VA Loan Inspection Requirements: Appraisal, MPRs & Checklist

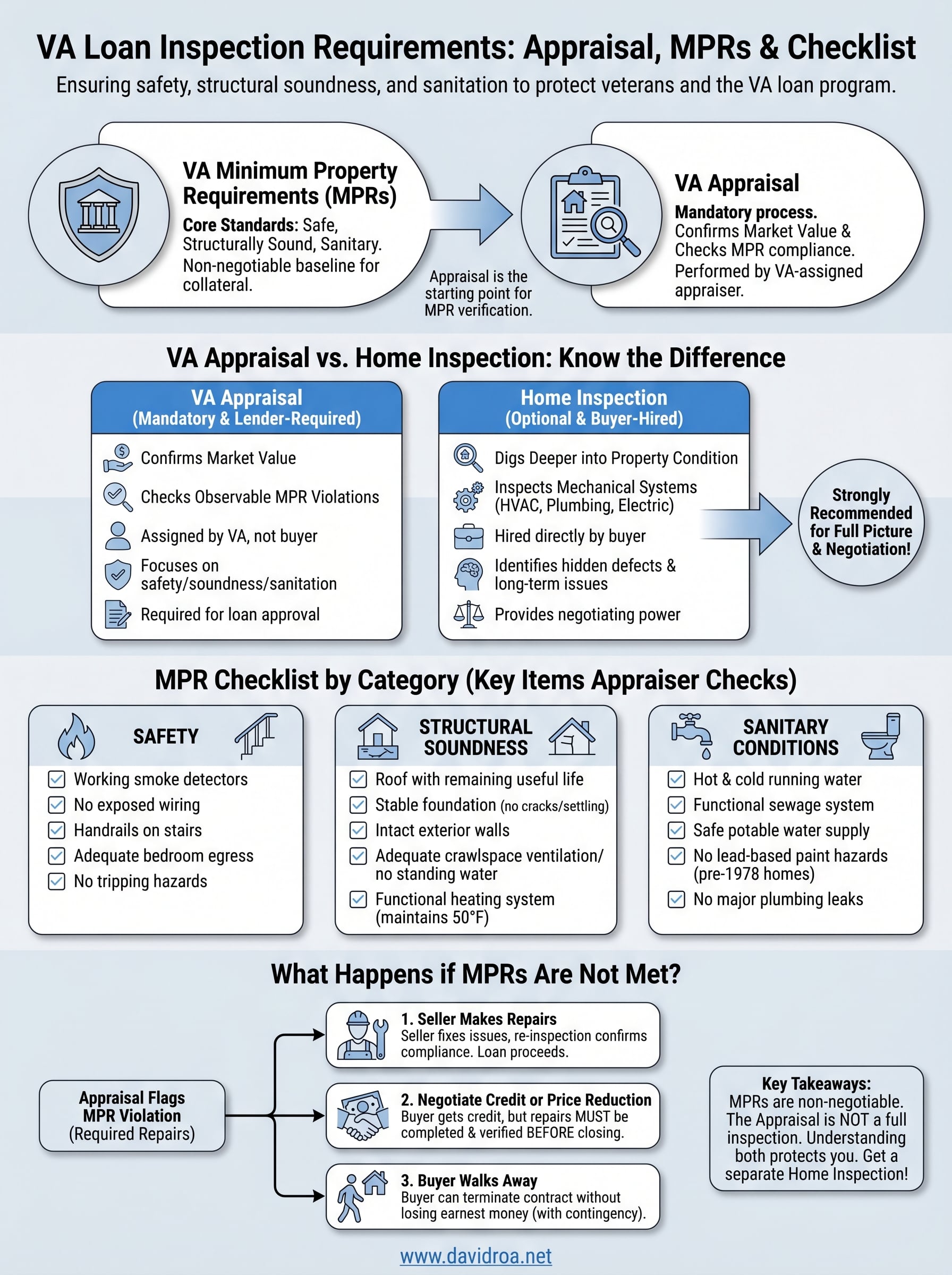

If you're using your VA loan benefit to buy a home, the property itself has to pass a set of standards before the Department of Veterans Affairs will back the loan. These are called Minimum Property Requirements (MPRs), and they exist to protect you from buying a home with serious safety, structural, or sanitary issues. Understanding VA loan inspection requirements before you start house hunting saves you time, money, and a lot of frustration at the closing table.

