How To Finance Investment Property: Loans, Rates, And Steps

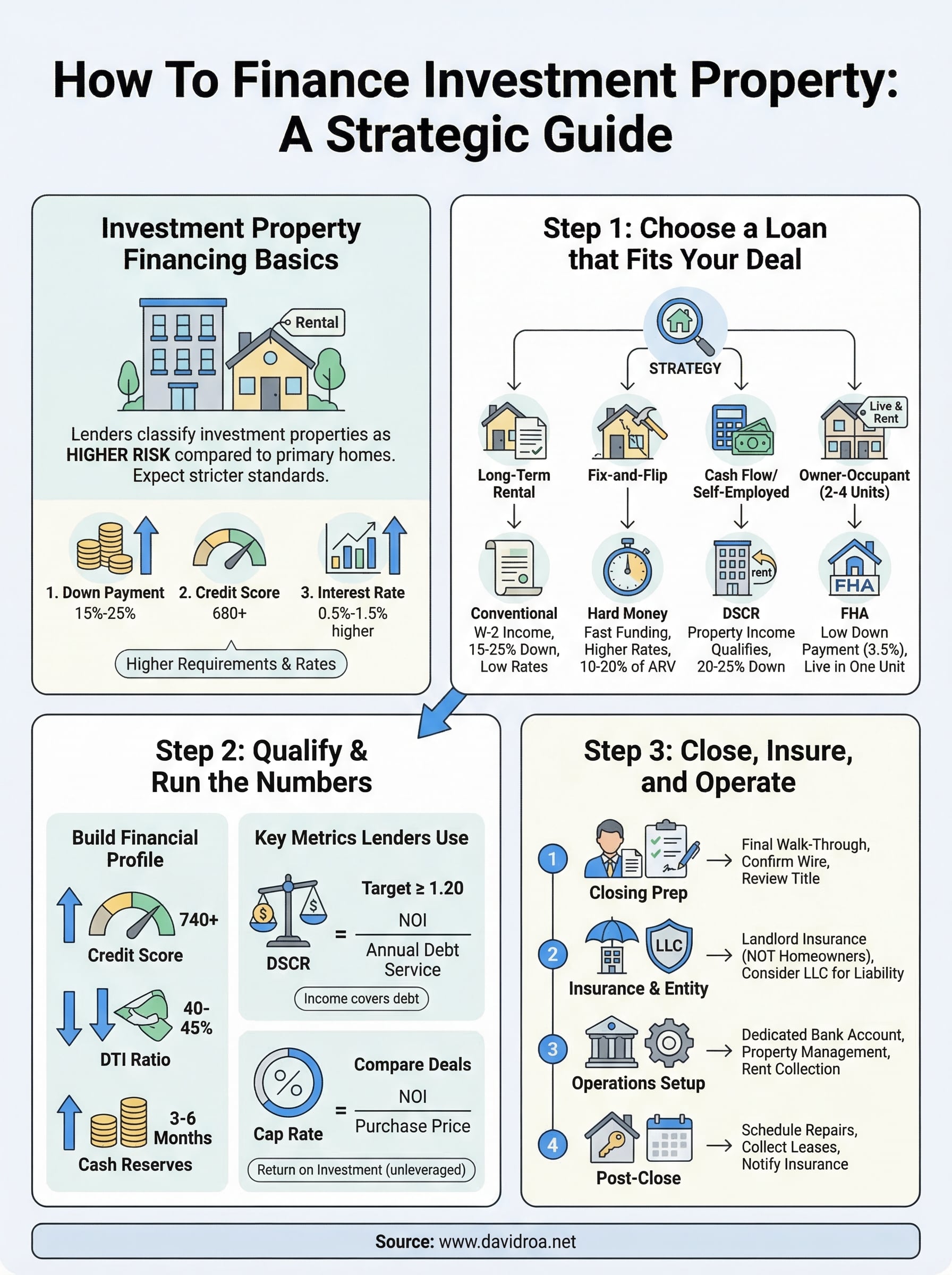

Buying a rental or flip property is one of the fastest ways to build wealth, but only if you get the financing right. Knowing how to finance investment property starts with understanding that lenders treat these deals differently than a standard home purchase. Expect higher down payments, stricter credit requirements, and interest rates that reflect the added risk lenders take on.

