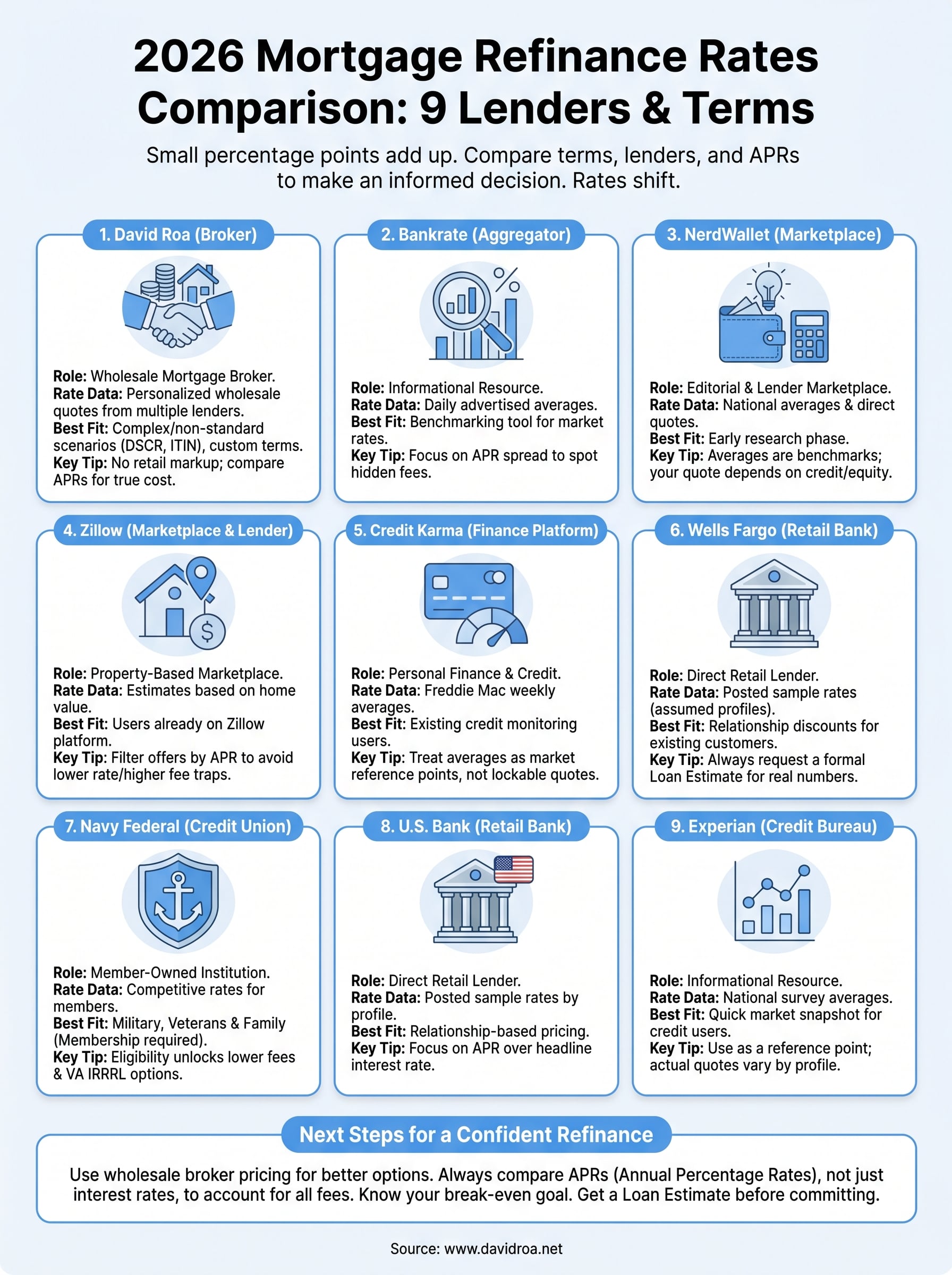

9 Mortgage Refinance Rates Comparison By Term & Lender (2026)

A mortgage refinance rates comparison can save you tens of thousands of dollars over the life of your loan, or cost you just as much if you pick the wrong option. With rates shifting throughout 2026, the difference between a 30-year fixed and a 15-year term, or between Lender A and Lender B, is often larger than most borrowers realize. The numbers matter, and small percentage points add up fast.

