DSCR Loan Pros And Cons: Rates, Rules, And When To Use Them

DSCR loans let real estate investors qualify based on a property's rental income rather than personal W-2s or tax returns. For investors building a portfolio, this sounds ideal. But before you commit, you need a clear picture of the DSCR loan pros and cons that will affect your bottom line.

These loans solve a specific problem: traditional lenders often penalize investors who write off expenses or own multiple properties. DSCR financing sidesteps those hurdles by focusing on one question, does the property's income cover the debt? That simplicity has driven their popularity, but higher interest rates and larger down payment requirements mean they're not right for every deal.

After funding over $150 million in loans and building my own real estate investment portfolio, I've seen exactly when DSCR loans make sense, and when they don't. This guide breaks down the rates, rules, and specific scenarios where DSCR financing delivers value versus when a conventional mortgage serves you better.

Why DSCR loans matter to real estate investors

Traditional lenders evaluate your personal income, tax returns, and debt-to-income ratio before approving a mortgage. This creates a ceiling for investors who need to finance multiple properties quickly. DSCR loans shift the focus entirely to the property's ability to generate income, letting you bypass the personal financial scrutiny that slows down portfolio growth.

Traditional lender roadblocks that block portfolio growth

Conventional mortgages cap most investors at four to ten financed properties, depending on the lender's overlays. After that limit, you face stricter requirements: larger down payments, higher credit scores, and extensive documentation of rental income history. Each new application becomes more complicated as lenders calculate your total debt load across all holdings.

Tax write-offs create another problem. Smart investors reduce taxable income through depreciation, expenses, and deductions. Your CPA celebrates those strategies, but mortgage underwriters see lower reported income and deny your application. DSCR loans eliminate this contradiction by ignoring your tax returns completely and focusing on whether rental income covers the mortgage payment.

"DSCR loans remove the penalty for running a tax-efficient investment business."

Portfolio scaling without income limits

You can finance as many properties as the numbers justify with DSCR loans. No arbitrary caps on property count exist because each deal stands on its own merit. If the rental income supports the debt service, you qualify. This approach lets you move quickly when you find undervalued properties in competitive markets.

Understanding the dscr loan pros and cons becomes critical when you're ready to scale beyond beginner investor status. Your W-2 income stops mattering, which opens opportunities for investors with strong deal-finding skills but complex tax situations. Real estate agents also benefit from knowing these products exist, as they can confidently bring investors to properties without worrying about conventional loan restrictions killing deals in underwriting.

Self-employed investors gain the most advantage. You no longer need to wait two years to show stable business income or explain fluctuating quarterly earnings. Instead, you present a property that generates $2,000 monthly rent against a $1,500 mortgage payment, and the loan moves forward based on that cash flow ratio alone.

How DSCR loans work and how lenders calculate DSCR

Lenders approve DSCR loans by dividing your property's monthly rental income by its total monthly debt obligations. That ratio tells them whether the property generates enough cash to cover the mortgage payment, taxes, insurance, and HOA fees. You don't provide tax returns or W-2s because your personal income sits outside the equation entirely.

