Commercial Real Estate Loan Requirements: 2026 Checklist

Getting approved for a commercial property loan is a different game than qualifying for a residential mortgage. The underwriting is more complex, the documentation is heavier, and the stakes are higher. If you're searching for commercial real estate loan requirements, you're probably getting ready to buy an office building, retail space, warehouse, or mixed-use property, and you want to know exactly what lenders expect before you apply. Smart move.

Whether you're a first-time commercial buyer or an experienced investor expanding your portfolio, lenders in 2026 are looking at a specific set of financial benchmarks, property metrics, and paperwork. Miss one piece, and your deal can stall for weeks, or fall apart entirely. That's the reality I've seen repeatedly across over 25 years of originating loans and funding more than $150 million in deals through my brokerage, David Roa.

This checklist breaks down every major requirement, credit scores, down payments, DSCR thresholds, entity documentation, and more, so you can walk into the process prepared and close on your timeline.

Why commercial loan requirements matter in 2026

The commercial lending market in 2026 looks materially different than it did even three years ago. Interest rates have stayed elevated compared to the historically low environment borrowers enjoyed in the early 2020s, and lenders have tightened their underwriting criteria across the board. Understanding the full scope of commercial real estate loan requirements before you apply isn't just helpful; it's the difference between a fast approval and a frustrating stall that costs you the deal.

The rate and liquidity environment

Since the Federal Reserve's aggressive rate cycle, commercial lenders have recalibrated their risk models significantly. Debt service coverage ratios that used to pass at 1.15x are now required to hit 1.25x or higher on most conventional commercial deals. Banks and credit unions are also holding more reserves and originating fewer speculative loans, which means they are more selective about which borrowers and properties they will commit to funding.

If your deal barely cleared the qualifying bar in 2022, run the updated numbers at current rates before you assume you'll qualify today.

Your net operating income now needs to carry more weight simply because the cost of debt is higher. A property generating the same rent it produced three years ago may no longer cover the debt service at today's rates. That's a math problem, not a lender problem, and you need to work through it before you submit anything.

Why preparation directly reduces your cost

Lenders price risk into every deal. When you walk into an application with complete documentation, a clean credit profile, and property metrics that line up with the lender's criteria upfront, you reduce their perceived risk. Lower perceived risk translates directly to better rate offers and fewer conditions or contingencies attached to your commitment letter.

Borrowers who show up unprepared, missing financial statements, unclear on their entity structure, or unsure about the property's income history, often get quoted higher rates or pushed into short-term bridge financing they never planned for. Taking time upfront to understand what lenders actually require puts you in a stronger position to negotiate terms and close on your timeline.