After funding over $150 million in loans across more than 25 years, I've walked hundreds of homeowners through refinancing decisions just like the one you're facing now. At David Roa, we work with residential borrowers, investors, and business owners daily, so we see exactly how rates vary across lenders, terms, and loan types in real time. That hands-on experience is what drives every recommendation we make, whether you're refinancing a primary residence or repositioning an investment property.

Below, you'll find 9 current mortgage refinance rate comparisons broken down by loan term and lender. Each one includes the context you need to evaluate whether refinancing makes sense for your situation, not just the rate itself, but what that rate actually means for your monthly payment and long-term cost. Use this as your starting point to make a confident, informed decision.

1. David Roa

Working directly with David Roa gives you access to a broker with over 25 years of active lending experience and a track record of more than $150 million funded. Unlike a rate aggregator or a bank with one product shelf, David Roa operates as a mortgage broker, which means he shops multiple wholesale lenders on your behalf to find the rate and terms that actually fit your situation.

What you can compare by term and loan type

David Roa offers a full range of refinance loan products, so your mortgage refinance rates comparison here goes well beyond a standard 30-year fixed. Common term options include 10-, 15-, 20-, and 30-year fixed loans, as well as adjustable-rate mortgages for borrowers who plan to sell or refinance again within a few years. You can also compare across these loan types:

- FHA refinance loans (including streamline options)

- VA refinance loans (IRRRL and cash-out)

- Conventional loans (conforming and jumbo)

- DSCR loans for investment properties

- ITIN loans for non-U.S. citizens

How the quote process works

Getting a quote starts with a direct conversation. You share your goals, current loan details, and financial picture, and David runs scenarios across multiple wholesale lenders to surface competitive options. Because he works on the wholesale side, the rates you see are not marked up the same way a retail bank would price them, which typically means better pricing for the same loan.

Working with a broker who actively invests in real estate and runs a business gives you a perspective that most loan officers simply don't have.

Best fit scenarios

Borrowers with complex or non-standard financial situations benefit the most from working with David Roa. That includes self-employed borrowers, real estate investors using DSCR loans, ITIN holders, or anyone who has been turned down by a traditional bank. If your file is straightforward, you still benefit from wholesale pricing and one-on-one service.

Fees and costs to expect

Expect standard broker fees, which David discloses upfront before you commit to anything. Origination fees, third-party closing costs, and appraisal fees all apply, but the broker model often offsets those through lower rates compared to retail lenders. No surprise charges get added at the closing table.

2. Bankrate

Bankrate publishes daily mortgage refinance rate data pulled from a network of lenders across the country. It functions primarily as an informational resource and lead generation platform, meaning the rates you see are averages and advertised figures rather than personalized quotes tied to your credit profile and loan details.

What you can compare by term and loan type

Bankrate covers the most common refinance terms, including 10-, 15-, 20-, and 30-year fixed loans, along with 5/1 and 7/1 adjustable-rate options. You can filter by loan type, including conventional and FHA refinance products, which makes it a useful starting point for a mortgage refinance rates comparison before you talk to a lender directly.

How to use the rate tables and APR data

The rate tables show both the interest rate and the APR, and that gap matters. A wider spread between the two signals higher lender fees baked into the loan. Use the APR column to compare true costs across lenders rather than focusing on the headline rate alone.

The APR is almost always the more honest number when you're comparing refinance offers side by side.

Best fit scenarios

Bankrate works best as a benchmarking tool rather than a transaction platform. Use it to understand where market rates sit before you apply anywhere.

Fees and costs to expect

Bankrate itself charges you nothing, but lenders listed on the platform carry their own origination fees, points, and closing costs that vary widely and only appear once you submit contact information.

3. NerdWallet

NerdWallet combines editorial rate data with a lender marketplace, giving you two separate layers of information in one place. It publishes daily refinance rate averages alongside actual lender quotes you can request directly through the site, which makes it more actionable than a pure data aggregator.

What you can compare by term and loan type

NerdWallet covers 15-year and 30-year fixed refinance loans as its primary comparison options, with some coverage of 10-year fixed and ARM products depending on market conditions. The platform includes conventional, FHA, and VA refinance loan types, so you can run a basic mortgage refinance rates comparison across the most common borrower scenarios before committing to a lender conversation.

How to use daily averages and lender marketplace quotes

The daily averages NerdWallet publishes reflect national rate trends, not your personal rate. They serve as a benchmark. The more useful tool is the lender marketplace section, where you enter basic details and receive quotes from participating lenders. Compare the APR figures across those quotes, not just the interest rate, to factor in lender fees accurately.

