCR of 1.0 is standard across most programs, though some lenders accept ratios below 1.0 with a larger down payment or stronger credit profile. Personal income documentation is not required.

Questions to ask before you apply

- What minimum DSCR ratio does this specific program require?

- Does the rate improve if you put 20% or 25% down?

- What prepayment penalty structure applies, and how many years does it run?

2. theLender

theLender is a wholesale non-QM lender that built its product line around investor-focused loan programs, including DSCR. It operates exclusively through mortgage brokers, which means you won't access this lender directly but can reach it through a broker who has an established relationship.

What theLender offers for DSCR borrowers

theLender offers DSCR loans for single-family, 2-4 unit, and small multifamily properties. Its programs are designed specifically for real estate investors, with flexible documentation requirements and no personal income verification needed to qualify.

Best fit for theLender

This lender suits experienced investors with solid credit and seasoned rental properties that show clean income history. It's a strong fit when you need reliable wholesale pricing and want a lender that understands investor deal structures without requiring extensive explanation.

If you work with a broker who already has a relationship with theLender, you can often move faster through underwriting because the channel is built for volume.

Rates, fees, and terms to expect

Rates generally fall in the 7.75% to 9.75% range in early 2026, depending on LTV and credit score. 30-year fixed and interest-only options are available on qualifying loans. Origination fees vary by broker.

Underwriting focus and DSCR requirements

theLender typically requires a minimum DSCR of 1.0 and a credit score of at least 680. LTV caps usually sit at 75% to 80% for most property types.

Questions to ask before you apply

- Does your broker have an active wholesale agreement with theLender?

- What's the minimum credit score for your target LTV?

- Are interest-only terms available on your specific property type?

3. LendingOne

LendingOne is a direct private lender built specifically for real estate investors. Unlike conventional lenders, LendingOne underwrites based on rental property cash flow rather than personal income, which removes a major obstacle for investors who don't show strong W-2 income on paper.

What LendingOne offers for DSCR borrowers

LendingOne provides DSCR loans for single-family, 2-4 unit, condo, and small multifamily properties. Its product line includes 30-year fixed, adjustable-rate, and interest-only options. The company handles underwriting in-house, which speeds up decisions compared to routing files through multiple parties. Among the best DSCR loan lenders in this space, LendingOne stands out for processing volume and in-house efficiency.

Best fit for LendingOne

This lender fits mid-volume investors with multiple rentals who want a reliable, repeatable process. If your properties generate consistent income and your credit profile is solid, LendingOne can move your application through quickly without unnecessary back-and-forth.

Investors managing five or more rentals benefit most from lenders that think in portfolio terms rather than reviewing each property as a standalone transaction.

Rates, fees, and terms to expect

Rates typically run 7.875% to 10% in early 2026 based on credit score and LTV. Loan amounts start at $150,000 with a ceiling around $2 million on most programs.

Underwriting focus and DSCR requirements

LendingOne requires a minimum DSCR of 1.0 and a credit score of at least 660. LTV caps typically sit at 75% for standard rental properties, though terms can shift based on property type and loan size.

Questions to ask before you apply

- What loan amount maximum applies to your specific property type?

- Does your credit score tier qualify you for a meaningfully lower rate?

- What does the prepayment penalty schedule look like on your selected term length?

4. Angel Oak Mortgage Solutions

Angel Oak Mortgage Solutions is one of the more established names among the best DSCR loan lenders in the non-QM space. The company has been originating alternative documentation loans since 2013 and built a substantial track record with rental property investors who can't qualify through conventional channels.

What Angel Oak Mortgage Solutions offers for DSCR borrowers

The company offers DSCR loans for single-family, 2-4 unit, and non-warrantable condo properties with no personal income verification required. This makes the program practical for investors who structure income through LLCs or other business entities. Loans are available in 30-year fixed and interest-only formats depending on the property and borrower profile.

