FHA Loan Credit Score Requirements: 500 vs 580 Explained

Your credit score doesn't have to be perfect to buy a home with an FHA loan. In fact, FHA loan credit score requirements are among the most flexible in the mortgage industry, which is why these government-backed loans remain a popular choice for first-time buyers and those rebuilding their credit. But here's what many borrowers don't realize: the score you bring to the table directly determines how much cash you'll need upfront.

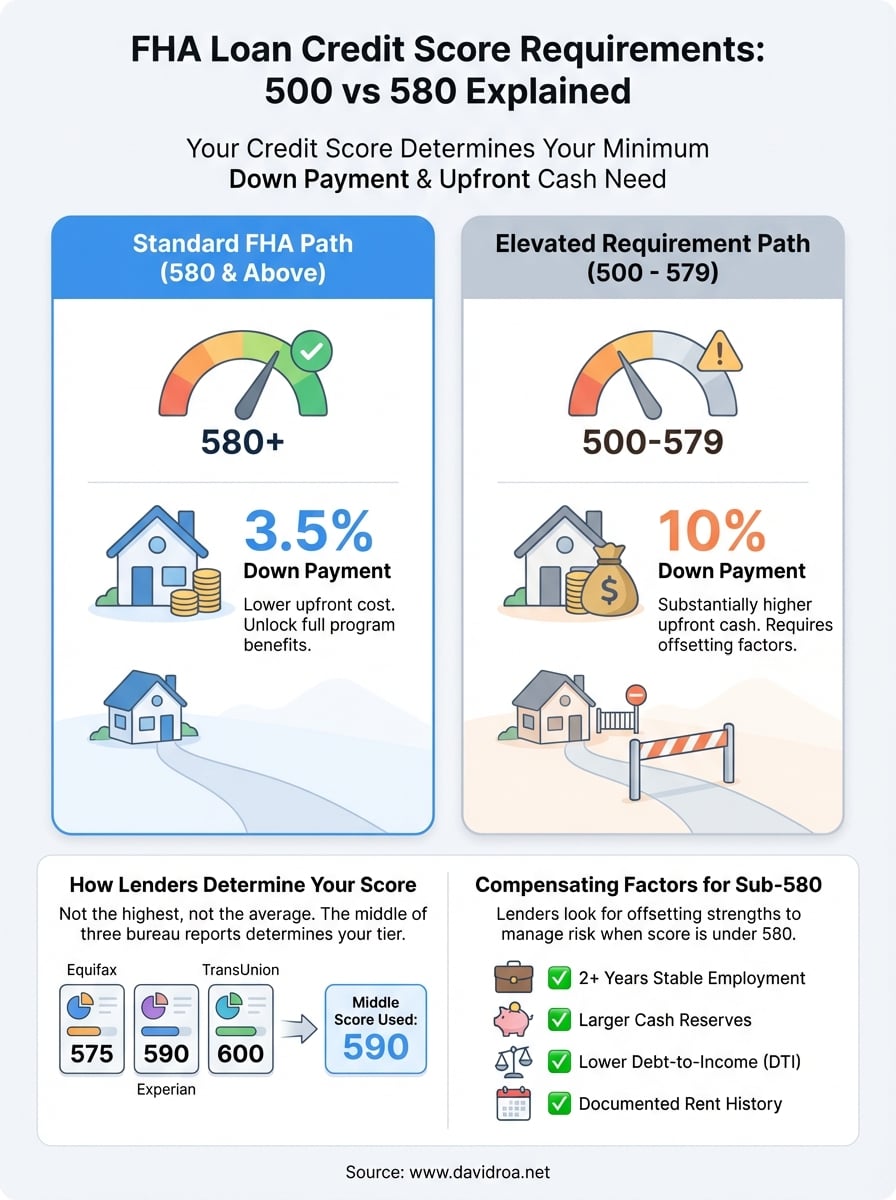

The magic numbers are 500 and 580. One qualifies you with a 10% down payment, while the other unlocks the minimum 3.5% down payment that makes FHA loans so attractive. Understanding where you fall on this spectrum, and what you can do about it, could save you thousands of dollars or help you get into a home months sooner than you expected.

With over 25 years of experience funding more than $150 million in loans, I've helped countless borrowers navigate these exact requirements at David Roa. Below, I'll break down exactly what credit score you need, how the tiers work, and what your options are regardless of where your credit stands today.

Why FHA credit score cutoffs matter

The difference between a 500 and 580 credit score isn't just a number on paper. It represents thousands of dollars in upfront cash you'll need to bring to closing and determines whether you can access the most affordable FHA entry point. When you understand these cutoffs, you can make informed decisions about timing your home purchase or prioritizing credit repair efforts that deliver the highest return.

The direct impact on your upfront costs

Your credit score dictates your minimum down payment requirement, and this creates a substantial financial gap between the two tiers. If you have a 580 or higher, you qualify for the 3.5% down payment option that makes FHA loans famous. But when your score falls between 500 and 579, lenders require a 10% down payment to offset the additional risk. On a $300,000 home, that's the difference between $10,500 and $30,000 upfront, not counting closing costs.

The 6.5% difference in down payment requirements can mean the difference between buying this year or waiting 12 to 18 months to save more cash.

What it means for your total buying power

Most buyers focus on monthly payments, but FHA loan credit score requirements also shape how much house you can realistically afford. When you need to put down 10% instead of 3.5%, you're pulling an extra $19,500 from your savings on that same $300,000 purchase. That money has to come from somewhere, which usually means either buying a less expensive home or delaying your purchase until you build up larger reserves. Your credit score essentially acts as a gatekeeper to your maximum purchase price, especially if you're working with limited savings or need to maintain emergency funds after closing.

