How To Get Preapproved For A Mortgage: Step-By-Step

Before you start touring homes or making offers, there's one move that puts you ahead of other buyers: learning how to get preapproved for a mortgage. A pre-approval letter tells sellers and agents you're serious, and it gives you a clear picture of what you can actually afford, no guessing, no wishful thinking.

But the process trips people up more often than it should. Some confuse pre-qualification with pre-approval. Others scramble to gather documents at the last minute or get blindsided by credit score requirements they didn't know about. These mistakes cost time, and in a competitive market, time can cost you the house.

With over 25 years in mortgage lending and more than $150 million funded, I've walked thousands of buyers through pre-approval, from first-time homeowners to investors scaling their portfolios. At David Roa, we handle everything from conventional and FHA loans to specialized programs like ITIN and VA financing, so the guidance here comes straight from daily, hands-on experience closing real deals.

This guide breaks down each step of the pre-approval process, the documents you'll need, the credit and income requirements lenders look for, and the difference between pre-qualification and pre-approval. By the end, you'll know exactly what to do, and what to avoid, so you can walk into your home search with confidence.

What mortgage preapproval is and why it matters

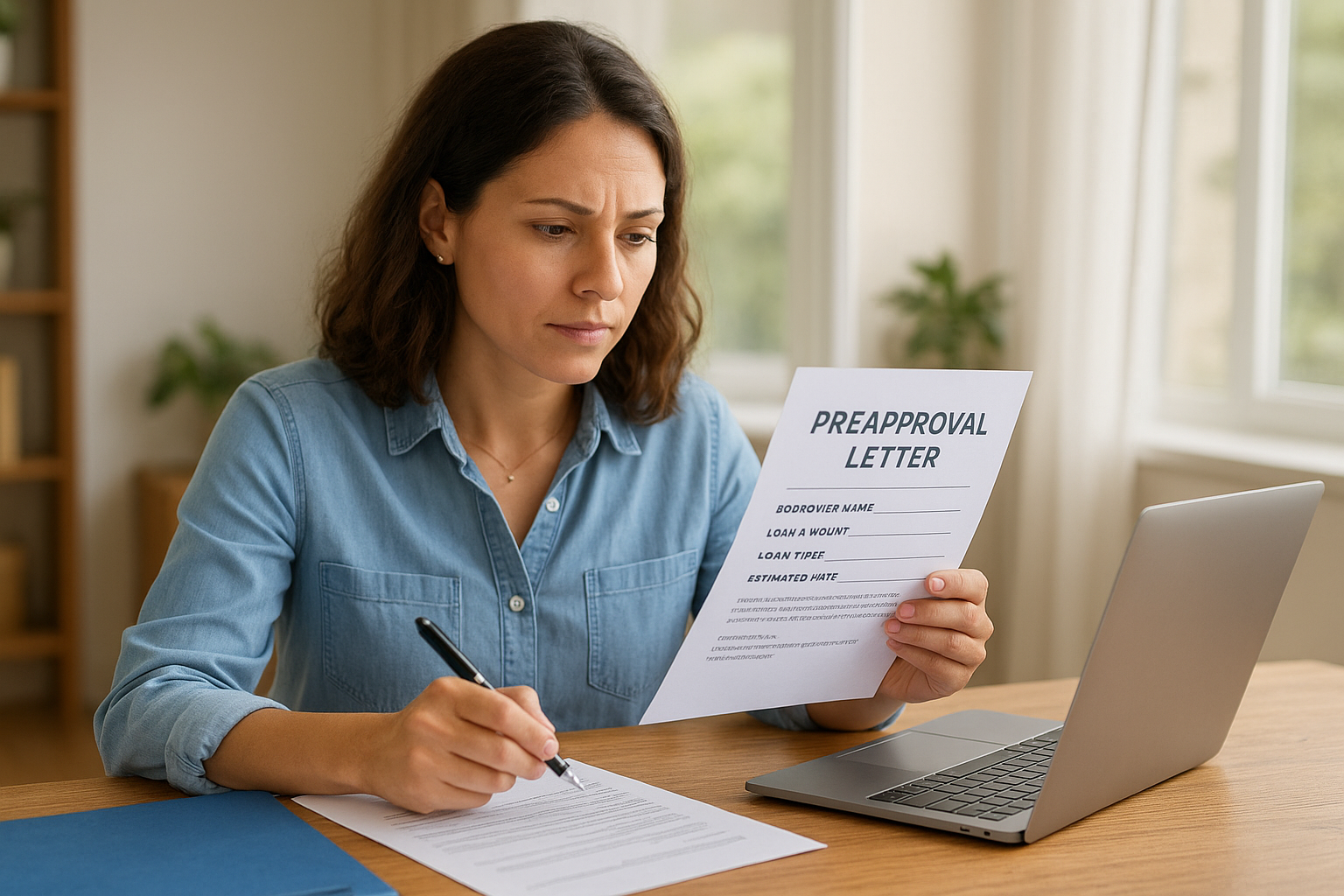

Mortgage preapproval is a formal evaluation by a lender that confirms how much they're willing to lend you based on your actual financial data. Unlike browsing affordability calculators online, preapproval requires you to submit real documentation, such as pay stubs, tax returns, and bank statements, and the lender runs a hard credit inquiry before issuing a decision. The result is a preapproval letter that states a specific loan amount, an estimated interest rate range, and the loan type you qualify for.

Pre-qualification vs. pre-approval: know the difference

These two terms get used interchangeably, but they are not the same thing, and confusing them can put you at a real disadvantage. Pre-qualification is a quick, informal estimate based on self-reported numbers. You tell a lender your income, debts, and assets, and they hand you a rough range with no verification. It takes minutes, but it carries little weight with sellers or real estate agents because nothing has been confirmed.