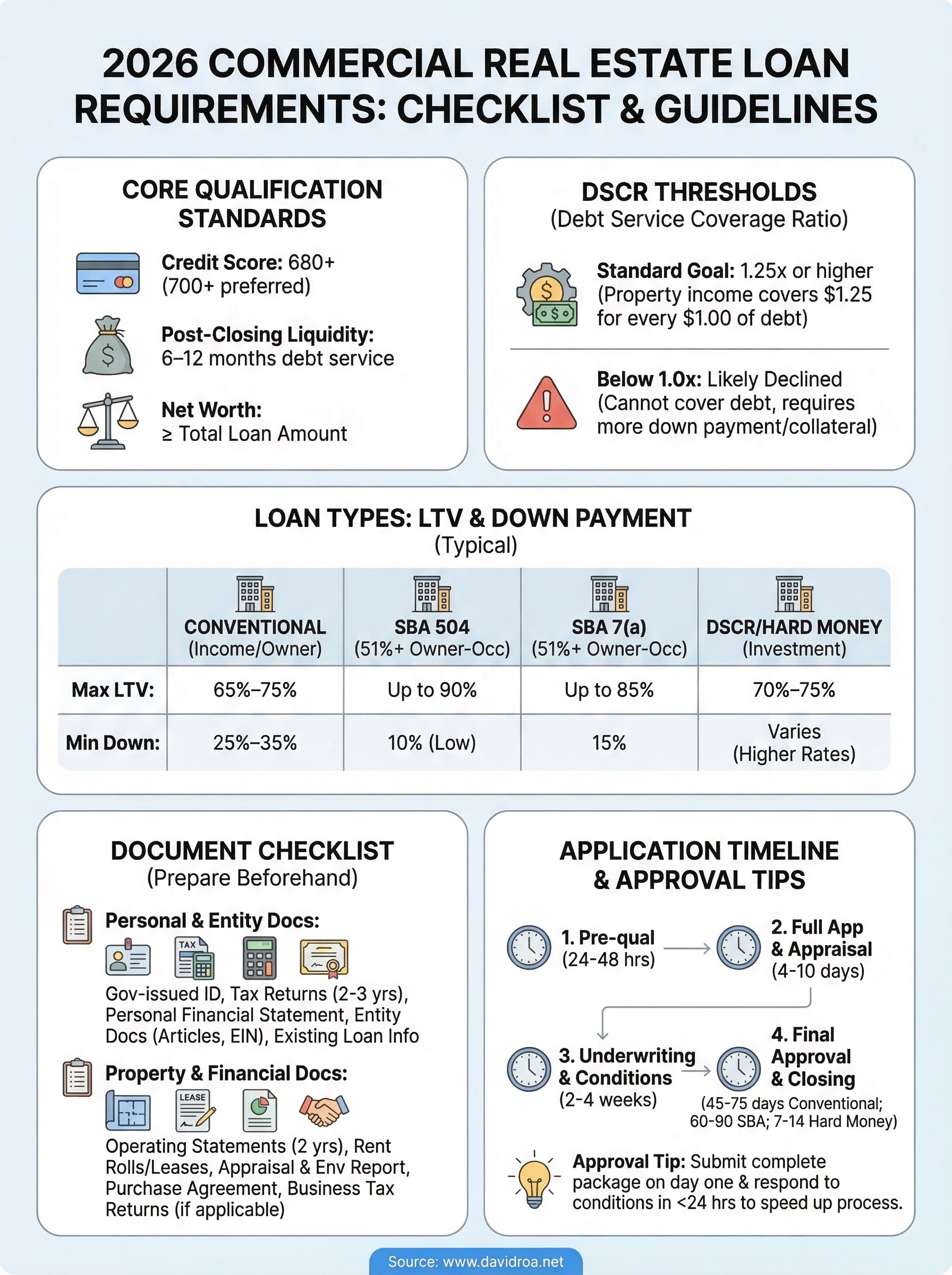

Core qualification standards lenders use

Every lender evaluates commercial real estate loan requirements through a consistent framework, regardless of the product you're pursuing. Before they review the property, they review you. Your credit profile, liquid reserves, and income documentation all determine whether a lender considers your file worth underwriting at competitive terms.

Credit score and net worth

Most conventional commercial lenders require a minimum credit score of 680, though scores above 700 open more programs and better pricing. Lenders also check your net worth and post-closing liquidity to ensure you can absorb setbacks after the deal closes. Generally, they want to see these minimums met:

- Credit score: 680+ (700+ preferred for conventional programs)

- Post-closing liquidity: 6 to 12 months of debt service in accessible accounts

- Net worth: Ideally equal to or greater than the total loan amount

Debt service coverage ratio

Your DSCR measures the property's net operating income against its total annual debt payments. A ratio above 1.25x is the standard threshold most lenders require in today's rate environment, meaning the property produces $1.25 for every $1.00 of loan payment owed. If your number falls below that mark, lenders typically require a larger down payment, a co-borrower, or additional collateral to offset the gap.

If your DSCR drops below 1.0x, most conventional lenders will decline the deal outright, no matter how strong your personal income appears on paper.

DSCR loan programs are also worth knowing as a standalone product. These programs qualify you based on the property's cash flow alone rather than personal tax returns, which makes them a practical tool for investors with significant business deductions pulling down their reported income.

Property and deal requirements by loan type

Not every property qualifies under every loan program, and the commercial real estate loan requirements shift significantly depending on which financing product you're pursuing. Understanding how lenders evaluate the deal structure alongside the property type saves you from wasting time applying to programs that simply won't work for your situation.

