How To Buy A House With An ITIN Number: Step-By-Step Guide

If you're wondering how to buy a house with an ITIN number, the short answer is: yes, you absolutely can. You don't need a Social Security Number to qualify for a mortgage in the United States. Thousands of ITIN holders purchase homes every year through specialized loan programs that most traditional banks won't tell you about, or simply don't offer.

The process looks different from a conventional mortgage, but it's straightforward once you know what lenders expect. You'll need to meet specific requirements around down payments, credit history, and documentation, all of which we'll break down in this guide. The biggest hurdle for most buyers isn't eligibility; it's finding a lender who actually knows how to close these loans.

That's where our experience matters. At David Roa, we've helped ITIN borrowers secure home financing for over 25 years, funding more than $150 million in loans across residential, commercial, and investment properties. ITIN lending is one of our core specialties, not a side offering we figured out last year.

This step-by-step guide covers everything from qualifying requirements to closing day, so you can move forward with clarity and confidence.

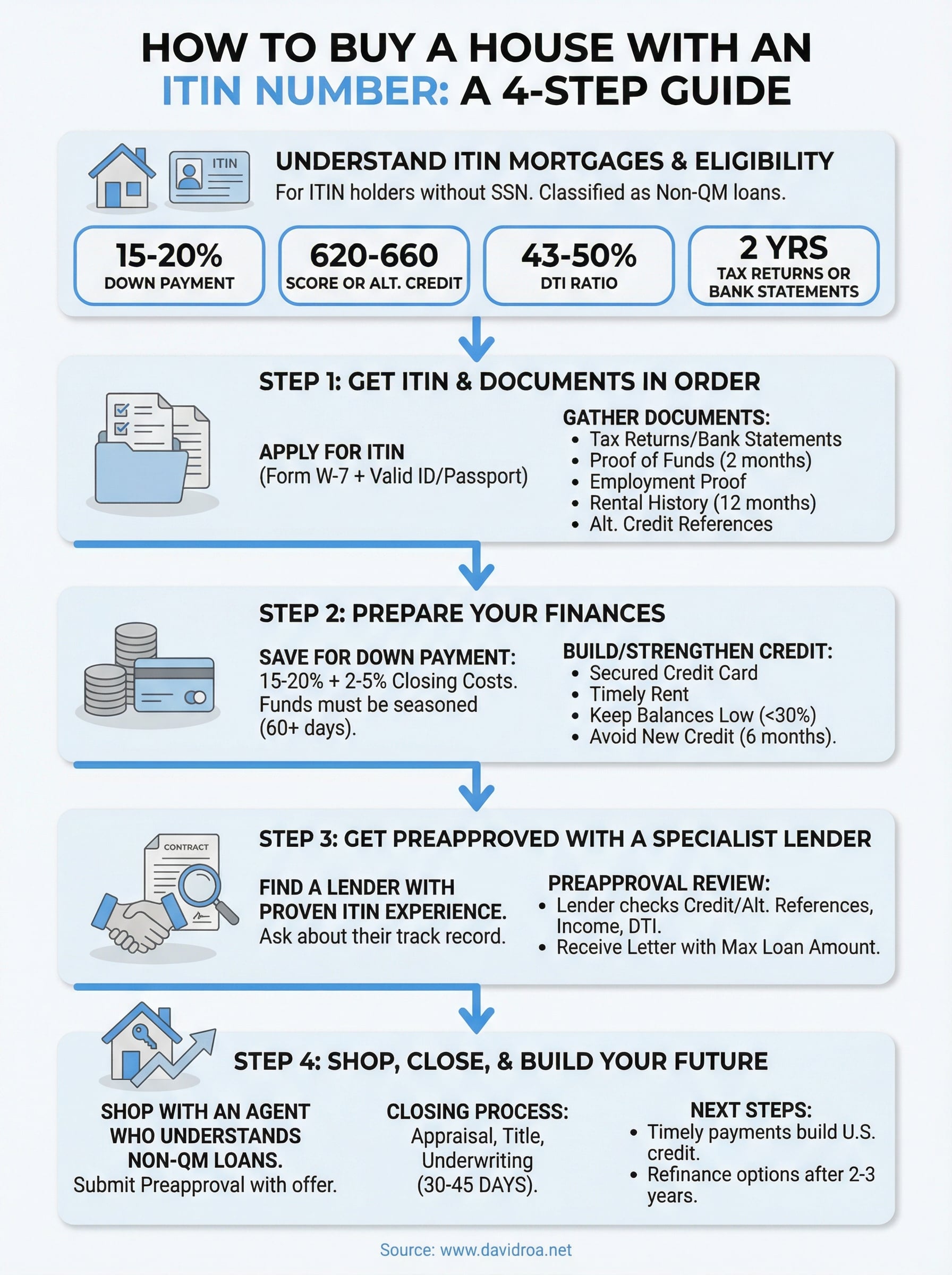

Understand ITIN mortgages and basic eligibility

An ITIN mortgage is a home loan designed for borrowers who have an Individual Taxpayer Identification Number but no Social Security Number. These loans exist because millions of people in the United States pay taxes, build credit, and establish financial stability without ever receiving an SSN. Lenders who specialize in this space have built programs that accept ITIN documentation in place of SSN-based credit reports, making homeownership accessible to a much broader group of buyers.

An ITIN mortgage isn't a second-class loan product. Many borrowers close on homes with competitive rates and standard 30-year terms.

What makes ITIN loans different from conventional mortgages

ITIN loans fall outside Fannie Mae and Freddie Mac guidelines, which means lenders classify them as non-QM (non-qualified mortgage) products. That label sounds intimidating, but it simply means the loan follows a different rulebook, not a worse one. Because these loans carry slightly more lender risk, you'll typically face higher down payment requirements and a stricter review of your income documentation compared to a standard FHA or conventional loan.

Lenders evaluate ITIN borrowers using alternative credit references when a traditional credit score isn't available. These references include rent payment history, utility bills, cell phone accounts, and similar recurring obligations. If you've already built a credit file through secured cards or ITIN-linked accounts, that history works directly in your favor during underwriting.

Basic eligibility requirements for ITIN borrowers

