Investment Property Mortgage Rates Today: 2026 Averages

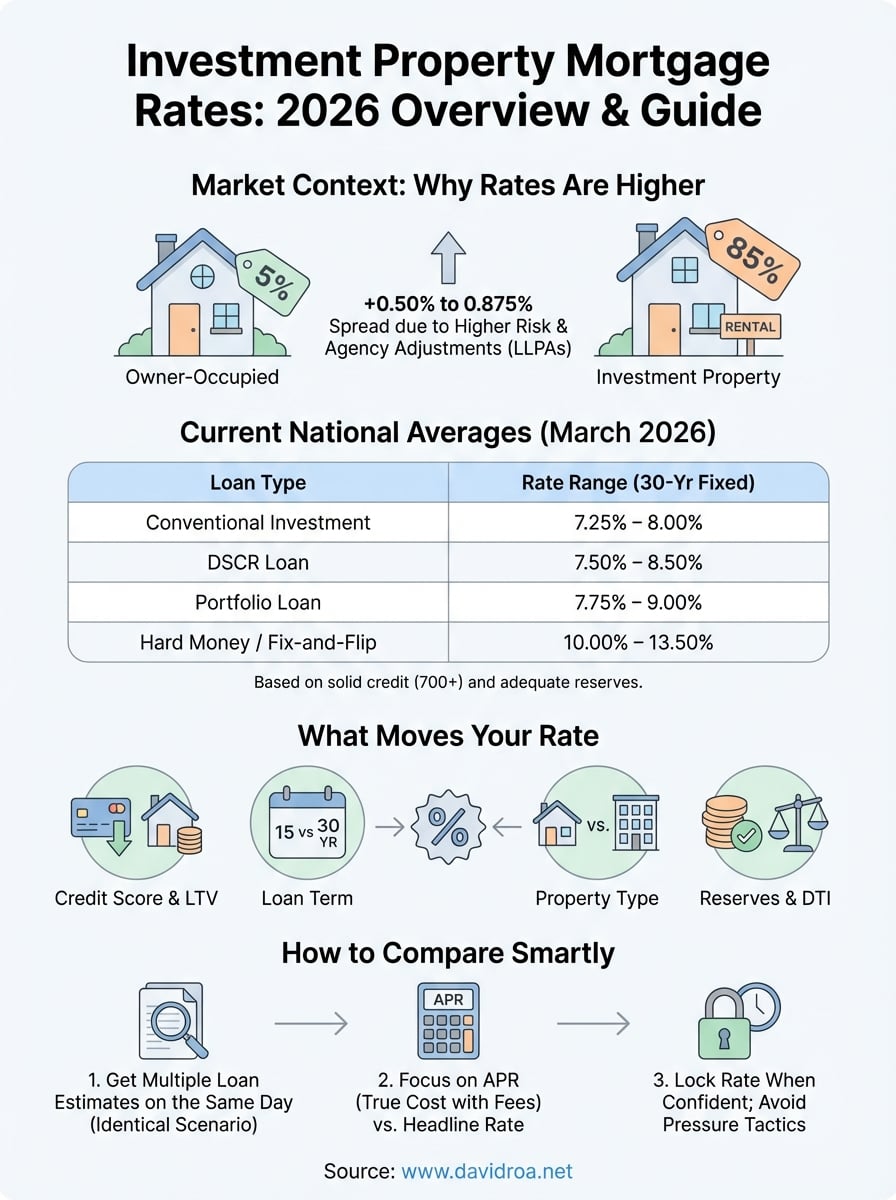

If you're checking investment property mortgage rates today, you already know that even a fraction of a percentage point changes your cash flow projections. As of early 2026, rates on investment properties continue to sit higher than primary residence loans, typically 0.50% to 0.875% above conventional owner-occupied rates, and the spread varies depending on your loan type, credit profile, and down payment.

This article breaks down current national averages for investment property mortgages, compares rate structures across popular loan programs like conventional, DSCR, and hard money, and gives you the context you need to evaluate what lenders are actually offering right now. No recycled data, just a clear picture of where rates stand in March 2026 and what's driving them.