The good news: you have more loan options than most people realize. From conventional mortgages and DSCR loans to hard money and SBA-backed programs, each path fits a different investor profile and strategy. The key is matching the right product to your deal, whether you're buying a long-term rental, flipping a distressed property, or acquiring a mixed-use building.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment properties. With 25+ years of hands-on lending experience, plus our own active real estate investment portfolio, we understand both sides of the transaction. This guide breaks down every major financing option, the rates you can expect, qualification requirements, and the exact steps to close your next investment property deal.

Investment property financing basics

Before you apply for a single loan, you need to understand how lenders think about investment properties. Lenders classify investment properties as higher-risk assets compared to primary residences because borrowers are statistically more likely to default on a property they don't live in. That means you'll face stricter underwriting standards across every loan type, from conventional mortgages to portfolio products, and knowing this framework upfront saves you from surprises during underwriting.

How lenders classify investment properties

Lenders separate properties into three categories: primary residences, second homes, and investment properties. Investment properties include single-family rentals, multifamily buildings with two to four units or more, fix-and-flip houses, and commercial real estate. Each category carries a different risk weight, which directly affects your interest rate, down payment requirement, and loan eligibility.

A two-unit property you plan to rent entirely is an investment property. A beach house you use personally a few months each year and occasionally rent is a second home. The distinction matters because misrepresenting your occupancy intention is mortgage fraud. Lenders verify your intent through your application, existing property ownership records, and the distance between properties.

Key differences from a primary home loan

When you're figuring out how to finance investment property, the gap between investment loans and standard home loans is significant. The table below shows the core differences you need to plan around before you make an offer:

| Factor | Primary Residence | Investment Property |

|---|---|---|

| Minimum down payment | 3% to 5% | 15% to 25% |

| Interest rate premium | Baseline rate | 0.5% to 1.5% higher |

| Credit score minimum | 580 to 620 | 620 to 680+ |

| Cash reserves required | 0 to 2 months | 3 to 6 months |

| Rental income counted | Not applicable | 75% of gross rents (varies) |

The rate premium on investment properties reflects default statistics, not a lender's arbitrary penalty. Knowing the spread before you run your numbers keeps your cash flow projections honest.

These differences don't make investment property financing out of reach. They mean you need to prepare your capital stack and credit profile in advance, not after a seller accepts your offer.

What lenders look at before approving you

Every lender runs a version of the same checklist, though the weight each factor receives varies by loan type. Your credit score, debt-to-income ratio (DTI), and cash reserves are the three levers that most directly control your rate and approval odds. On conventional loans, a DTI above 45% is typically a deal-breaker. On DSCR loans, your personal income matters far less because the property's cash flow becomes the primary qualifier instead.

Here's what lenders review before approving an investment property loan:

- Credit score: Most conventional products require 680 or higher for investment properties; DSCR and hard money lenders may accept scores in the 620 to 660 range.

- Down payment source: Lenders want seasoned funds, meaning money that has been in your account for at least 60 days before closing.

- Reserves: Expect to show 3 to 6 months of mortgage payments in liquid assets after your down payment clears.

- Property type and condition: A stabilized single-family rental is easier to finance than a distressed four-unit building with deferred maintenance.

- Rental income documentation: Lenders may use existing leases, market rent appraisals, or a percentage of projected rents depending on the loan program.

Understanding this checklist before you start shopping properties puts you in a stronger negotiating position with both sellers and lenders.

