Fannie Mae Investment Property Guidelines: 2026 Loan Rules

If you're buying a rental or investment property with a conventional loan, you'll need to meet a specific set of rules that go beyond what primary residence buyers face. Fannie Mae investment property guidelines dictate everything from minimum credit scores and down payment thresholds to reserve requirements and maximum financed property limits, and getting any of these wrong can stall or kill your deal.

These guidelines shifted heading into 2026, and the details matter. Whether you're acquiring your first rental or scaling a portfolio, the credit, income, and asset benchmarks Fannie Mae enforces will directly shape your loan terms and buying power. Understanding these rules upfront saves you from surprises at the underwriting table, and puts you in a stronger negotiating position with sellers.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment transactions over 25+ years. A significant share of that volume comes from investor clients navigating exactly these guidelines. This article breaks down the current Fannie Mae requirements for investment properties, credit scores, down payments, DTI ratios, reserves, and rental income rules, so you know precisely where you stand before you apply.

Why Fannie Mae rules matter for investors

Fannie Mae doesn't lend money directly to borrowers. Instead, it purchases loans from lenders and packages them into mortgage-backed securities. Because most conventional lenders need to sell those loans to Fannie Mae to free up capital for new originations, they underwrite every file against Fannie Mae's eligibility standards. If your loan doesn't conform to those standards, the majority of conventional lenders won't fund it.

Fannie Mae sets the floor for conventional lending

When you apply for a conventional investment property mortgage, the lender is running your file against Fannie Mae's underwriting matrix, even if Fannie Mae is never mentioned by name during the process. That matrix holds investor loans to stricter benchmarks than primary residence loans across nearly every category: higher minimum credit scores, larger required down payments, tighter debt-to-income ceilings, and mandatory post-closing cash reserves that must stay liquid after your transaction closes.

Getting your file to Fannie Mae's investor benchmarks before you apply is the most effective way to avoid a last-minute loan denial.

These tighter requirements exist because investment properties carry higher default rates than owner-occupied homes during economic stress. Fannie Mae prices that risk into its guidelines directly, and lenders pass it on through stricter qualification criteria and higher interest rates for investors compared to primary residence buyers.

Your loan terms hinge on investor-specific pricing

Fannie Mae uses loan-level price adjustments (LLPAs) to modify the cost of a loan based on risk variables like credit score, loan-to-value ratio, and property type. Investment properties trigger some of the largest LLPAs in the entire pricing matrix. A borrower purchasing a rental property with a 720 credit score and 25% down will face significantly higher pricing than that same borrower buying a primary residence with identical numbers.

Understanding the fannie mae investment property guidelines before you rate shop tells you exactly which variables to improve. Raising your credit score by 20 points or bumping your down payment from 20% to 25% can reduce your LLPA hit and lower your rate, sometimes by more than a quarter point on a 30-year term.

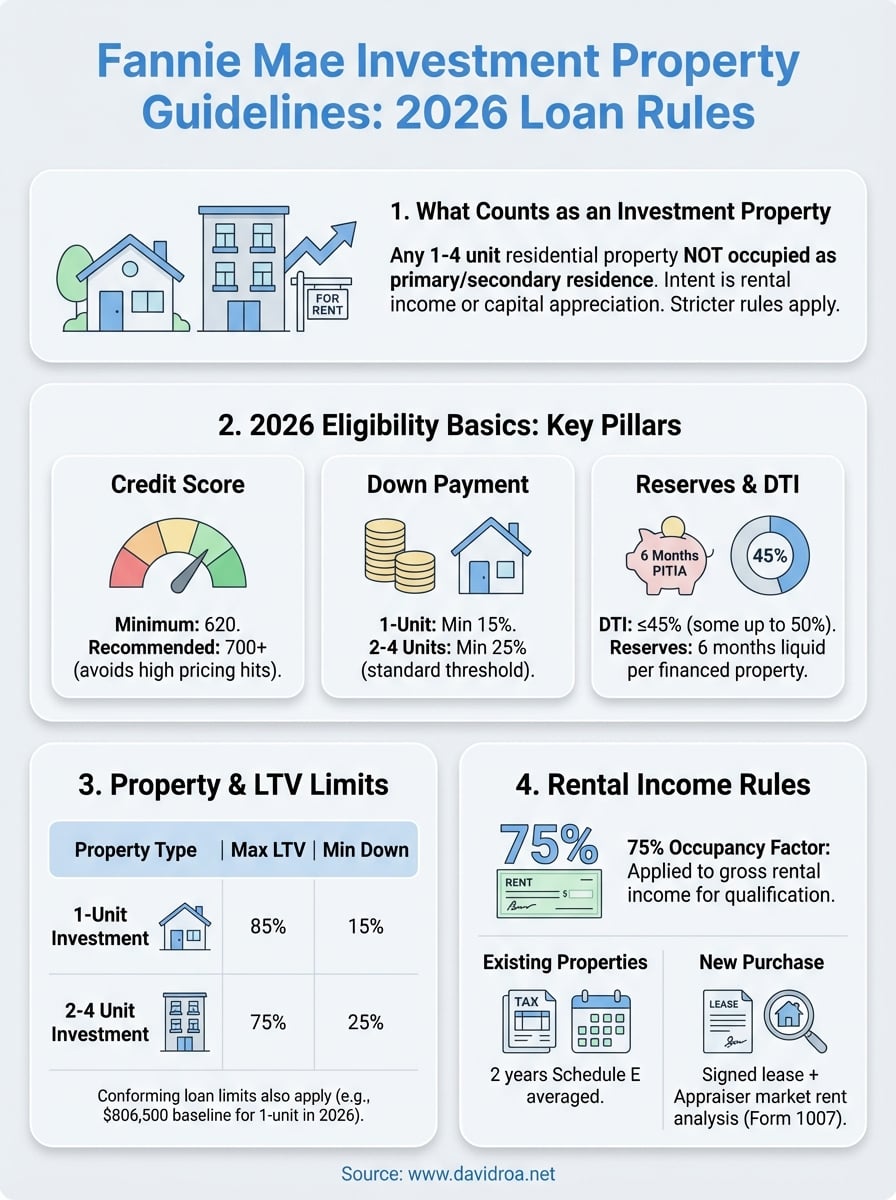

What counts as an investment property

Fannie Mae defines an investment property as any 1-4 unit residential property that the borrower does not occupy as a primary or secondary residence. The key word is intent: if you're purchasing the property to generate rental income or capital appreciation rather than to live in it, Fannie Mae treats it as an investment property and applies its stricter set of requirements.