One of the biggest points of confusion for VA buyers is the difference between a VA appraisal and a home inspection. They're not the same thing. The VA appraisal is mandatory, it determines the home's market value and checks for obvious MPR violations. A home inspection is optional but strongly recommended, and it digs much deeper into the property's condition. Knowing what each one covers (and what it doesn't) puts you in a stronger position as a buyer.

With over 25 years originating VA loans and more than $150 million in funded transactions, I've walked hundreds of veterans and active-duty service members through this exact process at David Roa. This guide breaks down every MPR category, explains what the VA appraiser is actually looking for, and gives you a practical checklist so you know exactly what to expect, and what to watch out for, before you make an offer.

What VA loan inspection requirements really are

VA loan inspection requirements are not a single document or a one-time checkbox. They are a layered set of standards that the VA uses to determine whether a property is safe, structurally sound, and sanitary enough to serve as collateral for a government-backed loan. When you apply for a VA loan, your lender orders a VA appraisal through the VA's automated assignment system, and the appraiser is required to evaluate both the home's market value and its compliance with Minimum Property Requirements. If the property falls short on either front, the loan cannot close until those issues are resolved.

The appraisal is the starting point

Most buyers think of an appraisal as purely a valuation exercise, but with a VA loan, it does more than that. The VA appraiser is a licensed professional assigned by the VA, not chosen by you or your lender, and they follow the specific guidelines outlined in the VA Lenders Handbook. Their job is to document the home's condition, flag any visible deficiencies that violate MPRs, and assign a market value all in a single visit.

The VA appraiser can only flag what they can see during a standard walkthrough, which is exactly why getting a separate home inspection is so important.

Because the appraiser covers a lot of ground in a limited amount of time, they focus on obvious, observable problems rather than hidden systems or long-term maintenance concerns. Peeling paint on a pre-1978 home triggers a required repair. A roof that appears to be at the end of its useful life gets flagged. Standing water in a crawlspace stops the process entirely. These are the kinds of conditions the VA treats as dealbreakers, not cosmetic preferences.

What Minimum Property Requirements actually cover

MPRs are organized around three core principles: the home must be safe, structurally sound, and sanitary. That language comes directly from VA guidelines, and it shapes every item on the appraiser's checklist. The VA is not trying to help you find a perfect home. It is trying to make sure the home you're buying will not put you at financial or physical risk from the start.

Within those three categories, va loan inspection requirements cover a wide range of property conditions. Roofing, electrical systems, plumbing, heating, and foundation integrity all fall under structural soundness. Water supply, sewage disposal, and the absence of lead-based paint hazards fall under sanitary conditions. Safety covers working smoke detectors, adequate egress from bedrooms, and the absence of exposed wiring or hazardous materials.

How this differs from a standard conventional appraisal

A conventional appraisal focuses almost entirely on market value. The appraiser compares the home to recent sales in the area, adjusts for features and condition, and delivers a number. If the roof is failing, it might lower the appraised value, but it does not automatically stop the loan from closing. With a VA loan, a flagged MPR violation creates a mandatory repair requirement before the loan can fund, regardless of the agreed purchase price.

That distinction matters a lot when you're making an offer on a home. A property priced below market because it needs work might look like a deal, but if that work involves MPR violations, you're looking at required repairs before closing, a renegotiated purchase price, or a lost transaction. Knowing this ahead of time helps you evaluate any home with realistic expectations before you're in the middle of a contract.

Why the VA has minimum property requirements

The VA created Minimum Property Requirements for one straightforward reason: it does not want veterans using their hard-earned benefit to buy a property that becomes a financial or physical liability. When the VA backs your loan, it assumes risk on your behalf. Ensuring the home meets a baseline standard of safety, soundness, and sanitation protects both you and the integrity of the loan program itself.

The VA is protecting the veteran, not just the loan

A lot of buyers assume MPRs exist to protect the lender, but that framing misses the point. The VA loan program was built to give veterans access to homeownership on favorable terms, and that mission falls apart if veterans end up in homes with failing foundations or contaminated water supplies. The VA's position is that a home must be livable from day one, not a project that requires immediate out-of-pocket spending after closing.

VA loan inspection requirements are a form of consumer protection built directly into the loan program, so you don't have to rely solely on seller disclosures or your own knowledge to spot serious problems.

This matters especially for first-time buyers and veterans relocating to unfamiliar markets. The MPR framework gives you a guaranteed second set of eyes on the property's core condition, even if you never order a separate inspection. That built-in protection is one of the most underappreciated advantages of the VA loan program.