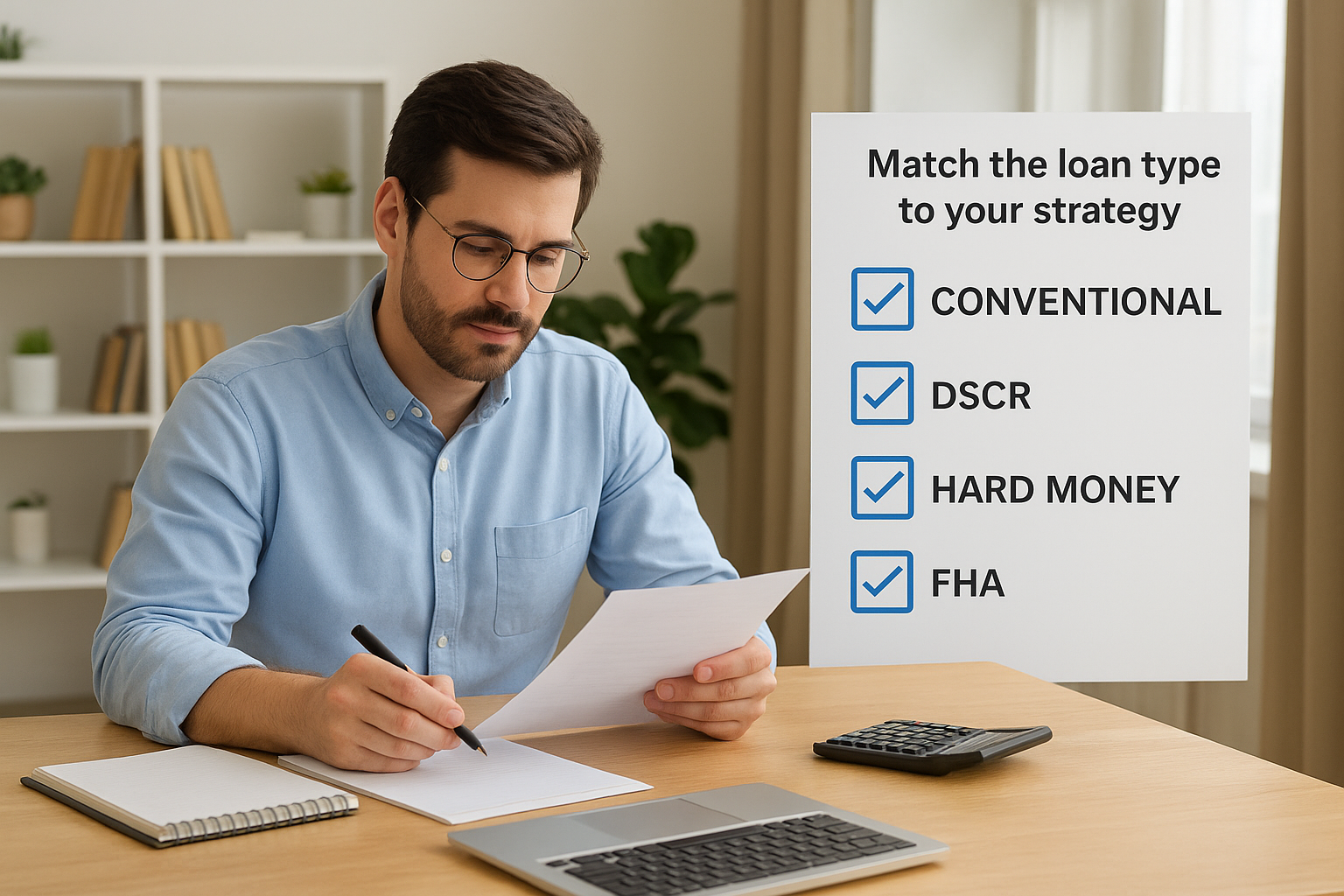

Step 1. Choose a loan that fits your deal

The first decision shapes every number in your deal. Your loan type determines your interest rate, down payment, closing timeline, and qualifying criteria, so picking the wrong product can kill a deal that would otherwise cash flow well. When figuring out how to finance investment property, start with your exit strategy and work backward to the loan that fits it.