At David Roa, we fund investment property loans daily, DSCR, fix-and-flip, rental portfolio financing, mixed-use deals, and more. With over $150 million funded and 25+ years in lending, our team works with investors at every level, from first-time landlords to operators scaling across multiple markets. That hands-on experience as both a lender and an active real estate investor means the rate guidance here comes from someone who sits on both sides of the closing table.

Investment property mortgage rates today in 2026

As of March 2026, investment property mortgage rates today are ranging from roughly 7.25% to 8.50% on conventional 30-year fixed loans, depending on your credit score, loan-to-value ratio, and the lender you approach. The Federal Reserve held its benchmark rate steady through the first quarter of 2026 after a cautious easing cycle in late 2025, which means mortgage rates have stabilized but have not dropped back to the lows many investors were hoping for. If you've been waiting on the sidelines expecting a dramatic rate cut, the current data suggests you'll get more traction by optimizing your loan structure than by timing the market.

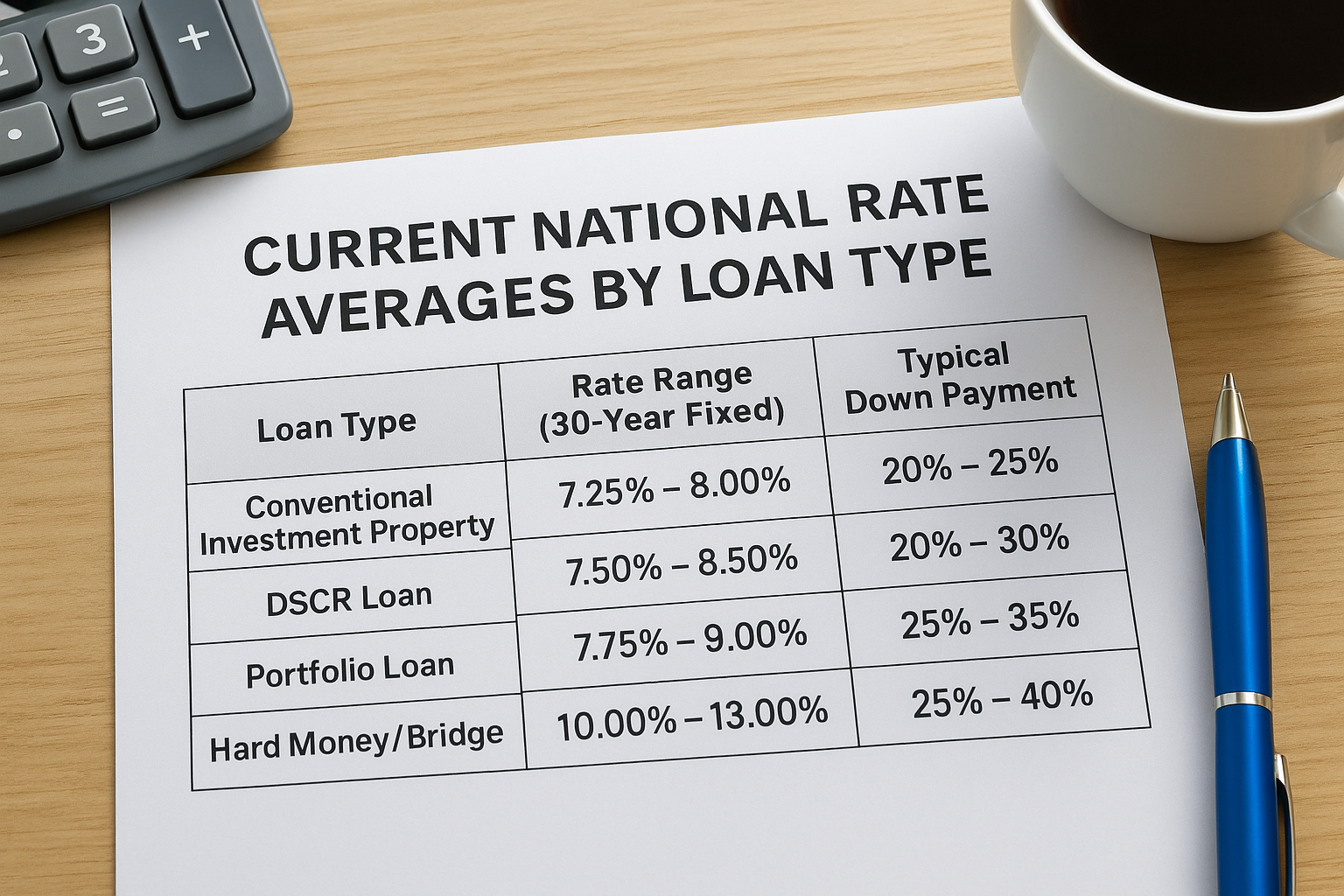

Current national rate averages by loan type

Different loan products carry different rate structures, and understanding where each one sits right now helps you compare quotes accurately. The table below reflects national averages for early March 2026 across the most common investor loan types.

| Loan Type | Rate Range (30-Year Fixed) | Typical Down Payment |

|---|---|---|

| Conventional Investment Property | 7.25% – 8.00% | 20% – 25% |

| DSCR Loan | 7.50% – 8.50% | 20% – 30% |

| Portfolio Loan | 7.75% – 9.00% | 25% – 35% |

| Hard Money / Bridge | 10.00% – 13.00% | 25% – 40% |

| Fix-and-Flip | 10.50% – 13.50% | Varies |

These ranges represent what borrowers with solid credit profiles (700+) and adequate reserves are seeing across the country. Your actual quote will sit higher or lower depending on factors covered in a later section of this article.

Even a 0.25% difference in rate on a $400,000 investment property loan translates to roughly $70 more per month, or over $25,000 across a 30-year term.

What the rate environment means for investors right now

The current lending environment rewards preparation over patience. Lenders are actively competing for qualified borrowers, but they're also pricing risk more carefully than they did during the low-rate years. Debt service coverage ratio (DSCR) loans have grown in popularity because they qualify based on the property's rental income rather than your personal income, and rates on these products have become more competitive as more lenders entered the space through 2024 and 2025.