Pre-approval involves actual verification. The lender pulls your credit report, reviews your documents, and produces a conditional lending commitment in writing. When sellers see a pre-approval letter, they know you've already cleared a meaningful financial review. In competitive markets, some sellers won't even consider an offer without one.

Pre-approval is not a guarantee of final loan approval, but it is the strongest signal you can give a seller before closing.

What a preapproval letter tells sellers

A preapproval letter does more than confirm your budget. It shows sellers that a licensed lender has reviewed your finances and found you creditworthy up to a specific dollar amount. The letter typically includes your name, the lender's contact information and NMLS number, the approved loan amount, the loan type, and an expiration date, usually 60 to 90 days from issuance. Here's what a standard preapproval letter looks like:

[Lender Name] | NMLS #[Number] Date: [Issue Date]

This letter confirms that [Borrower Name] has been pre-approved for a mortgage loan up to $[Loan Amount], based on a review of credit, income, and assets.

- Loan Type: FHA / Conventional / VA / Jumbo / Other

- Estimated Rate: Subject to market conditions at time of closing

- Expiration Date: [60 to 90 days from issue date]

This pre-approval is conditional upon a satisfactory appraisal, clear title, and final underwriting approval.

[Loan Officer Name], NMLS #[Number] | [Contact Information]

How long preapproval lasts

Most preapproval letters expire after 60 to 90 days, so timing your home search matters. Starting too early before your preapproval puts you at risk of it expiring before you find the right property, which means repeating the entire process. Beyond expiration, if your financial situation shifts during that window, such as a job change, new debt, or a drop in your credit score, the lender will need to re-evaluate your file before you can proceed.

Knowing how to get preapproved for a mortgage also means building your home search timeline around your preapproval window, not the other way around.

