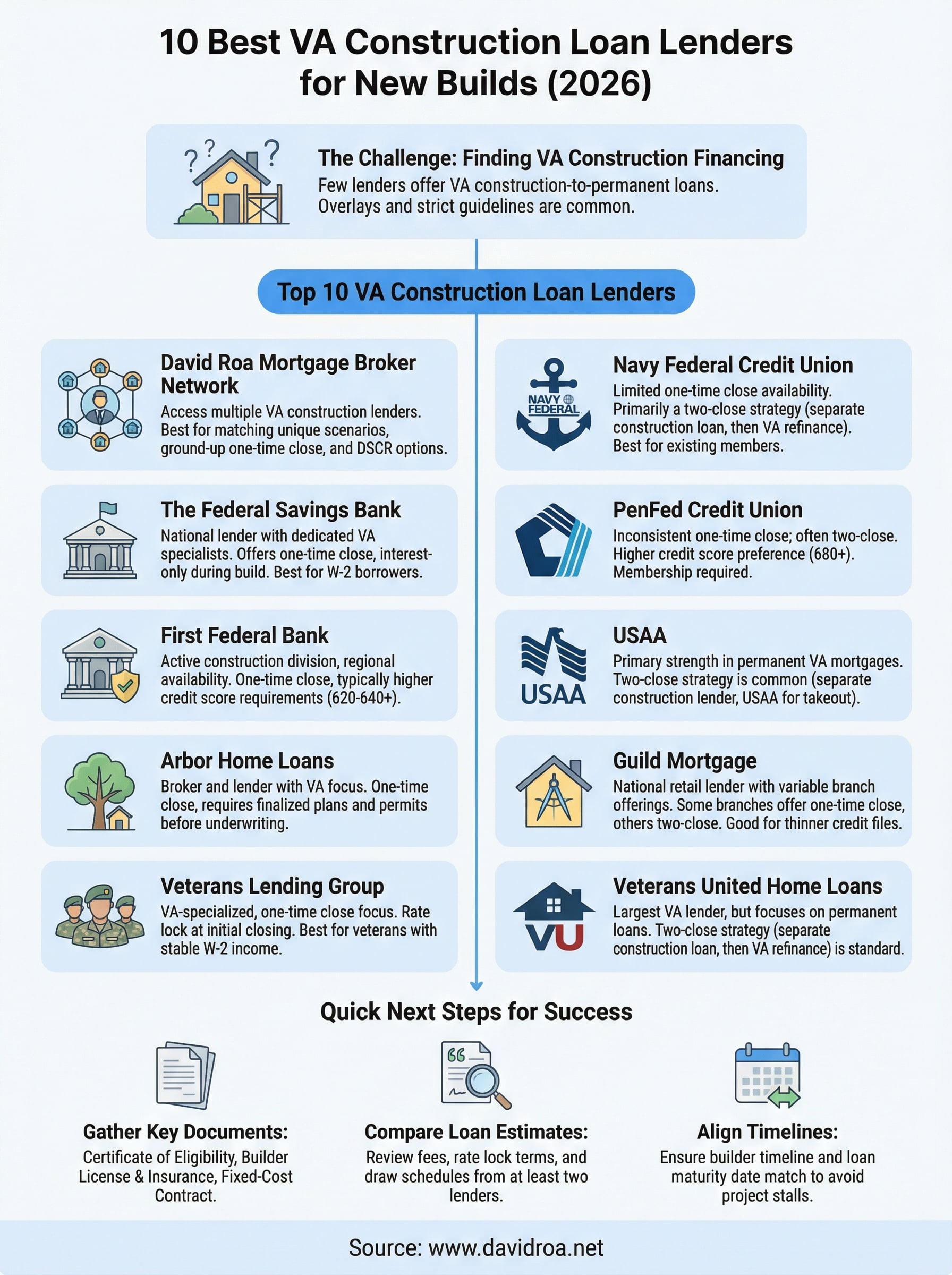

10 Best VA Construction Loan Lenders for New Builds (2026)

Building a home from the ground up with your VA benefits is one of the most powerful ways to use the no-down-payment advantage you've earned, but finding VA construction loan lenders who actually do these deals is a different story. Most lenders either don't offer construction-to-permanent VA loans at all, or they bury you in overlays that make the process feel impossible. The reality is that only a small percentage of VA-approved lenders handle new construction financing, which makes knowing where to look critical.

