1031 Exchange Timeline: IRS 45-Day & 180-Day Deadline Rules

Miss a single deadline in your 1031 exchange timeline, and the IRS treats your sale as fully taxable, no exceptions, no extensions. That's the reality investors face when executing a tax-deferred exchange, and it catches more people off guard than you'd expect. The rules are strict: 45 days to identify replacement properties and 180 days to close, both running from the moment you sell your relinquished property.

Having helped real estate investors secure over $150 million in funded transactions, I've walked clients through every phase of this process at David Roa. As a mortgage broker and active investor myself, I've seen firsthand how financing delays can collide with exchange deadlines, and what it takes to prevent that from happening.

This article breaks down each deadline in the 1031 exchange timeline, explains the IRS rules governing both windows, and covers the identification methods you can use to stay compliant. Whether you're planning your first exchange or your tenth, you'll walk away with a clear understanding of every critical date and how to work backward from each one.

Why the 1031 exchange timeline matters

A 1031 exchange lets you defer capital gains taxes on the sale of an investment property, but that deferral only holds if you follow the IRS rules precisely. The 1031 exchange timeline is not a guideline or a soft target. It is a strict legal requirement under IRC Section 1031, and the IRS provides no waivers, grace periods, or extensions under standard circumstances. Every day in the exchange window carries real financial weight, and understanding that upfront changes how you plan and execute each step.

The tax consequences of missing a deadline

If you miss either the 45-day or 180-day deadline, the IRS disqualifies the entire exchange. Your sale becomes immediately taxable in the year it closed, regardless of your intent to reinvest. A failed exchange can trigger:

- Federal capital gains tax of up to 20 percent on long-term gains

- Depreciation recapture tax at 25 percent on prior deductions claimed

- State income tax, which varies by location but can add several percentage points on top

Missing one deadline can wipe out years of investment gains in a single tax filing.

Why financing is the most common delay trigger

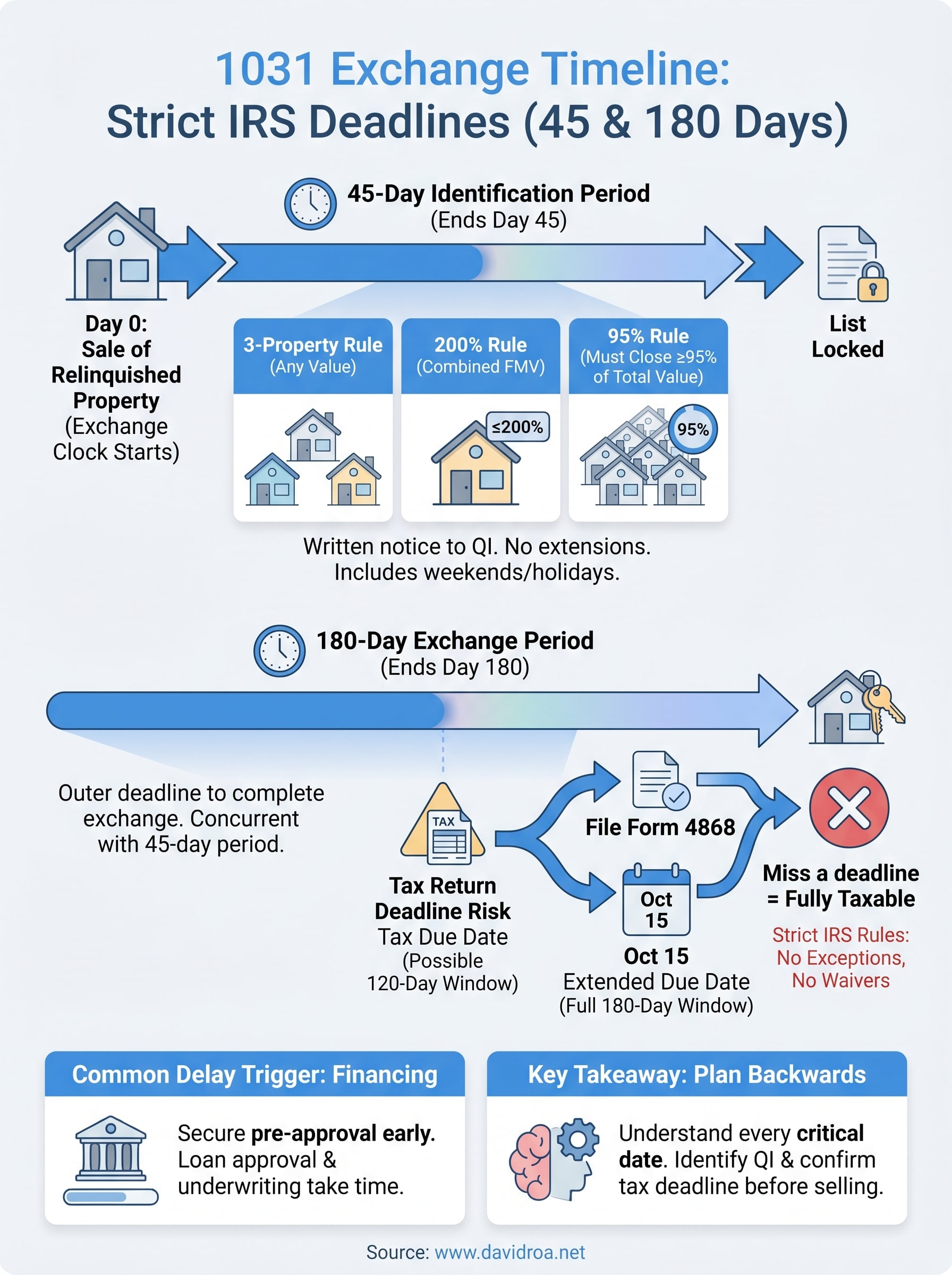

Most investors focus on finding the right replacement property but underestimate how long loan approval and closing actually take. Lenders need time to underwrite, appraise, and fund a new mortgage, and that process rarely moves at the speed an exchange demands. If your financing falls apart near the 170-day mark, you have almost no runway left before the 180-day window closes.