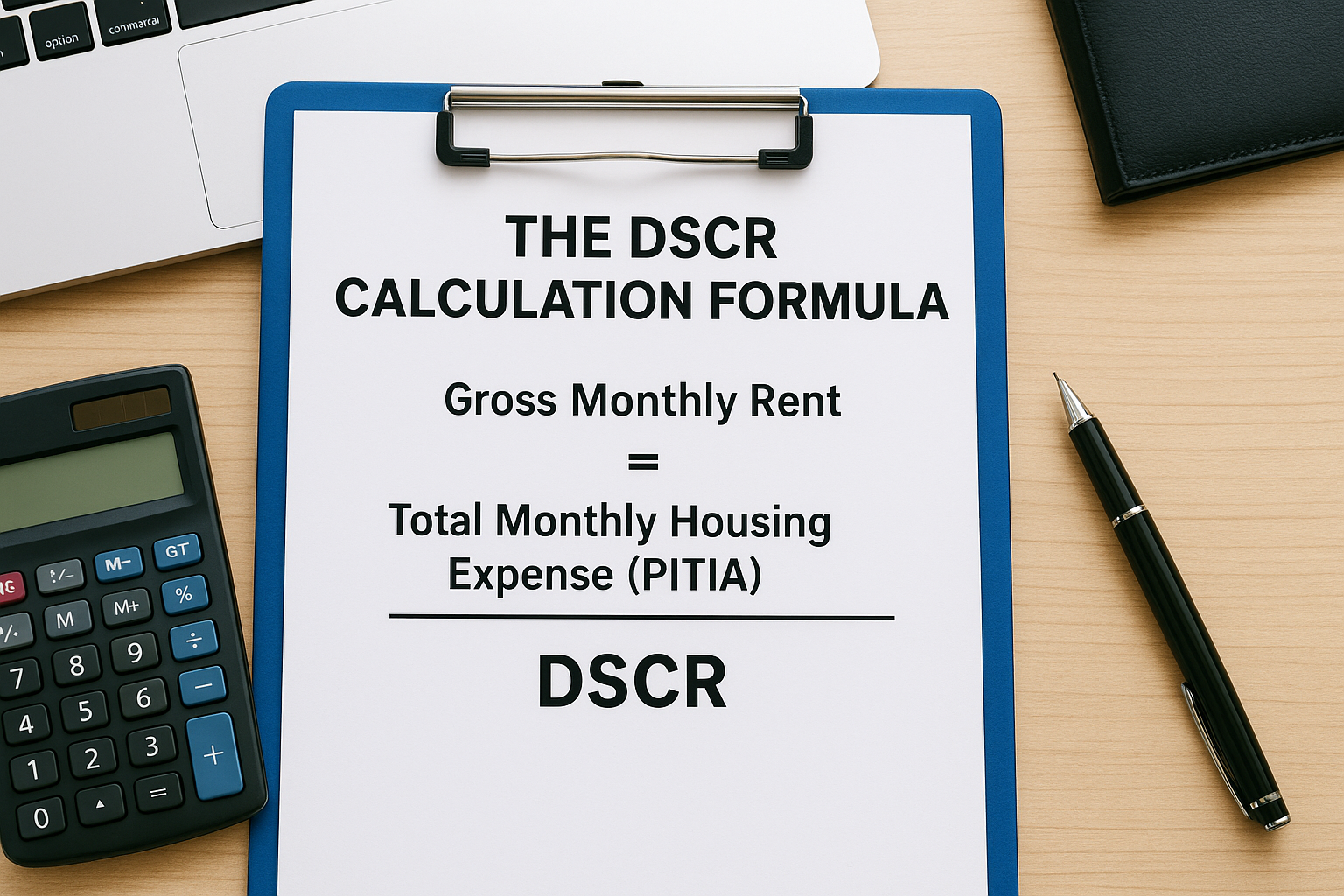

The DSCR calculation formula

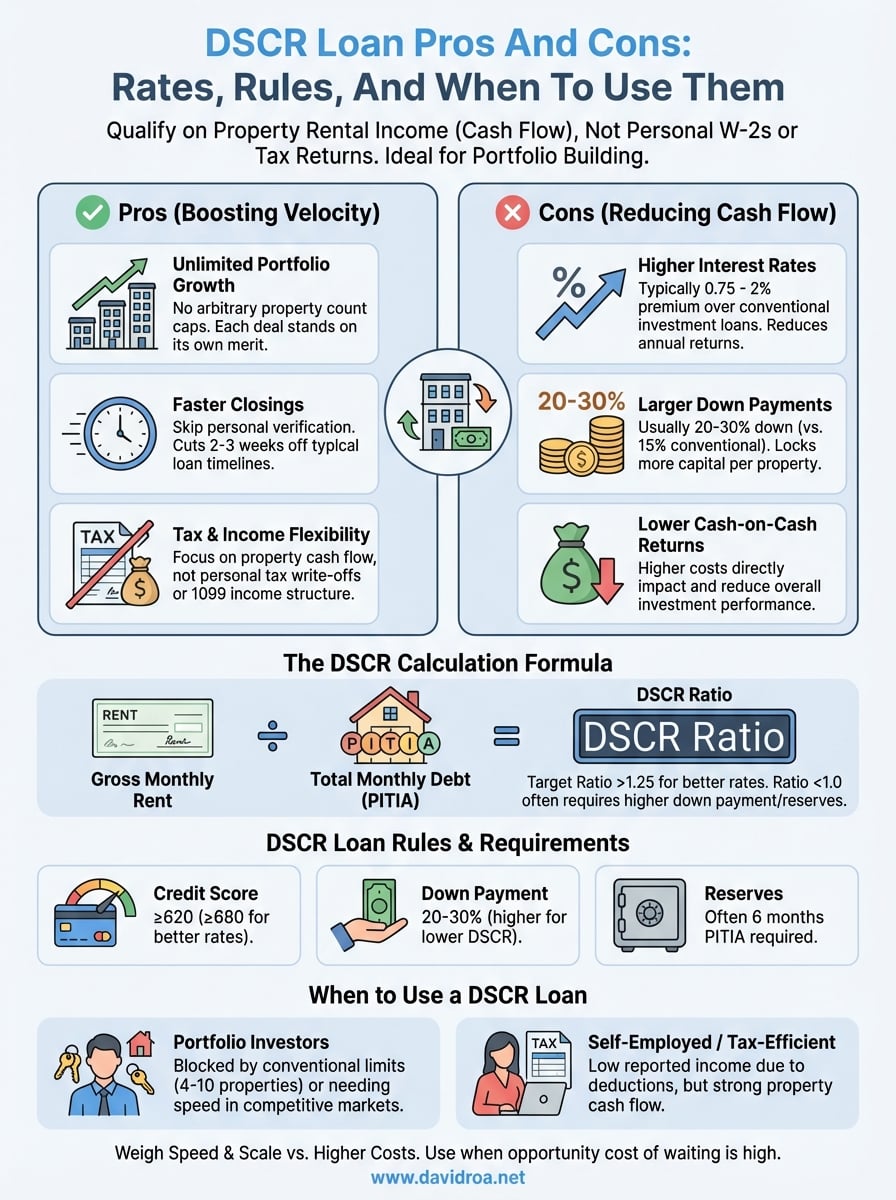

Your lender takes the gross monthly rent and divides it by the total monthly housing expense (PITIA: principal, interest, taxes, insurance, association dues). A DSCR of 1.0 means the rent exactly covers the payment. Most lenders require a minimum ratio between 0.75 and 1.0 to approve the loan, though rates improve significantly above 1.25.

A property renting for $2,400 monthly with a $2,000 total payment produces a DSCR of 1.2 ($2,400 ÷ $2,000 = 1.2). This 20 percent cushion tells lenders the property generates surplus income beyond debt service. Properties with ratios below 1.0 still qualify with many lenders, but you pay higher interest rates to offset the increased risk.

"The DSCR ratio directly impacts your interest rate more than any other factor in these loans."

Income documentation that lenders accept

You submit either a current lease agreement or a professional appraisal with rental analysis to prove income potential. Existing leases provide the strongest documentation because they show actual rents you're collecting today. Vacant properties require an appraisal that includes comparable rental data from similar properties in the area.

Weighing the dscr loan pros and cons starts with understanding this calculation determines everything: your approval, rate, and loan amount. Lenders don't care about your restaurant business income or your W-2 job because the property's cash flow stands alone as the qualifying metric.

DSCR loan rules and requirements

DSCR lenders set baseline standards you must meet before they review your property's income ratio. You typically need a credit score of 620 or higher, though better rates require scores above 680. Down payments start at 20 percent for most programs, with some lenders requiring 25 percent for properties below a 1.0 DSCR ratio.

Credit score and down payment thresholds

Your credit score determines both approval and pricing. Scores between 620 and 679 qualify you but carry higher interest rates, often 1 to 2 percentage points above prime tier pricing. Once you reach 680 or above, you access better rate tiers that significantly improve your cash-on-cash returns over the loan term.

Down payment requirements increase as risk factors stack. A property with a 1.25 DSCR might qualify at 20 percent down, while a 0.85 DSCR property requires 25 to 30 percent down to compensate lenders for negative cash flow. Cash reserves of six months PITIA often appear as requirements for properties with lower ratios.

"Higher down payments and reserve requirements protect lenders when rental income drops unexpectedly."