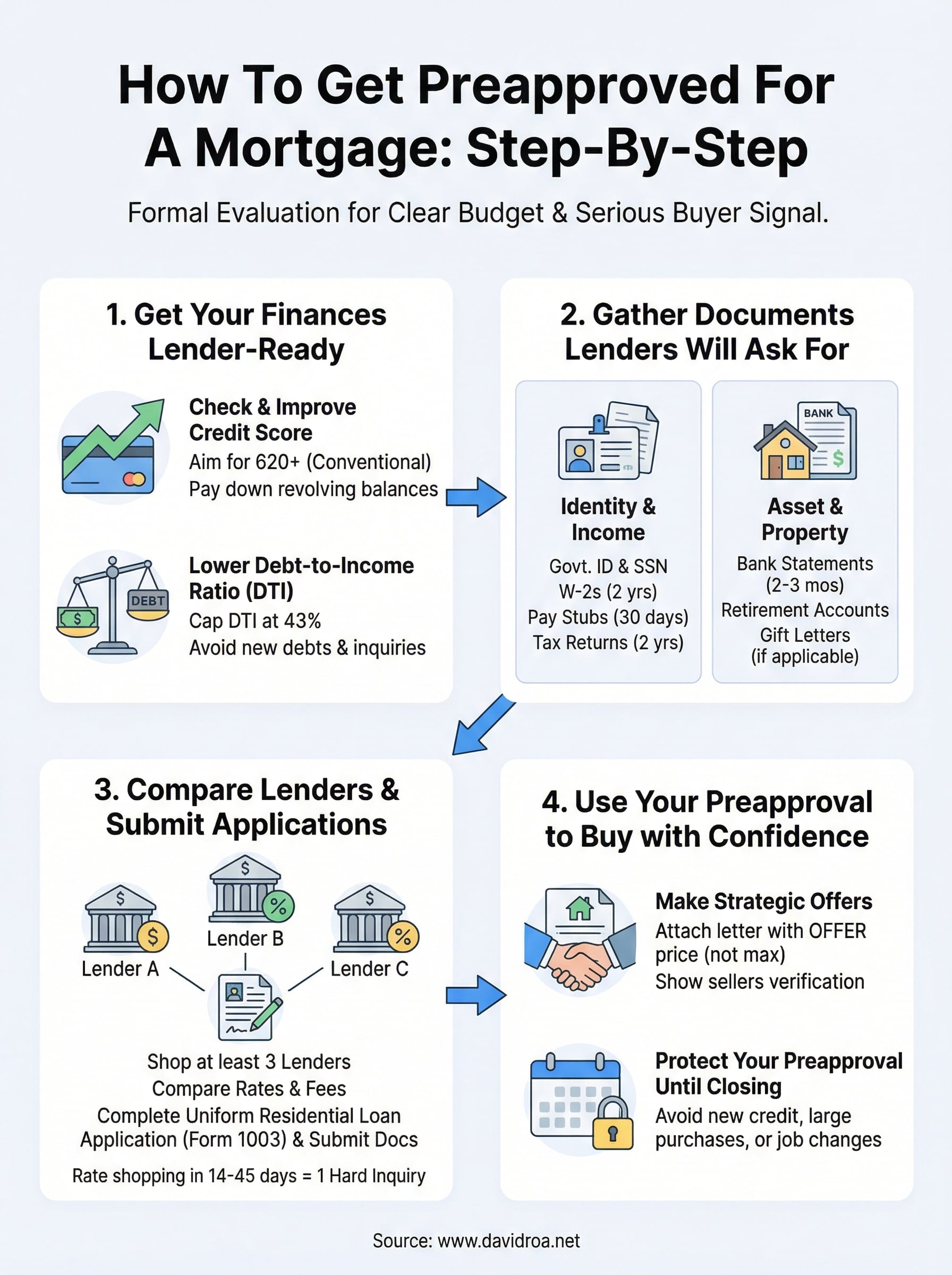

Step 1. Get your finances lender-ready

Before you submit a single application, you need your financial profile to be in the strongest position possible. Lenders evaluate three core areas when deciding how much to lend you and at what rate: your credit score, your debt-to-income ratio (DTI), and the stability of your income. Taking time to address each of these factors before you apply gives you a real advantage when the lender opens your file.

Check and improve your credit score

Your credit score is one of the first data points a lender reviews when you begin the process of how to get preapproved for a mortgage. For a conventional loan, most lenders require a minimum score of 620. FHA loans accept scores as low as 580 with a 3.5% down payment, while VA loans carry no official minimum though most lenders set their own floor around 620.

Pulling your own credit report does not hurt your score. Request your free annual report at AnnualCreditReport.com, the only federally authorized source under federal law.

Review your report for errors, outdated collections, and high revolving balances. Even a 30 to 40-point improvement from paying down one card can move you into a lower rate tier and save you thousands over the life of the loan.

Lower your debt-to-income ratio

Lenders calculate your debt-to-income ratio (DTI) by dividing your total monthly debt payments by your gross monthly income. Most programs cap DTI at 43%, though certain loan types allow up to 50% with compensating factors. Here's how the numbers break down:

| Monthly Gross Income | Total Monthly Debts | DTI Ratio |

|---|---|---|

| $6,000 | $2,000 | 33% (strong) |

| $6,000 | $2,700 | 45% (borderline) |

| $6,000 | $3,100 | 52% (likely too high) |

Pay down revolving balances in the two to three months before you apply. Avoid opening new credit accounts or taking on additional loans during that window, since both actions raise your monthly debt load and trigger hard inquiries that can pull your score down right before a lender reviews it.

Step 2. Gather documents lenders will ask for

Lenders don't take your word for anything on a mortgage application. When you're working through how to get preapproved for a mortgage, document preparation is the step where most applicants slow down or stall. Gathering everything before you contact a lender keeps your file moving and prevents delays that push your timeline back by days or weeks.

