Cash-Out Refinance vs Home Equity Loan: Which Saves More?

You've built equity in your home, and now you want to put it to work. Maybe it's a kitchen renovation, paying off high-interest debt, or funding an investment property. Whatever the reason, you're likely weighing cash out refinance vs home equity loan, two of the most common ways to access your home's value. Both let you borrow against what you own, but they work very differently when it comes to rates, repayment structure, and long-term cost.

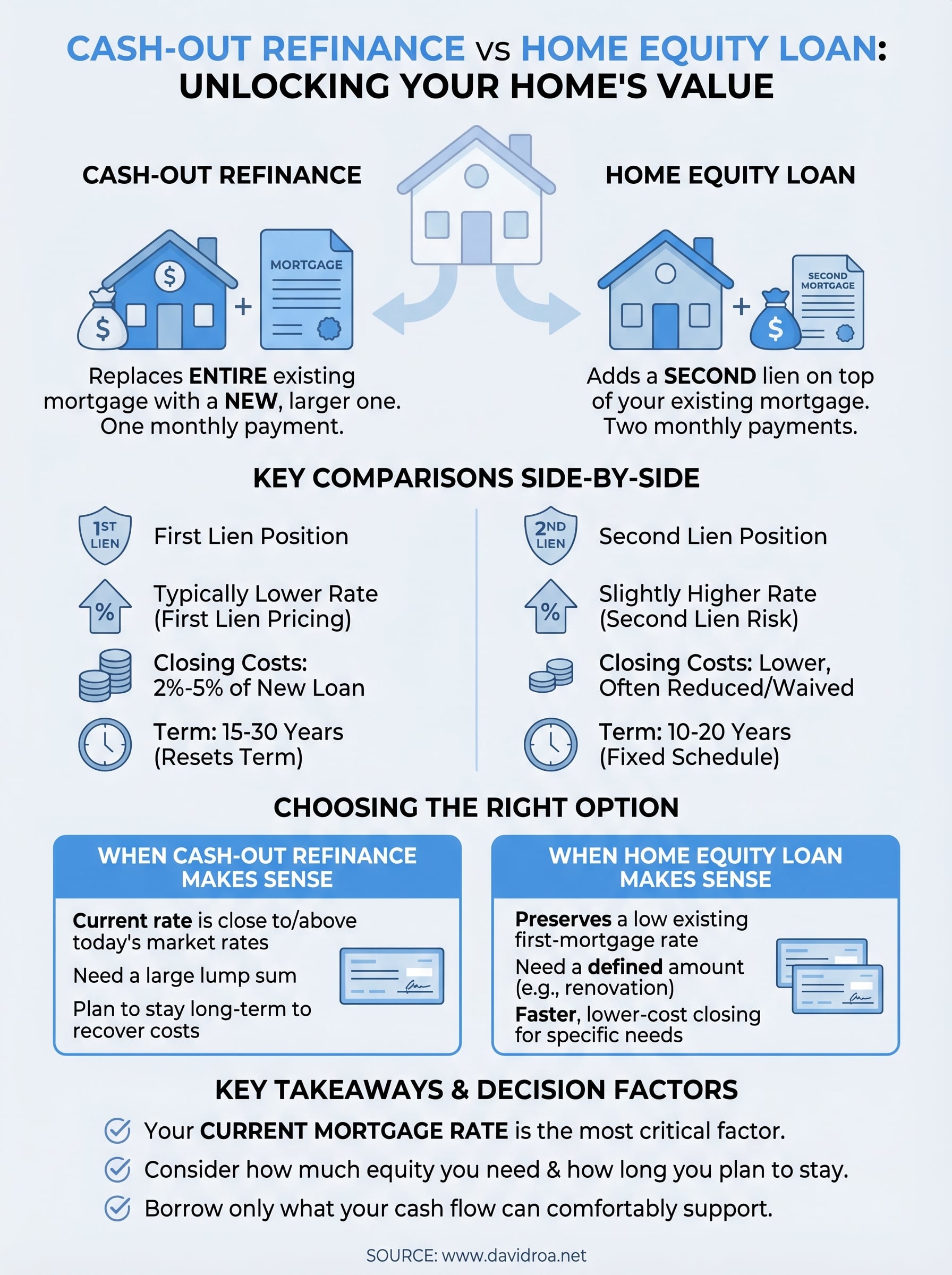

Choosing the wrong option can mean thousands of dollars left on the table over the life of your loan. A cash-out refinance replaces your entire mortgage with a new, larger one. A home equity loan adds a second lien on top of your existing mortgage. The right move depends on your current rate, how much equity you have, and what you plan to do with the funds, details that change the math significantly from one borrower to the next.

With over 25 years in mortgage lending and more than $150 million funded, I've walked homeowners through this exact decision hundreds of times at David Roa. This guide breaks down the real differences between these two products, costs, interest rates, closing fees, and loan terms, so you can figure out which one actually saves you more money. No fluff, just a straightforward comparison built on what I see work for borrowers every day.

