DSCR Loan Qualification: How To Qualify For DSCR Loan

Most real estate investors hit a wall when they try to finance rental properties through traditional lenders. Banks want W-2s, tax returns, and a debt-to-income ratio that doesn't account for the income your properties actually generate. That's exactly the problem DSCR loans solve. If you're wondering how to qualify for a DSCR loan, the short answer is this: the property's rental income does the heavy lifting, not your personal financials. But there are still specific requirements you need to meet, credit score thresholds, down payment minimums, and a debt service coverage ratio that proves the deal makes sense.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment properties, and DSCR loans are one of the most requested products from our investor clients. With 25+ years in the lending business, and hands-on experience as a real estate investor myself, I've walked hundreds of borrowers through exactly what it takes to qualify.

This guide breaks down every eligibility requirement, from credit scores and down payments to how lenders calculate your DSCR ratio. By the end, you'll know where you stand and what steps to take next to get approved. Let's get into it.

What a DSCR loan is and what lenders check

A DSCR loan (Debt Service Coverage Ratio loan) is an investment property mortgage where the lender qualifies you based on the rental income the property generates, not your personal tax returns or W-2s. This structure makes it one of the most practical financing options for real estate investors, particularly if you're self-employed, own multiple properties, or your personal income on paper doesn't reflect your actual financial position.

