Hard Money Lender Rates: Current Ranges, Points, And Terms

Whether you're flipping a property or need quick capital to close on an investment deal, understanding hard money lender rates is essential before you sign anything. These loans move fast and offer flexibility that banks can't match, but they come at a cost. Knowing what that cost looks like helps you run accurate numbers and avoid surprises that eat into your profits.

Most investors want straight answers: What interest rate should I expect? How many points will I pay upfront? What terms are standard versus predatory? These are the right questions, and the answers vary more than you might think. Rates depend on factors like loan-to-value ratio, property type, your exit strategy, and even the lender's own cost of capital.

With over 25 years funding real estate deals, including hard money and fix-and-flip loans, I've seen how rate structures directly impact investor returns. This article breaks down current hard money lender rates, explains the points and fees you'll encounter, and gives you the benchmarks you need to compare offers with confidence.

Why hard money lender rates matter

Hard money lender rates directly determine whether your investment deal generates profit or drains your capital. These interest charges compound quickly on short-term loans, and even a two-point difference in rate can swing a project from profitable to break-even. When you're holding a property for three to twelve months, the total interest cost becomes one of your largest expenses alongside renovation and holding costs.

Impact on your deal profitability

Your all-in financing cost includes both the interest rate and the upfront points charged at closing. A typical hard money loan at 10 percent interest plus 2 points means you pay $2,000 per $100,000 borrowed immediately, then $833 monthly in interest on that same amount. Extend your project timeline by just three months, and you've added $2,499 in carrying costs that eat directly into your flip margin.

The difference between a profitable flip and a financial loss often comes down to accurate rate calculations before you acquire the property.

Investors who underestimate their true cost of capital consistently overpay for properties because their initial analysis looked viable. You need to know your exact financing terms before making an offer, not after you've already committed to a deal that assumes cheaper money than what's actually available to you.

The speed-versus-cost tradeoff

Hard money rates run higher than conventional loans because lenders fund quickly and accept properties that banks reject. You're paying a premium for speed, flexibility, and asset-based underwriting that ignores credit scores and tax returns. This makes sense when timing matters: if you can close in seven days on a distressed property at 20 percent below market, the higher rate becomes irrelevant compared to the opportunity cost of missing the deal entirely.

However, this same speed can mask expensive terms if you don't compare multiple lenders. Some charge 12 to 15 percent with 3 to 4 points upfront, while others offer 9 to 11 percent with 2 points for similar loan-to-value ratios. Understanding standard market rates helps you spot outliers and negotiate better terms, especially when you bring strong exit strategies and verifiable experience to the table.