Property condition directly affects long-term financial stability

A home with structural problems, an inadequate heating system, or a roof at the end of its life is not just a safety concern. It is a financial risk that can drain your savings within the first few years of ownership. The VA understands that a veteran who buys a deteriorating home and then faces $20,000 in emergency repairs is in a worse financial position than before they purchased. MPRs are designed to reduce that outcome.

Lenders are also protected in the process, since a home in poor condition loses value quickly and can become difficult to sell if foreclosure ever becomes a factor. The VA's guarantee only holds up when the underlying collateral is sound. That shared interest between you, your lender, and the VA is exactly why minimum property standards are non-negotiable, not a formality you can waive with a signed disclosure.

VA appraisal vs home inspection and what each covers

The VA appraisal and a home inspection are two entirely different processes, but buyers often treat them as the same thing. The VA appraisal is required by your lender and assigned through the VA's system, while a home inspection is entirely optional and hired directly by you. Understanding the line between them helps you use both tools effectively, rather than assuming one covers what the other is actually doing.

What the VA appraisal covers

The VA appraiser's primary job is to confirm the home's market value and verify that it meets Minimum Property Requirements during a single walkthrough. They are not there to give you a full picture of the property's mechanical systems or long-term maintenance needs. Their scope covers observable conditions that would violate MPR standards, including exposed wiring, missing handrails on stairs, roof deterioration, and visible water intrusion. When the appraiser spots something that qualifies as a violation, it gets documented in the appraisal report and becomes a required repair before your loan can close.

The VA appraiser works for the loan process, not for you personally, which is why their report is not a substitute for an independent inspection.

| Element | VA Appraisal | Home Inspection |

|---|---|---|

| Required by lender | Yes | No |

| Confirms market value | Yes | No |

| Checks MPR compliance | Yes | No |

| Inspects mechanical systems | No | Yes |

| Buyer selects the professional | No | Yes |

| Identifies hidden defects | No | Yes |

What a home inspection covers

A home inspection goes far deeper than what va loan inspection requirements mandate from the VA appraiser. A licensed home inspector tests systems and components the appraiser is not there to evaluate, including HVAC performance, plumbing pressure, electrical panel condition, water heater age, and the function of windows and doors throughout the property. You pay for this out of pocket, typically between $300 and $500 depending on property size and your market.

Hiring an inspector gives you negotiating power that the appraisal alone cannot provide. If the inspector finds the HVAC unit is at the end of its service life or the electrical panel has documented safety issues, you can request a seller credit, a price reduction, or repairs before committing to the purchase. The VA appraisal confirms the home clears the minimum bar. The home inspection tells you everything that sits above it.

