What Is a Jumbo Loan? 2026 Limits, Rates & Rules For Buyers

When the home you want costs more than what standard mortgage programs allow, you enter jumbo loan territory. These loans exist specifically for properties that exceed conforming loan limits, and in 2026, that threshold sits at $806,500 for most U.S. counties (higher in designated high-cost areas). If you're shopping for a luxury home, a property in a competitive market, or simply a house that outpaces conventional limits, understanding how jumbo financing works becomes essential.

The rules for jumbo loans differ from standard mortgages in meaningful ways. Lenders take on more risk with these larger amounts since they can't sell them to Fannie Mae or Freddie Mac. That means stricter credit requirements, larger down payments, and more documentation. But it also means you gain access to financing that makes high-value properties possible, without needing to piece together multiple loans or drain your savings entirely.

This guide breaks down everything you need to know: current 2026 limits by location, how jumbo rates compare to conforming loans, and the specific qualifications lenders look for. With over 25 years in mortgage lending and more than $150 million funded across residential, commercial, and investment properties, I've helped buyers at every price point find the right financing structure. Whether you're a first-time jumbo borrower or expanding your real estate portfolio, you'll walk away knowing exactly what to expect and how to position yourself for approval.

What counts as a jumbo loan in 2026

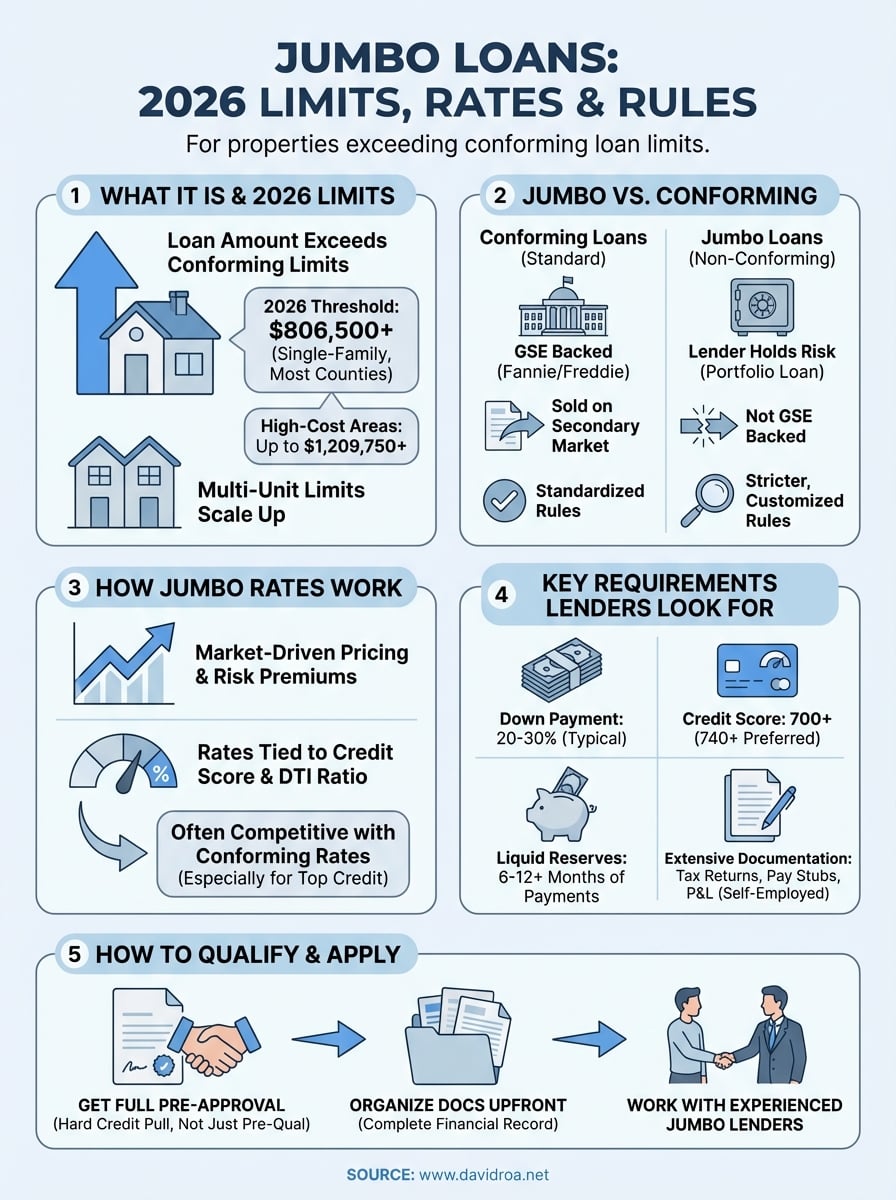

You cross into jumbo loan territory the moment your loan amount exceeds the conforming loan limit set by the Federal Housing Finance Agency (FHFA). For 2026, that baseline sits at $806,500 for single-family homes in most U.S. counties. Anything above this threshold requires jumbo financing because Fannie Mae and Freddie Mac won't purchase the loan, which fundamentally changes how lenders approach risk and pricing. Understanding what is a jumbo loan starts with knowing these exact numbers, since even a few thousand dollars over the limit triggers completely different underwriting standards.