How Fannie Mae draws the line

The classification hinges on occupancy type, and lenders verify this aggressively. A single-family home, a duplex, a triplex, or a four-unit building all qualify as investment properties under the fannie mae investment property guidelines when you won't be occupying one of the units. If you do plan to live in one unit of a 2-4 unit building, the property may qualify as owner-occupied, which unlocks significantly better loan terms.

Misrepresenting occupancy on a mortgage application is considered fraud, and lenders use data tools to cross-reference your application against other addresses on your credit report.

Vacation homes and second residences follow a separate set of Fannie Mae rules entirely. If your second home could realistically generate rental income but you plan to use it personally, how you classify it on the application matters, and your lender will ask direct questions to confirm the actual use.

2026 eligibility basics: credit, DTI, reserves

The fannie mae investment property guidelines set three hard eligibility benchmarks that underwriters check before anything else: your credit score, debt-to-income ratio, and post-closing reserves. Meeting the minimums gets you in the door, but your actual loan pricing and approval strength depend on how far above those minimums you land.

Credit score and down payment minimums

Fannie Mae requires a minimum 620 credit score for investment property loans, but most lenders won't approve a file that thin given the LLPA exposure. In practice, you want a 700 or higher to avoid punishing rate adjustments. On the down payment side, Fannie Mae requires a minimum of 15% for a single-unit investment property, but 25% is the standard threshold for 2-4 unit properties and for borrowers who want to avoid the steepest pricing hits.

Putting 25% down on a single-unit rental instead of the minimum 15% can meaningfully reduce your LLPA cost and lower your rate over the life of the loan.

DTI limits and reserve requirements

Your debt-to-income ratio must stay at or below 45%, though some automated underwriting approvals allow up to 50% with compensating factors. Beyond DTI, Fannie Mae requires six months of PITIA reserves for each financed investment property you hold. Reserves must be liquid, meaning cash or assets that convert to cash quickly. The more financed properties you carry, the larger your total reserve requirement grows.

2026 property and loan limits that change LTV

Two variables directly affect your loan-to-value ratio and what Fannie Mae will approve on an investment property: the number of units in the building and the conforming loan limit for your county. Both factors shift the LTV ceiling Fannie Mae allows, which changes your minimum down payment requirement.

Unit count and LTV ceilings

Your unit count determines the maximum LTV Fannie Mae permits under the fannie mae investment property guidelines. The more units in the property, the lower the LTV ceiling drops, and the more cash you need at closing.

| Property Type | Max LTV | Min Down Payment |

|---|---|---|

| 1-unit investment | 85% | 15% |

| 2-4 unit investment | 75% | 25% |

If you're buying a duplex or triplex as an investment, plan on 25% down from the start so your deal doesn't stall during underwriting.

Conforming loan limits in 2026

The 2026 baseline conforming loan limit sits at $806,500 for a single-unit property in most U.S. markets, with higher ceilings in designated high-cost areas. Knowing your county's limit before you make an offer helps you structure the right loan size.

Loans above this threshold move into jumbo territory, where Fannie Mae's standard guidelines no longer apply. Lenders set their own rules for jumbo investment loans, and those rules are typically stricter on credit score and reserves than conforming guidelines.

How to qualify and document rental income

Rental income can help you qualify for an investment property loan, but Fannie Mae has specific rules about when it counts and how much of it you can use. Under the fannie mae investment property guidelines, lenders apply a 75% occupancy factor to gross rental income to account for vacancies and maintenance costs before running your DTI calculation.

Using existing rental income on tax returns

If you already own rental properties, Fannie Mae requires two years of Schedule E from your federal tax returns to verify rental income. Lenders average the income across both years, and if income dropped year-over-year, they will scrutinize the reason. Any unreimbursed expenses or depreciation shown on Schedule E affects how much net income the lender can count toward qualifying you.

Documenting income on a property you're buying

For a new purchase with no rental history, lenders typically use a signed lease agreement combined with a market rent analysis from an appraiser. The appraiser completes Form 1007, which establishes the property's fair market rent. You can only use 75% of that figure, and only if your file receives an eligible finding through automated underwriting.

Having a signed lease in place before you apply strengthens your file significantly and reduces the lender's reliance on appraiser-estimated rents alone.

Next steps if you want to finance a rental

You now have a clear picture of what the fannie mae investment property guidelines require across credit, down payment, reserves, DTI, and rental income documentation. The next move is pulling your credit report, tallying your liquid reserves, and calculating your current DTI before you contact a lender. Knowing your numbers ahead of time keeps you in control of the conversation.

Before you apply, confirm the conforming loan limit for your target county, verify how many financed properties you currently hold, and get any existing leases organized. If you're buying a 2-4 unit building, budget for 25% down from the start.

Working with a lender who handles high-volume investor files regularly makes a measurable difference in how smoothly your deal closes. If you're ready to move forward on a rental property, connect with David Roa to review your file and build a loan strategy that fits your investment goals.