How Does A Cash-Out Refinance Work? Steps, Costs & Risks

You've been paying your mortgage for years, building equity in your home, and now you need a significant amount of cash. Maybe it's for renovations, paying off high-interest debt, or funding an investment property. So how does a cash out refinance work, and is it the right move for you? The short answer: you replace your current mortgage with a larger loan and pocket the difference as a lump sum.

But the details matter. The amount you can borrow, the costs involved, and the risks you take on will shape whether this strategy actually puts you ahead, or sets you back. With over 25 years of lending experience and more than $150 million in funded loans, I've walked thousands of borrowers through this exact decision at David Roa. I've seen cash-out refinances build real wealth for homeowners and investors alike, and I've seen people rush in without understanding the full picture.

This guide breaks down every step of the cash-out refinance process, from eligibility requirements to closing costs to the risks you need to weigh. By the end, you'll have a clear understanding of whether this option fits your situation and what alternatives might serve you better.

Why a cash-out refinance matters

Your home is likely your largest single asset, and the equity you've built inside it doesn't have to sit idle. Home equity grows every time you make a mortgage payment or your property value increases, and a cash-out refinance is one of the most direct ways to convert that value into usable capital. Rather than applying for a separate loan or line of credit with its own terms and timeline, you restructure your primary mortgage and walk away with cash you can deploy however your situation demands.

Your equity is a financial resource, not just a number

Many homeowners view their equity as something to preserve and protect, rather than a tool they can actively use. But liquid cash serves you better in most real-world financial situations than equity sitting locked inside a property. When you understand how does a cash out refinance work, you begin to see your home not just as a place to live, but as a financial instrument you can use to create options.

The difference between your home's current market value and your outstanding mortgage balance is your accessible equity. If your home is worth $400,000 and you owe $200,000, you have $200,000 in equity on paper. Most lenders allow you to borrow up to 80% of your home's appraised value, which sets the ceiling for how much cash you can realistically pull out. In this example, that could mean up to $120,000 in accessible funds, depending on your lender and loan type.

Equity sitting in a property produces no financial returns until you put it to work, whether through a refinance, a strategic sale, or a well-planned investment.

Why borrowers choose this over other options

Personal loans and credit cards carry significantly higher interest rates than a mortgage. For borrowers who need $30,000 or more, the difference between paying 20% or more on a credit card versus a mortgage rate in the 6% to 8% range adds up to tens of thousands of dollars in interest over time. A cash-out refinance gives you access to large sums at mortgage-level rates, which is lower than nearly any other consumer lending product available to you.

Home improvement projects represent one of the most practical uses. A kitchen renovation or a bathroom addition can increase your property's resale value, meaning the cash you extract may return to you, and then some, when you eventually sell. Real estate investors also use cash-out refinances to fund down payments on additional rental properties, a strategy that compounds portfolio growth without waiting years to accumulate savings from scratch.

When the timing makes a real difference

The current interest rate environment directly affects whether a cash-out refinance works in your favor. If you locked in a historically low rate several years ago, replacing that mortgage with a higher-rate loan raises your monthly payment even before accounting for the larger loan balance. That added cost needs to be justified by what you do with the cash.

Your specific financial goal shapes the math. Pulling equity to eliminate high-interest debt can make sense even when mortgage rates are elevated, because your overall cost of borrowing goes down across all accounts. But tapping equity for non-essential spending when rates are high rarely produces a net benefit. The numbers need to support the decision before you move forward.