Why this choice matters when you tap home equity

When you decide to pull equity out of your home, you're not just picking a loan product. You're restructuring your debt, and the structure you choose affects your monthly payment, your total interest paid, and how long you carry that balance. The decision between a cash out refinance vs home equity loan carries real financial weight, and a misstep here can cost you more than the project or investment you're funding in the first place.

The difference between these two products often comes down to your current mortgage rate and how much equity you've accumulated, factors that shift the math entirely.

Your existing mortgage rate is the starting point

The rate on your current mortgage is the single most important variable in this comparison. If you locked in a 3% or 4% rate several years ago, a cash-out refinance forces you to replace that loan with a new one at today's higher rates, which can push your monthly payment up significantly. Your break-even point on the refinance moves further out, and in many cases, a home equity loan preserves your low first-mortgage rate while still getting you the cash you need.

On the flip side, if you bought your home when rates were high and they've since dropped, refinancing into a lower rate while pulling cash out can make strong financial sense. You'd reduce your monthly payment and access funds at the same time. Knowing your current rate, and comparing it honestly to today's market, is the first calculation you should run before looking at anything else.

How much equity you have changes your options

Lenders typically require you to keep at least 20% equity in your home after either transaction. So if you own a $400,000 home and owe $300,000, you have $100,000 in equity but only about $20,000 available to borrow while staying above that 80% loan-to-value threshold. The more equity you hold above that floor, the more flexibility you get in choosing between products and negotiating terms.

Home equity loans are often capped at a combined loan-to-value of 85% to 90%, depending on the lender. Cash-out refinances follow similar rules. Understanding exactly where you stand on equity and LTV before you apply saves you from going deep into a loan process only to find the numbers don't work for your situation.

The purpose of the funds should drive the decision

What you plan to do with the money matters more than most borrowers realize. Short-term needs, like a single renovation project with a defined budget, often align better with a home equity loan's fixed lump sum and predictable repayment schedule. Long-term strategies, like funding a rental property acquisition or consolidating a large amount of high-interest debt, may justify the higher closing costs of a cash-out refinance if the rate and cash access make sense over time.

Matching the loan structure to your actual goal keeps you from overborrowing, locking in the wrong term, or paying closing costs that don't match the value you get from the transaction. Purpose drives product, not the other way around.

What a cash-out refinance is and how it works

A cash-out refinance replaces your existing mortgage with a new, larger loan that pays off your old balance and delivers the difference to you in cash at closing. You end up with one mortgage, one monthly payment, and a lump sum you can use however you choose. The lender places this new loan in first lien position, giving it the same standing as your original mortgage.

How the new loan replaces your old one

When you apply, the lender evaluates your home's current appraised value, your remaining balance, and your income and credit much like they did when you first purchased the property. If your home is worth $500,000 and you owe $300,000, you could borrow up to $400,000 at 80% LTV, putting $100,000 in your pocket after clearing the existing loan. That new loan becomes your only mortgage, repaid over a fresh term of 15 or 30 years.

Because a cash-out refinance resets your loan term, you may pay significantly more in total interest even if the new rate looks competitive on paper.

Keeping this in mind makes the cash out refinance vs home equity loan comparison more concrete. If your original loan carried a 3.5% rate and today's market sits at 6.5%, your monthly payment jumps on both the higher balance and the higher rate, sometimes by several hundred dollars each month.

What you pay to close and carry the loan

Closing costs on a cash-out refinance typically fall between 2% and 5% of the new loan amount, covering the appraisal, title work, origination fees, and recording charges. On a $400,000 loan, you're looking at $8,000 to $20,000 due at closing, though some lenders allow you to roll those costs into the loan balance.

Beyond closing, your ongoing interest rate will run slightly higher than a standard rate-and-term refinance because lenders price cash-out loans as carrying more risk. That rate difference is usually small, but it compounds over a 30-year term and should factor into your total cost calculation before you commit.

What a home equity loan is and how it works

A home equity loan lets you borrow a fixed lump sum against the equity you've built in your home without touching your existing mortgage. It sits in second lien position, meaning your original loan stays exactly as it is, with its current rate and payment schedule intact. You receive the funds at closing, then repay the home equity loan on a separate fixed schedule, typically over 10 to 20 years.

How the second lien structure works

Because the home equity loan is a second lien, the lender takes on more risk than the holder of your first mortgage. If you default and the property goes to foreclosure, the first lien gets paid before the second one sees anything. Lenders price that risk into the interest rate, which is why home equity loan rates typically run higher than first-mortgage rates. That said, they're usually lower than unsecured personal loans or credit cards, making them a competitive option when you need a defined amount of cash for a specific purpose.

Keeping your first mortgage untouched is the core advantage of a home equity loan, especially when your existing rate sits well below today's market.

