Apply For An Investment Property Loan: Steps & Requirements

Getting financing for an investment property isn't the same as buying a home you plan to live in. Lenders see more risk, which means higher down payments, stricter credit thresholds, and different documentation than what you'd face on a primary residence. If you're ready to apply for an investment property loan, understanding these differences upfront saves you time, money, and a lot of frustration.

Whether you're buying your first rental, scaling a portfolio, or funding a fix-and-flip, the application process has specific steps that trip up even experienced investors. From choosing the right loan product, conventional, DSCR, hard money, to gathering the paperwork lenders actually want to see, each decision affects your approval odds and your bottom line. With over 25 years in mortgage lending and more than $150 million funded, I've walked thousands of investors through this exact process at David Roa, including complex scenarios that traditional banks tend to pass on.

This guide breaks down the full process: eligibility requirements, loan options, and a step-by-step path from prequalification to closing. No guesswork, no filler, just what you need to move forward with a clear plan and the right financing in place.

Why investment property loans work differently

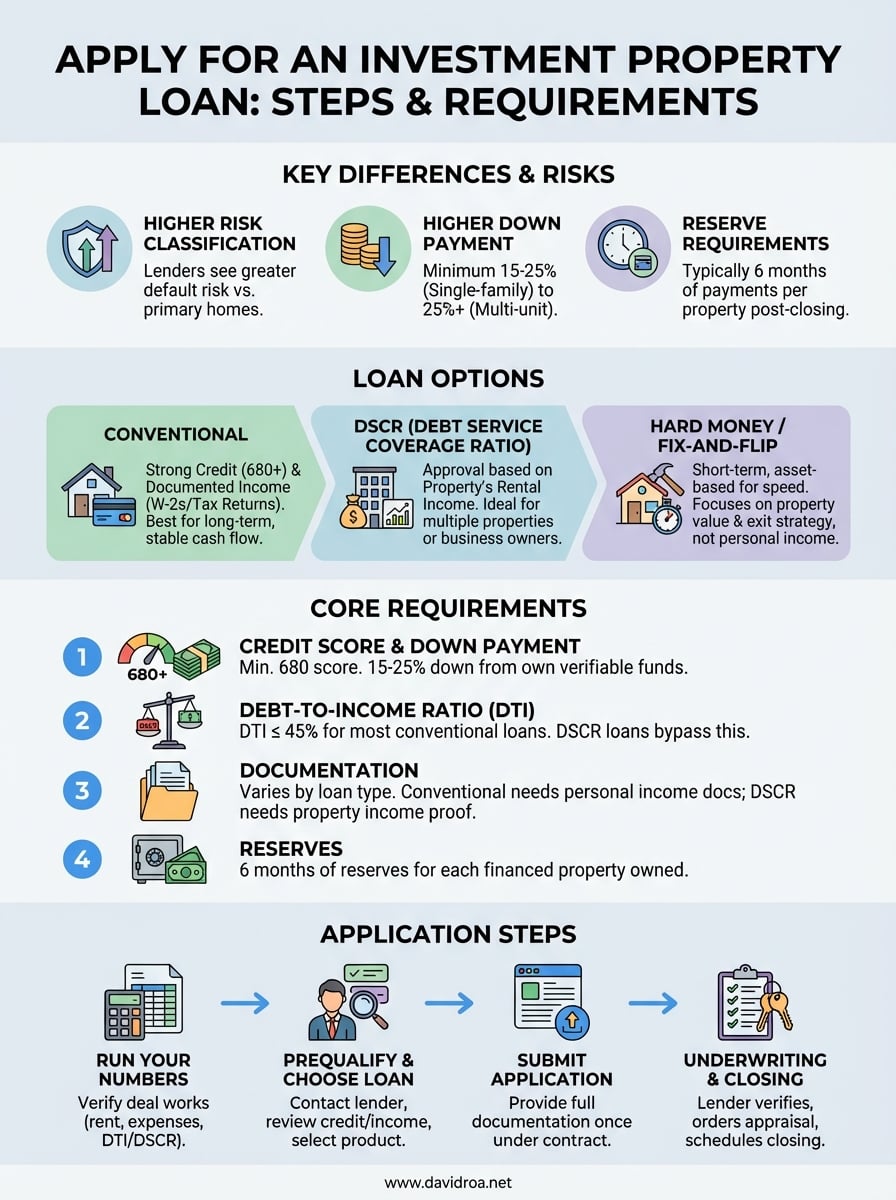

When you apply for an investment property loan, you're working within a completely different risk framework than a standard home purchase. Lenders classify investment properties as higher risk because if your finances get tight, you're statistically more likely to default on a rental than on the home where you live. That single assumption affects every part of the loan structure: your rate, your down payment requirement, your qualifying income, and how much cash you need to have sitting in reserve after closing.

