5 Best Commercial Bridge Loan Lenders Nationwide (2026)

A commercial bridge loan can mean the difference between closing on a time-sensitive deal and watching it slip away. Whether you're acquiring a new property, repositioning an asset, or need capital to bridge the gap until long-term financing kicks in, finding the right commercial bridge loan lenders matters more than most borrowers realize. Not all lenders move at the same speed, offer the same terms, or understand the nuances of short-term commercial financing, and those differences can cost you.

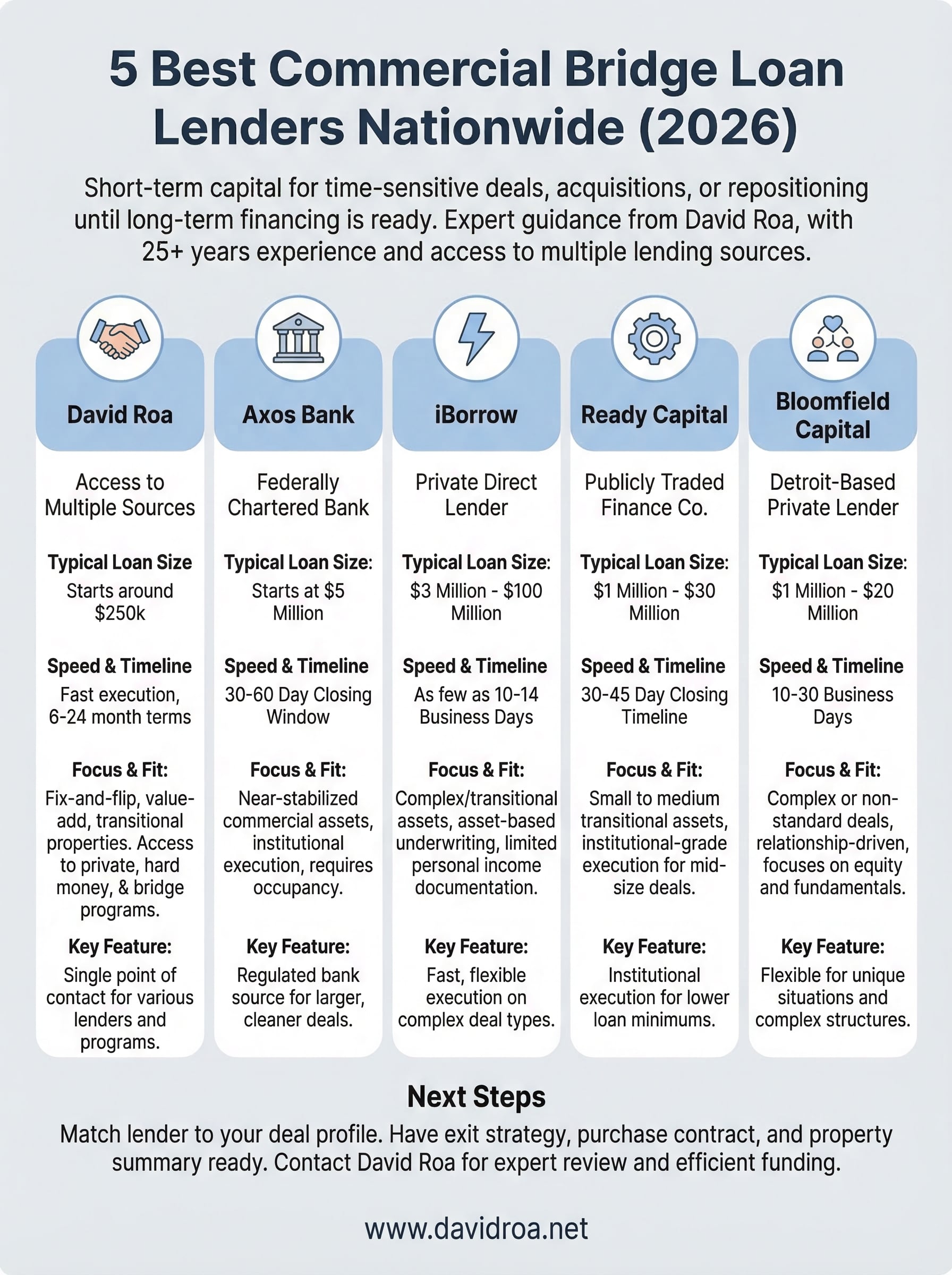

With over 25 years in mortgage lending and more than $150 million funded across residential, commercial, and investment deals, I've worked with (and alongside) many of the lenders on this list. At David Roa, we help business owners and real estate investors navigate these options daily, whether that's through our own lending programs or by connecting clients with the right capital source for their specific situation, including SBA financing, hard money, DSCR loans, and bridge products.