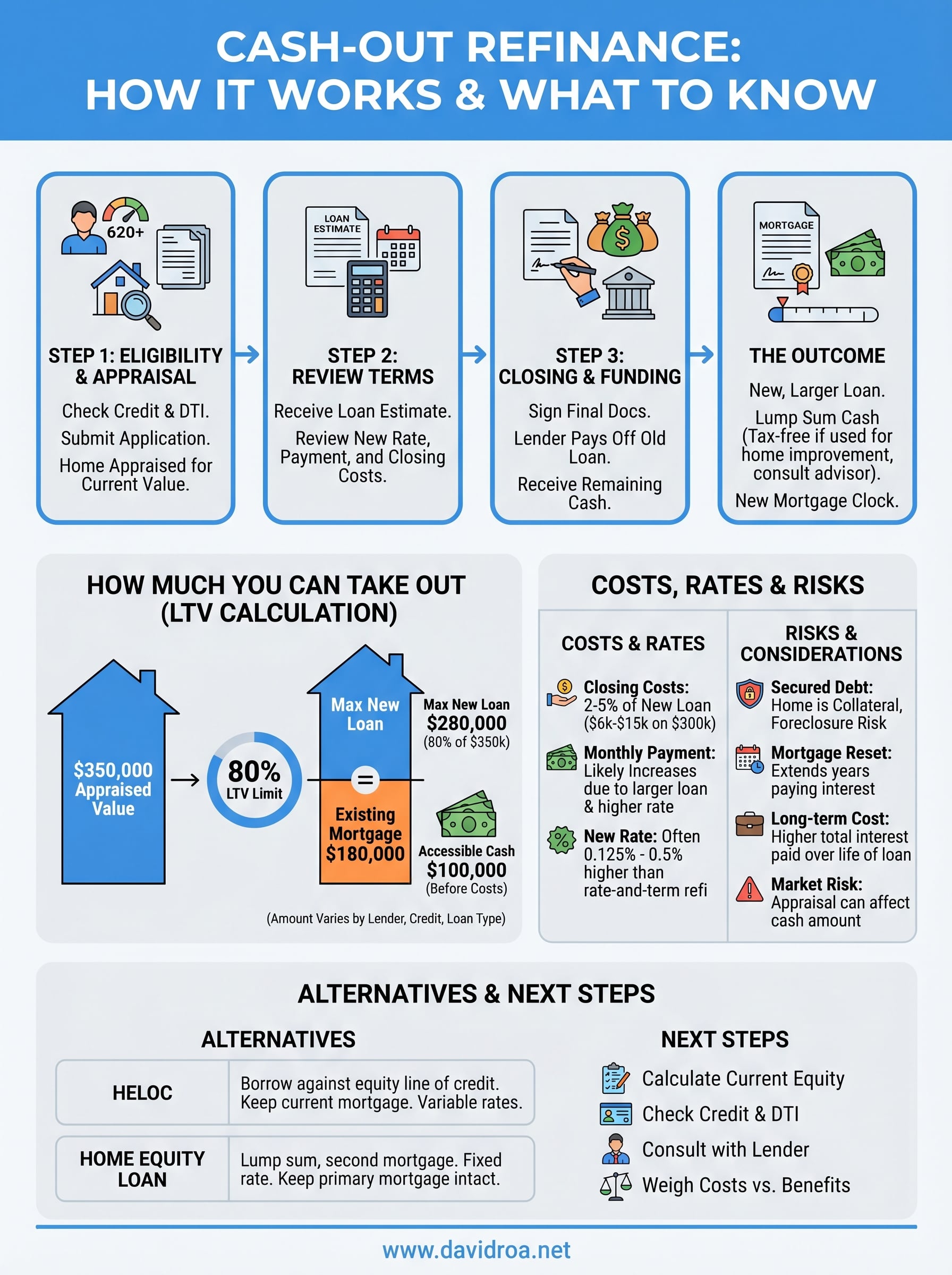

How a cash-out refinance works step by step

Understanding how does a cash out refinance work at a mechanical level helps you move through the process with confidence. The sequence is straightforward: you apply for a new mortgage larger than your current balance, your lender pays off the old loan, and you receive the remaining funds at closing. Each stage has specific requirements and decision points that directly affect your final outcome.

Step 1: Check your equity and eligibility

Before you contact a lender, you need a realistic picture of your current equity position and whether your credit profile qualifies you for favorable terms. Most lenders require a minimum credit score of 620 for a conventional cash-out refinance, though a score above 700 typically unlocks better rates. You also need at least 20% equity remaining in your home after the refinance closes, meaning you cannot borrow all the way to your property's full appraised value.

Lenders will also review your debt-to-income ratio, generally requiring it to stay below 43% to 45%. If your existing debts plus the proposed new mortgage payment push beyond that threshold, your application will likely be denied or require adjustments to the loan structure.

Step 2: Apply and get your home appraised

Once you confirm eligibility, you submit a formal loan application with documentation including pay stubs, tax returns, and bank statements. Your lender then orders a professional home appraisal to establish the property's current market value, which determines the maximum loan amount available to you. The appraisal is a critical step because a lower-than-expected valuation directly reduces the cash you can pull out.

The appraisal result can work for or against you, so understanding your local market conditions before applying gives you a realistic expectation of what you will receive.

Step 3: Review the loan terms and close

After the appraisal, your lender issues a Loan Estimate outlining the new interest rate, monthly payment, closing costs, and cash proceeds. Review every line carefully before you sign anything. At closing, the lender pays off your existing mortgage balance, deducts closing costs, and deposits the remaining funds directly into your bank account.

Federal law requires a three-business-day rescission period on refinances of primary residences, so you will not receive the funds immediately after signing. Once that window closes without cancellation, the money is yours to use.

How much cash you can take out and why

The amount of cash you can pull from your home depends on a straightforward calculation, but several variables shift the final number in meaningful ways. Lenders set a ceiling based on your home's current appraised value, your remaining mortgage balance, and the loan type you qualify for. Understanding these limits upfront prevents surprises late in the process and helps you plan around a realistic cash figure before you spend time gathering documents and submitting applications.

The loan-to-value limit and how it's calculated

Most conventional lenders cap your new loan at 80% of your home's appraised value, which is referred to as the maximum loan-to-value (LTV) ratio. To find your available cash, multiply your home's appraised value by 0.80 and subtract your current mortgage balance. If your home appraises at $350,000, your maximum new loan is $280,000. If you currently owe $180,000, you can take out up to $100,000 in cash before closing costs reduce that figure at the closing table.

The appraisal result drives everything in this calculation, so a lower-than-expected valuation directly reduces the cash available to you.