Property type and occupancy restrictions

DSCR loans fund single-family rentals, condos, townhomes, and properties up to four units. You cannot use DSCR financing for your primary residence because the product exists specifically for investment properties generating rental income. Mixed-use properties with commercial space on the first floor and residential units above sometimes qualify, depending on the lender's appetite for that asset class.

Evaluating the dscr loan pros and cons requires understanding these requirements limit which properties work in your strategy. Short-term rental properties face additional scrutiny, with many lenders requiring 12 months of rental history before considering Airbnb income in DSCR calculations.

Pros and cons that affect your returns

DSCR loans create specific trade-offs between speed and cost that directly impact your investment performance. You gain access to faster closings and unlimited property financing, but you pay premium rates and higher down payments. Understanding these dscr loan pros and cons helps you calculate whether the benefits justify the additional expense for each deal you evaluate.

Advantages that boost deal velocity

You qualify without tax returns or employment verification, cutting two to three weeks off typical loan timelines. This speed lets you close deals before other investors who need conventional financing can complete their applications. Portfolio investors benefit most because you avoid the arbitrary property limits that block conventional borrowers after four financed properties.

Income structure flexibility gives you another edge. Your business write-offs, 1099 income, or multiple LLCs no longer create underwriting problems. DSCR lenders simply verify the property generates sufficient rent to cover its debt service without examining your personal financial complexity.

"Faster closings often mean winning deals in competitive markets where sellers choose certainty over price."

Disadvantages that reduce cash flow

Interest rates typically run 0.75 to 2 percentage points higher than conventional investment property loans. This premium costs you $125 to $330 monthly on a $200,000 loan, reducing your annual cash-on-cash returns by 6 to 12 percent depending on your down payment amount.

Larger down payments lock more capital in each property. Where conventional loans accept 15 percent down for investment properties with strong borrower profiles, DSCR loans require 20 to 30 percent down depending on your property's income ratio. This requirement limits how many properties you can acquire with available capital.

When a DSCR loan makes sense

DSCR loans work best when the speed and flexibility outweigh the higher interest costs on properties with strong rental income. You calculate this by comparing the monthly rate premium against the opportunity cost of missing a deal or waiting months for conventional approval. Properties with DSCR ratios above 1.25 often justify the added expense because they generate enough surplus income to absorb the rate difference.

Portfolio investors blocked by conventional limits

You reach a point where conventional lenders stop approving loans regardless of your property performance or personal financial strength. DSCR financing removes this ceiling entirely, letting you acquire properties based solely on their income-generating capacity. Investors managing 10 or more rental properties find DSCR loans become necessary rather than optional.

The ability to close quickly also matters in competitive markets. When you compete against cash buyers or other investors, a 21-day DSCR closing beats a 45-day conventional timeline. Sellers choose certainty over price in tight markets, giving you negotiating leverage that reduces purchase costs enough to offset higher interest rates.

Self-employed investors with tax-efficient strategies

Your CPA structures your business to minimize taxable income through legitimate deductions, but conventional underwriters reject your loan application based on low reported earnings. DSCR loans solve this problem immediately by ignoring your tax returns completely. You qualify based on property income alone, which lets you maintain aggressive tax strategies without sacrificing borrowing power.

Understanding all dscr loan pros and cons reveals these products serve investors who value speed and scalability over minimizing interest costs. If you're building a portfolio beyond four properties or running a tax-efficient business, DSCR financing often becomes your only practical option for continued growth.

"DSCR loans become essential tools when conventional lending rules block otherwise profitable deals."

Bottom line

Weighing the dscr loan pros and cons comes down to your specific investment strategy and financial situation. You pay higher rates and larger down payments in exchange for unlimited portfolio growth and faster closings that conventional lenders cannot match. Properties with strong rental income ratios above 1.25 absorb these costs while still generating positive cash flow.

Your decision should focus on opportunity cost rather than just interest rates. Missing a profitable deal because you need three months for conventional approval costs more than paying an extra percentage point on your loan. Self-employed investors and portfolio builders find DSCR financing often becomes their only path forward after conventional lenders impose arbitrary property limits.

Calculate the actual monthly cost difference between DSCR and conventional rates on your target property. If that premium stays below the additional cash flow you generate from acquiring the property sooner or maintaining your current deal velocity, DSCR loans make financial sense. Contact me directly to run these numbers on your next investment property and determine which financing structure maximizes your returns.