Current hard money rate ranges in 2026

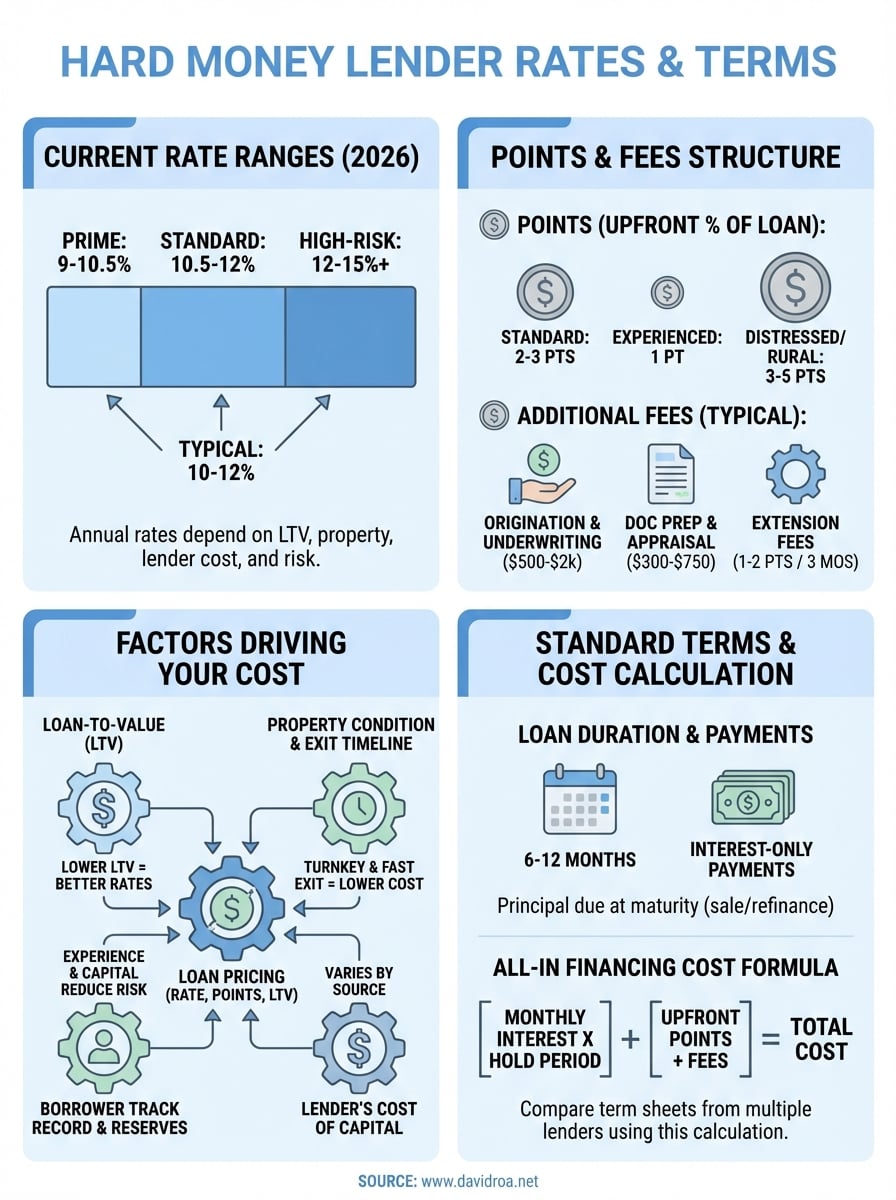

Hard money lender rates in 2026 typically fall between 9 and 15 percent annually, with most competitive lenders pricing deals in the 10 to 12 percent range for standard fix-and-flip scenarios. Your actual rate depends on your loan-to-value ratio, property condition, and the lender's own cost of funds. Lenders with institutional backing often charge less than private individuals funding deals from personal capital.

Typical interest rate brackets

You'll encounter three main pricing tiers based on your deal structure. Prime hard money loans with strong borrowers and clean properties sit at 9 to 10.5 percent, while standard investor deals run 10.5 to 12 percent. Higher-risk scenarios like vacant properties in tertiary markets or borrowers with recent foreclosures push rates to 12 to 15 percent or beyond.

Lenders price risk directly into your rate, so improving your loan-to-value ratio by 10 percent can drop your interest cost by 1 to 2 points.

Point structures you'll encounter

Upfront points represent percentages of your total loan amount paid at closing. Most lenders charge 2 to 3 points for conventional hard money deals, meaning you pay $2,000 to $3,000 per $100,000 borrowed before receiving funds. Some lenders offer 1-point options for experienced investors with multiple successful exits, while distressed or rural properties may carry 3 to 5 points to compensate for added risk. These points are non-refundable and separate from your interest charges, so you need to factor them into your total cost analysis from day one.

What drives your rate, points, and leverage

Lenders price your deal based on quantifiable risk factors that determine both your interest rate and the maximum loan-to-value ratio they'll approve. Understanding these variables helps you negotiate better terms and structure deals that qualify for competitive hard money lender rates. Each element below directly impacts the numbers on your term sheet.

Your loan-to-value ratio

The LTV percentage you request serves as the primary pricing lever for most lenders. Borrowing 65 percent of the after-repair value typically qualifies you for standard rates, while pushing to 75 or 80 percent adds 1 to 2 percentage points to your cost. Lenders view higher LTV as increased exposure because you have less equity cushion if the property value drops or your renovation timeline extends beyond projections.

Lower loan-to-value requests signal confidence and reduce lender risk, often unlocking better rates without formal negotiation.