Match the loan type to your strategy

Different investment strategies need different loan products. A long-term buy-and-hold investor needs low monthly payments and predictable terms over 15 to 30 years. A fix-and-flip investor needs fast funding with flexible repayment tied to the eventual sale. Here is a breakdown of the most common investment property loan types and where each one fits:

| Loan Type | Best For | Down Payment | Typical Rate Range |

|---|---|---|---|

| Conventional | Long-term rentals, strong W-2 income | 15% to 25% | 7% to 8.5% |

| DSCR | Cash-flow-based investors, self-employed | 20% to 25% | 7.5% to 9% |

| Hard Money | Fix-and-flip, fast closings | 10% to 20% of ARV | 10% to 13% |

| FHA (house hack) | Owner-occupant buying 2 to 4 units | 3.5% | 6.5% to 7.5% |

| SBA 504 | Commercial or mixed-use, owner-occupied | 10% | 6% to 8% |

DSCR loans are one of the most flexible tools available for investors who earn income through their real estate portfolio rather than a traditional paycheck.

How to narrow down your options

Once you know which category fits your strategy, two filters help narrow your choice: your credit profile and your timeline to close. Conventional loans offer the lowest rates but require 30 to 45 days and full income documentation. Hard money lenders can fund in 7 to 14 days but carry higher rates that only work when your rehab margin is wide enough to absorb that cost.

Ask yourself these three questions before you commit to a loan product:

- Do I need to close fast, or do I have time for full underwriting?

- Can I qualify on personal income, or does the property need to carry itself through rental cash flow?

- What is my hold period, and does a short-term rate structure create refinance risk before I stabilize the asset?

Your answers point directly to the right loan type and prevent you from wasting time applying for a product that was never built for your situation.

Step 2. Qualify for the best rate and terms

Your loan type opens the door, but your financial profile determines what it costs you to walk through it. Every 0.25% improvement in your interest rate translates directly into better monthly cash flow and a stronger return on your capital. Before you submit a single application, spend time hardening your credit score, reducing your debt load, and assembling a complete documentation package so you negotiate from a position of strength rather than react to whatever rate a lender quotes you first.

Build your credit profile before you apply

Lenders price investment property loans off your credit score, and the gap between a 680 and a 740 can mean a full percentage point or more in rate. Pull your credit reports from all three bureaus at least 60 to 90 days before you apply. Dispute any reporting errors immediately because corrections take time to process through the bureaus and a pending dispute can stall underwriting.

Focus on two levers that move your score fastest: pay down revolving balances below 30% of each credit limit and avoid opening any new accounts in the 90 days before you apply. A new inquiry or a new installment account signals credit-seeking behavior that underwriters flag, even when your overall score looks strong on the surface.

Pushing your score from the 680 range to 740 or above before you apply is often worth a short delay in your timeline, especially on larger loan amounts where the rate savings compound across a 30-year term.

Lower your DTI to expand your options

Debt-to-income ratio controls which loan products you qualify for and directly affects your pricing on conventional financing. Most conventional investment property programs cap DTI at 45%, and programs with the sharpest rates typically want you below 40%. Pay off any installment loans with fewer than 10 payments remaining before you apply, since most lenders exclude those balances from your DTI calculation entirely.

When working out how to finance investment property using DSCR products, your personal DTI matters far less, but your existing mortgage obligations still appear on your credit report and shape a lender's overall risk view. Keep that in mind if you already carry several financed properties.

Prepare your documentation package

Lenders move faster when your file is complete on day one. Disorganized documentation adds days or weeks to underwriting and gives lenders a reason to condition your approval. Gather these documents before you submit:

- Last 2 years of federal tax returns with all schedules

- Last 2 months of bank statements for every account you plan to use for reserves or down payment

- Current signed leases or a market rent appraisal for the subject property

- Proof of insurance on any existing investment properties you own

- Entity documents such as your articles of organization if you are purchasing through an LLC

Step 3. Run the numbers lenders and investors use

Financing a property without running the core metrics first is how investors end up owning assets that drain their cash reserves instead of building them. Lenders use specific ratios to approve or deny your loan, and investors use those same ratios to decide if a deal is worth buying in the first place. Learning how to finance investment property also means learning to speak the same numerical language your lender uses before you ever submit an application.