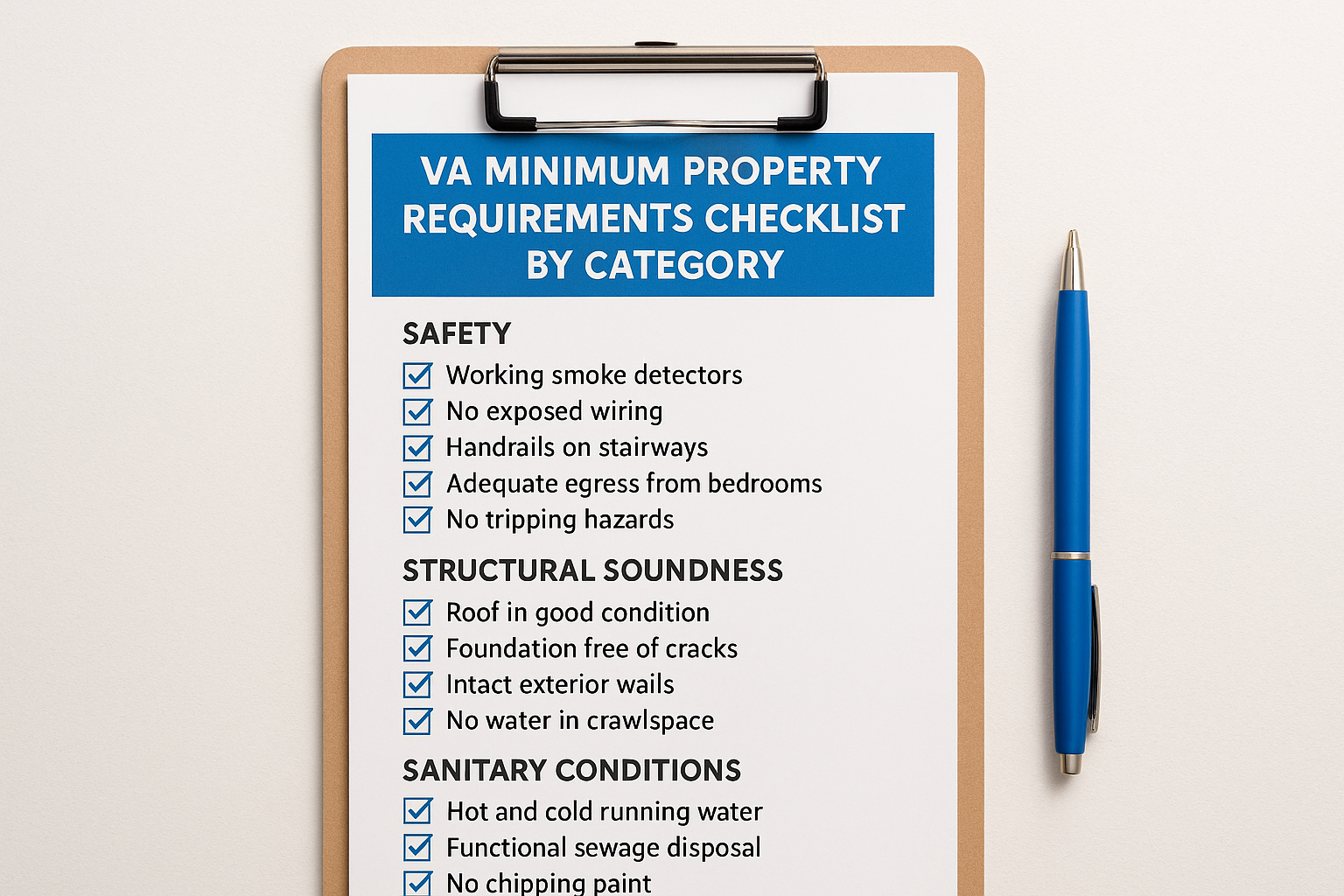

VA minimum property requirements checklist by category

The three pillars of VA loan inspection requirements are safety, structural soundness, and sanitation. Every item the VA appraiser evaluates falls into one of these categories, and knowing what's on that list before you start touring homes helps you filter out properties that are likely to create problems at the appraisal stage.

Safety

Safety requirements focus on conditions that could cause physical harm to the occupants from the moment they move in. The VA appraiser checks each of the following during the walkthrough:

- Working smoke detectors on every level of the home

- No exposed or frayed wiring anywhere in the property

- Handrails present on all stairways with more than one or two steps

- Adequate egress from all bedrooms, including windows that open fully

- No tripping hazards created by broken steps, damaged flooring, or deteriorating walkways

- No evidence of pest infestation, including visible termite damage

If any single safety item above is flagged, the VA appraiser will list it as a required repair, and your loan cannot close until it is corrected.

Structural soundness

Structural requirements address the physical integrity of the home itself, from the foundation through the roof. A structurally deficient home loses value quickly and creates serious risk for long-term owners.

- Roof must have remaining useful life and show no evidence of active leaking

- Foundation must be free of significant cracking, settling, or water intrusion

- All exterior walls must be intact with no major gaps or deterioration

- Crawlspaces must have adequate ventilation and no standing water

- The home must have a functional, permanently installed heating system capable of maintaining 50 degrees Fahrenheit in all living areas

- Basement and attic spaces must show no signs of structural compromise

Sanitary conditions

Sanitary requirements ensure the home delivers safe, functional, and code-compliant water and waste systems. These are non-negotiable because they directly affect the health of everyone living in the property.

- Hot and cold running water must be available in kitchens and bathrooms

- The sewage disposal system must be functional and properly connected to the municipal sewer or a compliant septic system

- Homes built before 1978 require all chipping or peeling paint to be addressed, since it may contain lead

- The property must have a safe, potable water supply with no visible contamination risk

- No evidence of major plumbing leaks or non-functioning fixtures

Running this checklist against any home you are seriously considering gives you a fast read on whether the property is likely to clear the VA appraisal without complications.

What can make a home fail the VA appraisal

The VA appraisal is not designed to be difficult to pass, but certain property conditions create automatic flags that stop a loan from closing. Most of these issues are visible during a standard walkthrough, which means the appraiser does not need to dig into walls or pull up flooring to spot them. Knowing the common failure points helps you evaluate a property with realistic expectations before you're locked into a purchase contract.