At David Roa, we've spent over 25 years helping borrowers navigate specialized loan products that traditional banks often shy away from, including VA loans, renovation financing, and construction lending. With more than $150 million funded across residential, commercial, and investment deals, we understand how construction timelines, builder approvals, and VA appraisal requirements intersect in ways that can make or break your project.

This guide breaks down the 10 best lenders offering VA construction loans in 2026, along with what to expect from the application process, how to qualify, and key factors that separate a smooth build from a frustrating one.

1. David Roa mortgage broker network

Working with a mortgage broker rather than a single lender gives you access to multiple VA construction loan lenders at once, which matters when so few banks fund these deals in the first place.

What you can finance for a new build with VA benefits

Through the David Roa network, you can finance ground-up construction on a primary residence using a one-time close structure that combines the build and the permanent mortgage into a single loan. This structure covers the land purchase, construction draws, and final conversion without requiring a second closing or a second set of closing costs.

Why a broker helps when lenders say no to construction

Most retail banks add their own overlays on top of VA guidelines, which means their credit minimums, builder approval requirements, and draw limits are stricter than what the VA actually requires. Matching you with the right lender from the start avoids the wasted time and credit inquiries that come from applying to lenders whose guidelines never fit your scenario.

A single lender denial is not a VA denial. A broker finds the lender whose requirements actually fit your deal.

Best fit borrowers and scenarios

This option works best for veterans with a licensed general contractor already selected, or for borrowers who own land and want to build without a down payment. It also fits investors who need a DSCR loan after construction and want to map out the full financing path before breaking ground.

What to ask for before you choose a lender

Before committing, ask how many VA construction loans the lender has closed in the past year, and get a written breakdown of their draw schedule and inspection process. These two questions reveal whether a lender has real construction experience or is learning on your timeline.

- How many VA construction closings in the last 12 months?

- Who orders draw inspections and how long do approvals take?

- Is the interest rate locked through the full build period?

How to start with David Roa

Reach out directly to review your VA eligibility, your builder's credentials, and your property details before submitting any application. This upfront review keeps your credit inquiry count low and puts you in front of the right lender from the first conversation, not the third.

2. The Federal Savings Bank

The Federal Savings Bank is one of the more recognized VA construction loan lenders that actively markets a one-time close product to veterans. They operate nationally and have dedicated VA loan specialists who handle construction deals as a defined part of their product lineup.

VA construction loan options they tend to offer

Their primary product is a one-time close construction-to-permanent loan that folds the build and the takeout mortgage into a single closing. This means you pay one set of closing costs and avoid a second appraisal when the build completes.

- Land purchase can often be wrapped into the loan

- Interest-only payments typically apply during the build phase

- The permanent rate converts at certificate of occupancy

Best fit borrowers and property types

This lender works best for W-2 borrowers with steady income building a single-family primary residence. Self-employed borrowers should expect stricter income documentation and a longer underwriting review.

Builder, plans, and appraisal requirements to expect

Your builder must hold a valid license and general liability insurance, and you need finalized plans with a project budget before the lender orders the VA appraisal. The appraisal assigns value to the completed home, not the current lot.

Submit your builder's full documentation package before you apply - incomplete files stall approvals more than any other factor.

Common timeline and draw process

Expect a 45- to 60-day closing window after you submit a complete package. An independent inspector verifies each construction phase before funds move to your builder.

How to screen your loan officer and get a quote

Ask how many VA construction loans this officer has personally closed in the past 12 months. Then request a written Loan Estimate to compare origination charges, rate lock length, and draw fees against other lenders.