The conforming limit doesn't stay fixed. It adjusts annually based on median home price changes across the country, which means the threshold tends to rise in strong housing markets. For 2026, the $806,500 baseline represents an increase from prior years, reflecting continued upward pressure in real estate values. If you're shopping in a market where homes routinely sell above this amount, you'll need to prepare for jumbo loan requirements from the start of your search.

Standard conforming limits across most counties

Most U.S. counties follow the baseline $806,500 limit for single-family homes in 2026. This applies to roughly 80 percent of the country, covering areas where housing costs align more closely with national averages. If you're buying in suburbs, smaller cities, or regions without extreme cost-of-living pressures, you'll work with this standard threshold. Loans at or below this amount qualify as conforming, which gives you access to more favorable terms, lower rates, and less stringent documentation requirements.

The limit scales upward for properties with multiple units. A two-unit property allows up to $1,032,500, a three-unit property reaches $1,247,850, and a four-unit property maxes out at $1,549,950. These figures matter if you're buying a duplex, triplex, or fourplex as an owner-occupied investment, where you live in one unit and rent the others. Each additional unit increases the conforming limit proportionally, giving you more room before triggering jumbo status.

High-cost area exceptions

Designated high-cost areas operate under different rules. In counties where median home values significantly exceed the national average, the FHFA sets higher conforming limits to reflect local market conditions. For 2026, these limits can reach as high as $1,209,750 for single-family homes in the most expensive markets. You'll find these elevated thresholds in places like San Francisco, Los Angeles, New York City, and parts of Colorado and Hawaii, where even modest homes routinely surpass baseline conforming limits.

High-cost area limits exist to prevent borrowers in expensive markets from automatically needing jumbo loans for properties that represent average local inventory.

Lenders in these regions use the adjusted limits when determining loan type. If you're buying a $900,000 home in San Mateo County, California, where the limit sits above $1.2 million, you still qualify for conforming financing. The same home in a standard-limit county would require jumbo financing. This geographic distinction directly affects your rate, down payment, and approval odds, which is why checking your specific county's limit before you start shopping saves confusion later.

How to check your county's specific limit

You need to verify your exact county limit before making assumptions. The FHFA publishes an official lookup tool on their website that lets you search by county and state to find the current conforming loan limit. This takes under a minute and removes any guesswork about whether your target price range requires jumbo financing. Real estate agents and lenders can also provide this information, but checking directly ensures you're working with accurate, current data.

County lines matter more than you might expect. Two neighboring counties can have vastly different limits if one qualifies as high-cost and the other doesn't. If you're considering homes in multiple counties, you may find that staying within a specific boundary keeps you in conforming territory while crossing it pushes you into jumbo range. This knowledge helps you make strategic decisions about where to focus your search based on financing realities, not just property preferences.

Jumbo vs conforming loans and why it matters

The core difference between jumbo and conforming loans comes down to government-sponsored enterprise (GSE) backing. Conforming loans meet the size and underwriting standards set by Fannie Mae and Freddie Mac, which allows lenders to sell those mortgages on the secondary market. Jumbo loans exceed those limits, which means lenders hold the risk entirely on their books or sell them through private channels. This fundamental distinction ripples through every aspect of how these loans work, from rates and requirements to approval timelines and flexibility.

Understanding what is a jumbo loan versus a conforming option matters because it directly impacts your borrowing costs and qualification hurdles. When lenders can't offload the loan to Fannie or Freddie, they compensate for the added risk by tightening standards. You'll face higher credit score minimums, larger down payment requirements, and more rigorous income verification. The tradeoff is that you gain access to financing amounts that conforming programs simply can't support, which becomes essential when you're targeting properties in competitive or high-cost markets.

