Buy Investment Property In Chicago: Listings, Yields, Loans

Chicago remains one of the most accessible major metros for real estate investors. Median home prices sit well below cities like Los Angeles, Miami, and New York, while rental demand stays strong across dozens of neighborhoods. Whether you're buying your first duplex or adding a multi-unit building to an existing portfolio, the math here can actually work, if you know where to look and how to finance the deal.

But deciding to buy investment property in Chicago is just the starting line. You need to identify the right neighborhoods based on real rental yield data, understand what landlording looks like on the ground, and, critically, lock in financing that fits an investor's profile rather than a traditional homebuyer's. That last part is where most people hit a wall. Banks aren't always eager to fund investment deals, especially for buyers who rely on property income instead of W-2s.

That's the gap I work in. With over 25 years in mortgage lending and more than $150 million funded, including DSCR loans, hard money, and fix-and-flip financing, I help Chicago investors move from "interested" to closed. This guide breaks down current listings worth watching, the neighborhoods delivering the strongest yields, and the loan options that make each deal possible.

What to know before you buy in Chicago

When you decide to buy investment property Chicago offers real opportunity, but the city has specific factors that can quietly eat your returns if you skip the groundwork. Property taxes, landlord-tenant regulations, and neighborhood-level vacancy rates each affect your net operating income in ways that don't show up on a basic listing price comparison. Understanding these three areas before you make an offer saves you from deals that look good on paper but perform poorly in practice.

Chicago property taxes will test your underwriting

Cook County property taxes rank among the highest in the country, and investment properties face steeper effective rates than owner-occupied homes. The county reassesses values every three years in a rolling cycle, and your tax bill can jump significantly after reassessment. Always pull the current tax bill from the Cook County Assessor's database and model a 15 to 20 percent increase into your projections for the next cycle.

If your deal only pencils out at the current tax rate, walk away. A reassessment could push you into negative cash flow within two years.

Triennial reassessment cycles mean you need to know which township your target property sits in and when it comes up next. That single variable has blindsided more investors than any other line item in this market.

Landlord-tenant law in Chicago is tenant-friendly

Chicago's Residential Landlord and Tenant Ordinance (RLTO) sets strict requirements around security deposit handling, required lease disclosures, habitability standards, and notice periods. Violating any of these rules exposes you to statutory damages and legal fees that can far exceed the rent you collected.

Before you close, budget for RLTO compliance costs upfront, including written disclosures, proper deposit accounts, and any required building inspections. For six-unit buildings and above, the Department of Buildings adds another layer of code requirements you need to price in.

Vacancy rates vary sharply by neighborhood

Average citywide vacancy runs roughly 5 to 7 percent, but that number hides wide variation at the neighborhood level. Logan Square, Pilsen, and Bridgeport consistently post lower vacancy due to steady demand from long-term residents and young professionals. Some areas further south show vacancy above 10 percent, which means more months of lost rent baked into your annual return.

Run your numbers using a conservative vacancy assumption of 8 to 10 percent for any neighborhood where you don't yet have operating history. Once you have 12 months of actual data from your own building, you can revisit that figure and adjust.