Identity and income documents

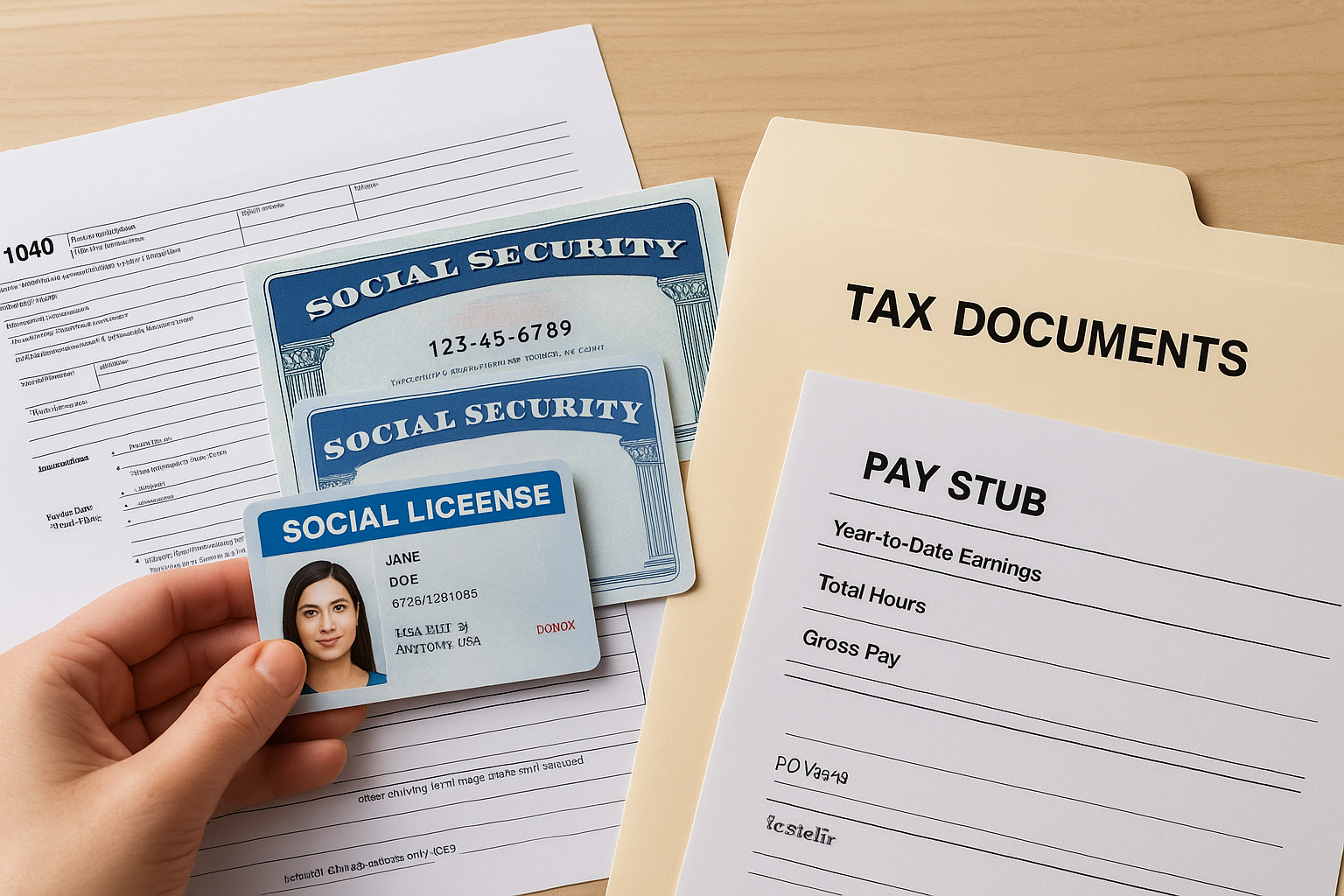

The lender needs to confirm who you are and verify that your income is consistent and documentable. Pull these together before you submit a single application:

- Government-issued photo ID: Driver's license or passport

- Social Security number (ITIN accepted on select loan programs, including non-U.S. citizen programs)

- Two years of W-2s (or 1099s if you are self-employed or a contract worker)

- 30 days of recent pay stubs showing year-to-date earnings

- Two years of federal tax returns, all schedules included

- Proof of additional income: Social Security award letters, rental income records, or court-ordered alimony documentation if applicable

Self-employed borrowers should expect lenders to average net income across both years, so one strong year alone does not carry the application.

Asset and property documents

Your income tells lenders you can make the monthly payment. Asset documentation tells them you have the funds to actually close. Lenders will trace any large or unusual deposits in your account history to verify the source, so keep your accounts clean and avoid moving money around in the two to three months before you apply.