The core concept: property income covers the debt

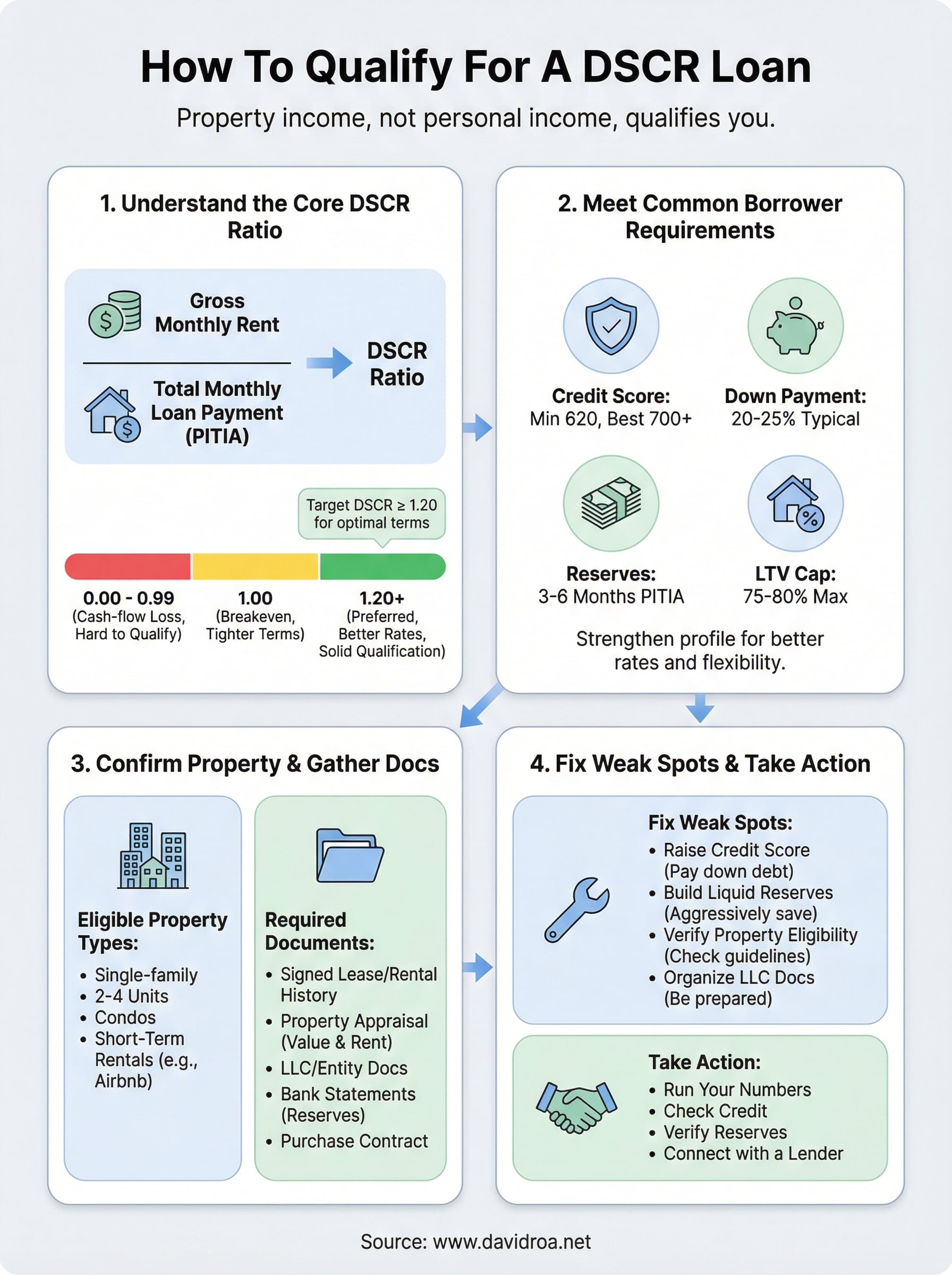

The ratio itself is straightforward: gross monthly rent divided by the total monthly loan payment (principal, interest, taxes, insurance, and any HOA dues). A DSCR of 1.0 means the rent exactly covers the payment. Most lenders want to see a DSCR of at least 1.20, meaning the property produces 20% more income than it costs to carry each month. Some programs allow ratios as low as 0.75 for borrowers with strong credit and larger down payments, but you'll face tighter terms and higher rates at that level.

A DSCR below 1.0 signals the property runs at a cash-flow loss on paper, and most lenders will either decline the file outright or require significant compensating factors like a larger down payment or strong reserves.

What lenders actually review in your file

Knowing how to qualify for a DSCR loan requires understanding the full checklist lenders work through, not just the ratio. Here's what they evaluate on every file:

| Factor | Typical Requirement |

|---|---|

| Credit score | 620 minimum; best rates start at 700+ |

| Down payment | 20-25% of the purchase price |

| Loan-to-value (LTV) | Usually capped at 75-80% |

| Reserves | 3-6 months of mortgage payments in liquid assets |

| Property type | Single-family, 2-4 units, condos, short-term rentals each follow specific guidelines |

Each factor carries weight, and a weakness in one area can sometimes be offset by strength in another, but only up to a point.

Step 1. Calculate DSCR from rent and loan payment

Before you move into credit scores or down payments, run this number first. Understanding how to qualify for a DSCR loan starts here, because your ratio determines whether the lender approves the file and on what terms. The formula itself is straightforward: divide the gross monthly rent by the total monthly loan payment, which includes principal, interest, taxes, insurance, and any HOA dues (commonly written as PITIA).

Run the numbers on a real example

Most lenders require a DSCR of at least 1.20 to approve a file at standard terms, meaning the property produces 20% more rent than it costs to carry each month. Here's how that calculation looks with actual figures:

| Component | Amount |

|---|---|

| Gross monthly rent | $2,500 |

| Principal + interest | $1,600 |

| Taxes | $250 |

| Insurance | $100 |

| HOA | $50 |

| Total PITIA | $2,000 |

| DSCR | 1.25 |

Dividing $2,500 by $2,000 gives you a DSCR of 1.25, which clears the standard threshold and puts you in solid qualifying territory.

If your DSCR falls below 1.0, the property loses money on paper each month, and most lenders will decline the file or require a significantly larger down payment to offset the risk.

Step 2. Hit the common borrower requirements

Once your DSCR clears the lender's threshold, they shift focus to your borrower profile. Understanding how to qualify for a DSCR loan means knowing which personal requirements you need to meet before the deal moves forward.

