Cash Out Refinance vs HELOC: Costs, Rates, And Best Use

You've built equity in your home, and now you want to put it to work. Maybe it's a renovation, debt consolidation, or funding an investment property. The question most homeowners land on is cash out refinance vs HELOC, two products that tap the same asset but work in completely different ways. Choosing the wrong one can cost you thousands in unnecessary interest or lock you into terms that don't match your goals.

The differences go beyond just rates. Each option carries its own fee structure, repayment timeline, and impact on your existing mortgage. A cash-out refinance replaces your current loan entirely, while a HELOC acts as a revolving credit line on top of it. The right pick depends on how much you need, how fast you need it, and what your current mortgage rate looks like.

With over 25 years in mortgage lending and more than $150 million funded, I've walked homeowners, investors, and business owners through this exact decision hundreds of times. At David Roa, we structure these loans daily, from straightforward primary residences to complex investor scenarios using DSCR and renovation financing. This guide breaks down the costs, rates, and best use cases for each option so you can make a confident, informed choice.

Why this choice matters when you tap home equity

When you access your home equity, you're not just borrowing money. You're restructuring a significant financial obligation that can follow you for decades. The decision between cash out refinance vs HELOC isn't just a rates comparison. It changes your monthly payment, your tax exposure, and your cash flow flexibility going forward. Getting it wrong doesn't just cost you money short term; it can constrain your financial options for years.

Your existing mortgage rate changes everything

The rate at which you originally locked your mortgage directly impacts which option makes sense today. If you secured a 30-year fixed mortgage at 3.5% and current rates sit above 6%, a cash-out refinance forces you to replace that low-rate loan with a higher-rate one on your entire balance. That can add hundreds of dollars to your monthly payment even if you only needed $50,000 in cash. A HELOC, in that scenario, lets you keep your original loan intact and borrow only what you need as a separate line.

If your current mortgage rate is well below today's market, a cash-out refinance will almost always cost you more over time than a HELOC, regardless of the HELOC's variable rate.

On the other hand, if you locked in a higher rate during a peak period and rates have since dropped, a cash-out refinance can make strong financial sense. You lower your mortgage rate, consolidate debt, and pull cash out all in one streamlined transaction, which can produce real monthly savings.

The wrong product can create cash flow problems

A HELOC gives you a draw period, typically 10 years, during which you can borrow and repay as needed. But when that period ends, the repayment phase kicks in and your payments can increase substantially. Homeowners who treat a HELOC like a long-term fixed loan often get caught off guard when their monthly obligation shifts. If you're using the funds for a single, defined purpose like a full home renovation, a cash-out refinance with a fixed repayment schedule removes that uncertainty entirely.

Your spending pattern also matters here. A HELOC works best when you need funds in phases, such as staging a fix-and-flip project or funding a business across multiple draws. Pulling a large lump sum at once from a HELOC means you're paying interest on the full draw immediately, which often eliminates any rate advantage it had over a cash-out refi in the first place.