Gather the last two to three months of statements for every account you plan to use: checking, savings, retirement, and investment accounts. If someone is gifting part of your down payment, you'll also need a gift letter from the donor. Here's a basic template:

Mortgage Gift Letter Date: [Date] Donor Name and Relationship: [Full Name] | [Relationship to Borrower] Gift Amount: $[Amount] Source of Funds: [Bank Name, Last 4 Digits of Account] Statement: "These funds are a gift and are not a loan. No repayment is expected or required." Donor Signature: _________________ Date: _________

Step 3. Compare lenders and submit applications

Most buyers apply with the first lender they find and leave real money on the table. Shopping at least three lenders before you commit is one of the most impactful moves you can make when you're figuring out how to get preapproved for a mortgage. A difference of even a quarter of a percentage point on your interest rate can add up to tens of thousands of dollars over a 30-year loan.

How to evaluate lenders side by side

Not all lenders offer the same products, rates, or turnaround times. You want to compare loan options, estimated rates, and lender fees before you decide where to submit your full application. Ask each lender for a Loan Estimate, which is a standardized three-page form that breaks down every cost associated with the loan, including origination fees, title fees, and prepaid expenses.

Rate shopping within a 14 to 45-day window typically counts as a single hard inquiry under FICO scoring models, so applying to multiple lenders in that window protects your credit score.

Use this comparison framework when you evaluate your options:

| Factor | What to Look For |

|---|---|

| Interest rate | Compare APR, not just the stated rate |

| Origination fee | Ask if it's a flat fee or a percentage of the loan |

| Loan types offered | Confirm they offer the program you need (FHA, VA, DSCR, ITIN, etc.) |

| Response time | Ask how long preapproval typically takes |

| Communication style | You want a direct point of contact, not a call center |

What to do when you submit your application

Once you select a lender, the formal submission is straightforward. Complete the Uniform Residential Loan Application (Form 1003) honestly and accurately, then attach every document from the list in Step 2. Gaps or inconsistencies in your file are the most common reason preapprovals get delayed, so review your submission before you send it.

After submission, the lender will process your file, run the hard credit pull, and typically issue a decision within one to three business days. Some lenders, including brokers who work with multiple underwriters, can move faster. Ask upfront what the expected timeline is so you can plan your home search accordingly.

Step 4. Use your preapproval to buy with confidence

Your preapproval letter is not just paperwork. It's a negotiating tool that puts you ahead of buyers who are still figuring out how to get preapproved for a mortgage while you're already ready to move. Once you have it, the goal is to use it strategically, protect the financial standing that earned it, and act decisively when you find the right property.

Make strategic offers with your letter in hand

When you submit an offer, your agent attaches your preapproval letter to show the seller you're financially verified and ready to close. Most sellers weigh multiple offers, and one backed by a preapproval letter from a credible lender carries far more weight than one with a basic pre-qualification estimate. One tactical move: ask your lender to issue the letter at the specific purchase price, not your maximum approved amount. This keeps your full borrowing capacity private while still satisfying the seller's requirements.

A preapproval letter issued at the exact offer price, rather than your maximum, prevents sellers from knowing your full budget and gives you room to negotiate.

Use this checklist each time you submit an offer:

- Attach the preapproval letter matching the exact offer price

- Confirm the letter is dated within the last 30 days to signal it's current

- Have your agent share the lender's direct contact information so the listing agent can verify the letter

- Avoid adding contingencies that weaken your position unless the situation genuinely requires them

Protect your preapproval until closing

Keeping your financial profile stable from preapproval through closing day is not optional. Lenders run a final credit check before funding, and any changes to your debt, income, or employment during that window can trigger a full re-evaluation or an outright denial.

Follow these rules until your loan closes: do not open new credit accounts, do not make large purchases on existing cards, avoid changing jobs, and keep your bank balances consistent. Notify your loan officer immediately if anything shifts in your financial situation, since catching issues early gives the lender time to address them before they affect your closing date.

Your next move

You now have a complete picture of how to get preapproved for a mortgage, from cleaning up your credit and organizing your documents to comparing lenders and protecting your file through closing. The process is straightforward when you prepare in the right order and know exactly what lenders are looking for at each stage.

The next step is simple: start with your financial profile today. Pull your credit report, run your DTI numbers, and begin gathering the documents from Step 2. The buyers who move fast in competitive markets are the ones who already have their preapproval in hand before they fall in love with a property.

If you want experienced guidance through the process, especially for complex situations like ITIN loans, DSCR financing, or FHA programs, connect with David Roa directly. With over 25 years of lending experience and $150 million funded, the right loan for your situation is a conversation away.