For investors focused on long-term rental holds, locking a 30-year fixed conventional loan at or below 7.75% with 25% down remains a viable strategy in most markets where rent-to-price ratios support positive cash flow. Short-term investors running fix-and-flip projects are naturally accepting higher short-term rates, since the hold period is measured in months rather than years.

How your loan size and property type affect current quotes

Loan size matters more than most borrowers realize. Conforming loan limits for investment properties in 2026 top out at $806,500 for single-unit properties in most markets, and loans above that threshold fall into jumbo territory with their own rate adjustments. Multi-unit properties, two to four units, also carry additional pricing hits compared to single-family rentals at the same loan amount.

Property type plays a direct role too. A single-family rental typically gets the best conventional pricing, while a duplex, triplex, or fourplex may trigger a 0.25% to 0.50% rate add-on depending on the lender's guidelines. Commercial properties and mixed-use deals step outside conventional altogether and land in portfolio or DSCR territory by default.

Why investment property rates run higher than primary home rates

When you look at investment property mortgage rates today and compare them to a primary residence quote, the gap is not arbitrary. Lenders charge more for investment properties because the statistical default risk is measurably higher. When a borrower faces financial hardship, they prioritize keeping a roof over their own head before protecting a rental or flip property. That behavioral pattern is reflected directly in the rate you receive.

Lenders price the loan based on what happens when things go wrong, not when things go right.

How lenders measure default risk on investment loans

The risk calculation starts with occupancy type. Fannie Mae and Freddie Mac, which set the pricing rules for most conventional loans, assign loan-level price adjustments (LLPAs) based on property use. An investment property carries a higher LLPA than an identical loan on an owner-occupied home at the same credit score and LTV. These adjustments translate directly into your rate or your closing costs, depending on how your lender structures the quote.

Lenders also look at cash reserves more carefully on investment deals. A primary home borrower might need two months of mortgage payments in reserve. On an investment property, most conventional lenders want to see six to twelve months of reserves, and the reasoning is straightforward. If the property sits vacant for a quarter, the lender wants evidence that you can still make payments without the rental income.

