Refinance Mortgage With ITIN Number: Eligibility Guide

If you already own a home and used an ITIN to get your original mortgage, you may be wondering whether you can refinance mortgage with ITIN number to get a better rate, lower your monthly payment, or tap into your equity. The short answer is yes, but the process looks different from a conventional refinance, and not every lender offers this option.

Most traditional banks won't touch ITIN refinances. That leaves many homeowners stuck in loans with higher rates than they need to be paying, unaware that specialized programs exist specifically for their situation. The eligibility requirements, documentation, and lender expectations differ significantly from SSN-based refinances, and understanding those differences before you apply can save you time, money, and a lot of frustration. Whether you're looking at a rate-and-term refinance or a cash-out option, knowing what qualifies you is step one.

At David Roa, we've spent over 25 years helping clients navigate exactly these kinds of non-traditional lending scenarios. With more than $150 million funded across residential, commercial, and investment loans, including ITIN mortgage programs, we work with borrowers who are often overlooked by conventional lenders. This guide breaks down who qualifies for an ITIN refinance, what documents you'll need, how lenders evaluate your application, and where to find programs that actually serve ITIN holders.

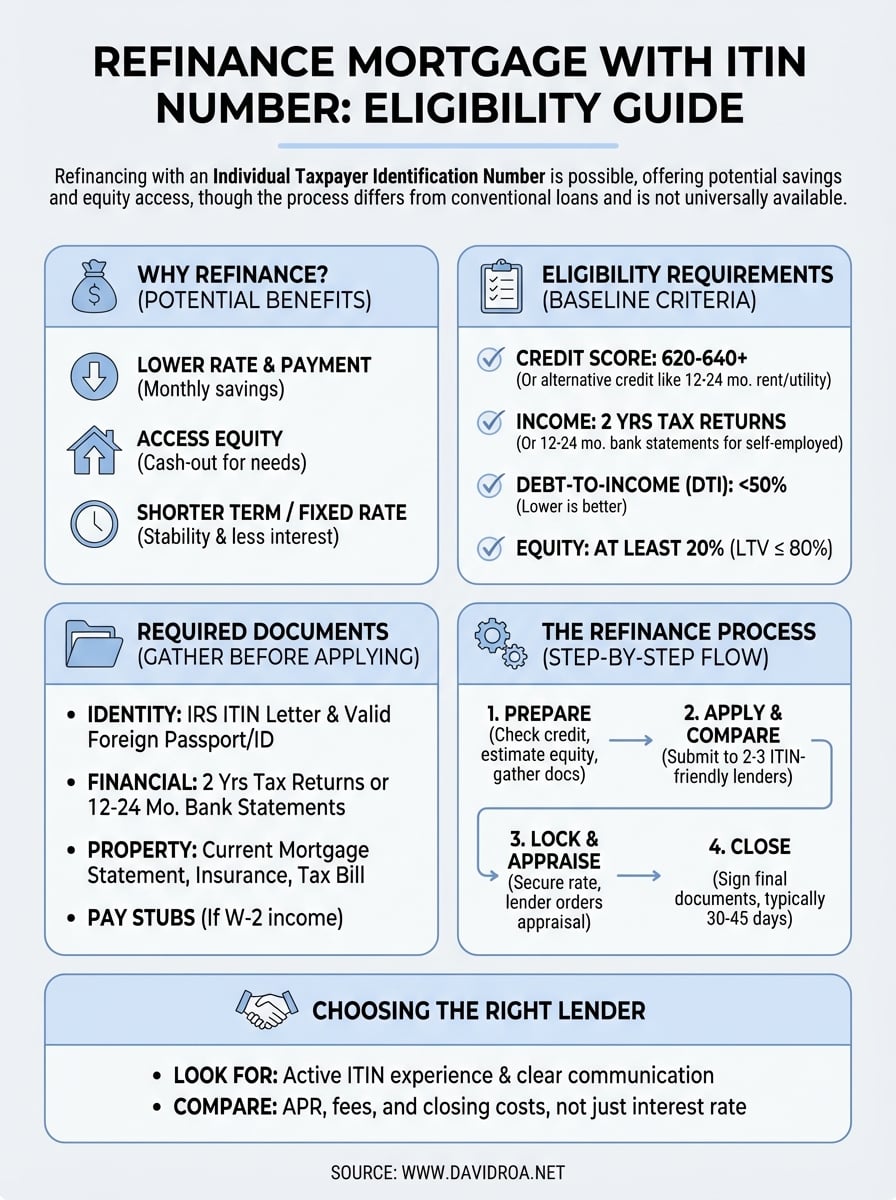

Why refinancing with an ITIN can make sense

When you first got your ITIN mortgage, your options were limited, so you likely accepted whatever rate and terms were available at the time. ITIN lending programs have expanded significantly over the past several years, meaning the rate you locked in originally may be much higher than what you'd qualify for today. Taking the time to refinance mortgage with ITIN number can translate into real savings each month without requiring you to sell or move.

Lower your rate and monthly payment

If your original loan came with a higher-than-average interest rate because lender options were scarce, refinancing now could put hundreds of dollars back into your pocket every month. Many ITIN borrowers secured loans during periods when specialized programs were rare and lenders charged bigger risk premiums to offset what they saw as uncertainty. That landscape has shifted, and more competitive programs exist today than most borrowers realize.

Your financial profile has also likely strengthened since you first closed on your home. More on-time payments, consistent tax returns filed with your ITIN, and a longer credit history all give lenders more confidence, which gives you more leverage to qualify for better terms than you had before.

A half-point rate reduction on a $300,000 loan saves roughly $90 per month, which adds up to more than $32,000 over the full life of a 30-year mortgage.

Additional reasons an ITIN refinance makes financial sense