Lenders price in higher risk from day one

Most investment property loans carry interest rates 0.5% to 0.75% higher than comparable owner-occupied loans. On a $400,000 loan, that spread adds meaningful money to your monthly payment and compounds over the life of the loan. Lenders also require a minimum down payment of 15% to 25% depending on the loan type, the property, and your credit profile. Single-family investment properties typically land at the lower end of that range, while two-to-four-unit properties often push higher.

The down payment on an investment property almost never comes from gift funds. Lenders want to see that the money is yours because it signals you have genuine financial commitment to the deal.

Beyond the upfront costs, most lenders require you to hold cash reserves equal to six months of mortgage payments for each investment property you own after closing. If you're building a portfolio, that reserve requirement stacks up fast and can become the actual limiting factor in your growth. This is one reason experienced investors often shift toward alternative loan products as they add properties.

How lenders evaluate income on investment properties

On a primary residence, lenders focus on your personal income, W-2s, and tax returns to verify you can carry the payment. Investment properties introduce a second layer: the income the property itself generates, or is projected to generate. How lenders treat that rental income varies significantly by loan type, and it matters more than most borrowers expect.

With a conventional loan, lenders typically allow you to count 75% of projected or actual rental income toward your qualifying income, discounting 25% to account for vacancies and maintenance costs. That sounds useful, but it can actually hurt you if the numbers don't come in high enough to offset the new debt payment. Some investors end up in a tighter qualifying position than they anticipated because the rental income credit doesn't move the needle enough.

DSCR loans operate on a completely different model. Instead of scrutinizing your personal income, the lender evaluates whether the property's rental income covers its own mortgage payment. A DSCR of 1.0 means the property breaks even; most lenders want 1.1 or higher to approve the loan. This structure works well for investors with complex tax returns or multiple existing properties, since your personal income largely stays out of the underwriting equation. Knowing which income model your target loan uses shapes everything from which documents you prepare to which properties actually make financial sense to pursue.

Investment property loan options you can apply for

When you apply for an investment property loan, the first decision is picking the right product for your situation. Each loan type carries distinct qualifying criteria, timelines, and cost structures, so choosing the wrong one early creates problems mid-process. Your property type, income situation, and investment timeline all point toward different options.

Conventional investment loans

Conventional loans are the most common entry point for investors with strong credit and documented personal income. Backed by Fannie Mae or Freddie Mac guidelines, these loans offer competitive rates and work well for single-family or two-to-four-unit rentals. You'll need at least 15% to 25% down and a credit score at or above 680.

These loans work best for buy-and-hold investors focused on building long-term, stable cash flow from rental income. The trade-off is that Fannie Mae caps financed investment properties at ten, so investors scaling quickly will hit that ceiling faster than expected.

Once you reach the conventional loan limit, DSCR and portfolio products become your primary path for adding more properties.

DSCR loans

DSCR loans base approval on the property's rental income rather than your personal earnings. If the monthly rent covers the mortgage payment at a ratio of 1.1 or higher, you clear the primary hurdle. No W-2s, tax returns, or employment history are required, which makes this product especially useful for self-employed investors and business owners with complex returns.

DSCR loans work well for:

- Investors with multiple existing properties

- Business owners who show lower taxable income due to deductions

- Anyone who wants to separate property performance from personal finances

Hard money and fix-and-flip loans

Hard money loans are short-term, asset-based financing built for speed, typically used on fix-and-flip projects or distressed properties that don't qualify for conventional underwriting. Lenders focus on the property's value and your exit strategy rather than personal income or credit history.

Rates typically run between 9% and 13%, and funding can close in days rather than weeks. That speed often makes hard money the only realistic option when a deal requires a fast close.

Requirements to qualify for an investment property loan

Before you apply for an investment property loan, lenders run your full financial profile through a stricter filter than they use for primary residences. Meeting the baseline thresholds on all key metrics is what separates a smooth approval from a stalled application. Understanding exactly what lenders look for lets you identify and fix weak spots before you submit anything.

Credit score and down payment

Most conventional investment property loans require a minimum credit score of 680, though lenders offer better rates and terms at 720 and above. A higher score doesn't just look good; it directly reduces your interest rate and can lower your required reserves. On the down payment side, expect to put down at least 15% for a single-family rental and 25% for a two-to-four-unit property. This money must come from your own verifiable funds, not gifts or borrowed sources.

Borrowers who arrive with 25% or more down on a single-family rental often unlock significantly better pricing and fewer lender conditions.

