12 Best Jumbo Loan Refinance Rates And Lenders (2026)

If you're sitting on a jumbo mortgage and watching rates shift, you're probably wondering whether now is the right time to refinance, and who's actually offering competitive terms. Finding the best jumbo loan refinance rates takes more than a quick Google search because these loans fall outside conforming limits, and lenders price them differently based on their own risk appetite and portfolio strategy. That means rate differences between lenders can be significant, sometimes by half a percent or more.

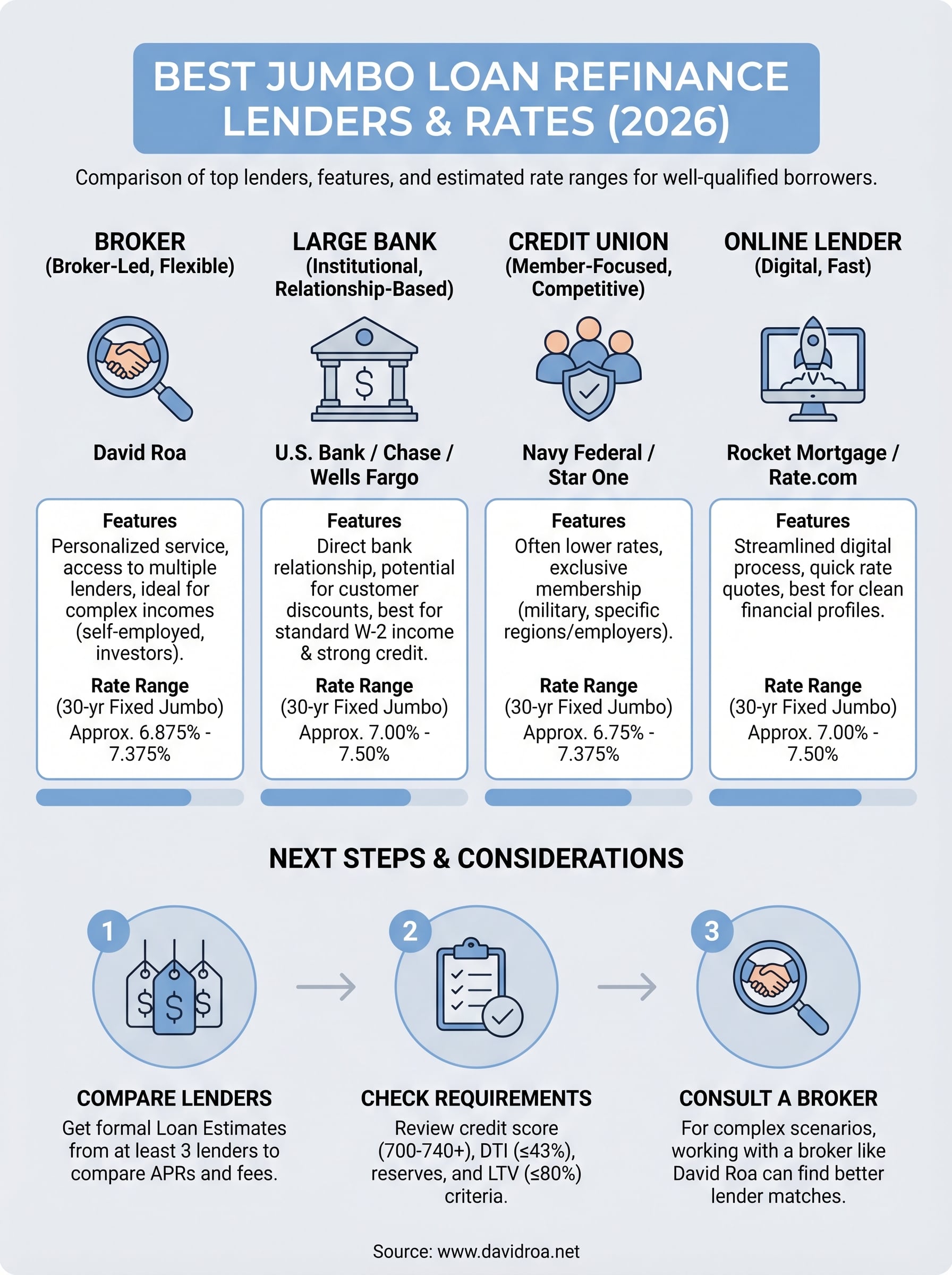

At David Roa, we've helped borrowers navigate high-balance financing for over 25 years, funding more than $150 million in loans across residential, commercial, and investment deals. Jumbo refinances are one of the areas where our experience matters most, these aren't cookie-cutter transactions, and the right lender match can save you tens of thousands over the life of your loan. We know which lenders perform and which ones don't because we work with them daily.