Why secondary market rules drive the pricing difference

Most conventional mortgages get sold into the secondary market through Fannie Mae or Freddie Mac after closing. Those agencies set detailed pricing grids, and investment properties land in a higher-cost tier because their historical loss data supports it. Your lender is not simply adding margin; they are passing along agency-mandated adjustments that apply regardless of which bank or broker you work with.

This is also why shopping multiple lenders can still produce different quotes on the same investment property. Lenders vary in how they absorb or pass through LLPAs, and some portfolio lenders operate entirely outside agency guidelines. Understanding this structure helps you ask the right questions when you compare rate sheets side by side.

What moves your investment property rate and APR

Several variables stack on top of each other to produce the final rate you see on a loan estimate. Understanding which levers you actually control helps you walk into a rate conversation with realistic expectations and a clear strategy for improving your position before you apply.

Credit score and loan-to-value ratio

Your credit score carries the most individual weight in the pricing formula. On a conventional investment property loan, the difference between a 680 and a 740 score can move your rate by 0.375% to 0.75%, and that gap compounds with your loan-to-value ratio. Lenders use both factors together, not in isolation, so a lower score at a higher LTV produces the largest pricing hit. Bringing your LTV down to 25% or 30% by increasing your down payment can partially offset a weaker credit profile, but it rarely eliminates the spread entirely.

The single most cost-effective move before applying is pulling your credit report 90 days in advance and resolving any errors or outstanding collections that are suppressing your score.

Loan term length and property type

Shorter loan terms typically come with lower rates. A 15-year fixed investment property loan will price noticeably better than a 30-year fixed, though the monthly payment is significantly higher. If your cash flow projections support it, a 20-year term offers a middle ground that many investors overlook when comparing investment property mortgage rates today across different structures.

Property type also feeds directly into your rate. A single-family rental prices the most favorably under conventional guidelines, while a two-to-four-unit property triggers additional adjustments. Non-warrantable condos and mixed-use buildings fall outside conventional pricing entirely and typically land in portfolio loan territory with higher rates by default.

How reserves and debt-to-income ratio factor in

Lenders treat your liquid reserves as a buffer against vacancy and unexpected expenses. More reserves documented at closing can sometimes shift your rate slightly, but their bigger function is keeping your file approvable at the rate tier you qualify for. Your debt-to-income ratio matters on income-documented loans. A lower DTI signals capacity, and some lenders will price a well-structured file more aggressively when your overall debt load is clearly manageable relative to your documented income.

Loan types that investors use and how rates compare

Not every investor uses the same loan product, and the type of financing you choose shapes your rate as much as your credit score does. Understanding how each loan category prices in the current market gives you a sharper lens for evaluating what you see when you pull investment property mortgage rates today across different lenders.

Conventional loans and DSCR loans

Conventional investment property loans follow Fannie Mae and Freddie Mac guidelines, which means they offer the most competitive rates for borrowers who can document personal income through tax returns and W-2s. If your debt-to-income ratio is clean and your credit score sits above 720, a conventional loan will typically give you the lowest rate available on a rental property purchase. The tradeoff is that qualification requires full income documentation, which disqualifies a significant number of real estate investors who run income through LLCs or hold multiple properties.

DSCR loans solve that problem by qualifying the loan based on the property's rental income rather than your personal tax returns. If the monthly rent covers the mortgage payment, you have a viable path to approval. Rates on DSCR products currently run 0.25% to 0.75% above comparable conventional rates, but for investors with complex income structures or large existing portfolios, that premium is often worth it.

DSCR loans have expanded the pool of qualified investors more than any other product introduced in the past decade, and lenders continue to compete aggressively on pricing in this space.

Hard money, bridge, and fix-and-flip financing

Hard money and fix-and-flip loans operate on entirely different logic. These products are asset-based, short-term, and priced for speed rather than efficiency. Rates in the 10% to 13.5% range reflect the elevated risk and compressed timeline these loans carry, not poor underwriting on your part. If you're renovating a property over six to nine months and exiting through a sale or a long-term refinance, the higher rate is a project cost you factor into your spread, not a long-term carrying burden. Bridge loans serve a similar function for investors transitioning between properties or waiting on a longer-term loan to close.