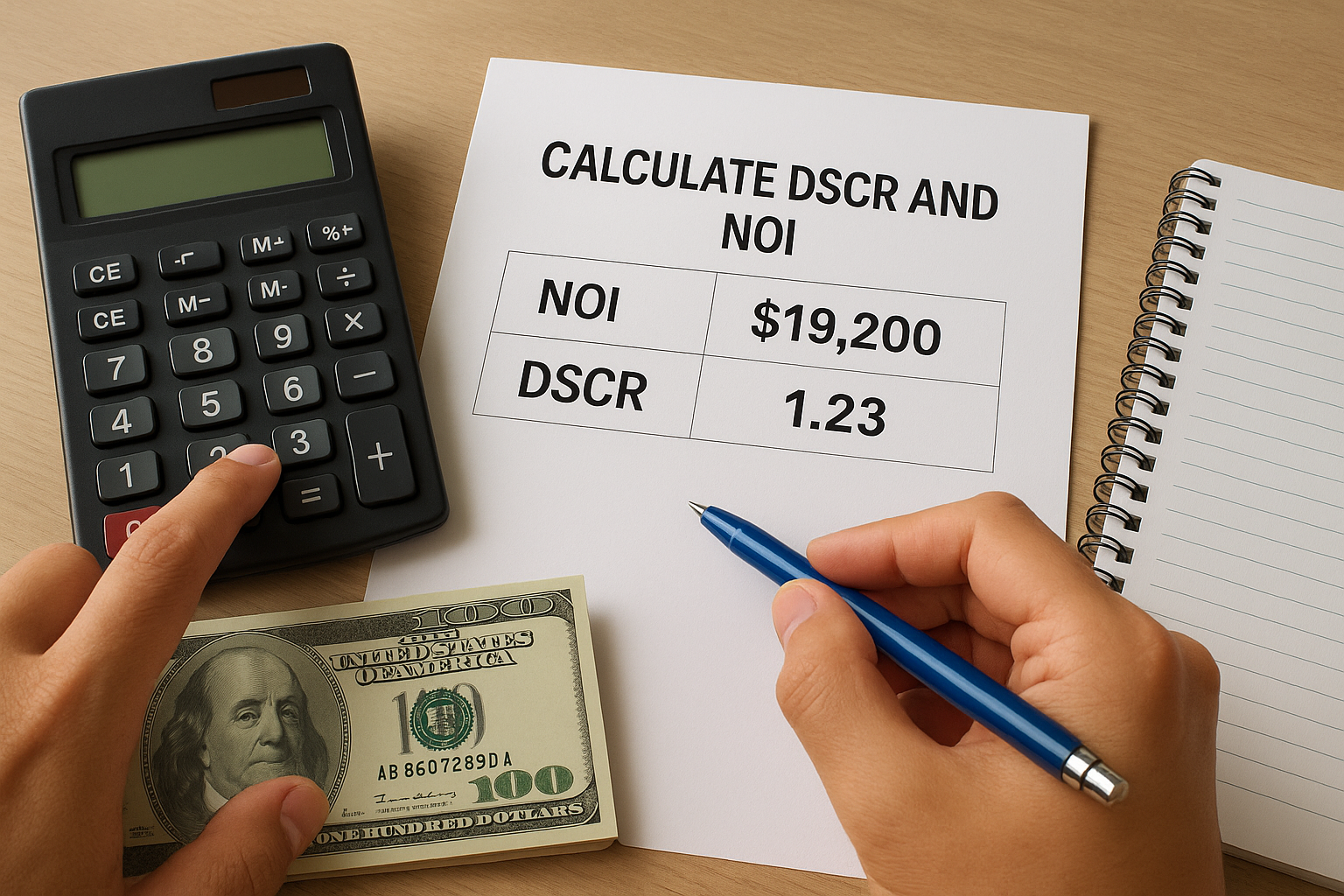

Calculate DSCR and NOI

Your net operating income (NOI) is the starting point for almost every investment property calculation. Subtract all operating expenses from your gross rental income to get it. Operating expenses include property taxes, insurance, property management fees, maintenance reserves, and vacancy allowance. Do not include your mortgage payment in this calculation because NOI is a pre-debt figure.