Credit score and loan-to-value limits

Your credit score is the first filter lenders apply. Most programs require a minimum of 620, but you'll access the best rates and terms at 700 or above. Lenders also cap how much they'll lend relative to the property's value, typically setting a maximum LTV of 75-80%.

| Credit Score Range | Typical Impact |

|---|---|

| 700+ | Best rates and LTV flexibility |

| 660-699 | Standard terms, slightly higher rate |

| 620-659 | Higher rate, tighter LTV requirements |

Down payment and reserves

Most DSCR lenders require 20-25% down on the purchase price. On a $300,000 rental property, that means bringing $60,000-$75,000 to closing, and that's before reserves.

Beyond the down payment, lenders want to see 3-6 months of your full PITIA payment sitting in a liquid, verifiable account after closing.

Lenders treat reserves as a safety net. If your property sits vacant for a month or two, your reserves show the lender you can still cover the mortgage without missing a payment.

Step 3. Confirm property rules and required documents

Not every property qualifies for a DSCR loan, and submitting incomplete documents can delay or kill your closing entirely. Knowing which property types lenders accept and exactly what paperwork you need ready before you apply saves you significant time and prevents last-minute surprises.

Property types lenders accept

Most DSCR lenders work with single-family rentals, 2-4 unit properties, condos, and short-term rentals like Airbnb listings. Mixed-use and small multifamily properties may qualify depending on the specific lender and program. Rural properties or unique structures like geodesic domes often fall outside standard program guidelines entirely.

Short-term rental income is typically verified using a platform history report or a third-party market rent analysis rather than a standard lease agreement.

Documents you need to submit

Understanding how to qualify for a DSCR loan also means arriving at the application with your paperwork organized. Lenders move faster when your file is complete on the first submission, so gather these documents before you apply:

- Signed lease agreement or short-term rental income history (12 months minimum)

- Property appraisal confirming both market value and market rent

- Entity documents if you're purchasing under an LLC

- Bank statements showing post-closing reserves (2-3 months)

- Purchase contract or a completed property information sheet

Step 4. Fix weak spots and avoid common deal killers

Most declined DSCR files share the same handful of fixable problems. Knowing how to qualify for a DSCR loan also means knowing how to strengthen your file before you apply so you don't lose time restarting a deal from scratch once you're already under contract.

Address weak spots before you apply rather than trying to negotiate around them once you're already under contract and on the clock.

Raise your credit score and build reserves

Your credit score and reserves are where small improvements produce the biggest impact on your rate and approval odds. If your score sits below 680, pay down revolving balances below 30% utilization and dispute any errors before you apply. Move reserve funds into a single verifiable account at least 60 days before closing so lenders can document the balance cleanly without sourcing questions slowing down your file.

Deal killers to catch early

These are the most common deal killers that stall or sink DSCR files at the last minute. Catching them early in your process gives you time to correct course before the lender does it for you:

- Low DSCR: Negotiate a lower purchase price or raise rent before closing

- Thin reserves: Delay 60-90 days and save aggressively into one account

- Property outside program guidelines: Confirm eligibility with your lender before making an offer

- Missing LLC documents: Have your entity paperwork organized and ready on day one

Wrap it up and take the next step

Now you know exactly how to qualify for a DSCR loan: run your ratio first, meet the credit and reserve requirements, confirm your property fits the program, and fix any weak spots before you submit your file. Each step builds on the last, and handling them in order prevents the most common delays investors run into.

Your next move is straightforward. Pull your property numbers, check your credit score, and verify your reserves are sitting in a clean, verifiable account. If everything lines up, you're ready to move forward. If you find a gap, you now know exactly what to fix and how to fix it.

When you're ready to get a real quote or talk through your specific scenario, connect with David Roa directly. With over $150 million funded and 25+ years working with investors, we'll tell you exactly where your file stands and how to close the deal.