Portfolio lending creates different rules

Jumbo loans typically function as portfolio loans, meaning the lender keeps them as assets rather than selling them immediately. This changes the dynamic between you and the institution. Lenders have more flexibility to adjust terms since they're not bound by GSE requirements, but they also scrutinize your financial profile more carefully because they're assuming all default risk. You might encounter stricter debt-to-income ratios, mandatory reserve requirements, or unique documentation requests that wouldn't appear with conforming financing.

Portfolio status also means lenders can customize solutions for complex situations. If you have significant assets but irregular income, relationship banking becomes valuable. Some institutions offer better jumbo terms to clients who maintain substantial deposits or investment accounts with them. This personalized approach doesn't exist in the conforming space, where standardized guidelines dominate.

Lenders hold jumbo loans longer, which means they care more about your overall financial stability than just meeting minimum requirements.

Rate and cost differences you'll notice

Jumbo loans historically carried higher interest rates than conforming mortgages, sometimes by 0.25 to 0.75 percentage points. That gap has narrowed in recent years, and in some market conditions, jumbo rates actually run lower than conforming rates due to the high-credit-quality borrowers these loans attract. You'll still pay more in upfront costs though, with higher origination fees and appraisal requirements that reflect the increased loan amount and property value.

Closing costs scale proportionally. A 1 percent origination fee on an $850,000 jumbo loan costs $8,500 compared to $5,000 on a $500,000 conforming loan. These differences compound when you factor in potentially higher insurance requirements and escrow reserves, making the total cost to close noticeably steeper even when rates look competitive.

How jumbo loan rates work

Jumbo loan rates follow market-driven pricing that reflects the added risk lenders assume when they can't sell your mortgage to Fannie Mae or Freddie Mac. You'll notice rates fluctuate based on broader economic indicators like Treasury yields, Federal Reserve policy decisions, and the overall health of the mortgage-backed securities market. Unlike conforming loans where rates cluster tightly around published benchmarks, jumbo rates vary significantly between lenders because each institution prices risk according to its own capital requirements and appetite for large-balance loans. This variability means shopping around becomes even more critical when you're pursuing jumbo financing.

Market conditions drive pricing

Lenders adjust jumbo rates daily based on investor demand for mortgage-backed securities and the cost of holding loans in portfolio. When bond markets experience volatility, jumbo rates typically rise faster than conforming rates because lenders need higher returns to justify keeping larger loans on their balance sheets. You'll see the most competitive pricing during periods of economic stability, when institutions feel confident about borrower performance and property values. Conversely, market uncertainty or rising default concerns push rates upward as lenders build in risk premiums to protect against potential losses.

The spread between jumbo and conforming rates narrows or widens based on these conditions. During stable markets with strong demand from high-net-worth borrowers, you might find jumbo rates matching or even beating conforming rates. Economic stress reverses this advantage quickly, sometimes pushing jumbo rates 0.50 to 1.00 percentage points higher within weeks.

Your credit profile determines your rate tier

Lenders tier jumbo rates based on credit score bands, with the best pricing reserved for scores above 740. Drop below 700, and you'll pay a rate premium that can cost thousands annually on a large loan balance. Your debt-to-income ratio also factors heavily into rate assignments, since lenders view lower ratios as stronger repayment capacity. Keeping your DTI under 43 percent positions you for better pricing, while ratios approaching 45 percent trigger rate increases or additional scrutiny.

Jumbo lenders reward pristine credit profiles with their sharpest rates because these borrowers represent the lowest default risk.

Loan-to-value ratio matters too. Putting down 25 percent instead of 20 percent often unlocks better rate tiers because you're reducing the lender's exposure. Some institutions offer their absolute best jumbo pricing only at 30 percent down or higher, treating these as premium-tier transactions. Understanding what is a jumbo loan means recognizing that your financial profile directly determines your cost of borrowing in ways that matter more than with smaller conforming mortgages.

Jumbo loan requirements lenders look for

Lenders impose stricter standards on jumbo loans because they carry the full risk without government backing. You'll need to demonstrate exceptional financial stability through multiple data points that go beyond what conforming loans require. Understanding what is a jumbo loan means accepting that approval hinges on proving you can handle large payments even during economic disruptions or income changes. Institutions scrutinize your entire financial profile, not just your ability to make the monthly payment, since they're protecting against default on loans that often exceed $1 million.

Credit score minimums

Most lenders set minimum credit scores at 700, though many prefer 740 or higher to offer their best terms. Scores below 680 typically disqualify you outright, and the few exceptions come with significantly higher rates and additional compensating factors like massive down payments or substantial liquid reserves. Lenders also examine your credit history depth, looking for established patterns of managing large credit lines responsibly over multiple years rather than just recent improvements.