Below, I've put together a list of five reputable commercial bridge loan lenders operating nationwide in 2026. Each one brings something different to the table in terms of loan size, speed, and flexibility. The goal here is simple: give you enough detail to compare your options with confidence and move forward with the lender that fits your deal.

1. David Roa

Working with David Roa gives you access to multiple bridge lending sources through a single point of contact. Rather than approaching lenders cold, you get a broker with 25-plus years of commercial and residential lending experience who already knows which programs fit which deals.

Where bridge loans fit in your deal

Bridge financing works best when you need to move fast and your long-term financing isn't ready to close. That gap between acquisition and stabilization is exactly where short-term commercial capital plays a critical role in keeping your deal alive.

How David sources bridge lenders nationwide

David works with a national network of private lenders, hard money sources, and commercial bridge loan lenders to match your deal with the right capital. Every scenario gets reviewed against multiple programs before a recommendation lands on the table.

Accessing multiple lenders through one experienced broker often produces better terms than approaching any single lender directly.

Best-fit scenarios

The deals that fit this program best include:

- Fix-and-flip or value-add acquisitions needing quick capital

- Transitional commercial properties in lease-up

- Time-sensitive closings where traditional banks are too slow

- Investors who qualify on asset income rather than personal income

Typical loan structure and features to expect

Most bridge products arranged through David run 6 to 24 months with interest-only payments. Loan amounts typically start around $250,000, and leverage depends on the asset type and your documented exit strategy.

What documents and deal info you will need

Come prepared with a clear exit strategy and property summary before the first conversation. Lenders also want your purchase contract, entity documents, and a basic financial overview of the deal.

Common red flags and how to avoid them

Weak exit strategies and inflated after-repair values are the two fastest ways to kill a deal. Keep your numbers conservative and make sure your repayment timeline is realistic before approaching any lender.

2. Axos Bank

Axos Bank is a federally chartered bank that offers commercial bridge products alongside its broader lending portfolio. As one of the more established commercial bridge loan lenders in the market, Axos targets experienced sponsors with a solid track record of closing and stabilizing deals.

What Axos typically finances

Axos focuses on transitional commercial real estate including multifamily, mixed-use, retail, and office properties. Light value-add and lease-up scenarios fit their program best.

Typical loan size and leverage range

Loan amounts generally start at $5 million, with leverage typically capped around 70% to 75% of as-is value. Stronger sponsors with cleaner deals can sometimes negotiate tighter pricing.

Speed and process overview

Axos moves faster than a traditional bank but slower than a private lender. Expect a 30 to 60 day closing window depending on how complete your deal package is when you apply.

Having full documentation ready before your first conversation with Axos is the single fastest way to keep your timeline on track.

Recourse, occupancy, and collateral expectations

Most Axos bridge products carry full recourse requirements, and they prefer properties with some existing occupancy. Fully vacant assets rarely fit their underwriting criteria.

Fees, prepayment, and extension options to confirm

Origination fees typically start around 1%, and prepayment terms vary by deal structure. Always confirm extension availability upfront, since eligibility depends on loan performance at the time of the request.

When Axos makes the most sense

Axos works best when you need institutional execution on a near-stabilized commercial asset above $5 million and prefer a regulated bank over a private capital source.

3. iBorrow

iBorrow is a private direct lender that focuses exclusively on commercial real estate bridge financing. As one of the more flexible commercial bridge loan lenders in the non-bank space, iBorrow moves fast and keeps its underwriting focused on the asset rather than the borrower's personal financial profile.

What iBorrow typically finances

iBorrow finances transitional commercial and multifamily properties across the country. Their focus includes value-add acquisitions, repositioning projects, and properties that traditional lenders won't touch due to occupancy or cash flow gaps.

Typical loan size and property types

Loan sizes typically range from $3 million to $100 million, covering multifamily, office, retail, hospitality, and mixed-use assets. Their appetite for complex deal types sets them apart from most bank lenders.