What the FHA rules say about 500 and 580

The Federal Housing Administration sets clear benchmarks that determine your down payment tier, and these numbers come directly from HUD Handbook 4000.1, the official policy manual for FHA loans. You'll find two distinct credit score thresholds that shape your path to homeownership: 580 for the standard program and 500 for the higher down payment option. These aren't suggestions or guidelines that lenders can adjust. They represent hard floors established by federal policy that every approved lender must follow.

The 580 threshold for standard financing

When your credit score reaches 580 or higher, you qualify for the 3.5% minimum down payment that defines most FHA loans. This tier gives you access to the program's full benefits without additional cash requirements beyond the standard down payment, closing costs, and reserves. The 580 cutoff applies to the middle score from all three credit bureaus, not your highest or lowest score.

FHA lenders must use your middle credit score when you have reports from all three bureaus, which can work against you if one bureau shows significantly lower numbers.

The 500 floor with elevated requirements

FHA loan credit score requirements allow borrowers with scores between 500 and 579 to qualify, but you'll need a 10% down payment to offset the additional lending risk. This option keeps the door open for buyers working through credit challenges, though you'll face a substantially higher upfront cash requirement to access financing.

How lenders calculate and use your credit score

Lenders don't just pick one credit score and call it done. When you apply for an FHA loan, your lender pulls reports from all three major credit bureaus (Equifax, Experian, and TransUnion), and the calculation method directly impacts whether you qualify for that 3.5% down payment. Understanding this process helps you identify which score you need to focus on improving and prevents surprises during underwriting.

The three-bureau middle score method

Your lender takes the middle score from all three bureaus, not the highest or the average. If your scores come back as 590, 605, and 580, you'll qualify based on the 590 middle score, even though you have a higher option available. When you only have two credit reports, lenders use the lower of the two scores. This middle score methodology means you can't rely on a single monitoring service that only shows you one bureau's data.

Improving your middle score, not your highest score, determines whether you hit the 580 threshold for FHA loan credit score requirements.

Why your score can vary between lenders

Different lenders may pull your credit at different times, and your score fluctuates based on recent account activity. A credit card payment that posts today might not appear on all three bureaus simultaneously, creating temporary score differences. Additionally, each bureau uses slightly different data sources and reporting timelines, which explains why you see different numbers across the three reports even when pulled on the same day.

What changes when you put down 3.5% vs 10%

The down payment shift between credit score tiers creates a ripple effect that extends far beyond your initial cash outlay. When you move from the 3.5% to the 10% down payment requirement, you're not just bringing more money to closing. You're also adjusting your loan-to-value ratio, monthly mortgage insurance costs, and the amount of equity you start with on day one.

The immediate cash gap you need to bridge

On a $250,000 home purchase, the 3.5% down payment equals $8,750, while 10% requires $25,000. That $16,250 difference represents money you could otherwise allocate toward closing costs, home improvements, or emergency reserves after you move in. For buyers working with limited savings or those who need to maintain adequate reserves for FHA approval, this gap often determines whether you can purchase now or need to wait several months to build up additional funds.

The 6.5% difference in fha loan credit score requirements down payment tiers represents roughly 18 to 24 months of additional savings for most first-time buyers.

How your loan balance and equity shift

Putting down 10% instead of 3.5% reduces your starting loan balance by $16,250 on that same purchase, which translates to approximately $75 to $90 less in monthly principal and interest payments. You also begin with substantially more equity, giving you a stronger financial cushion if property values fluctuate.

How to qualify if your score is under 580

When your credit score falls between 500 and 579, you can still access FHA financing, but you'll face stricter requirements that go beyond the standard 10% down payment. Most approved lenders add their own risk overlays on top of the baseline fha loan credit score requirements, which means you need to demonstrate stronger financial stability through compensating factors. These additional safeguards help offset the increased lending risk and improve your chances of underwriting approval.

Work with an experienced FHA lender

Not all lenders accept applications in the 500 to 579 credit range, even though FHA guidelines technically allow it. You need to find a lender who actively works these files and understands how to structure your application to highlight your strengths. Experienced loan officers know which underwriters will consider lower credit scores and can guide you through documentation requirements that prove your ability to repay.

Each lender maintains different approval thresholds based on their internal risk tolerance and investor relationships. Some restrict FHA lending to borrowers with 580 or higher scores, while others specialize in serving the sub-580 market with appropriate safeguards.

Build your compensating factors

Underwriters look for offsetting strengths when your credit score sits below 580. Stable employment history spanning two or more years carries significant weight, as does maintaining larger cash reserves beyond minimum requirements. A debt-to-income ratio under 35% demonstrates budget room for your mortgage payment, while 12 months of documented on-time rent payments proves your housing reliability.

Compensating factors transform your application from a credit score number into a complete financial picture that underwriters can approve.

Next steps

Understanding fha loan credit score requirements gives you clarity on where you stand and what path forward makes the most sense for your situation. If you have a 580 or higher score, you can access the 3.5% down payment option and move forward with standard FHA financing. When your score sits between 500 and 579, focus on building compensating factors while saving for the 10% down payment requirement.

Your next move depends on your timeline. Buyers ready to purchase within 90 days should connect with an experienced FHA lender who can review your specific credit profile and map out exactly what you need to close. Those with more time can work on raising their middle credit score above 580 to unlock lower down payment requirements and expand their lender options.

I've helped hundreds of borrowers navigate these exact scenarios over the past 25 years. If you need guidance on qualifying with your current credit situation or want to explore your FHA loan options, reach out to discuss your specific situation.