The gap between the advertised average and your actual quote depends heavily on your credit score, equity position, and loan size.

Best fit scenarios

NerdWallet fits borrowers in the early research phase who want to understand rate ranges before talking to a loan officer.

Fees and costs to expect

NerdWallet charges no fees to use the platform. Individual lenders set their own origination costs, points, and closing fees, which only become visible once you request a personalized quote.

4. Zillow Home Loans marketplace

Zillow Home Loans operates as both a direct lender and a comparison marketplace, which sets it apart from pure rate aggregators. The platform pulls your home's estimated value from Zillow's property database to personalize the rate display, giving you a more grounded starting point for a mortgage refinance rates comparison than a site using generic inputs.

What you can compare by term and loan type

Zillow covers the most common refinance terms, including 15-year and 30-year fixed-rate loans, along with select ARM products. Conventional and FHA refinance options are available through the marketplace, though the overall range of loan types is narrower than what a broker shopping wholesale lenders can put in front of you.

How to compare lenders and filter offers

You enter your property details, estimated credit score, and current loan balance to generate competing rate offers from multiple lenders in a single view. The platform lets you filter results by APR, monthly payment, or lender fees, which makes it more useful than a table showing only interest rates.

Always sort by APR when filtering offers, since a lower rate with higher lender fees can end up costing more over your loan term.

Best fit scenarios

Zillow works best for borrowers who already rely on the platform for property research and want a fast, consolidated look at refinance options without opening separate lender tabs.

Fees and costs to expect

The marketplace itself is free to use, but each participating lender applies its own origination charges, discount points, and closing cost structures that only appear once you request a full personalized quote.

5. Credit Karma

Credit Karma positions itself as a personal finance platform that includes mortgage refinance rate data alongside credit monitoring and financial product recommendations. It pulls Freddie Mac weekly survey averages to populate its rate displays, which means the numbers reflect national trends rather than offers tied to your specific credit file.

What you can compare by term and loan type

Credit Karma focuses primarily on 30-year and 15-year fixed refinance rates for conventional loans. The platform does not offer the same depth of loan type variety you would find through a broker, so your mortgage refinance rates comparison here is limited to the most common conforming loan scenarios.

How to read Freddie Mac average rate data vs offers

The rate figures Credit Karma displays come from Freddie Mac's Primary Mortgage Market Survey, which is a weekly national average, not a lender quote. When Credit Karma connects you to lender offers, those figures will almost always differ from the published averages based on your credit score, loan-to-value ratio, and loan size.

Treat any national average you see on Credit Karma as a market reference point, not a number you can actually lock.

Best fit scenarios

Credit Karma works best for borrowers who already use the platform for credit score tracking and want a quick glance at where refinance rates sit without leaving the app.

Fees and costs to expect

Credit Karma charges no fees for rate browsing. Individual lenders set their own origination fees and closing cost structures, which only surface once you pursue a full application.

6. Wells Fargo

Wells Fargo is one of the largest retail mortgage lenders in the United States, offering refinance products through its branch network and online platform. As a direct bank, Wells Fargo prices loans from its own product shelf, which means you get one institution's rates rather than a competitive wholesale market working in your favor.

What you can compare by term and loan type

Wells Fargo publishes refinance rates for 15- and 30-year fixed loans as its primary options, with some 10- and 20-year terms available depending on loan type. Conventional and FHA refinance products are both accessible, giving you a limited but usable starting point for a mortgage refinance rates comparison against other retail lenders.

How to interpret posted rates vs personalized quotes

The rates Wells Fargo posts online are sample figures built around assumed borrower profiles, typically a high credit score, a specific loan amount, and a set loan-to-value ratio. Your actual quote shifts once you submit a full application and the bank reviews your file. The gap between the posted rate and your real offer can be meaningful if your equity position or credit score differs from those assumptions.

Always request a Loan Estimate before comparing Wells Fargo to any other lender so you're working with actual numbers, not sample figures.

Best fit scenarios

Wells Fargo works best for borrowers who already hold deposit or investment accounts with the bank and want to explore a relationship-based pricing discount during the refinance process.

Fees and costs to expect

Wells Fargo applies origination fees, appraisal costs, and standard closing charges to most refinance transactions, and the full breakdown only appears once you formally apply and receive a Loan Estimate.

7. Navy Federal Credit Union

Navy Federal Credit Union is the largest credit union in the United States by membership and assets, serving active-duty military, veterans, Department of Defense civilians, and their immediate family members. As a member-owned institution, it operates outside the traditional bank structure, which often translates into more competitive rates and lower fees for qualified borrowers.