Underwriting focus and borrower profile

iBorrow underwrites primarily on asset value and deal fundamentals rather than borrower credit scores. Experienced sponsors with a clear business plan get the most traction here.

If your deal has a strong equity position and a realistic exit, iBorrow's underwriting process works in your favor.

Funding timeline and closing mechanics

iBorrow can close in as few as 10 to 14 business days on clean deals. Your ability to provide a complete deal package upfront directly drives how fast they move.

Fees, reserves, and exit strategy expectations

Origination fees typically run 1% to 2%, and iBorrow requires a defined exit strategy before approving any loan. Expect interest reserves to be factored into the loan structure.

When iBorrow makes the most sense

iBorrow fits best when you need fast, asset-based capital on a complex or transitional property above $3 million and your personal income documentation is limited.

4. Ready Capital

Ready Capital is a publicly traded commercial real estate finance company focused on small to medium-balance bridge loans. They bring institutional-grade execution to deal sizes that larger lenders routinely skip, making them one of the more practical commercial bridge loan lenders for transitional assets in the $1 million to $30 million range.

What Ready Capital typically finances

Ready Capital targets transitional multifamily, mixed-use, and light commercial properties nationwide. Value-add acquisitions and properties in active lease-up or light renovation fit their program well.

Typical loan size, term, and use cases

Loan sizes typically range from $1 million to $30 million, with terms running 12 to 36 months. Interest-only structures are standard, which keeps your monthly carrying costs manageable during repositioning.

Underwriting focus and borrower profile

Ready Capital weighs both asset fundamentals and sponsor experience. Borrowers with a completed deal history consistently get more favorable underwriting outcomes.

Your track record carries real weight here. Documented completed deals move your file forward faster than anything else.

Timing, execution, and what drives approvals

Expect a 30 to 45 day closing timeline. A complete package with current rent rolls and a defined exit strategy is what accelerates your approval.

Fees, prepayment, and extension terms to confirm

Origination fees generally start at 1%, and prepayment terms vary by deal structure. Always confirm extension availability and associated costs before signing your term sheet.

When Ready Capital makes the most sense

Ready Capital fits best when your deal sits between $1 million and $30 million and you want institutional execution without the high loan minimums that larger bridge lenders typically require.

5. Bloomfield Capital

Bloomfield Capital is a Detroit-based private lender that operates as one of the more relationship-driven commercial bridge loan lenders in the country. They specialize in deals where timing or property complexity makes traditional financing impractical.

What Bloomfield typically finances

Bloomfield targets transitional commercial real estate including multifamily, mixed-use, hospitality, and land deals. Their appetite for complex deal structures sets them apart from most bank-side bridge programs.

Typical loan size and term range

Loan sizes typically range from $1 million to $20 million, with terms running 12 to 36 months. Interest-only structures are standard across most of their deals.

Underwriting focus and deal profile

Bloomfield focuses on equity position and deal fundamentals rather than personal financials. A solid business plan and clear exit strategy carry more weight here than your credit score.

Your exit strategy is the single most important document you bring to a Bloomfield conversation.

Timeline and process overview

Bloomfield can close in 10 to 30 business days depending on deal complexity. Having your property summary and purchase contract ready before outreach shortens that window.

Fees, structure, and extension terms to confirm

Origination fees typically start at 1% to 2%, and extension availability depends on loan performance. Always confirm prepayment terms before signing a term sheet.

When Bloomfield makes the most sense

Bloomfield fits best when your deal is complex or non-standard and you need a lender that evaluates the asset rather than your personal income documentation.

Next Steps

Each of the commercial bridge loan lenders on this list serves a different deal profile. Your best move is to match the lender to your specific situation before you make any calls. If your deal is above $5 million and near stabilization, Axos or Ready Capital make sense. If you need fast, asset-based capital on a complex property, iBorrow or Bloomfield are stronger fits.

Before you reach out to any lender, have your exit strategy, purchase contract, and property summary ready. Lenders move faster when you bring a complete package from the start, and it signals that you're a serious sponsor.

If you want someone to review your deal and point you toward the right capital source, reach out to David Roa directly. With 25-plus years of lending experience and a nationwide network, the goal is to get your deal funded efficiently, without wasting time on lenders that were never a fit.