PNC Equipment Finance: Solutions, Contact, Login & Payments

Whether you're acquiring heavy machinery, upgrading a vehicle fleet, or investing in technology, the right financing can make or break your timeline. PNC Equipment Finance is one of the more recognized names in this space, offering leasing and lending products designed for businesses that need to fund critical assets without draining cash reserves. Understanding what they offer, and how to navigate their systems, puts you in a stronger position before you sign anything.

This article breaks down PNC's equipment financing solutions, walks you through how to contact their team, and covers the practical details like logging into your account and making payments. We'll also look at what makes their programs work and where they might fall short depending on your situation. As a lending professional with over 25 years of experience funding commercial and business loans at David Roa, I've helped business owners across the Chicago area and nationwide evaluate financing options just like these, so you'll get a grounded perspective here, not a sales pitch.

Let's get into the details so you can decide whether PNC's equipment finance products fit your business goals, or if an alternative route makes more sense for your specific financial picture.

What PNC Equipment Finance does

PNC Equipment Finance operates as a dedicated division of PNC Bank, one of the largest financial institutions in the United States. Their focus is specifically on commercial asset financing, meaning they provide capital for businesses to acquire equipment through either loans or lease agreements. Rather than drawing from general business credit lines, this division uses underwriting processes built around the assets themselves, which changes how approvals and pricing work compared to a standard business loan.