Accessing your equity is another compelling reason to refinance. A cash-out refinance lets you convert the equity you've built over years of payments into usable funds for home improvements, debt consolidation, or acquiring another property. Many ITIN homeowners don't know this option exists because their original lender never offered it or specialized in only one type of product.

Beyond rate reductions and cash-out, several other situations make an ITIN refinance worth evaluating:

- Adjustable rate to fixed rate: If your ARM has adjusted upward or you expect future increases, locking into a fixed rate removes payment uncertainty and protects your monthly budget.

- Shorter loan term: Refinancing from a 30-year to a 15-year mortgage reduces total interest paid significantly over time, even if the monthly payment increases slightly.

- Remove or add a borrower: If your household situation has changed, restructuring the loan lets you adjust who carries the financial responsibility going forward.

ITIN refinance eligibility requirements

Before you apply to refinance mortgage with ITIN number, you need to understand what lenders actually evaluate. The requirements vary by lender, but most ITIN refinance programs follow a consistent set of baseline criteria that you can prepare for in advance. Meeting these benchmarks before you apply improves your approval odds and the terms you'll receive.

Credit and payment history

Your credit score plays a central role in any refinance approval, and ITIN refinances are no different. Most specialized lenders look for a minimum score of 620 to 640, though stronger scores above 680 open up better rates and more flexible terms. If you don't have a traditional credit score, some lenders accept non-traditional credit references such as 12 to 24 months of on-time rent, utility, or insurance payments as substitutes.

Lenders want to see that you've managed your current mortgage responsibly, so a clean 12-month payment history with no late payments carries significant weight in the approval decision.

Income and equity requirements

Consistent, verifiable income is another key factor. ITIN refinance lenders typically want two years of tax returns filed under your ITIN to document earnings. Self-employed borrowers can often use bank statements from 12 to 24 months as an alternative when tax returns don't fully reflect actual income. Your debt-to-income ratio should generally stay below 50%, though tighter programs may cap it at 43%.

On the equity side, most programs require you to retain at least 20% equity after the refinance closes, which means your loan-to-value ratio should sit at or below 80%. Cash-out refinances sometimes carry stricter equity thresholds depending on the lender.

Documents lenders usually ask for

Gathering your paperwork before you apply to refinance mortgage with ITIN number speeds up the process and reduces the chance of delays. Lenders need to verify your identity, income, and property value, and missing even one document can stall your approval. Knowing what's expected lets you walk into the application fully prepared.

