6 Best FHA 203k Lenders Near Me: Rates, Fees, Requirements

Finding the right FHA 203k lenders near me can feel overwhelming when you're trying to finance both a home purchase and renovations in one loan. Not every lender offers this specialized product, and among those who do, experience levels vary dramatically. The wrong choice could mean delays, higher costs, or a deal that falls apart.

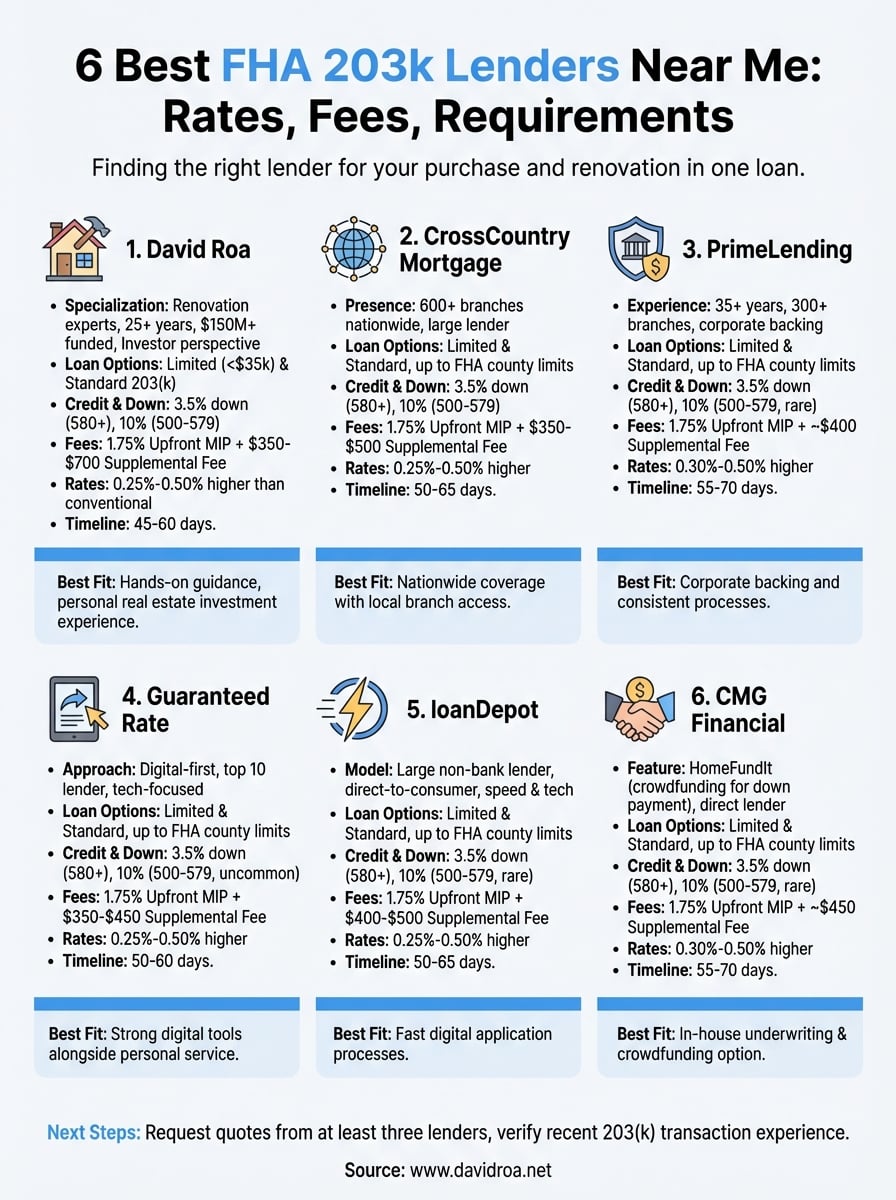

After 25+ years in the mortgage industry and over $150 million funded, I've seen firsthand how the right 203(k) lender makes or breaks a renovation project. At David Roa, we specialize in FHA 203(k) loans alongside other renovation financing options like HomeStyle loans, so I know exactly what separates capable lenders from the rest.

This guide breaks down six top FHA 203(k) lenders worth considering, covering their rates, fees, and requirements. Whether you're buying a fixer-upper as your primary residence or exploring renovation financing for the first time, you'll walk away knowing which lenders fit your situation and what to expect from the application process.

1. David Roa

When you're searching for fha 203k lenders near me, you want someone who doesn't just process paperwork but actually understands renovation projects from experience. My team specializes in FHA 203(k) loans alongside ITIN loans, HomeStyle loans, and investor financing, which means we bring a complete perspective to your renovation purchase. With over 25 years in lending and more than $150 million funded, we've helped hundreds of buyers turn fixer-uppers into dream homes.

203k loan options and renovation limits

You can access both Limited 203(k) loans for repairs under $35,000 and Standard 203(k) loans for major renovations exceeding that threshold. Limited 203(k) works for non-structural repairs like new flooring, appliances, or painting, while Standard 203(k) covers everything from foundation work to room additions. Your maximum loan amount depends on FHA limits in your county, which can reach $1,149,825 in high-cost areas as of 2026.