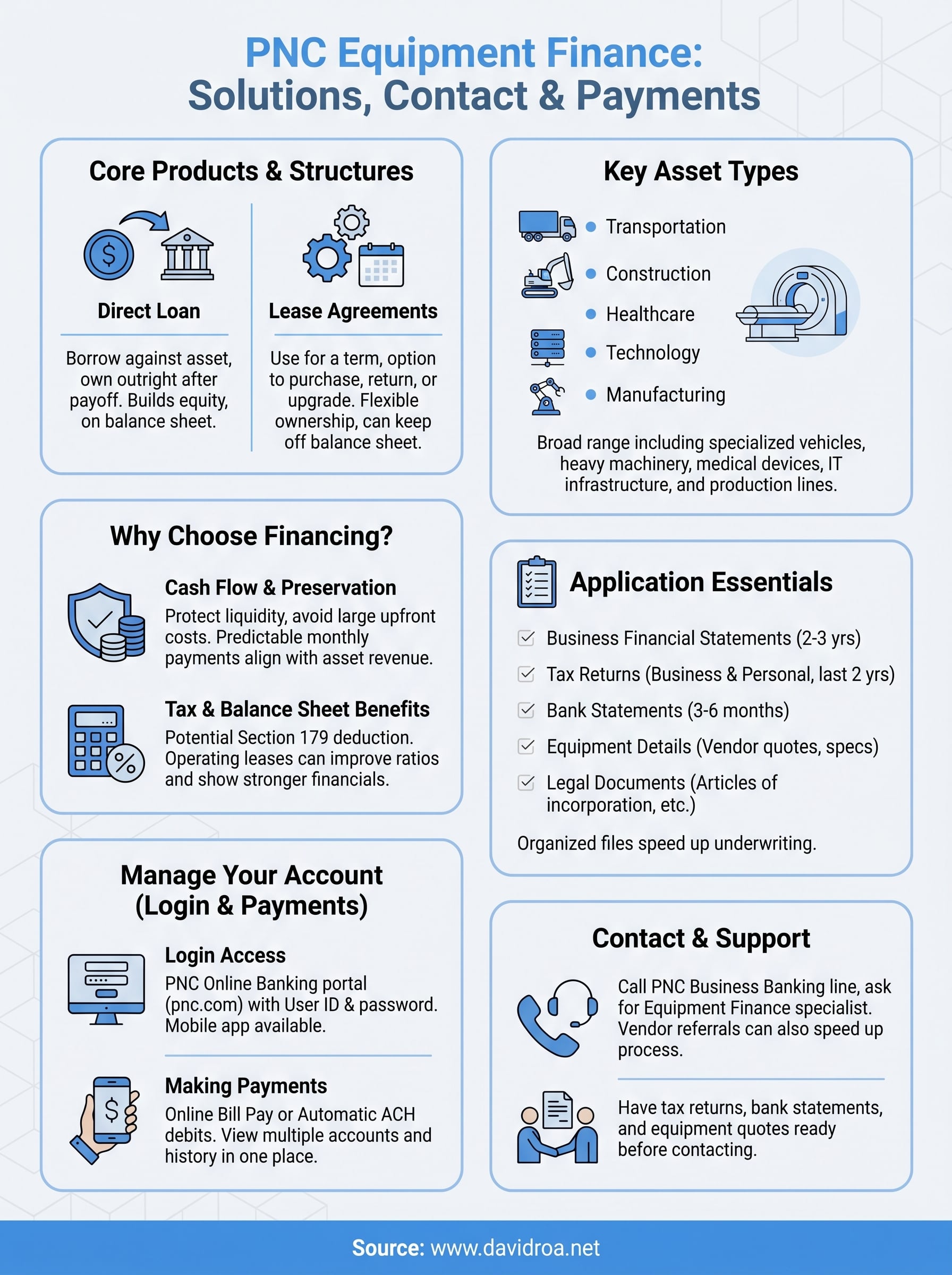

Core products and asset types

PNC structures their equipment financing around two primary vehicles: direct loans and lease agreements. A direct loan works like a traditional purchase, where you borrow against the asset and own it outright once you've paid off the balance. A lease lets you use the equipment for a set term while PNC retains ownership, giving you the option to purchase, return, or upgrade at the end of that term.

The range of assets they finance is broad. Common categories include:

- Transportation and fleet vehicles: semi-trucks, delivery vans, and specialized vehicles

- Construction and heavy equipment: cranes, excavators, and loaders

- Healthcare and medical devices: imaging systems, lab equipment, and surgical tools

- Technology and IT infrastructure: servers, networking hardware, and enterprise software systems

- Manufacturing equipment: production lines, industrial machinery, and processing units

The range of asset types means most industries can find a workable structure through PNC, but approval terms will vary significantly depending on asset value, depreciation rate, and your business's credit profile.

Lease vs. loan: how the structures differ

Understanding which product fits your situation matters more than most borrowers realize. With a loan structure, you build equity in the asset from day one, and you carry it on your balance sheet as a depreciable asset. This works well for equipment with a long useful life where ownership makes financial sense over time.

Lease agreements offer more flexibility when your industry moves fast or when preserving working capital is the priority. An operating lease keeps the asset off your balance sheet in many cases, which can improve certain financial ratios. A capital lease (also called a finance lease) functions more like ownership and does appear on your balance sheet, so your accountant should weigh in before you choose.

Who they typically work with

PNC equipment finance programs are primarily designed for mid-size to larger businesses with established credit histories. Their minimum transaction sizes tend to skew toward larger deals, often starting around $100,000, though this can vary by program and asset class.

Beyond credit history, PNC also evaluates the residual value of the equipment being financed. Assets that hold value well, like certain medical or construction equipment, often qualify for better terms because the collateral risk is lower. If you're financing something that depreciates quickly or becomes obsolete fast, expect that to factor into your rate and term options.

Why businesses use equipment financing

Most businesses that turn to equipment financing aren't doing it because they can't afford the purchase outright. Many are doing it because tying up capital in a single asset purchase creates unnecessary risk, especially when that capital could fund payroll, inventory, or growth opportunities instead. Financing lets you put equipment to work immediately while spreading the cost over time in a way that aligns with the revenue the asset helps generate.

Cash flow and capital preservation

When you finance equipment rather than pay cash, you protect your liquidity. A $500,000 piece of machinery doesn't have to hit your bank account all at once. Instead, you structure payments against the income that equipment produces, which creates a more predictable monthly cost you can plan around. This matters most in industries with seasonal revenue swings or businesses that are scaling quickly.

Preserving working capital gives you room to respond when opportunities or unexpected costs come up, which happens in every business eventually.

Programs like PNC equipment finance are built on this logic. The goal isn't just to get you the equipment, it's to give you a structure that doesn't put your operating cash flow under pressure while you're still putting the asset to use.

Tax and balance sheet advantages

Depending on how you structure the deal, equipment financing can create meaningful tax benefits. Under Section 179 of the IRS tax code, businesses can deduct the full purchase price of qualifying financed equipment in the year it's placed into service, rather than depreciating it gradually. This can reduce your taxable income significantly in the year of acquisition.

Lease structures add another layer of flexibility. An operating lease keeps the asset off your balance sheet in many cases, which can improve your debt-to-equity ratio and make your financials look stronger to other lenders. Your accountant should always review the specific structure before you commit, since the accounting treatment will affect how the deal performs from a tax and reporting standpoint.

How to apply for PNC equipment financing

Applying for PNC equipment finance starts with understanding that this is a commercial lending process, not a quick online form. You'll work with a dedicated representative who reviews your deal, asks questions, and structures terms based on both your business financials and the asset you're acquiring. Knowing what to expect before you start saves time and helps you present your business in the strongest possible light.