Understanding how to buy a house with an ITIN number starts with knowing the baseline standards most ITIN lenders apply. While exact terms vary by lender and loan program, the typical requirements look like this:

| Requirement | Typical Range |

|---|---|

| Down payment | 15% to 20% of purchase price |

| Minimum credit score (if applicable) | 620 to 660 |

| Alternative credit references (if no score) | 3 to 4 tradelines, 12-month history |

| Debt-to-income ratio | 43% to 50% |

| Income documentation | 2 years of ITIN tax returns or 12 to 24 months of bank statements |

Your tax filing history carries significant weight in this process. Most ITIN lenders want to see at least two years of consistent income reported under your ITIN. A stable employment record with the same employer or within the same industry strengthens your application considerably and helps underwriters assess your repayment ability with confidence.

Step 1. Get your ITIN and documents in order

Before you can move forward on how to buy a house with an ITIN number, you need two things in place: a valid ITIN and a complete documentation package. Lenders review your file based on what you submit, so organizing your paperwork early saves you from delays once you're under contract on a home.

How to apply for an ITIN

The IRS issues ITINs through Form W-7, which you submit along with proof of identity and foreign status. You can apply directly through the IRS or work with a Certified Acceptance Agent who reviews your documents on-site without requiring you to mail your original identification.

You can download Form W-7 and review the full instructions directly on the IRS website.

To complete your W-7 application, you'll need:

- Valid passport (the single document that satisfies both identity and foreign status requirements)

- Or a combination of two documents such as a national ID card plus a birth certificate

- Your most recent federal tax return if you have filed before

- Completed Form W-7 with your U.S. mailing address

Documents your lender will require

Once your ITIN is active, gather your financial documents before contacting any lender. Most ITIN loan programs require a consistent, organized package that underwriters can review without back-and-forth requests.

Your standard document checklist includes:

- Two years of ITIN tax returns or 12 to 24 months of bank statements

- Two months of bank statements showing your down payment funds

- Proof of employment or self-employment income such as pay stubs or profit and loss statements

- Rental history letter from your landlord covering at least 12 months

- Utility bills or other alternative credit references

Step 2. Prepare your finances for an ITIN loan

Financial preparation is what separates buyers who close from buyers who stall. ITIN loan programs carry stricter financial benchmarks than conventional mortgages, so knowing the specific targets before you apply puts you in a much stronger position when a lender reviews your file.