How to compare quotes and lock a good rate

Comparing investment property mortgage rates today across lenders requires more discipline than most borrowers apply. Lenders quote rates differently, roll fees in or out of the APR, and adjust points based on how they want the deal to look on paper. Without a consistent framework for comparing offers, you're choosing between apples and oranges while thinking you're comparing apples to apples.

Pull multiple loan estimates on the same day

Rate quotes are time-sensitive because they reflect the market at the moment the lender pulls them. If you collect three quotes over two weeks, you're comparing different market conditions as much as different lender pricing. Request loan estimates from at least three lenders on the same day, ideally within a 24-hour window, so you're working with data that reflects identical market conditions.

When you request each quote, give every lender the same exact loan scenario: the same purchase price, down payment, property type, loan term, and credit tier. If you let each lender interpret the scenario differently, the quotes become incomparable before you've even read them.

A loan estimate issued on the same day from three different lenders is the only apples-to-apples comparison available to you.

Understand the difference between rate and APR

The interest rate tells you what your monthly payment will be. The annual percentage rate (APR) tells you what the loan actually costs once you factor in origination fees, discount points, and lender charges. A lender quoting 7.50% with two discount points may look cheaper than a lender quoting 7.75% with no points, but the APR calculation will show you whether buying that rate down pencils out given your expected hold period.

Focus on APR when you plan to hold the loan for a long time, and focus on rate when your hold period is short or uncertain. Paying points to reduce your rate only makes financial sense if you keep the loan long enough to recoup the upfront cost through the monthly savings.

How to decide when to lock

Once you have a competitive quote in hand, locking quickly protects you from rate movement during the underwriting period. Most lenders offer 30-day, 45-day, and 60-day rate locks, with longer locks costing slightly more. If your closing timeline is clear, match the lock period to your actual close date without overbuilding in extra cushion you'll pay for but not need.

Red flags and common mistakes when shopping rates

Shopping investment property mortgage rates today looks straightforward until you realize how many ways the process can work against you. Borrowers who move too fast, accept the first quote they receive, or misread a loan estimate end up paying significantly more than necessary. Recognizing the most common mistakes before you start saves you real money at closing and over the life of the loan.

Chasing the lowest advertised rate without reading the fine print

Lenders know that a low headline rate draws attention, and some use that number to get you in the door before revealing the true cost structure. A rate that looks attractive often comes loaded with origination fees, discount points, or prepayment penalties that change the math entirely. Before you take any quote seriously, request the full loan estimate and read line by line. If a lender is reluctant to provide a formal loan estimate before you commit, that reluctance tells you something important about how they operate.

A rate quoted verbally over the phone carries no legal weight. Only a written loan estimate gives you enforceable numbers to compare.

Skipping credit review before you apply

Applying for an investment property loan before reviewing your credit report is one of the most expensive mistakes an investor can make. Errors on your report, outdated collections, or a thin credit file can push your rate into a higher pricing tier that costs tens of thousands of dollars over a 30-year term. Pull your report from AnnualCreditReport.com at least 60 to 90 days before applying so you have time to dispute inaccuracies and resolve anything that is actively suppressing your credit score.

Letting a lender rush you through the lock decision

Some lenders push borrowers to lock a rate quickly by overstating market volatility or suggesting the window is about to close. That pressure tactic benefits the lender, not you. A legitimate lender will give you enough time to compare loan estimates and make an informed decision about when to lock. If you feel rushed into committing before your questions are answered or before you have competing quotes in hand, treat that as a clear signal to slow down and look elsewhere.

Next steps

You now have a complete picture of investment property mortgage rates today, including where national averages sit, why the pricing gap versus primary residence loans exists, and what you can do to improve your rate before you apply. The most practical move right now is to pull your credit report, organize your reserve documentation, and request loan estimates from multiple lenders on the same day using an identical loan scenario so your comparisons are actually valid.

Working with a lender who understands investor-specific loan structures, from DSCR and conventional rental financing to fix-and-flip and hard money, means you spend less time educating your lender and more time closing deals. David Roa's team has funded over $150 million in loans across exactly these product types, backed by 25 years of direct experience on both sides of the closing table. Connect with David Roa today and get a rate comparison built around your actual investment scenario.