Roof and structural deficiencies

A deteriorating roof is the single most common reason a VA appraisal comes back with required repairs. The VA appraiser evaluates whether the roof has remaining useful life, and if it shows active leaking, significant missing materials, or visible sagging, it becomes a required repair item. You do not need a complete roof failure for this to be flagged. A roof that looks like it has two years left is enough for an appraiser to document it as a deficiency under va loan inspection requirements.

Foundation problems create some of the most serious flags because they affect the entire structure. Significant cracking, uneven settling, or water intrusion at the foundation level signals long-term instability. Crawlspaces with standing water get flagged immediately, and homes without adequate crawlspace ventilation face the same outcome. These are not negotiable repairs that sellers can defer until after closing.

If structural issues appear in the appraisal report, your lender cannot move forward until a licensed contractor completes the required work and the appraiser re-inspects the property.

Hazardous conditions inside the home

Lead-based paint is a mandatory concern for any home built before 1978. If the appraiser spots chipping, peeling, or flaking paint anywhere on the property, including exterior surfaces, it gets documented as a required repair. The seller is typically responsible for stabilizing or removing the affected paint before the loan can close, which can create friction in negotiations if the seller was not expecting that requirement.

Exposed wiring, missing GFCI outlets near water sources, and inoperable electrical panels all trigger appraisal flags. The VA treats visible electrical hazards as immediate safety risks, not deferred maintenance items. Non-functional heating systems also fail the appraisal in most climates, since the VA requires a heating system capable of maintaining 50 degrees Fahrenheit in all living spaces. If a property relies solely on wood-burning stoves or portable heaters, the appraiser will document the absence of a permanently installed system as a violation.

What happens if the home does not meet MPRs

When a VA appraiser documents an MPR violation, your loan goes on hold until that issue is resolved. The appraisal report lists each deficiency as a required repair, and your lender cannot submit the file for final approval until the VA confirms the condition is corrected. This does not automatically kill your purchase, but it does add time, cost, and negotiation pressure to the transaction. How the situation gets resolved depends on the severity of the repairs and how willing the seller is to cooperate.

The seller makes the required repairs

The most common outcome is that the seller agrees to fix the flagged items before closing. This works smoothly when the repairs are minor, like stabilizing peeling paint or installing a missing handrail. Once the seller completes the work, your lender requests a re-inspection through the VA, and the same appraiser or another VA-assigned appraiser returns to confirm the repairs meet the standard. Only after that confirmation can your loan move forward toward closing.

Make sure any seller-completed repairs are done by a licensed contractor where required, since the appraiser will look for professional workmanship, not a quick patch job.

Larger repairs create more friction. If the roof needs replacement or the foundation requires structural work, the seller is facing a significant bill, and not every seller will agree to absorb that cost. This is where your agent's negotiation skills matter considerably, and where understanding va loan inspection requirements before making an offer becomes a real advantage.

You request a credit or price reduction instead

Some sellers prefer to lower the purchase price or offer a closing cost credit rather than manage repairs themselves. This approach gives you the cash to handle the repairs after closing, but it creates a complication: the VA appraiser still needs to confirm the property meets MPRs before your loan funds. A price reduction alone does not clear an MPR violation, which means you would need to complete and document the repairs before closing, not after.

You walk away from the deal

If the seller refuses to make repairs and will not negotiate on price, you have the right to walk away without losing your earnest money in most cases, as long as your purchase contract includes a VA loan contingency. Not every property is the right fit for a VA loan, and recognizing that early protects your time and your benefit. Moving on to a property that already meets MPR standards is far better than forcing a deal that stalls or falls apart at the finish line.

Key takeaways

VA loan inspection requirements come down to three non-negotiable standards: the home must be safe, structurally sound, and sanitary before the VA will back your loan. The mandatory appraisal handles MPR compliance and market value in one visit, but it is not a substitute for hiring your own inspector. A separate home inspection gives you the full picture on mechanical systems and hidden defects that the appraiser is not there to evaluate. Getting both protects you at the closing table and beyond.

When the appraisal flags an MPR violation, you have three paths: seller repairs, a negotiated credit, or walking away from the deal entirely. Each option carries real trade-offs, and knowing them before you make an offer keeps you in control throughout the transaction. If you're ready to move forward with a VA loan or want to talk through a specific property situation, connect with David Roa for guidance from a senior loan officer with over 25 years of VA lending experience.