Property condition and exit timeline

Properties requiring extensive renovation carry higher rates than turnkey investments because construction delays create holding cost risk. A cosmetic flip with a 90-day timeline receives more favorable pricing than a gut rehab projected at six months. Location also matters: properties in strong metro markets with liquid buyer pools command better terms than rural areas with longer days-on-market averages.

Your track record and capital reserves

First-time investors typically pay 1 to 2 points more than borrowers who've completed multiple successful flips. Lenders reward proven operators because historical performance predicts future results better than any application can. Demonstrating liquid reserves beyond your down payment also improves your positioning, as it proves you can handle unexpected costs without defaulting when renovation budgets overrun initial estimates.

Standard hard money terms and fees to expect

Beyond the interest rate and points, hard money loans carry specific term structures and fees that you need to factor into your total cost analysis. Most lenders follow similar frameworks, though individual line items can vary significantly. Understanding these standard expectations helps you identify when a lender's fee structure sits outside normal market practice.

Loan duration and payment structure

Hard money loans typically run six to twelve months, with most lenders offering interest-only monthly payments that keep your carrying costs predictable. You pay the full principal balance at maturity, usually when you sell the renovated property or refinance into conventional financing. Some lenders extend terms to 18 or 24 months for larger commercial projects, but shorter durations remain standard for residential flips.

Interest-only payments reduce your monthly outflow during renovation periods when cash flow matters most.

Extension options usually cost 1 to 2 points per additional three months if your project timeline runs long. Lenders charge these extension fees because they've priced their original term based on specific return expectations and capital deployment schedules.

Additional fees beyond rate and points

You'll encounter origination fees, underwriting charges, and processing costs that range from $500 to $2,000 depending on loan size. Document preparation typically runs $300 to $750, while appraisal fees for investment properties cost $400 to $600. Some lenders bundle these costs into closing, while others require separate payment upfront. Prepayment penalties appear less frequently now than in previous years, but verify this detail before signing because early payoff charges can eliminate the savings from a faster flip timeline.

How to compare lenders and estimate total cost

Shopping hard money lender rates requires calculating your true all-in cost across multiple lenders to identify the most competitive financing. You can't compare rates in isolation because upfront points, fees, and loan terms combine to determine your actual capital expense. A lower rate with higher points often costs more than a slightly higher rate with minimal upfront charges.

Calculate your all-in financing cost

Your total financing expense includes interest charges plus all closing costs paid to secure the loan. Take the monthly interest payment, multiply it by your expected hold period, then add origination points and fees. For example: a $150,000 loan at 11 percent with 2 points held for six months costs $3,000 in points, plus $8,250 in interest, totaling $11,250 in financing expense.

Running this calculation for each lender quote reveals which offer actually saves you money over your project timeline.

Request comparable term sheets from multiple lenders

Contact three to five hard money lenders and provide identical deal parameters: purchase price, renovation budget, after-repair value, and your requested loan-to-value ratio. You need written term sheets that specify the interest rate, points, monthly payment amount, prepayment terms, and all additional fees. This creates an apples-to-apples comparison that prevents lenders from burying costs in fine print or verbal assurances that never appear in your final documents. Experienced investors prioritize lenders who fund quickly and close on time over those offering rates half a point lower but with histories of delayed closings that cost you more in lost opportunities.

Final takeaways

Understanding hard money lender rates before you make an offer protects your profit margins and prevents expensive surprises during your project timeline. You need to calculate your all-in cost by adding interest charges, upfront points, and fees across your expected hold period. This gives you the real number that determines whether your deal generates returns or breaks even.

Compare written term sheets from multiple lenders using identical deal parameters so you can spot the best financing structure for your specific project. Rates between 9 and 12 percent with 2 to 3 points represent competitive pricing in 2026 for standard fix-and-flip scenarios. Your loan-to-value ratio, property condition, and track record directly impact the terms you receive.

If you're working on residential flips, commercial acquisitions, or investment properties that need fast, flexible financing, contact David Roa for hard money and DSCR loan options backed by 25 years of real estate lending experience and over $150 million in funded deals.