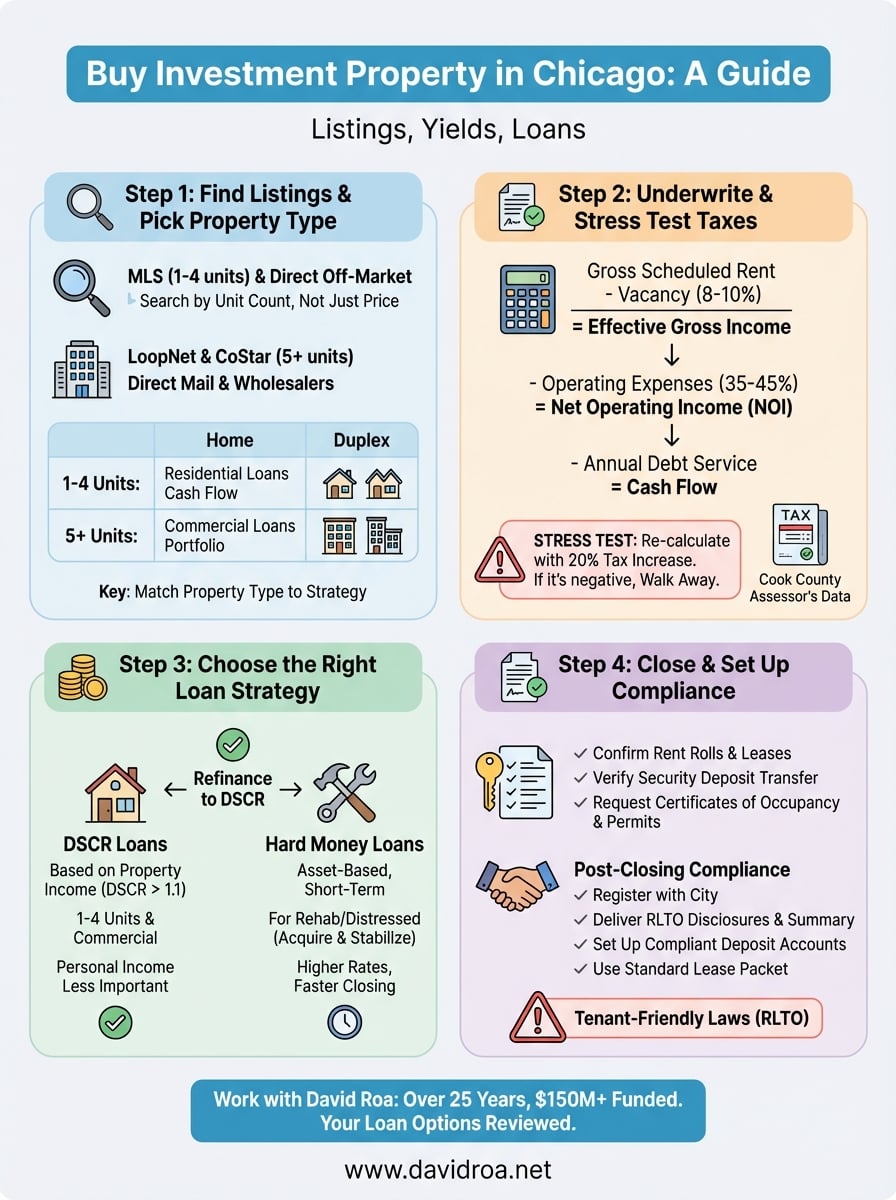

Step 1. Find listings and pick your property type

When you decide to buy investment property Chicago has no shortage of inventory, but not all listings market directly to investors. Most MLS databases mix owner-occupied homes with income properties, so search by unit count rather than by price alone. Flag any listings that include current rent rolls or tenant information, because those details tell you far more about actual performance than the listing price ever will.

Where to search for Chicago investment listings

The MLS through a buyer's agent gives you the broadest access, but you should also work direct off-market channels. Many Chicago multi-unit deals, especially two-to-four flats in neighborhoods like Pilsen, Bridgeport, and Albany Park, trade without hitting public listings at all.

Ask your agent to set a saved search specifically for two-to-six unit buildings in your target neighborhoods, not just "multi-family," because MLS classifications vary by listing agent.

Here are the main sources worth running in parallel:

- MLS (via a buyer's agent): Best for two-to-four unit buildings where residential financing still applies

- LoopNet and CoStar: Focused on commercial and five-plus unit properties

- Direct mail to owners: Targets off-market sellers in high-demand zip codes

- Wholesalers: Access to distressed properties, typically requiring cash or hard money

Match the property type to your strategy

Your financing options shift significantly depending on whether you buy a one-to-four unit building or a five-plus unit property. Buildings with four or fewer units qualify for conventional and DSCR residential loans. Five or more units move into commercial loan territory, which changes your down payment requirements, rate structure, and underwriting criteria entirely.

Use this table to match your goals to the right property type before you submit any offers:

| Property Type | Units | Best For | Typical Loan |

|---|---|---|---|

| Single-family | 1 | First-time investors | Conventional, DSCR |

| Two-to-four flat | 2-4 | House hackers, cash flow | FHA (owner-occ), DSCR |

| Small apartment | 5-10 | Portfolio builders | Commercial bridge, DSCR |

| Mixed-use | Varies | Business plus rental income | Commercial, SBA |

Step 2. Underwrite the deal and stress test taxes

Before you buy investment property Chicago requires more rigorous underwriting than most other markets because property taxes and operating costs here are not negotiable line items you can trim later. Run your numbers on actual rent rolls, not asking rents, and build your model before you submit an offer, not after inspection.

Build your cash flow model from gross rent down

Start with gross scheduled rent, then subtract vacancy, operating expenses, and debt service to arrive at your real cash flow. A clean model catches deals that look strong at the asking price but collapse once you account for actual costs.