Identity and ITIN documentation

Your Individual Taxpayer Identification Number is the foundation of the entire application. Lenders will ask for your original IRS-issued ITIN letter along with a valid foreign passport or consular ID card to confirm your identity. Some programs also accept a combination of a foreign national ID plus a second document like a utility bill or bank statement to establish residency.

The IRS issues ITINs specifically for tax reporting purposes, and lenders use your filing history tied to that number to establish your financial track record in the U.S.

Financial and property documents

Two years of tax returns filed under your ITIN are the standard income documentation most lenders require. If you're self-employed or your returns don't reflect your full income, 12 to 24 months of bank statements work as an alternative for many ITIN refinance programs. You'll also need recent pay stubs if you receive W-2 income.

On the property side, expect to provide your current mortgage statement, homeowners insurance declarations page, and a recent property tax bill. Your lender will also order a new appraisal to confirm your home's current value and verify that your loan-to-value ratio meets program requirements before moving your file forward.

How to refinance with an ITIN number step by step

The refinance process follows a predictable sequence, and knowing each step before you begin keeps you in control of your timeline. When you refinance mortgage with ITIN number, the overall flow mirrors a conventional refinance, but the details at each stage require more preparation and the right lender from the start.

From Application to Closing

Following a clear sequence gives you the best shot at a smooth approval. Start by pulling your credit report to confirm your score and dispute any errors before a lender sees your file. Run a quick estimate of your home's current value against your remaining loan balance to see where your equity stands. If your loan-to-value ratio sits at or below 80%, you're in a solid position to move forward with most ITIN refinance programs.

Getting your credit and equity numbers in order before talking to a lender puts you in a stronger negotiating position from the first conversation.

Next, assemble every document outlined in the previous section so you're ready to submit a complete file immediately. Incomplete applications slow underwriting and can push your rate lock deadline, which costs you time and sometimes money. Once your documents are ready, contact two to three ITIN-friendly lenders and submit formal applications to compare loan estimates side by side. Choose your lender, lock your rate, and schedule the appraisal your lender orders on your property. After underwriting reviews your file and clears any conditions, you sign your final closing documents. Most ITIN refinances close within 30 to 45 days from the time you submit a complete application.

How to choose an ITIN refinance lender and offer

Not every lender who claims to offer ITIN loans actually specializes in them. When you refinance mortgage with ITIN number, working with a lender who handles these files regularly makes a real difference in approval speed, rate competitiveness, and how smoothly underwriting runs. The wrong lender can cost you weeks and ultimately turn down your file for reasons an experienced ITIN lender would never flag.

What to look for in a lender

Your first priority is confirming that a lender has active ITIN refinance programs, not just a page on their website mentioning ITINs. Ask directly how many ITIN refinance loans they've closed in the past 12 months. A lender with real volume knows how to handle alternative documentation, non-traditional credit, and foreign national ID verification without unnecessary delays.

A lender's familiarity with ITIN files often matters more than their advertised rate because an inexperienced underwriting team can create delays that cost you your rate lock.

Beyond experience, evaluate their communication and response time. ITIN refinances often require back-and-forth on documentation, so a lender who responds within one business day and assigns you a dedicated point of contact is worth more than one offering a marginally lower rate with slow follow-through.

Comparing loan offers

Once you have at least two to three loan estimates in hand, compare them on more than just the interest rate. Look at the annual percentage rate, which reflects the true cost including fees, and review origination charges, appraisal costs, and any prepayment penalties. A lower rate with high origination fees can cost more over five years than a slightly higher rate with minimal closing costs, so run the full numbers before you decide.

Next steps

You now have a clear picture of what it takes to refinance mortgage with ITIN number, from the eligibility requirements and documentation to finding the right lender and comparing offers. The process is more accessible than most ITIN homeowners realize, and the potential savings in monthly payments or equity access make it worth pursuing seriously. Your biggest advantage at this point is preparation, so pull your credit report, estimate your current equity, and start gathering the documents outlined in this guide before you contact a lender.

Working with someone who has handled ITIN refinances before makes the difference between a smooth closing and a stalled file. Over 25 years of experience and $150 million funded means we understand exactly what these applications require and how to get them across the finish line. If you're ready to explore your options, connect with David Roa to start the conversation today.