1031 Exchange Rules: Timeline, Deadlines, And Requirements

Selling an investment property at a profit sounds great, until the capital gains tax bill shows up. That's where 1031 exchange rules come into play. Named after Section 1031 of the Internal Revenue Code, this provision lets real estate investors defer taxes by reinvesting sale proceeds into a like-kind replacement property. But the process is strict, and missing a single requirement can disqualify the entire exchange.

Over 25 years of funding real estate deals, more than $150 million and counting, I've walked investors through every stage of this process. As a mortgage broker, active investor, and business owner, I've seen firsthand how a properly executed 1031 exchange can accelerate portfolio growth, and how a poorly planned one can cost investors tens of thousands in unexpected taxes. The rules aren't optional. They're the whole game.

This guide breaks down the timelines, deadlines, property requirements, and eligibility criteria you need to know before attempting a 1031 exchange. Whether you're flipping your first rental or restructuring a multi-property portfolio, understanding these rules upfront saves you from expensive surprises on the back end. Let's get into what the IRS actually requires, step by step.

What a 1031 exchange is and is not

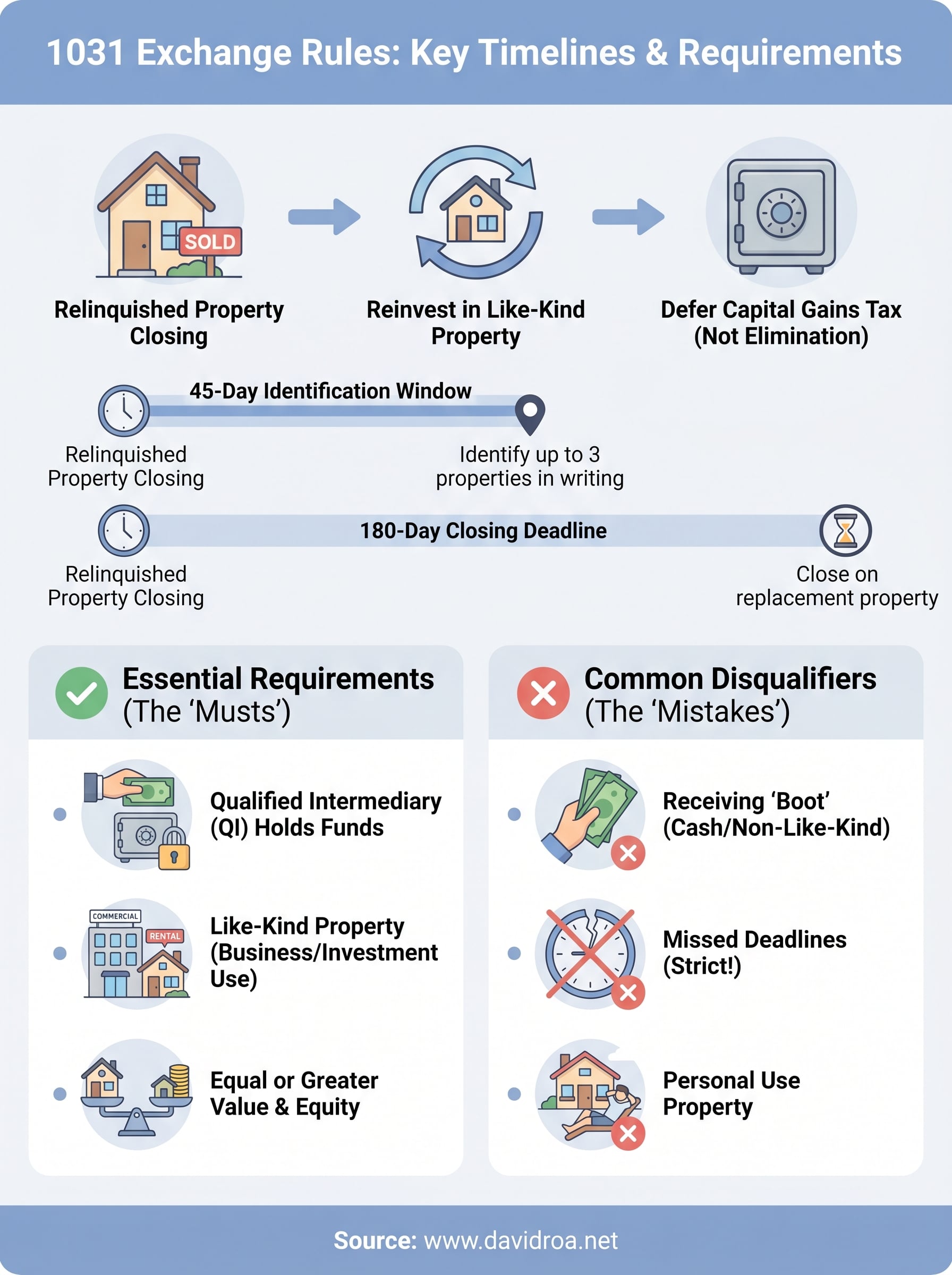

A 1031 exchange is a tax deferral strategy, not a tax elimination. When you sell a qualifying investment property and reinvest the proceeds into another qualifying property, the IRS lets you postpone paying capital gains tax on the sale. The tax doesn't disappear, but it moves forward in time, giving you more capital to work with today. This distinction matters because many investors expect a permanent tax break and end up surprised when they learn the bill eventually comes due if they sell the replacement property without completing another exchange.

The 1031 exchange is one of the few tools the IRS provides that lets you compound real estate wealth without surrendering a portion of each gain along the way.

What the exchange actually covers

The 1031 exchange rules apply specifically to real property held for business or investment purposes. That means rental properties, commercial buildings, raw land, and multi-family units all generally qualify. The IRS requires that both the property you sell, called the relinquished property, and the property you buy, called the replacement property, be held for productive use in a trade, business, or investment. If you use a property as your primary residence or hold it primarily for resale, it does not qualify under Section 1031.

Qualifying as "like-kind" is broader than most investors expect. You can exchange a single-family rental for a commercial building, or raw land for an apartment complex. The IRS defines like-kind as any real property located in the United States, provided both properties meet the investment or business use requirement. You do not need to swap properties of the same type, size, or value to satisfy this condition.