Conventional and SBA commercial loans

Conventional commercial loans typically require a minimum loan-to-value (LTV) ratio of 65% to 75%, meaning you bring 25% to 35% as a down payment. SBA 504 loans are slightly more flexible, allowing down payments as low as 10% for owner-occupied properties. Both programs require the property to be income-producing or owner-occupied, with stabilized occupancy generally above 85%.

| Loan Type | Max LTV | Min Down Payment | Occupancy Requirement |

|---|---|---|---|

| Conventional | 75% | 25% | 85%+ stabilized |

| SBA 504 | 90% | 10% | 51% owner-occupied |

| SBA 7(a) | 85% | 15% | 51% owner-occupied |

SBA loans require the borrower's business to occupy at least 51% of the property, which disqualifies purely investment-held commercial buildings from these programs entirely.

DSCR and hard money loans

DSCR loan programs qualify the deal based on property income rather than your personal tax returns, making them a strong fit for investors with complex financials. These programs accept LTVs up to 70% to 75% and focus primarily on whether the property's cash flow covers the debt payment without requiring W-2s or personal income documentation.

Hard money and bridge loans move faster but carry higher rates, typically 9% to 13%, and work best for short-term holds, fix-and-flip projects, or properties that don't yet qualify for conventional financing due to low occupancy or deferred maintenance.

Documents you need: 2026 checklist

Meeting the commercial real estate loan requirements for 2026 means showing up with a complete file on day one. Lenders move faster and offer better terms when they can underwrite your deal without chasing down missing paperwork. Organizing everything before you submit is one of the simplest ways to protect your timeline.

A disorganized submission signals risk to underwriters, even when your financials are strong.

Personal and entity documents

Your personal financial picture is the foundation every lender reviews first. Before they look at the property, they want to confirm who they're lending to and whether that borrower is financially stable. Have these ready before you initiate contact with any lender:

- Government-issued ID and any relevant visa or ITIN documentation

- Personal tax returns for the past two to three years

- Personal financial statement showing assets and liabilities

- Entity formation documents: articles of incorporation, operating agreement, EIN

- Any existing loan statements or schedule of real estate owned

Property and financial documents

Once your personal credentials are verified, lenders shift focus to the deal itself. They need to confirm that the property generates sufficient income to service the debt and that the purchase price reflects the asset's actual value. Prepare the following:

- Last two years of property operating statements or rent rolls

- Current lease agreements for all tenants

- Third-party appraisal and environmental report (Phase I minimum)

- Purchase and sale agreement

- Business tax returns if the property supports your operating business

Application timeline and approval tips

Understanding how long the process takes helps you protect your closing date and avoid surprises. Commercial loan timelines vary by product, but most conventional commercial deals close in 45 to 75 days from application to funding. SBA loans typically run 60 to 90 days due to the additional government review layer, while hard money and bridge loans can close in as few as 7 to 14 days when your file is clean.

What to expect at each stage

The process moves through predictable stages once you submit your application. Pre-qualification typically takes 24 to 48 hours and clarifies your borrowing power before you commit to a purchase price. After you submit a full application, underwriting runs 2 to 4 weeks on conventional programs while the lender orders the appraisal, reviews your financials, and clears conditions.

Delays almost always come from missing documents or appraisal scheduling, not from the lender's underwriting queue itself.

Here is a general timeline to plan around:

- Days 1 to 3: Pre-qualification and term sheet

- Days 4 to 10: Full application submission and appraisal order

- Days 11 to 35: Underwriting and condition clearing

- Days 36 to 75: Final approval, commitment letter, and closing

How to speed up approval

Knowing the full scope of commercial real estate loan requirements before you apply is the fastest path to a smooth closing. Submit your complete document package on day one rather than sending files in pieces as the lender asks. Respond to underwriter conditions within 24 hours whenever possible, because slow responses push your file back in the queue and add days to your timeline.

Next Steps

You now have a complete picture of commercial real estate loan requirements for 2026, covering credit scores, DSCR thresholds, loan types, and the exact documents lenders expect on day one. The smartest move right now is to audit your financial position against every standard covered in this guide before you contact a single lender.

Pull your credit reports, run your DSCR calculation using the property's actual income at current rates, and get your entity and tax documents organized into one clean package. Arriving prepared shortens your approval timeline and directly affects the rate and terms you receive. Deals stall when borrowers submit incomplete files, not because lenders are slow. If you have questions about a specific deal structure or loan program, getting an expert review early saves you from costly delays later.

Talk to a commercial lending expert at David Roa to walk through your scenario and find the right loan program for your goals.