3. First Federal Bank

First Federal Bank operates as one of the VA construction loan lenders that maintains an active construction lending division for veterans. They offer a construction-to-permanent program built specifically for borrowers using VA benefits to build a primary residence from the ground up.

VA construction to permanent basics

Their program combines the construction phase and the permanent mortgage into one closing, which eliminates duplicate closing costs and a second appraisal. Interest-only draw payments apply during the build, and the permanent loan activates once the home passes final inspection.

Best fit borrowers and regions served

Availability at First Federal Bank varies by state and region, so confirm they lend in your area before you invest time in an application. Their program fits W-2 borrowers with consistent employment history who plan to occupy the finished home as their primary residence.

Credit, reserves, and down payment expectations

VA loans require no down payment, but First Federal Bank typically sets their own credit floor above the VA minimum. Expect a credit score requirement around 620 to 640 and several months of liquid reserves to account for potential cost overruns during construction.

Confirm their exact score overlay before applying, because the VA's own guidelines are often more flexible than what individual lenders enforce.

Builder approval and warranty requirements

Your builder must carry a current state license and active general liability insurance. They also require a signed builder's warranty and a fixed-cost construction contract before your file moves to underwriting.

Questions to ask about rate locks and changes

Ask whether your interest rate locks at initial closing or floats through the full build period. Also confirm what happens to your terms if construction runs past the scheduled completion date.

4. Arbor Home Loans

Arbor Home Loans is a mortgage broker and lender that handles VA construction financing as part of its active product lineup. Their focus on VA-specific programs puts them among the va construction loan lenders worth contacting early in your new build planning.

VA construction lending overview

Arbor offers a one-time close construction-to-permanent loan backed by VA benefits. You sign one set of closing documents that covers both the build phase and the permanent mortgage, which keeps your total closing costs lower than a two-close approach.

Best fit borrowers and home types

This lender fits veterans and active-duty borrowers building a single-family primary residence. Their program works best when you bring:

- A licensed general contractor with an active insurance certificate

- A clear project scope and fixed-cost construction contract

- A credit profile at or above 620

How they handle land, permits, and plan review

Arbor requires finalized architectural plans and a complete permit package before underwriting begins. If you already own land, they can often roll it into the loan, which reduces the cash you need at the closing table.

Pull your permits and finalize your plans before you apply - incomplete construction packages stall more files than any credit issue does.

Draw schedule, inspections, and final signoff

Funds move to your builder in scheduled draws tied to completed construction milestones. An independent inspector verifies each phase before the next draw releases, which protects both you and the lender.

What fees to compare across lenders

Ask Arbor for a written Loan Estimate that breaks out origination fees, draw inspection charges, and extension fees if your build timeline runs long. Then compare those line items directly against at least two other lenders before you commit.

5. Veterans Lending Group

Veterans Lending Group positions itself as a VA-specialized lender with a focus on helping veterans navigate construction financing. Their program sits among the more focused va construction loan lenders in the market because they concentrate on VA products rather than spreading across conventional and FHA lines.

One time close focus and what that means

Their primary product is a one-time close construction-to-permanent loan, which means you sign one set of documents covering both the construction phase and the long-term mortgage. You lock in your permanent rate at the initial closing, which eliminates the uncertainty of floating rates through a 6- to 12-month build.

A one-time close structure protects you from rate changes that could shift your payment significantly if the market moves during construction.

Best fit borrowers and use cases

This lender fits veterans and active-duty borrowers building a single-family primary residence with a licensed contractor already selected. Borrowers with stable W-2 income and a clear project budget tend to move through underwriting faster.

Builder screening and documentation checklist

Your builder needs a current state license and general liability insurance, plus a fixed-cost construction contract before Veterans Lending Group will open your file. Prepare these documents before you apply to avoid delays.

- Builder's license and insurance certificates

- Signed fixed-price construction contract

- Finalized architectural plans and project timeline

How to plan for contingencies and cost overruns

Build a 10 to 15 percent contingency buffer into your project budget before closing, because most lenders will not increase your loan mid-construction if costs rise unexpectedly.