What you can compare by term and loan type

Navy Federal offers refinance products across 15-year and 30-year fixed-rate terms as its primary options, along with select adjustable-rate mortgage products. Your mortgage refinance rates comparison here covers conventional loans and VA refinance products, including VA IRRRL (Interest Rate Reduction Refinance Loan) options, which are specifically designed for eligible military borrowers looking to reduce their current rate with minimal documentation.

How membership and eligibility can affect options

Your access to Navy Federal's refinance products depends entirely on membership eligibility, which the credit union determines before you can apply. If you qualify, your membership status can unlock rate discounts and fee reductions that non-member applicants at retail banks simply cannot access.

Membership eligibility is the single biggest factor that determines whether Navy Federal belongs in your comparison at all.

Best fit scenarios

Navy Federal works best for active-duty service members, veterans, and their families who want to refinance using VA loan benefits and prefer working with an institution that understands military financial situations.

Fees and costs to expect

Standard closing costs and appraisal fees apply to most refinance transactions, though VA IRRRL loans can reduce some upfront costs depending on your loan scenario.

8. U.S. Bank

U.S. Bank is a major national retail lender that publishes refinance rates directly on its website and processes applications both online and through its branch network. As a direct bank, it prices loans from its own product shelf, which limits your comparison to what one institution offers rather than a competitive wholesale market.

What you can compare by term and loan type

U.S. Bank supports refinance terms including 15-year and 30-year fixed-rate loans, along with select 10-year and 20-year options depending on your loan scenario. Conventional and FHA refinance products are available, giving you a functional starting point for a mortgage refinance rates comparison against other retail lenders. VA refinance options are also listed for eligible borrowers.

How to evaluate posted refinance rates and APRs

The rates U.S. Bank displays online are built around specific assumed borrower profiles, including credit score ranges and loan-to-value thresholds. Your actual quote shifts once you apply and the bank reviews your full file. Focus on the APR figure rather than the interest rate alone to account for lender fees when comparing U.S. Bank against other options.

Always request a Loan Estimate from U.S. Bank before treating any posted rate as final.

Best fit scenarios

U.S. Bank works best for borrowers who already hold accounts with the institution and want to explore relationship-based pricing during the refinance process.

Fees and costs to expect

Origination fees, appraisal costs, and standard closing charges apply, and the full breakdown surfaces only once you submit a formal application and receive a Loan Estimate.

9. Experian

Experian is primarily known as one of the three major credit bureaus in the United States, but it also publishes mortgage refinance rate content through its personal finance platform. Unlike direct lenders or broker marketplaces, Experian functions as an informational resource that aggregates national rate data and connects you to lending partners rather than issuing loans itself.

What you can compare by term and loan type

Rate content on Experian focuses on 30-year and 15-year fixed refinance loans as the core comparison options, with some coverage of ARM products and FHA refinance scenarios. Your mortgage refinance rates comparison here is limited to broad national data rather than personalized lender quotes tied to your actual credit profile and equity position.

How to use national averages and understand assumptions

The rate figures Experian publishes reflect national survey averages built around idealized borrower assumptions, including high credit scores and specific loan-to-value ratios. When you see a rate on Experian, treat it as a market reference point, not a number you can walk into a lender's office and lock.

The stronger your credit profile, the closer your actual quote will land to any national average you see on a platform like Experian.

Best fit scenarios

Borrowers who are already monitoring their credit through the platform benefit most from Experian's rate content, since it delivers a quick market snapshot before they contact a lender directly.

Fees and costs to expect

Experian charges no fees to browse rate data on its platform. Any fees you encounter come directly from lenders you connect with through the site, and those costs only become clear once you request a full personalized quote.

Next steps to lock a refi you can defend

A mortgage refinance rates comparison only delivers value when you act on it with the right information in hand. Pull your current loan statement, check your credit score, and write down your break-even goal before you contact any lender. Knowing how long you plan to stay in the home tells you whether a lower rate actually saves you money after factoring in closing costs and fees.

Once you have that baseline, work with a lender who shops the market for you rather than selling from one product shelf. Wholesale broker pricing typically beats what retail banks post online, and access to multiple loan programs means your refinance gets structured around your actual situation rather than a generic template. Run your numbers against real lender quotes, compare APRs instead of headline rates, and verify every fee before you sign. If you are ready to move forward, contact David Roa and get a quote you can actually defend.