Working directly with investors on DSCR and investment property loans, I've seen deals collapse in the final weeks simply because financing was not secured early enough. Establishing lender relationships and pre-approvals before you close on the relinquished property is one of the most practical steps you can take to keep your exchange on track from start to finish.

The 45-day identification period explained

The 45-day identification period starts the day after you close on your relinquished property. You have exactly 45 calendar days to identify potential replacement properties in writing, and that written notice must go to your qualified intermediary or another party involved in the exchange. No verbal agreements count, and the IRS does not accept late submissions under any standard circumstances.

Your 45-day clock runs through weekends and holidays without a single pause.

The three identification rules

The IRS gives you three different methods to identify replacement properties within your 1031 exchange timeline, and you must follow at least one of them strictly. Choosing the right method depends on how many properties you plan to target and at what value.

- Three-Property Rule: You can identify up to three properties of any fair market value. This is the most straightforward approach and the one most investors use.

- 200% Rule: You can identify more than three properties, but their combined fair market value cannot exceed 200 percent of the relinquished property's sale price.

- 95% Rule: You can identify any number of properties at any total value, but you must actually close on at least 95 percent of that identified value within the 180-day window.

The 180-day exchange period and tax return deadline

The 180-day window runs concurrently with your 45-day identification period, starting the same day your relinquished property closes. You have 180 calendar days to close on one or more of your identified replacement properties. This is the outer boundary of your entire 1031 exchange timeline, and crossing it without closing means the exchange fails entirely.

If your 180th day falls on a weekend or holiday, the IRS does not automatically extend your deadline to the next business day.

The tax return deadline that can shorten your window

Your 180 days can actually shrink if your federal tax return due date falls before the 180th day of your exchange. The IRS requires you to complete the exchange by the earlier of 180 days or the due date of your tax return, including extensions, for the year in which you sold the relinquished property.

If you sold a property in December, your April tax filing deadline could cut your window to roughly 120 days. Filing for an extension using IRS Form 4868 pushes your return due date to October, which restores your full 180-day window in most cases and gives you the runway you need to close on the right property.

How to identify replacement property correctly

Identifying replacement property correctly means more than picking a property you like. Your written identification notice must include a clear description of each property, typically a legal description or street address, and it must be signed and delivered to your qualified intermediary before midnight on day 45.

A verbal agreement or informal email without the required details does not satisfy IRS identification requirements.

What your identification notice must include

Your identification notice needs to meet specific IRS standards to count as valid within your 1031 exchange timeline. Each property you list must be described with enough detail that there is no ambiguity about which property you mean. For most residential and commercial properties, a street address or legal property description satisfies this standard.

- Property address or legal description

- Signature from the exchanger

- Delivery to the qualified intermediary before the 45-day deadline

Changing your identified properties

Revising or revoking your identification list is allowed before the 45-day deadline passes, but once that window closes, your list is locked. Any property you attempt to close on that was not identified in writing during those 45 days will disqualify the exchange for that specific acquisition, even if you are otherwise within the 180-day window.

Timeline examples and a simple date calculator

Seeing the 1031 exchange timeline mapped to real dates makes the deadlines concrete and easier to plan around. The two most common scenarios investors face are a mid-year closing and a late-year closing, each carrying different risks depending on where the tax return deadline falls.

A late-year closing is the most dangerous scenario because the April tax filing date can compress your 180-day window to roughly 120 days.

Two real-world closing scenarios

The table below shows how your key deadlines shift based on your relinquished property closing date.

| Closing Date | 45-Day Deadline | 180-Day Deadline | Tax Return Risk |

|---|---|---|---|

| June 1 | July 16 | November 28 | None (April deadline passed) |

| December 1 | January 15 | May 30 | Yes (file Form 4868) |

How to calculate your own dates

Calculating your personal deadlines requires just two inputs: your closing date and your tax return due date. Start by adding 45 calendar days to your closing date to find your identification deadline. Then add 180 calendar days to that same closing date for your outer exchange deadline. Compare that result against your tax return due date and use the earlier of the two as your true cutoff.

Next steps

The 1031 exchange timeline gives you a clear framework, but meeting those deadlines consistently requires preparation that starts well before you close on your relinquished property. Identify your qualified intermediary early, understand which identification rule fits your situation, and confirm your tax return deadline so you know your true 180-day cutoff.

Financing is where most exchanges run into trouble, and getting your loan pre-approval in place before day one removes the biggest variable from your timeline. Whether you need a DSCR loan for a rental property, hard money for a fix-and-flip acquisition, or conventional financing for a larger replacement property, having the right lender lined up keeps your exchange on track.

Your next move is to connect with a lender who understands investment property financing and the time pressure that comes with an active exchange. Work with David Roa to get your loan structure in place before your relinquished property closes.