What to ask about underwriting and timelines

Ask for their average underwriting timeline and confirm whether they process your file in-house or through a third-party underwriter, since that detail directly affects how soon your build can start.

6. Navy Federal Credit Union

Navy Federal Credit Union is one of the largest credit unions serving the military community, but their position among va construction loan lenders is more limited than their name recognition suggests. Understanding what they actually offer prevents you from spending weeks on an application that won't close.

VA construction loan availability and alternatives

Navy Federal does not consistently offer a one-time close construction-to-permanent VA loan. Your most realistic path through them involves securing a separate construction loan and then refinancing into a permanent VA mortgage once the build completes.

- Confirm their current product lineup directly before applying

- Ask about construction-only loans they may offer as a short-term bridge

Best fit borrowers who already bank with them

This option works best if you already have an established banking relationship with Navy Federal and plan to keep your permanent mortgage there long-term. Their service reputation is strong, but that strength shows most during repayment, not during construction draws.

Membership, eligibility, and COE notes

You must qualify for Navy Federal membership before applying for any product. Membership covers active-duty military, veterans, Department of Defense employees, and immediate family members. Confirm your Certificate of Eligibility before starting any application.

Membership approval does not guarantee loan approval - confirm their current construction products before committing to any timeline.

How to compare their terms to brokered options

Request a written Loan Estimate and compare rates, fees, and draw flexibility against at least two brokered lenders. A broker often surfaces better construction-phase terms than a single institution can offer.

Questions to ask to confirm they will fund draws

Ask directly whether they fund construction draws in-house or require a separate lender for the build phase, because that answer changes your entire financing strategy.

7. PenFed Credit Union

PenFed Credit Union serves military members and their families with a range of mortgage products, but their position among va construction loan lenders stays limited. Verify what they actually fund for new construction before you invest time in a full application.

VA construction loan availability and alternatives

Their one-time close construction-to-permanent VA loan availability is inconsistent across markets and changes over time. If that product is not available in your state, your most realistic path involves pairing a short-term construction loan with a separate VA mortgage once the build completes.

Best fit borrowers and credit profile expectations

PenFed works best for borrowers with credit scores above 680 who already hold membership and primarily need a permanent VA mortgage after a separate construction phase. Borrowers expecting a true single-close structure may find better options through a broker.

Confirm their current construction product availability in your state before gathering documents, because their offerings vary by location and can shift.

Fees, rate structure, and lock considerations

Request a written Loan Estimate that itemizes origination fees and any rate lock extension charges if your build runs past the scheduled completion date. Compare those line items directly against at least two other lenders before you commit.

What to confirm about land and construction timelines

Ask whether PenFed allows you to roll land purchase costs into the loan and what their maximum construction phase length is. Some lenders cap the build period at 12 months, which may not fit a larger custom project.

How to apply and what documents to prepare

Start by verifying your membership eligibility and requesting their current construction product sheet. Then assemble these items before submitting anything formal:

- Builder's license and general liability insurance certificate

- Signed fixed-cost construction contract

- Your Certificate of Eligibility

8. USAA

USAA serves active-duty military, veterans, and their families with a range of financial products, but their standing among va construction loan lenders is narrow. They do not consistently offer a one-time close construction-to-permanent VA loan, so confirm what they currently fund before building your timeline around them.

VA construction loan availability and common paths

USAA's primary strength sits in permanent VA mortgages, not construction financing. The most realistic path involves completing your build with a separate construction lender, then using a USAA VA loan to pay off the construction debt at completion.

Best fit borrowers and what USAA does well

This approach works best for existing USAA members who already trust the institution and want to consolidate banking and mortgage under one roof. Their service record is strong, particularly for borrowers who want a smooth permanent loan experience after the build phase ends.

How to pair a construction loan with a VA takeout plan

Line up your construction lender and your permanent VA lender before you break ground. Confirm that USAA will issue a commitment letter covering the takeout loan so your builder and construction lender have written confirmation of the exit plan.