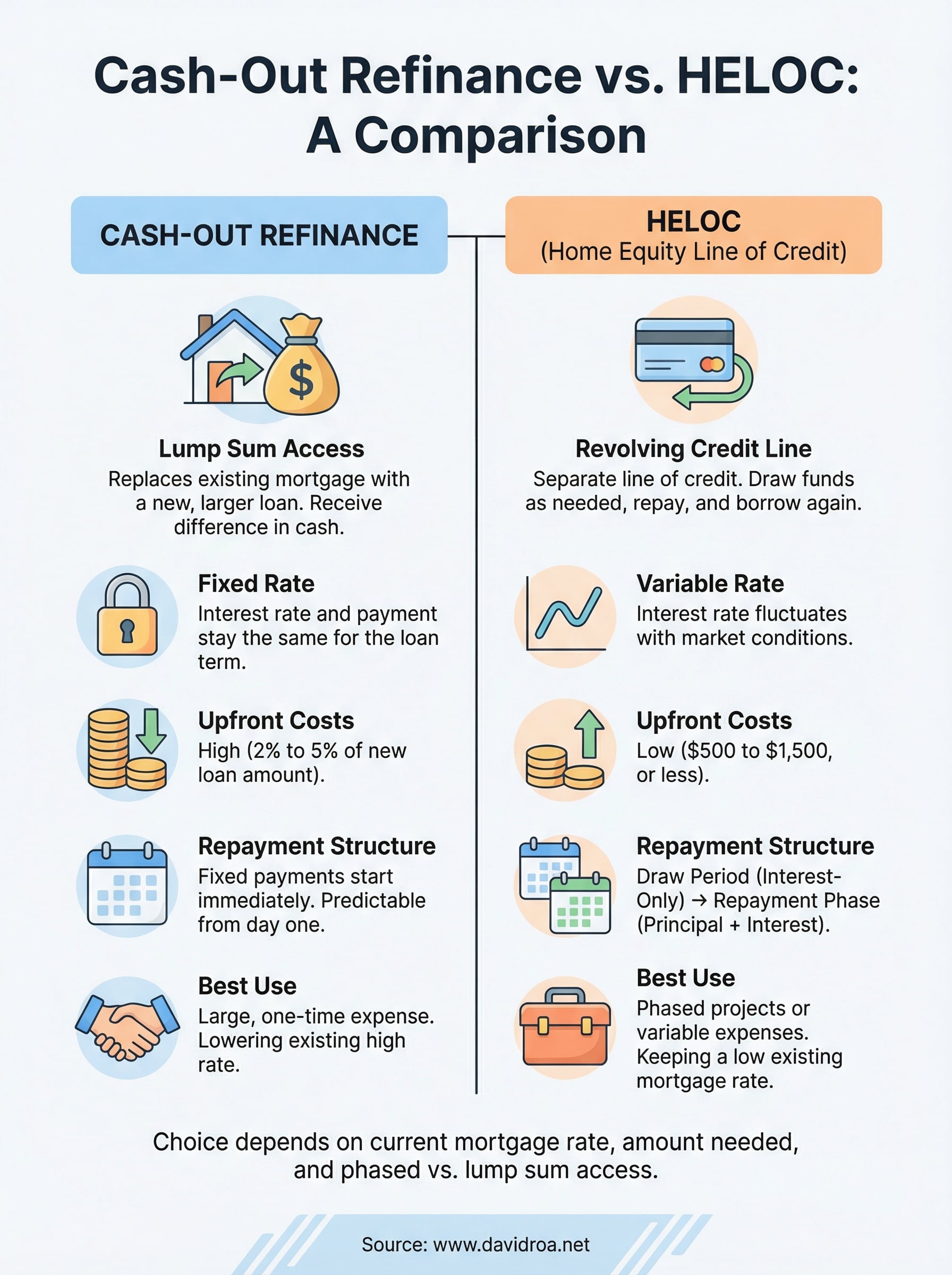

How a cash-out refinance works

A cash-out refinance replaces your existing mortgage with a brand-new, larger loan. The difference between the new loan amount and your current balance goes directly to you as cash at closing. If your home is worth $400,000 and you owe $200,000, you might refinance into a $280,000 loan and walk away with $80,000 in hand, minus closing costs.

What the lender evaluates

Lenders assess your loan-to-value ratio (LTV) to determine how much you can borrow. Most conventional lenders cap cash-out refinances at 80% LTV, meaning you need to retain at least 20% equity after closing. Your credit score, income, and debt-to-income ratio also shape the approval decision and the rate you receive.

Here are the key factors lenders review during underwriting:

- LTV ratio: Most programs require you to keep at least 20% equity post-closing

- Credit score: 620 minimum for conventional loans; 680 or higher gets better pricing

- DTI ratio: Most lenders want total monthly debts below 45% of gross income

- Home appraisal: An independent appraisal confirms the current market value of your property

What closing costs look like

A cash-out refinance carries the same closing costs as a standard mortgage. You're typically looking at 2% to 5% of the new loan amount, covering appraisal fees, title insurance, origination charges, and other lender costs. On a $280,000 loan, that's $5,600 to $14,000 out of pocket or rolled into your new balance. This cost structure is one of the sharpest differences in the cash out refinance vs HELOC comparison, which is why the product makes the most financial sense when you need a large lump sum or can reduce your existing rate at the same time.

A cash-out refinance only pencils out if the total cost of resetting your mortgage is outweighed by the cash you receive or the rate improvement you lock in.

How a HELOC works

A HELOC, or home equity line of credit, gives you access to a revolving credit line secured against your home's equity. Rather than receiving a lump sum like a cash-out refinance, you draw funds as you need them, repay them, and borrow again within your approved limit. When comparing cash out refinance vs HELOC options, this flexible access structure is often the defining factor for homeowners who don't need all their cash at once.

The draw period and repayment phase

A HELOC operates in two distinct phases. During the draw period, which typically runs 10 years, you can borrow and repay freely. Most lenders only require interest payments on what you've actually drawn, not on the full credit line. That keeps your initial payments low while giving you on-demand access to capital for phased projects or variable expenses.