Minimum credit and down payment

Most borrowers qualify with a credit score of 580 and just 3.5% down, though stronger credit in the 620+ range opens better rate options. If your score sits between 500 and 579, you'll need to put down 10% instead. We work with clients who have non-traditional credit histories or recent financial challenges, so don't assume you're disqualified before we review your situation.

Typical fees, rate notes, and timeline

Expect to pay standard FHA fees including 1.75% upfront mortgage insurance premium and an additional supplemental origination fee ranging from $350 to $700 for the 203(k) complexity. Rates typically run 0.25% to 0.50% higher than conventional loans due to the added risk and processing requirements. Your timeline stretches to 45 to 60 days for closing, with renovations completed within six months after purchase.

"The supplemental fee covers the extra underwriting, consultant coordination, and draw management that 203(k) loans require compared to standard mortgages."

How to find a local loan officer near you

You can reach my team directly at www.davidroa.net or call to schedule a consultation where we'll review your property and renovation budget. We serve clients nationwide but maintain strong roots in the Chicago area, making us particularly responsive for Midwest buyers.

Best fit and watch-outs

This option works best if you want hands-on guidance from someone who owns rental properties and flips homes personally. Watch out for timeline expectations because 203(k) loans involve more documentation and consultant approvals than typical mortgages, which can frustrate buyers expecting instant closings.

2. CrossCountry Mortgage

CrossCountry Mortgage operates more than 600 branches across all 50 states, making them one of the largest fha 203k lenders near me options for buyers nationwide. Their size brings both advantages and potential complications, as you'll find loan officers with varying levels of 203(k) experience depending on your local branch.

203k loan options and renovation limits

You can choose between Limited 203(k) for repairs up to $35,000 and Standard 203(k) for larger projects. Their system handles renovations up to FHA loan limits in your county, which means you could finance properties exceeding $1 million in high-cost areas with substantial renovation budgets included.

Minimum credit and down payment

CrossCountry typically requires a minimum credit score of 580 with 3.5% down for standard eligibility. Borrowers with scores between 500 and 579 face the higher 10% down payment requirement that FHA mandates.

Typical fees, rate notes, and timeline

Standard FHA charges apply including the 1.75% upfront mortgage insurance premium, plus you'll pay a supplemental origination fee between $350 and $500. Rates generally run 0.25% to 0.50% above conventional loans. Your closing timeline stretches to 50 to 65 days on average.

How to find a local loan officer near you

Visit their website's branch locator to identify offices in your area, then verify that specific loan officers handle 203(k) products before committing to an application.

Best fit and watch-outs

This lender works well if you want nationwide coverage with local branch access. Watch out for inconsistent service quality across branches, as some offices rarely process 203(k) loans and lack the specialized knowledge required.

"Branch size doesn't guarantee 203(k) expertise, so always confirm your loan officer's actual renovation loan experience before starting an application."

3. PrimeLending

PrimeLending brings over 35 years of lending experience to the table with more than 300 branches nationwide. As a subsidiary of Hilltop Holdings, they offer financial stability that some smaller fha 203k lenders near me can't match, though their corporate structure means less flexibility in underwriting compared to independent brokers.

203k loan options and renovation limits

Both Limited 203(k) and Standard 203(k) products are available, covering repairs from $5,000 up to your county's maximum FHA loan limit. Standard loans handle structural changes like roof replacements or foundation repairs, while Limited versions work for cosmetic updates that don't require architectural drawings.

Minimum credit and down payment

Your application needs a minimum credit score of 580 for the standard 3.5% down payment structure. Scores between 500 and 579 trigger the 10% down requirement, though PrimeLending rarely approves these lower-tier applications in practice.

Typical fees, rate notes, and timeline

You'll pay the standard 1.75% upfront MIP plus a supplemental fee around $400 for 203(k) processing. Rates typically sit 0.30% to 0.50% higher than conventional mortgages. Expect 55 to 70 days from application to closing.

How to find a local loan officer near you

Their website includes a branch finder tool, but call ahead to confirm your specific loan officer has completed 203(k) transactions within the past six months.

Best fit and watch-outs

This lender fits borrowers who value corporate backing and consistent processes. Watch out for rigid underwriting guidelines that leave little room for creative problem-solving when your renovation plans hit snags.

"Large lenders follow strict corporate protocols, which means fewer workarounds when your contractor estimates come in higher than expected."

4. Guaranteed Rate

Guaranteed Rate ranks among the top 10 retail mortgage lenders in the United States with a digital-first approach that appeals to tech-savvy borrowers. Their online platform streamlines much of the application process, though 203(k) loans still require significant human interaction due to renovation complexity. You'll find loan officers across the country, but expertise in handling fha 203k lenders near me searches varies widely by location.

203k loan options and renovation limits

Both Limited 203(k) and Standard 203(k) programs are available through their system. Your renovation budget can reach up to FHA loan limits in your county, which accommodates substantial remodeling projects when combined with the purchase price.