Best fit for Angel Oak Mortgage Solutions

This lender works best for investors with strong credit who hold properties through business entities rather than in their personal name. If you're building a portfolio under an LLC and want a lender familiar with that structure, Angel Oak's non-QM depth makes them a reliable choice.

Lenders with deep non-QM experience handle LLC-owned rentals more cleanly in underwriting, which cuts down on unnecessary delays during processing.

Rates, fees, and terms to expect

Rates typically range from 8.0% to 10.25% in early 2026, depending on credit score, LTV, and property type. Loan amounts generally start at $150,000 with upper limits reaching $3 million on qualifying properties.

Underwriting focus and DSCR requirements

Most programs require a minimum DSCR of 1.0 with credit score minimums around 660. LTV caps sit at 75% to 80% for standard rental properties, with stricter limits applying to condos and certain property types.

Questions to ask before you apply

- Does your LLC structure meet Angel Oak's entity documentation requirements?

- What credit score threshold unlocks the most favorable rate tier?

- Are interest-only terms available for your specific loan amount and property type?

5. Dominion Financial Services

Dominion Financial Services is a Baltimore-based private lender that focuses almost entirely on real estate investors. Unlike banks that treat rental property loans as a secondary product, Dominion built its entire platform around investor financing, which shows in how its underwriters evaluate DSCR deals.

What Dominion Financial Services offers for DSCR borrowers

The company offers DSCR loans for single-family rentals, 2-4 unit properties, and small multifamily assets. Dominion also provides bridge and fix-and-flip loans, which gives investors a single lending source for both short-term acquisition financing and long-term rental holds. No personal income verification is required on DSCR products.

Best fit for Dominion Financial Services

This lender suits newer investors and experienced buyers who want to work with a lender that specializes in investor products exclusively. If you're evaluating the best DSCR loan lenders that also offer short-term capital under the same roof, Dominion's cross-product setup is worth a close look.

Pairing your DSCR loan with a bridge product from the same lender can simplify the refinance transition after a fix-and-flip project closes.

Rates, fees, and terms to expect

Rates generally run 8.0% to 10.5% in early 2026, with 30-year fixed terms available on qualifying rental properties. Loan amounts typically start at $75,000.

Underwriting focus and DSCR requirements

Dominion requires a minimum DSCR of 1.0 and a credit score of at least 660. LTV caps sit around 75% for most standard rental programs.

Questions to ask before you apply

- Can you combine a bridge loan and DSCR product within the same process?

- What is the minimum loan amount for your target property?

- Does a larger down payment improve your rate or DSCR threshold?

6. CV3 Financial Services

CV3 Financial Services is a private direct lender focused exclusively on real estate investors. The company offers a range of investor loan products, with DSCR loans positioned as a core part of its rental property financing lineup. Because CV3 operates as a direct lender, it controls its own underwriting, which gives it more flexibility than correspondent lenders who sell decisions upstream.

What CV3 Financial Services offers for DSCR borrowers

CV3 provides DSCR loans for single-family rentals, 2-4 unit properties, and small multifamily assets. The platform also handles fix-and-flip and bridge financing, making it a useful option for investors who want to keep multiple deal types under one lending relationship. No personal income documentation is required to qualify.

Best fit for CV3 Financial Services

CV3 fits investors who want a direct lender with cross-product capability and are evaluating the best DSCR loan lenders that can also support short-term deals. It works particularly well for borrowers building a portfolio who want one lender familiar with their history and investment approach.

Lenders that see your full activity across multiple loan types often apply more favorable judgment when underwriting your next deal.

Rates, fees, and terms to expect

Rates typically run 8.25% to 10.5% in early 2026, with 30-year fixed terms available on qualifying rental properties. Loan minimums generally start around $100,000.

Underwriting focus and DSCR requirements

CV3 typically requires a minimum DSCR of 1.0 with credit scores starting at 660. LTV caps sit around 75% for most rental programs.