Your credit score also influences how close to that 80% ceiling a lender will go. Borrowers with stronger credit profiles tend to get approved at higher LTV ratios within program limits, while those near the minimum qualifying score may face a more conservative cap. Lenders also weigh your debt-to-income ratio during this calculation, since a higher existing debt load can narrow the loan amount they're willing to extend even when your equity position looks strong.

How loan type changes your limit

Not every program follows the same 80% rule, and knowing how does a cash out refinance work across different loan types helps you identify which product fits your situation best. VA loans allow eligible veterans to borrow up to 100% of their home's value in certain cases, making them one of the most flexible cash-out options available.

FHA cash-out refinances cap the LTV at 80%, matching conventional guidelines, but they carry mortgage insurance requirements that raise your overall borrowing cost. Jumbo loans, which exceed conforming loan limits set by the Federal Housing Finance Agency, often impose stricter LTV caps, sometimes at 70% or lower depending on the lender, property type, and total loan size.

Costs, rates, and payment changes to expect

A cash-out refinance is not a free transaction. You are taking out a new mortgage, which means you will pay closing costs similar to what you paid when you first bought the home, and your monthly payment will almost certainly change. Knowing these numbers in advance helps you decide whether the cash you receive justifies the costs you absorb.

Closing costs you'll pay upfront

Most cash-out refinances carry closing costs between 2% and 5% of the new loan amount. On a $300,000 refinance, that means $6,000 to $15,000 in fees before you see a dollar of cash proceeds. These costs typically include the appraisal fee, title search, lender origination fee, and prepaid items like homeowners insurance and property taxes. Some lenders offer a "no-closing-cost" option, but that simply rolls the fees into your loan balance or compensates with a higher interest rate, meaning you pay over time rather than upfront.

Rolling closing costs into your loan balance increases the total interest you pay over the life of the loan, so run the numbers on both options before you decide.

How your rate and monthly payment shift

Understanding how does a cash out refinance work on a cost level means looking at your new rate against your current one. Because you are borrowing more money at today's rates, your monthly payment will increase in most scenarios. Even a modest rate difference compounded over a larger loan balance adds up significantly over a 30-year term. Lenders also typically price cash-out refinances slightly higher than rate-and-term refinances, often by 0.125% to 0.5%, because they view the higher loan balance as added risk.

What breakeven actually means for you

Your breakeven point is how long it takes for your financial benefit to offset the cost of refinancing. Divide your total closing costs by the monthly savings or income generated by the cash you receive. If you spend $8,000 in closing costs and the cash you pull out generates $400 per month in value, you break even in 20 months. If you plan to sell or refinance again before that point, the transaction may cost you more than it returns.

Risks, pros, cons, and alternatives

Understanding how does a cash out refinance work means looking honestly at both sides of the transaction. The cash you receive comes with a larger mortgage balance, a potentially higher rate, and a longer timeline to pay off your home. Before you commit, weigh the full picture rather than focusing only on the lump sum you receive.

The real risks you're taking on

The most significant risk is converting unsecured debt into secured debt. If you pull equity to pay off credit cards and then run those balances back up, you've added to your total debt load while putting your home on the line as collateral. A cash-out refinance also resets your mortgage clock, meaning you could extend the years you spend paying interest even if your current loan is nearly paid off.

Your home secures the new loan, so a financial setback that leads to missed payments puts you at risk of foreclosure in a way that credit card debt never does.

When it works in your favor

A cash-out refinance genuinely benefits you in specific situations. The pros are strongest when your use of funds produces a measurable return, such as a home improvement that raises your property value or a debt consolidation that drops your total monthly obligations.

- Access to large amounts of capital at mortgage-level interest rates

- Potential tax benefits if funds are used for home improvements (consult a tax advisor)

- Single monthly payment instead of managing multiple high-interest accounts

- Flexibility to fund real estate investments or business capital needs

Alternatives worth considering

If the risks outweigh the benefits in your current situation, two strong alternatives exist. A home equity line of credit (HELOC) lets you borrow against your equity without replacing your existing mortgage, preserving your original rate while giving you flexible access to funds. A home equity loan delivers a lump sum at a fixed rate as a second mortgage, so your primary loan stays untouched. Both options carry lower closing costs and leave your current mortgage terms intact, which matters significantly if you locked in a low rate.

Next steps before you refinance

Now that you understand how does a cash out refinance work, the next move is to get clear on your specific numbers before you apply. Pull your most recent mortgage statement, check your home's estimated value using recent comparable sales in your area, and calculate your current equity position. That single calculation tells you whether this option is worth pursuing or whether an alternative like a HELOC fits your situation better.

From there, review your credit score and your debt-to-income ratio so you walk into a lender conversation with realistic expectations. The borrowers who get the best terms are the ones who arrive prepared, not caught off guard by what they find during underwriting.

When you're ready to talk through your options with someone who has funded more than $150 million in loans across every type of scenario, reach out to David Roa to get a clear, direct assessment of what makes the most financial sense for your situation.