Once you have your NOI, divide it by your annual debt service (total principal and interest payments) to get your debt service coverage ratio, or DSCR. A DSCR of 1.0 means the property generates exactly enough income to cover its loan payments. Most DSCR lenders want to see a ratio of 1.20 or higher, meaning the property earns 20% more than its annual debt obligation.

Use this template to run the calculation before you apply:

| Line Item | Example Amount |

|---|---|

| Gross monthly rent | $2,500 |

| Vacancy allowance (8%) | -$200 |

| Property management (10%) | -$250 |

| Taxes and insurance | -$350 |

| Maintenance reserve | -$100 |

| Monthly NOI | $1,600 |

| Annual NOI | $19,200 |

| Annual debt service | $15,600 |

| DSCR | 1.23 |

A DSCR above 1.25 gives you a buffer that covers unexpected vacancies or repair costs without pushing your property into negative cash flow territory.

Use cap rate to compare deals

Capitalization rate (cap rate) tells you the return a property generates independent of how you finance it. Divide the annual NOI by the purchase price to calculate it. A property generating $19,200 in annual NOI purchased for $240,000 carries an 8.0% cap rate.

Cap rate lets you compare two deals on equal footing even when their financing structures are completely different. Markets with higher cap rates typically carry more risk or lower appreciation potential, so use it as a comparison tool alongside DSCR rather than the only metric you rely on.

Step 4. Close, insure, and set up operations

You've selected your loan, qualified, and run your numbers. Now the deal moves from spreadsheet to reality. Closing an investment property requires more preparation than a standard home purchase, and the work you do in the 48 hours before and after closing directly affects your cash flow, legal protection, and long-term returns.

What to expect at the closing table

Your lender will issue a Closing Disclosure at least three business days before your scheduled closing date. Review every line item against your Loan Estimate to confirm the rate, fees, and cash-to-close haven't changed. If there's a discrepancy, flag it immediately because last-minute corrections can delay your closing date and cost you your rate lock.

Before you sit down to sign, verify these items are complete:

- Final walk-through of the property to confirm the condition matches your contract

- Wiring instructions confirmed directly with your closing attorney or title company by phone, not email, to prevent wire fraud

- Cashier's check or wire for your down payment and closing costs sent 24 hours ahead when possible

- Title insurance commitment reviewed for any exceptions or liens you didn't anticipate

Set up insurance and entity structure

Landlord insurance, not standard homeowners insurance, is the product you need before your first tenant moves in. A standard homeowners policy voids the moment you rent the property to someone else. Landlord insurance covers rental income loss, liability claims from tenants, and property damage, all of which a homeowners policy excludes.

Holding investment properties inside an LLC provides liability separation between your personal assets and your rental portfolio. If you plan to use an LLC, work this out before closing because retitling a property after the fact triggers transfer taxes in some states and can complicate your existing financing.

Talk to a real estate attorney about your entity structure before you close, not after, because fixing it retroactively costs significantly more than setting it up correctly the first time.

Build your operations checklist from closing day forward

Part of knowing how to finance investment property is recognizing that closing is the start of operations, not the finish line. Set up a dedicated bank account for rental income and expenses from day one so your records stay clean for tax time and future lender reviews.

Your first-week checklist should include:

- Schedule any deferred maintenance or agreed-upon repairs immediately

- Collect or transfer existing leases and security deposits if the property was tenant-occupied at purchase

- Set up automated rent collection through a property management platform

- Notify your insurance carrier of the closing date and occupancy status

Next steps

Knowing how to finance investment property puts you ahead of most buyers who show up to a lender without a strategy. You now have the full picture: loan types matched to specific strategies, the qualification levers that control your rate, the metrics lenders use to approve deals, and the closing steps that protect your investment from day one. The gap between investors who build portfolios and those who stay stuck at one property is almost always execution, not information.

Your next move is to take the loan type that fits your deal and get a real quote. Pull your credit reports, calculate your DSCR on your target property, and organize your documentation package before you talk to anyone. If your deal involves a complex scenario like DSCR financing, ITIN qualification, or a fix-and-flip timeline, work with a lender who has closed deals like yours before. Connect with David Roa to review your options and build a financing plan around your actual numbers.