What does not qualify

Several common property types fall outside the scope of a 1031 exchange. Personal residences, vacation homes used primarily for personal enjoyment, stocks, bonds, partnership interests, and business equipment do not qualify as like-kind real property under Section 1031. Some investors assume a short-term rental or a property they occasionally use personally will qualify, but the IRS looks closely at your actual intent and documented use pattern when reviewing eligibility.

Receiving any cash or non-like-kind property during the exchange triggers a tax liability on that portion. The IRS calls this "boot," and it can catch investors off guard if they haven't structured the deal carefully. Avoiding or minimizing boot is one of the first planning steps you should work through with a qualified intermediary before you list your relinquished property for sale.

Why the rules matter for taxes and deal safety

The 1031 exchange rules aren't just paperwork requirements. They determine whether you walk away from a sale with your gains intact or hand a significant portion to the IRS immediately. Real estate investors who skip this process often face combined federal and state capital gains tax rates that can reach 30% or more on a profitable sale, depending on your income bracket and the state where the property is located.

The tax exposure you're trying to avoid

When you sell an investment property you've held for more than a year, the IRS classifies the profit as long-term capital gain. Federal rates on long-term gains currently sit at 0%, 15%, or 20% depending on your taxable income. But that's not the full picture. You also face depreciation recapture tax, which the IRS taxes at a flat 25% rate on any deductions you've claimed over the years. Add state taxes on top of that, and a single sale can trigger a bill that significantly shrinks the capital you have left to reinvest.

Depreciation recapture alone can cost investors tens of thousands of dollars if they sell without a structured deferral plan in place.

How a single misstep can derail the deal

Missing a deadline, receiving cash at closing, or purchasing a property that doesn't qualify can disqualify your entire exchange and trigger the full tax liability immediately. The IRS does not grant exceptions for miscommunication, deal delays, or poor planning. Every requirement exists for a specific reason, and the IRS reviews each transaction against those requirements without flexibility. Working with a qualified intermediary, a tax advisor, and an experienced lender before you close the relinquished property is the only way to protect both your tax deferral and your deal structure from the start.

1031 Exchange Timeline and Deadlines

The 1031 exchange rules give you a fixed window to complete your exchange, and the IRS does not extend it for any reason. From the day you close on the relinquished property, two hard deadlines control the entire process. Missing either one collapses your tax deferral and makes the full gain taxable in the year of the sale.