What you need before you apply

Before you contact PNC, pull together the documents their team will almost certainly request. Having these ready speeds up underwriting and signals that your business is well-organized and financially transparent, which matters more than most borrowers expect.

- Business financial statements: two to three years of profit and loss statements and balance sheets

- Tax returns: business and personal, typically covering the last two years

- Bank statements: three to six months of recent statements showing cash flow patterns

- Equipment details: vendor quotes, asset descriptions, and estimated useful life

- Business legal documents: articles of incorporation, operating agreements, or similar formation records

The more complete your file when you first reach out, the faster PNC's team can move toward a decision.

What happens after you submit

Once you submit your application and supporting documents, PNC's underwriting team evaluates both your creditworthiness and the collateral value of the equipment. This review period typically takes several business days, though complex deals or larger transactions may take longer depending on the asset class and overall deal structure.

You'll receive either an approval with proposed terms or a request for additional documentation. If approved, review the lease or loan agreement carefully before signing. Pay close attention to the rate, term length, end-of-lease options, and any fees tied to early payoff or equipment return, since those details have a direct impact on your total cost over the life of the deal.

How to handle login and payments

Once your PNC equipment finance deal closes, day-to-day account management happens through PNC's online banking platform. You access your equipment finance account using the same PNC Online Banking portal you'd use for any other PNC product, which keeps everything consolidated in one place rather than juggling separate systems.

Logging into your account

To log in, go to pnc.com and enter your User ID and password on the main banking login page. If you're a new customer setting up online access for the first time, select the enrollment option and have your account number and business tax ID ready to verify your identity during setup. PNC also offers a mobile app for iOS and Android, which gives you access to balances, payment history, and account details directly from your phone.

If you run into access issues, call PNC's business banking support line directly rather than trying to resolve login problems through email, since account security issues move faster over the phone.

Making payments on your equipment loan or lease

Payments on your equipment financing can be made through PNC's online bill pay system or set up as automatic ACH debits from your business checking account. Auto-pay is worth using because it eliminates the risk of a missed payment, which can trigger late fees and potentially affect your business credit profile. If you prefer manual payments, schedule them a few days early to account for processing time.

For businesses managing multiple equipment finance agreements with PNC, the online portal lets you view each account separately and apply payments to the correct contract. Keep records of each transaction, especially around payoff periods, since final payment amounts often differ slightly from your regular installment due to accrued interest or outstanding fees that built up over the loan term.

Contact options and what to prepare

Reaching the right person at PNC equipment finance matters more than most borrowers expect. Their commercial lending team handles deals differently than a retail bank branch does, so going through the right channel gets you a faster, more useful response. You can start by visiting pnc.com and navigating to their Business Banking or Equipment Finance section, where you'll find contact forms and regional representative information based on your location.

How to reach PNC's equipment finance team

The most direct route is calling PNC's business banking line and asking to be connected with an equipment finance specialist. Representatives at the branch level often handle smaller business products, but equipment deals of any real size typically route to a dedicated commercial lending team. If your deal involves a large transaction or a specialized asset class, ask specifically for a relationship manager who handles commercial equipment, not a general business banker.

Getting to the right specialist on your first call saves you from repeating your situation multiple times to people who can't actually move your deal forward.

You can also reach out through a vendor referral if you're purchasing from a dealer or manufacturer that has an existing relationship with PNC. Many equipment vendors maintain financing partnerships, and those introductions can speed up your application process since the vendor relationship adds context to your deal from the start.

What to have ready before you call

Walking into any conversation with a lender unprepared slows everything down. Before you contact PNC, pull together your business tax returns for the last two years, recent bank statements showing cash flow, and a vendor quote or equipment description with the asset's estimated useful life. Having your business formation documents on hand also helps, since lenders verify legal standing early in the process. The more organized your file, the faster PNC can give you a clear answer on terms and structure.

Next steps

PNC equipment finance gives you a solid set of tools if your business needs structured asset funding and you have the financials to back a mid-to-large deal. Before you apply, confirm that your documents are current, your cash flow story is clear, and you understand whether a loan or lease structure fits your balance sheet better. Those three things alone will make your first conversation with their team more productive.

Not every deal fits a large bank's criteria, though. If your situation involves non-traditional income, a newer business, or a deal size that falls below PNC's typical minimums, a broker with direct access to multiple lenders often gets you better terms faster. That's where experience and relationships with the right capital sources make a real difference. If you want a second opinion on your equipment financing options before you commit, reach out to David Roa and get a straightforward assessment of what your deal could look like.