What closing costs and repayment look like

Closing costs on a home equity loan are considerably lower than on a cash-out refinance, generally running between 2% and 5% of the loan amount, and many lenders offer programs with reduced or no closing costs in exchange for a slightly higher rate. Your monthly payment is fixed from day one, so you know exactly what you owe each month for the life of the loan.

In the cash out refinance vs home equity loan comparison, this predictability works in the home equity loan's favor for borrowers who need a specific amount and want a clean repayment timeline. You're not resetting a 30-year clock or absorbing thousands in closing costs just to access funds you've already earned through years of mortgage payments and property appreciation.

Costs, rates, taxes, and risks side by side

Putting the cash out refinance vs home equity loan decision into a single view makes the trade-offs easier to act on. Each product carries a distinct cost structure, and understanding both before you apply keeps you from choosing an option that looks attractive upfront but costs more over the life of the loan.

Interest rates and closing costs

Interest rates on cash-out refinances follow first-mortgage pricing, which typically runs lower than second-lien products. Home equity loans carry slightly higher rates because they sit in second position and represent more risk to the lender. That spread usually lands between 0.5% and 1.5%, depending on your credit score, LTV, and current market conditions.

| Factor | Cash-Out Refinance | Home Equity Loan |

|---|---|---|

| Lien position | First | Second |

| Typical rate | Lower (first-lien pricing) | Slightly higher (second-lien) |

| Closing costs | 2%–5% of new loan amount | 2%–5%, often reduced or waived |

| Loan term | 15–30 years (resets term) | 10–20 years |

| Monthly payments | One payment on new balance | Two payments: existing + new |

Closing costs on a refinance apply to the full new loan balance, which amplifies the dollar amount fast. On a $350,000 cash-out loan, 3% in closing costs runs $10,500. A $75,000 home equity loan at 3% costs roughly $2,250 to close, making it the lower out-of-pocket entry point when you only need a defined amount.

Tax implications and risk exposure

The IRS allows you to deduct mortgage interest on funds used to buy, build, or substantially improve your home, and this rule applies to both products, subject to current loan limits. If you pull cash out for debt consolidation or personal expenses, that deduction no longer applies. Talk to a tax professional before assuming either option delivers a write-off, because the use of funds controls eligibility entirely.

Using home equity for purposes other than home improvement disqualifies the interest deduction under current IRS rules, and that changes your real after-tax cost.

Both products use your home as collateral, so default carries the same consequence: you risk losing the property. A cash-out refinance ties that exposure to your entire outstanding balance, while a home equity loan limits it to the second-lien amount. Borrow only what your cash flow can comfortably support.

How to choose the option that saves you more

The right call between cash out refinance vs home equity loan depends on three numbers: your current mortgage rate, the amount you need, and how long you plan to stay in the home. Run those numbers honestly before you commit to either path, because the product that looks cheaper at signing can easily become the more expensive one over a 15 or 20-year repayment window.

If your current mortgage rate sits more than 1% below today's market, preserving that rate with a home equity loan almost always saves you more money over time.

When a cash-out refinance makes more sense

If today's rates are close to or below your current rate, a cash-out refinance gives you a single monthly payment and access to a larger equity pool in one transaction. This option also works well when you need a substantial amount, say $150,000 or more, because the closing cost percentage stays proportional while the rate advantage compounds over a long term.

Consider a cash-out refinance when you match these conditions:

- Your current rate is at or above today's market rates

- You need a large lump sum that would push a home equity loan to a very high balance

- You plan to stay in the home long enough to recover closing costs through monthly savings

When a home equity loan makes more sense

Choosing a home equity loan protects a low first-mortgage rate you can't replicate in today's market. If you locked in below 5% and only need $50,000 to $100,000 for a renovation or investment, keeping your first loan intact and adding a fixed second payment almost always costs less in total interest than resetting your entire mortgage balance at a higher rate.

A home equity loan also gives you a faster, lower-cost path to closing when you need funds on a tighter timeline. Fewer documents, smaller fees, and a shorter process make it the practical choice for borrowers who have a specific, defined need and want to avoid a full underwriting cycle on their primary mortgage.

Key Takeaways and Next Steps

The cash out refinance vs home equity loan decision comes down to your current rate, the amount you need, and how long you plan to stay in the home. If your existing mortgage rate sits well below today's market, a home equity loan protects that advantage while giving you access to funds. If today's rates match or beat your current rate, a cash-out refinance consolidates everything into one payment and may lower your monthly costs over time.

Both products use your home as collateral, so borrow only what your cash flow can comfortably support. Match the loan structure to your actual goal, factor in closing costs, and calculate total interest before you sign anything. The option that looks cheapest at closing is not always the one that saves you the most over a 15 or 20-year repayment window.

Ready to run the real numbers on your situation? Connect with David Roa for a direct comparison built around your rate, equity position, and goals.