Save for a larger down payment

Most ITIN lenders require 15% to 20% down, which means you need to plan your savings around the actual purchase price you're targeting. On a $300,000 home, that's $45,000 to $60,000 in verified funds before you can move forward.

Your down payment funds must be sourced and seasoned, meaning lenders want to see those funds sitting in your account for at least 60 days before closing.

Your lender will also require closing costs, which typically run 2% to 5% of the loan amount. Budget for both so you're not caught short when it counts.

Build or strengthen your credit profile

Understanding how to buy a house with an ITIN number means recognizing that credit history matters, even when you don't have a traditional score. If you already have a credit score, work to keep it above 620 before applying. If you don't, focus on building at least three to four alternative tradelines with 12 months of on-time payment history.

Practical steps to strengthen your profile before applying:

- Open a secured credit card and pay the balance in full each month

- Pay rent on time and request a landlord reference letter documenting your payment history

- Keep existing account balances below 30% of their credit limits

- Avoid applying for new credit in the six months before your mortgage application

Step 3. Get preapproved with an ITIN lender

Preapproval is the step that converts your financial preparation into real buying power. Most sellers and real estate agents won't take your offer seriously without one, so securing a preapproval letter before you start shopping is non-negotiable. For ITIN borrowers, this step also filters out lenders who lack the experience to actually close your loan.

Find a lender who specializes in ITIN loans

Not every mortgage lender offers ITIN programs, and working with the wrong one costs you time and can damage your credit. When you're learning how to buy a house with an ITIN number, choosing a lender with a proven ITIN track record is the single most important decision you make in the process. Ask direct questions upfront: How many ITIN loans have you closed in the last 12 months? Do you hold these loans in-house or broker them to another lender?

A lender who hesitates or gives vague answers to those questions is not the right fit for your file.

What happens during the preapproval review

Your lender will pull your credit report or alternative credit references, verify your income documentation, and calculate your debt-to-income ratio. Submit your complete document package from Step 1 at this stage so underwriting doesn't stall on missing items. Expect the review to take five to ten business days for ITIN applications, slightly longer than a standard preapproval because lenders perform additional income verification steps.

Once approved, you'll receive a preapproval letter stating the maximum loan amount you qualify for, which you'll present alongside every offer you submit on a property.

Step 4. Shop for a home and close the loan

With your preapproval letter in hand, you're ready to start searching for a property. Shopping for a home as an ITIN borrower works the same way it does for any other buyer from a real estate standpoint. The difference is that you need to keep your lender informed throughout the process so your financing doesn't stall once you're under contract.

Work with a real estate agent who understands ITIN transactions

Your agent doesn't need to be an ITIN specialist, but they do need to understand your loan type and communicate it clearly to sellers. When you submit an offer, your agent will include your preapproval letter and may need to explain to the listing agent that your financing is a non-QM product. Some sellers are unfamiliar with this, but a confident agent who has worked with non-traditional buyers before handles that conversation without slowing your deal down.

Choosing an agent who has closed deals with non-traditional financing before reduces friction at the offer stage significantly.

What to expect at closing

Once your offer is accepted, your lender will order an appraisal and title search, then move your file into full underwriting. This is where knowing how to buy a house with an ITIN number pays off, because you've already organized your full document package in the earlier steps. Respond to any underwriter conditions within 24 to 48 hours to avoid delays.

At the closing table, you'll sign your final loan documents, pay your down payment and closing costs, and receive your keys. The process from accepted offer to closing typically takes 30 to 45 days for ITIN loans.

Next steps after you close

Closing day marks the start of your ownership, not the finish line. Once you have your keys, make your first mortgage payment on time and set up automatic payments so you never miss one. Your payment history from this point forward directly builds the U.S. credit profile that will serve you in every future financial decision, including refinancing into a lower rate once you qualify.

Now that you understand how to buy a house with an ITIN number, you can also start thinking ahead. Many ITIN borrowers refinance into a conventional loan within two to three years once they've established a stronger credit history. Others use their equity to purchase a second property or investment home. Each step compounds your financial position in ways renting never can.

If you're ready to move from planning to action, connect with David Roa's ITIN lending team and get your preapproval process started today.