Questions to ask before you apply

- Does CV3 offer rate discounts for repeat borrowers or portfolio relationships?

- What prepayment penalty terms apply to your selected product?

- Can you lock your rate during the underwriting period?

7. Visio Lending

Visio Lending is a national direct lender built specifically for single-family rental investors. The company has funded over $3 billion in DSCR loans since its founding, which puts it among the more experienced platforms when evaluating the best DSCR loan lenders in the long-term rental space.

What Visio Lending offers for DSCR borrowers

Visio focuses on single-family and 2-4 unit rental properties with a straightforward income-based qualification process. No personal income verification is required, and the company offers both 30-year fixed and interest-only options on qualifying loans.

Best fit for Visio Lending

This lender works best for investors building long-term single-family rental portfolios who want a lender with a deep track record in exactly that asset class. If your portfolio runs on stabilized rentals rather than value-add plays, Visio's underwriting is well-calibrated for your deal type.

Lenders that specialize in one asset class tend to move faster and ask fewer redundant questions during underwriting.

Rates, fees, and terms to expect

Rates typically fall in the 8.0% to 10.25% range in early 2026 based on LTV and credit score. Loan amounts start at $100,000 with upper limits reaching $2 million on most programs.

Underwriting focus and DSCR requirements

Visio requires a minimum DSCR of 1.0 with credit scores starting at 680. LTV caps sit at 75% to 80% depending on property type and borrower profile.

Questions to ask before you apply

- Does your rental income cover the required DSCR at your target loan amount?

- What prepayment penalty terms apply to your chosen loan structure?

- Are interest-only terms available for your property type and credit tier?

8. RCN Capital

RCN Capital is a Connecticut-based direct lender that has been funding real estate investor loans since 2010. The company operates nationwide and positions itself among the best DSCR loan lenders for investors who want cross-product depth and a long track record in private lending.

What RCN Capital offers for DSCR borrowers

RCN Capital provides DSCR loans for single-family rentals, 2-4 unit properties, and small multifamily assets with no personal income verification required. The company also offers fix-and-flip, bridge, and new construction financing, which gives you a single lending relationship across multiple stages of a deal cycle.

Best fit for RCN Capital

This lender fits active investors who cycle between short-term and long-term strategies and prefer keeping their financing with one platform. If your business model moves between flipping and holding rentals, RCN's product range covers both without forcing you to establish a new lender relationship each time.

Investors who build a track record with a lender on bridge loans often receive more favorable treatment when transitioning those properties into DSCR financing.

Rates, fees, and terms to expect

Rates typically run 8.0% to 10.5% in early 2026, with 30-year fixed terms available on qualifying rental properties. Loan amounts generally start at $75,000 with ceilings reaching $2.5 million on most programs.

Underwriting focus and DSCR requirements

RCN Capital requires a minimum DSCR of 1.0 and a credit score of at least 660. LTV caps sit around 75% to 80% for standard rental properties, with stricter limits applying to certain asset types.

Questions to ask before you apply

- Does an existing relationship with RCN on other products improve your DSCR rate?

- What prepayment penalty structure applies to your selected term length?

- Can you qualify with a DSCR below 1.0 using a larger down payment?

Choosing your DSCR lender

Every lender on this list qualifies you based on property income rather than personal earnings, but the details underneath that shared feature vary in ways that directly affect your returns. Rates, prepayment penalties, minimum DSCR ratios, and LTV limits all shift the math on a deal, so the right lender depends on your credit profile, target property type, and how long you plan to hold.

Start by identifying the two or three lenders whose borrower profile and loan structure match your situation most closely, then compare rates on the same property scenario to get a true side-by-side picture. Working with a broker who has active relationships across multiple programs gives you access to the best DSCR loan lenders without shopping each one separately.

If you want hands-on guidance from a lender who actively invests in real estate, connect with David Roa to review your options before you apply.