Debt-to-income ratio and reserves

Your debt-to-income ratio, or DTI, should sit at or below 45% for most conventional investment loans. Lenders calculate this by adding your total monthly debt obligations, including the new investment property payment, and dividing by your gross monthly income. DSCR loans bypass personal DTI entirely, but conventional products still require this calculation. Beyond DTI, lenders typically require six months of cash reserves for each financed property you own, which includes your primary residence if you carry a mortgage on it.

Documentation lenders expect

The paperwork requirements vary by loan type, but most lenders will ask for a consistent set of core documents. For conventional loans, prepare your last two years of tax returns, W-2s or 1099s, recent bank statements, and a signed purchase contract. If you're applying for a DSCR loan, replace personal income documents with a current lease agreement or a rental market analysis from an appraiser. Having these documents organized before you start the process speeds up underwriting and reduces back-and-forth requests.

How to apply for an investment property loan step by step

The process moves faster and smoother when you know exactly what each stage requires before you reach it. When you apply for an investment property loan, working through these steps in order prevents the most common delays and keeps your deal on track from the start.

Run your numbers before contacting a lender

Before you fill out a single form, verify that the deal actually works financially. Calculate your projected rent, estimate your expenses including taxes, insurance, and maintenance, and confirm the property will hit a DSCR of at least 1.1 if you're targeting a DSCR loan. For conventional financing, check that your current DTI stays below 45% after adding the new payment. Deals that look strong on paper before the lender review move through underwriting with far fewer surprises.

Investors who run this analysis first also negotiate better because they know their numbers cold before any conversation with a seller or lender.

Get prequalified and choose your loan product

Contact a lender to start the prequalification process. At this stage, the lender reviews your credit score, income documentation, and available assets to identify which loan products you qualify for and at what terms. Prequalification is not a full application, but it surfaces any issues early and gives you a concrete financing picture before you go under contract. Use this conversation to confirm which loan type, conventional, DSCR, or hard money, fits your investment strategy and timeline.

Submit your application and move through underwriting

Once you're under contract on a property, submit the full application with all required documentation. The lender orders an appraisal, verifies your financials, and confirms the property meets lending guidelines. Respond quickly to any underwriter requests for additional documents. Delays at this stage usually come from missing paperwork or appraisal issues, both of which you can reduce by preparing your documents in advance and choosing a property in solid condition. After underwriting clears, the lender issues a clear-to-close and schedules your closing date.

Common mistakes and key questions to ask lenders

Even experienced investors run into avoidable problems when they apply for an investment property loan. Knowing the most common errors in advance lets you sidestep the ones that delay closings or cost you the deal entirely.

Mistakes that stall or kill applications

The single most damaging mistake is waiting until you're under contract to check your finances. If your DTI is too high or your reserves fall short, you won't have time to fix either problem without losing the deal. A close second is applying to multiple lenders simultaneously without understanding how hard credit inquiries affect your score. Multiple pulls within a short window can lower your score enough to push you into a less favorable rate tier, which changes the math on the whole deal.

Changing jobs, opening new credit lines, or making large deposits without paper trails between application and closing are the fastest ways to trigger an underwriting hold.

Another common error is misrepresenting how you plan to use the property. Stating that a property will be owner-occupied when it won't is mortgage fraud. Lenders verify occupancy intent, and the consequences go well beyond a declined application.

Questions to ask before you commit to a lender

Once you've identified a lender, asking direct, specific questions before you submit anything protects you from surprises at closing. Use these questions in your initial conversation:

- What is the minimum DSCR or DTI you require for this specific loan product?

- How do you calculate rental income, and what documentation do you need to support it?

- What are your reserve requirements, and do they stack across all financed properties I currently own?

- What is your average time from application to closing, and what typically causes delays?

- Are there prepayment penalties, and if so, over what term?

A lender who answers these questions clearly and quickly is one you can work with efficiently. Vague or evasive answers at this stage are a reliable signal to keep looking.

Next steps

You now have a clear picture of what it takes to apply for an investment property loan, from picking the right product to gathering documentation and avoiding the mistakes that stall deals. The difference between investors who close quickly and those who don't usually comes down to preparation: knowing your numbers, having your paperwork ready, and working with a lender who understands the full scope of investment financing.

Your next move is to take action while the details are fresh. Pull your credit report, calculate your current DTI, and verify you have enough reserves to meet lender requirements. Once you know where you stand financially, you're ready to have a productive conversation with a lender who can match your goals to the right loan structure.

If you're ready to start that conversation, connect with David Roa for direct guidance on investment property financing backed by over 25 years of hands-on lending experience.