Minimum credit and down payment

You need a minimum credit score of 580 to qualify with 3.5% down. Borrowers with scores between 500 and 579 face the 10% down payment threshold, though approvals at this level are uncommon.

Typical fees, rate notes, and timeline

Standard charges include the 1.75% upfront MIP plus a supplemental origination fee between $350 and $450. Rates run approximately 0.25% to 0.50% above conventional loans. Your closing timeline extends to 50 to 60 days typically.

How to find a local loan officer near you

Their website features a loan officer search tool, but verify your assigned officer has recent 203(k) transaction history before proceeding.

Best fit and watch-outs

This lender works well if you want strong digital tools alongside personal service. Watch out for their preference to push simpler loan products over 203(k) options, as their commission structure incentivizes faster-closing conventional loans.

"Digital platforms help with paperwork but can't replace the specialized knowledge required to navigate 203(k) contractor bids and draw schedules."

5. loanDepot

loanDepot operates as one of the nation's largest non-bank retail mortgage lenders with a direct-to-consumer model that emphasizes speed and technology. Their platform processes thousands of loans monthly, though 203(k) products represent a smaller portion of their business compared to conventional mortgages. When searching for fha 203k lenders near me, you'll find their loan officers available in most states, but their focus tilts heavily toward purchase and refinance loans that close quickly.

203k loan options and renovation limits

You can access both Limited 203(k) loans for projects under $35,000 and Standard 203(k) loans for major renovations. Your combined loan amount follows FHA county limits, allowing significant renovation budgets in high-cost areas while maintaining the 3.5% down payment structure.

Minimum credit and down payment

Applications require a minimum credit score of 580 with the standard 3.5% down payment. Scores between 500 and 579 push your down payment requirement to 10%, though loanDepot rarely approves these lower-credit applications.

Typical fees, rate notes, and timeline

You'll pay the 1.75% upfront MIP plus a supplemental fee ranging from $400 to $500 for 203(k) processing. Rates typically sit 0.25% to 0.50% higher than conventional products. Expect 50 to 65 days from application to closing.

How to find a local loan officer near you

Their website includes a loan officer directory, though you should verify your assigned officer has completed 203(k) transactions recently rather than just conventional loans.

Best fit and watch-outs

This lender works well if you prioritize fast digital application processes and competitive conventional rates. Watch out for their tendency to steer borrowers toward simpler products, as 203(k) loans require more manual processing that conflicts with their automated workflow emphasis.

"High-volume lenders often lack the patience required for 203(k) contractor coordination and multiple draw inspections throughout renovation periods."

6. CMG Financial

CMG Financial stands out among fha 203k lenders near me options with their HomeFundIt platform that enables crowdfunding for down payments and closing costs. Their status as a direct lender rather than a broker means they underwrite and fund loans in-house, which can speed up decision-making when renovation timelines matter. You'll find loan officers in most states who handle 203(k) products, though their primary expertise lies in conventional and jumbo financing rather than renovation loans.

203k loan options and renovation limits

Both Limited 203(k) and Standard 203(k) programs are available through their lending platform. Your renovation budget can extend up to FHA county limits when combined with the purchase price, allowing substantial remodeling projects in most markets across the country.

Minimum credit and down payment

You need a minimum credit score of 580 to qualify with the standard 3.5% down payment. Borrowers with scores between 500 and 579 face the 10% down requirement, though CMG Financial rarely approves applications at this lower tier.

Typical fees, rate notes, and timeline

Standard charges include the 1.75% upfront MIP plus a supplemental origination fee around $450 for 203(k) processing. Rates typically run 0.30% to 0.50% higher than conventional mortgages. Expect 55 to 70 days from application to closing.

How to find a local loan officer near you

Their website includes a branch locator tool, but confirm your assigned loan officer has recent 203(k) experience before starting your application.

Best fit and watch-outs

This lender fits borrowers who want in-house underwriting and the unique HomeFundIt crowdfunding option. Watch out for their limited 203(k) volume compared to conventional products, which means fewer loan officers have deep renovation financing expertise.

"Direct lenders control their own underwriting but may lack the specialized 203(k) knowledge that dedicated renovation finance brokers provide through daily practice."

Next steps

You've now reviewed six qualified fha 203k lenders near me options, each with different strengths depending on your renovation budget, timeline, and service preferences. The right choice depends on whether you prioritize hands-on expertise from someone who personally invests in real estate, nationwide branch access with corporate backing, or digital convenience through streamlined platforms.

Start by requesting rate quotes from at least three lenders on this list to compare closing costs, supplemental fees, and timelines. Ask each loan officer how many 203(k) transactions they've closed in the past six months, as this number reveals actual experience beyond marketing claims and general mortgage knowledge.

If you're ready to explore FHA 203(k) financing with someone who understands renovation projects from an investor's perspective, schedule a consultation with David Roa. With over 25 years closing complex loans and a personal portfolio of flips and rentals, I'll help you determine if 203(k) fits your situation or if another renovation product like HomeStyle or hard money works better for your specific property goals.