The 45-Day Identification Window

You have exactly 45 calendar days from the closing date of your relinquished property to identify potential replacement properties in writing. Your identification must be submitted to your qualified intermediary and follow one of three IRS-approved rules: the three-property rule, the 200% rule, or the 95% rule. Most investors use the three-property rule, which lets you identify up to three properties regardless of their total value.

Missing the 45-day deadline by even one day disqualifies your exchange entirely, with no appeals process available.

The 180-Day Closing Deadline

You must close on your replacement property within 180 calendar days from the same sale closing date, not from the end of the 45-day identification period. Both deadlines run simultaneously from day one, so you're working against two clocks at the same time. If your federal tax return for the sale year is due before the 180 days expire, you may need to file an extension to preserve the full window.

Securing your financing early is essential for protecting your timeline. Lenders need time to underwrite your replacement property loan, and delays on the lending side can eat into your 180-day window faster than most investors anticipate. Lining up your financing before you list the relinquished property puts you in the strongest possible position.

Key Eligibility and Documentation Requirements

The 1031 exchange rules set firm conditions on who can use the exchange and what paperwork the IRS expects to see. Skipping any of these requirements, even unintentionally, puts your tax deferral at risk and can trigger an immediate tax bill on the full gain from your sale.

Who Qualifies to Use the Exchange

Both individuals and entities can execute a 1031 exchange, including LLCs, partnerships, corporations, and trusts, as long as they hold the relinquished property for investment or business use. The IRS checks the ownership structure and intent on both the relinquished and replacement properties, so the taxpayer who sells must be the same taxpayer who buys. Transferring ownership between related parties before or after the exchange can raise red flags and invite closer scrutiny.

The IRS evaluates your intent at the time of purchase, so holding a property for at least one to two years before initiating an exchange strengthens your position significantly.

Documentation You Need Before and After Closing

Proper paperwork protects your exchange if the IRS ever reviews the transaction. You need to prepare and retain the following before and during your exchange:

- Exchange agreement signed with your qualified intermediary before you close on the relinquished property

- Written identification notice listing replacement properties, submitted within the 45-day window

- Closing statements for both the relinquished and replacement properties

- Form 8824, filed with your federal tax return for the year the exchange occurs

Your qualified intermediary holds the sale proceeds in a separate escrow account during the exchange period. You cannot receive or control those funds at any point without triggering full taxation on the gain.

Common Scenarios and Mistakes to Avoid

Even investors who understand the 1031 exchange rules well can stumble on execution. The most costly mistakes share a common thread: they all stem from poor timing or misunderstanding the structural requirements the IRS enforces at every stage of the transaction.

Starting the Search Too Late

Many investors close on their relinquished property and then begin looking for a replacement. That approach puts you in a weak negotiating position immediately. You have 45 days to identify and only 180 days to close, and sellers don't adjust their timelines for your exchange deadlines. The investors who succeed start identifying target properties before they even list the relinquished property. That preparation gives you real options instead of a scramble under deadline pressure.

Entering the 45-day window without a shortlist of replacement properties is one of the most common ways investors lose their tax deferral.

Receiving Proceeds Directly

Some investors attempt to handle the sale proceeds themselves and transfer funds later. The IRS treats any direct receipt of funds as a taxable event, ending the exchange immediately. You must designate a qualified intermediary before closing on the relinquished property, and that intermediary must hold the funds throughout the entire exchange period. You cannot have constructive access to the money at any point without forfeiting the deferral.

Buying Down in Value

Purchasing a replacement property at a lower price than the relinquished property triggers a taxable gain on the difference. This partial boot situation catches investors off guard when they assume any like-kind property will fully protect their deferral. Your replacement property must be equal or greater in value and fully funded with the exchange proceeds to defer the entire gain.

Next Steps for Your Exchange Plan

You now have a clear picture of what the 1031 exchange rules require, from the 45-day identification window to the documentation your qualified intermediary needs before your first closing. The next step is converting that knowledge into a concrete action plan before you list any property for sale. Identify your replacement property targets early, line up your financing, and select a qualified intermediary well before you need them. Each of those steps takes time, and the IRS timeline does not wait for anyone.

Working with an experienced lender who understands investment property financing makes a real difference when your 180-day clock is running. Whether you need a DSCR loan, a conventional investment property mortgage, or a commercial bridge product to fund your replacement property, the right financing partner keeps your deal on track. Reach out to discuss your investment financing options and build a plan that protects your tax deferral from day one.