Once the draw period ends, the repayment phase begins and your payments shift to cover both principal and interest, which can increase your monthly obligation significantly.

After the draw period closes, the repayment phase begins, typically lasting 10 to 20 years. At this point, you can no longer draw funds and must repay the outstanding balance. Many borrowers underestimate how much their payment can jump at this transition, which is why understanding both phases before signing is critical.

What lenders evaluate for a HELOC

Lenders review similar criteria as a cash-out refinance, but HELOC approval often requires a stronger credit profile given the revolving nature of the product. Most lenders want to see the following:

- LTV ratio: Typically capped at 85% combined loan-to-value across your first mortgage and HELOC

- Credit score: Most lenders look for 680 or higher for competitive rates

- DTI ratio: Below 43% is standard for most HELOC approvals

- Equity position: You generally need at least 15% to 20% equity remaining after the line is established

Costs, rates, and repayment differences

The cost gap between these two products is one of the clearest factors in the cash out refinance vs HELOC decision. A cash-out refinance typically carries 2% to 5% in closing costs on the full loan amount, while a HELOC usually runs $500 to $1,500 in upfront fees, sometimes even less. That difference alone can make a HELOC the cheaper entry point when you need a smaller amount or want to avoid a large upfront expense.

The lower upfront cost of a HELOC can disappear fast if rates rise and you're carrying a large balance through the repayment phase.

Rate structure and what drives your cost

Cash-out refinances almost always come with a fixed interest rate, which means your rate and payment stay the same for the life of the loan. HELOCs, by contrast, carry variable rates tied to the prime rate, which means your cost can rise or fall with market conditions. If the Federal Reserve increases rates, your HELOC payment goes up. That unpredictability is a real risk when you're carrying a large balance over several years.

Some lenders offer the option to convert a portion of your HELOC balance to a fixed rate, which adds some protection. But that conversion typically comes with fees, and it doesn't apply to the entire line unless you request it specifically.

Repayment timelines

With a cash-out refinance, your repayment starts immediately and runs for the full loan term, usually 15 or 30 years. The payment is predictable from day one. A HELOC works differently. During the draw period, you often pay interest only on what you've borrowed. Once repayment kicks in, you pay principal plus interest on the full outstanding balance, which can produce a meaningful payment increase.

How to choose between a cash-out refi and a HELOC

The best way to frame the cash out refinance vs HELOC decision is to start with two questions: what is your current mortgage rate, and how do you plan to use the funds? Those two factors will point you toward the right product faster than any rate comparison alone.

When a cash-out refinance makes more sense

A cash-out refinance works best when you need a large, one-time lump sum and your current mortgage rate sits at or above today's market rates. If you can lower your existing rate while pulling cash out, you get a double benefit in one transaction. This option also fits well when you want a fixed, predictable payment and prefer not to manage a revolving credit line with a variable rate that can shift with market conditions.

When a HELOC makes more sense

Choose a HELOC when you need flexible, phased access to capital and your current mortgage rate sits well below today's market. Drawing funds in stages, paying down the balance, and borrowing again makes a HELOC the stronger tool for multi-phase projects or ongoing business expenses. The lower upfront cost also gives you an advantage when you're not certain exactly how much you'll need from the start.

If you're unsure which product fits your situation, the deciding factor is almost always your current mortgage rate compared to today's rates.

Here's a quick comparison to help you decide:

| Factor | Cash-Out Refinance | HELOC |

|---|---|---|

| Rate type | Fixed | Variable |

| Best for | Large lump sum | Phased draws |

| Upfront cost | High (2% to 5%) | Low ($500 to $1,500) |

| Payment structure | Fixed from day one | Interest-only during draw period |

| Existing mortgage | Replaced entirely | Kept intact |

A simple next step

The cash out refinance vs HELOC decision comes down to three things: your current mortgage rate, how much you need, and whether you want phased access or a single lump sum. Neither product is universally better. The right one depends entirely on your specific numbers and goals.

Running the comparison on paper is a useful starting point, but the real clarity comes from talking through your actual loan balance, rate, and equity position with someone who structures these products every day. Small differences in rate, timing, or draw strategy can shift the total cost by thousands of dollars over the life of the loan.

If you're ready to see which option fits your situation, reach out to David Roa for a direct conversation. With 25 years of mortgage experience and over $150 million funded, you get straightforward guidance built around your numbers, not a generic recommendation.