Down payment expectations

You'll need at least 20 percent down for most jumbo loans, though many lenders push that requirement to 25 or 30 percent for loan amounts exceeding $1.5 million. Larger down payments reduce lender risk and often unlock better pricing tiers, making the extra cash investment worthwhile if you can manage it. Some institutions allow 10 to 15 percent down for exceptionally strong borrowers, but you'll pay premium rates and face additional reserve requirements that offset the lower equity position.

Lenders view your down payment as a direct measure of your commitment to the property and your ability to weather market downturns.

Income and asset documentation

Expect to provide two years of tax returns, pay stubs, W-2s, and detailed documentation of all income sources. Self-employed borrowers face even more scrutiny, often needing profit and loss statements reviewed by CPAs and evidence of business stability over multiple years. Lenders want to see consistent or growing income patterns, not fluctuations that raise questions about your ability to maintain payments during lean periods.

Reserve requirements

Most jumbo lenders require six to twelve months of mortgage payments in liquid reserves after closing. Higher loan amounts push this requirement toward the upper end or beyond, sometimes demanding 18 to 24 months for loans exceeding $2 million. These reserves must sit in accessible accounts like savings, checking, or taxable investment portfolios, not tied up in retirement accounts or real estate equity that can't quickly convert to cash.

How to qualify and apply without surprises

Applying for a jumbo loan requires more preparation than standard mortgages, but you can avoid setbacks by understanding what lenders need before you start. The process begins with honest assessment of your financial position against jumbo requirements: credit score above 700, down payment of 20 to 30 percent, debt-to-income ratio under 43 percent, and substantial liquid reserves. If you fall short in any category, address those gaps before initiating formal applications, since jumbo lenders reject borrowers who don't meet baseline standards regardless of property value or motivation.

Get pre-approved before you shop

You need full pre-approval, not just pre-qualification, before making offers on high-value properties. Pre-qualification relies on self-reported information and gives you rough estimates, while pre-approval involves hard credit pulls, income verification, and asset documentation that produces an actual commitment letter. Sellers and listing agents take pre-approved buyers seriously because they know the financing has been vetted, which matters significantly in competitive markets where properties above jumbo thresholds attract multiple offers.

Start this process at least 60 to 90 days before you plan to submit offers. This timeline gives you room to address documentation requests, resolve credit issues, or adjust your target price range if pre-approval comes back lower than expected. Lenders can update pre-approval letters quickly once you find a property, but the initial review takes time when you're dealing with complex income structures or substantial asset portfolios.

Organize documentation upfront

Gather your complete financial record before contacting lenders: two years of tax returns including all schedules, recent pay stubs, W-2s, bank statements covering three to six months, investment account statements, and explanations for any large deposits or transfers. Self-employed borrowers add profit and loss statements reviewed by CPAs plus business bank statements that demonstrate consistent revenue patterns. Having this package ready accelerates underwriting and prevents the frustration of repeated document requests that delay closing.

Lenders process jumbo applications faster when you provide comprehensive documentation upfront rather than responding piecemeal to underwriter requests.

Work with experienced jumbo lenders

Choose institutions with proven jumbo loan expertise rather than defaulting to whoever handled your last mortgage. Not all lenders offer jumbo products, and those that do vary significantly in their appetite for large-balance loans, portfolio lending capacity, and willingness to work with complex income scenarios. Understanding what is a jumbo loan from a lender's perspective helps you identify who can actually close your transaction versus who will waste weeks only to deny approval based on internal portfolio limits.

Ask potential lenders about their typical jumbo loan volume, average loan size they fund, and whether they portfolio loans or sell them immediately. These questions reveal whether you're dealing with a specialist or someone treating your application as an occasional exception to their standard business.

Next steps for jumbo homebuyers

You now understand what is a jumbo loan and how it differs from conforming financing in qualification standards, rates, and documentation requirements. The next move involves assessing your financial position against the benchmarks covered here: credit above 700, down payment funds totaling 20 to 30 percent, and reserves sufficient to cover six to twelve months of payments. If you meet these thresholds, contact specialized lenders who regularly fund large-balance loans and can provide accurate pre-approval based on your specific circumstances.

Properties above conforming limits require strategic financing partnerships with professionals who understand portfolio lending, investor scenarios, and the nuances of jumbo underwriting. Whether you're buying a primary residence, expanding your real estate portfolio, or upgrading to a higher-value property, the right guidance makes the difference between approval and rejection. Work with an experienced loan officer who has funded jumbo transactions and can navigate complex income structures or asset verification requirements that standard lenders often mishandle.