Getting a written commitment from your permanent lender before construction starts removes the biggest risk from a two-close strategy.

Key risks to avoid before you break ground

Never assume your permanent loan approval carries over automatically after construction. Changes in your income, credit, or the appraisal can affect the final approval.

What to ask to avoid surprises at conversion

Ask USAA directly how long their VA loan commitment stays valid and what triggers a full re-underwrite when you convert from construction to permanent financing.

9. Guild Mortgage

Guild Mortgage is a national retail lender with a large branch network, and their offering among va construction loan lenders depends heavily on which loan officer and regional office you work with. Their product availability is not uniform across the country, so confirming what your local branch actually funds matters before you apply.

VA construction loan availability and what varies by branch

Guild offers VA loans broadly, but their construction-to-permanent product availability shifts by state and branch. Some offices handle one-time close builds actively, while others route borrowers toward a two-close strategy instead. Call your local branch directly and ask which structure they funded most recently.

Best fit borrowers including nontraditional scenarios

Guild has a reputation for working with borrowers who have thinner credit files or nontraditional income, which makes them worth contacting if other lenders have pushed back on your profile. Their loan officers vary significantly in experience, so finding one with direct construction loan closings on their record matters more than the brand name itself.

The loan officer you work with at Guild matters more than Guild's national product lineup, so ask specifically about their construction experience.

Underwriting items that commonly decide approvals

Your builder's documentation and the appraisal value of the completed home carry the most weight in underwriting. Gaps in the construction contract or a low appraisal stop more files than credit issues do.

Builder, budget, and appraisal basics

Bring a fixed-cost contract and finalized plans before you apply, because incomplete construction packages stall Guild files consistently.

How to shop Guild against other lenders

Request a written Loan Estimate and compare origination fees, rate lock terms, and draw inspection costs against at least two other lenders before you commit to any single option.

10. Veterans United Home Loans

Veterans United Home Loans is one of the largest VA mortgage lenders in the country by volume, but their strength sits in permanent VA mortgages rather than construction financing. Understanding that distinction before you apply saves you weeks of wasted effort as one of your searches for va construction loan lenders.

How they fit into new builds if they do not fund construction

Veterans United does not consistently offer a one-time close construction-to-permanent loan. Most borrowers use them as the permanent VA lender after completing their build through a separate construction lender, which means you are managing two loan relationships instead of one.

Best fit borrowers using construction then VA refinance

This two-step path works best for veterans with stable income and strong credit who can qualify for a short-term construction loan on their own and then convert to a permanent VA mortgage once the project finishes.

When a VA cash out refinance may apply after construction

If you build using conventional or hard money financing, a VA cash-out refinance can pay off that construction debt once the home appraises at completion. This only works when you have sufficient appraised equity to cover the payoff balance.

Confirm your exit financing strategy before you break ground, because a surprise at the permanent loan stage can stall your entire project.

Seasoning, occupancy, and appraisal checkpoints to plan for

VA lenders require occupancy confirmation and a completed appraisal before they fund the permanent loan. Ask Veterans United directly whether they require a seasoning period after construction closes before your file moves forward.

How to coordinate your builder, construction lender, and VA lender

Collect written commitments from all three parties before construction begins. Confirm that your builder's completion timeline and your construction loan maturity date both line up with Veterans United's closing window so nothing expires mid-project.

Quick next steps

Finding the right va construction loan lenders comes down to one thing: matching your specific scenario to a lender whose guidelines actually fit your deal before you submit an application. Start by gathering your Certificate of Eligibility, your builder's license and insurance documents, and a fixed-cost construction contract, because those three items decide whether a lender can open your file or not.

From there, request a written Loan Estimate from at least two lenders and compare origination fees, rate lock terms, and draw inspection costs line by line. Your builder's timeline and your loan's maturity date need to align or your project stalls at the worst possible moment. If you want an experienced set of eyes on your scenario before you apply anywhere, connect with David Roa to review your eligibility, your builder's credentials, and your best financing path without wasting a credit inquiry.