Use this template as your baseline:

| Line Item | Example Figure |

|---|---|

| Gross Scheduled Rent (annual) | $36,000 |

| Vacancy (8%) | - $2,880 |

| Effective Gross Income | $33,120 |

| Operating Expenses (35%) | - $11,592 |

| Net Operating Income (NOI) | $21,528 |

| Annual Debt Service | - $16,800 |

| Cash Flow | $4,728 |

Thirty-five percent for operating expenses is a reasonable baseline for a two-to-four flat in Chicago. Older buildings or those with deferred maintenance will run closer to 40 to 45 percent, so adjust accordingly based on the inspection report.

Stress test your numbers against a tax reassessment

Once you have your base model, run a second scenario with property taxes increased by 20 percent. Pull the current bill from the Cook County Assessor's public database, apply that increase, and recalculate your NOI and cash flow.

If the deal still cash flows at the higher tax figure, you have a real margin of safety. If it goes negative, the current price does not support your investment.

A deal that survives the tax stress test is worth pursuing to the next stage. One that fails it is telling you the seller needs to come down on price before the numbers work in your favor.

Step 3. Choose the right loan for your strategy

When you buy investment property Chicago offers several loan structures, and picking the wrong one can compress your cash flow before the first tenant signs a lease. Your loan type controls your down payment, rate, and qualification criteria, so lock in your financing strategy before you start making offers, not after you find a property you want.

DSCR loans work for most rental strategies

DSCR (Debt Service Coverage Ratio) loans qualify you based on the rental income the property generates rather than your personal tax returns or W-2 statements. If the property earns enough rent to cover its debt service, you qualify. Most lenders require a DSCR of 1.1 or higher, meaning the property brings in at least 10 percent more than the monthly debt payment costs.

A DSCR loan is the most practical tool for investors who own multiple properties or are self-employed, because your personal income documentation does not drive the approval decision.

DSCR products cover one-to-four unit buildings and extend into commercial structures for five-plus unit properties. Rates run modestly higher than conventional loans, but the underwriting flexibility makes this the default choice for most Chicago rental investors.

Hard money loans fit short-term acquisition plays

Hard money lending uses the property's asset value as collateral rather than your credit profile or income history. If you plan to acquire a distressed building, renovate it, and then refinance or sell, hard money gives you fast access to capital, often closing in under two weeks. The trade-off is higher short-term rates and repayment windows of 12 to 24 months.

Acquire and stabilize the property using hard money, then refinance into a long-term DSCR loan once you have a documented rent roll and at least 90 days of operating history.

Step 4. Close and set up landlord compliance

Once you buy investment property Chicago marks you as a landlord the moment you close, and your compliance obligations start on day one, not when you find your first tenant. Chicago requires specific registrations, disclosures, and physical building standards before you can legally collect rent. Missing any of these steps exposes you to fines and tenant claims that can drain cash flow faster than a vacant unit.

What to review before closing day

Your final walkthrough and closing checklist should cover more than just the physical condition of the building. Verify the existing rent rolls match the signed leases, confirm all security deposits transfer to you at closing, and request the seller's current Certificate of Occupancy from the City of Chicago.

If the seller cannot produce proof of compliant deposit handling under the RLTO, negotiate a credit at closing rather than assuming liability for their prior practices.

Run through this checklist before you sign:

- Confirm rent roll matches signed leases for each occupied unit

- Verify security deposits transfer to a separate interest-bearing account in your name

- Request all open building permits and inspection reports

- Confirm property tax escrow setup with your lender

Register your rental unit and deliver required disclosures

Chicago landlords must register multi-unit buildings with the City and provide tenants with a copy of the Chicago RLTO summary, a city-approved disclosure document, within the first 10 days of a new tenancy. You can download the required disclosure directly from the City of Chicago's official website at chicago.gov.

New leases and renewal notices must also include your contact information and the name and address of anyone authorized to manage the property. Build a standard lease packet that includes all required disclosures so every tenancy starts in full compliance and reduces your exposure to statutory damages under the RLTO.

Next Steps

When you decide to buy investment property Chicago rewards the investors who do the preparation work upfront. Use the cash flow model from Step 2 on every deal, and run the tax stress test before you submit any offer. You now have a complete framework covering listings, underwriting, loan selection, and landlord compliance, so you can move through each stage with a clear process rather than guessing as you go.

Your next move is locking in your financing structure before you start making offers. The loan type you choose controls your down payment, qualification criteria, and long-term cash flow from day one. Whether you need a DSCR loan, hard money, or commercial financing, matching the right product to your strategy is what separates closed deals from ones that fall apart at the finish line.

Work with David Roa to get your loan options reviewed by a lender with over 25 years in investment financing and more than $150 million funded across residential, commercial, and investor deals.