This guide breaks down 12 of the best jumbo refinance lenders available in 2026, with a close look at their current rates, standout features, and who they're best suited for. Whether you're refinancing a primary residence, a second home, or an investment property, you'll find concrete options to compare side by side, so you can make a decision based on real numbers, not guesswork.

1. David Roa jumbo refinance options

Working with a broker who actively lends and invests gives you a fundamentally different experience than walking into a bank branch. David Roa brings over 25 years of mortgage experience and more than $150 million funded to every jumbo refinance conversation, which means you get real-world insight into what lenders are currently accepting, not just what the published guidelines say.

Rate snapshot and APR notes

Jumbo loan refinance rates through David Roa depend on your loan amount, credit profile, property type, and the lender matched to your scenario. As of April 2026, here's a general snapshot of where rates are landing for well-qualified borrowers:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 6.875% to 7.375% |

| 15-year fixed jumbo | 6.375% to 6.875% |

| 7/1 ARM jumbo | 6.25% to 6.75% |

ARM products like the 7/1 can work well if you plan to sell or refinance again within the fixed window. Keep in mind that the APR will always run higher than your note rate because it spreads origination fees, discount points, and other costs across the full loan term.

Comparing APRs across lenders, rather than just interest rates, gives you a more accurate picture of your total borrowing cost on a jumbo refinance.

Who this fits best

David Roa is a strong fit if your loan amount exceeds the 2025 conforming limit of $806,500 and your situation has any complexity to it. That includes self-employed borrowers, real estate investors using DSCR documentation, non-U.S. citizens with ITIN numbers, and high-net-worth borrowers with non-traditional income structures.

Borrowers in the Chicago metro area also benefit from the local market knowledge David brings to every deal, particularly for investment properties and fix-and-flip scenarios that most retail lenders won't touch.

Typical jumbo refinance requirements

Most jumbo lenders want to see a strong financial profile before approving a refinance. You'll generally need a credit score of at least 700, though some portfolio lenders allow scores down to 680 with compensating factors such as significant reserves.

- DTI ratio: 43% or below is standard

- Cash reserves: 12 months after closing, minimum

- LTV: At or below 80% to avoid pricing adjustments

- Appraisal: Full interior appraisal required on most jumbo refinances

Fees, points, and closing costs to expect

Closing costs on a jumbo refinance typically run between 2% and 4% of the loan amount. That covers origination fees, title insurance, appraisal, and prepaid items. Because David works with a network of lenders, fee structures vary by product, and you can often choose between buying down your rate with discount points or accepting a slightly higher rate in exchange for reduced upfront costs.

How to get a quote with David Roa

Getting a quote starts with a direct conversation at davidroa.net, where you can submit your basic loan details and receive a rate comparison across multiple lenders at once. You'll walk away with concrete rate and fee scenarios you can actually compare side by side, not a vague ballpark number that disappears when you apply.

2. Bankrate jumbo refinance rates

Bankrate aggregates rate data from lenders nationwide and publishes daily rate tables for jumbo mortgage products, including refinances. It's one of the most common starting points for borrowers who want to gauge where national jumbo loan refinance rates are sitting before reaching out to individual lenders.

Rate snapshot and APR notes

As of April 2026, Bankrate's published jumbo refinance averages are running in these ranges for well-qualified borrowers:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 5/1 ARM jumbo | 6.50% to 7.00% |

These are advertised rates from lenders who participate on the platform, not guaranteed quotes. Your actual rate will vary based on your credit score, loan-to-value ratio, and the individual lender's current pricing model.

Always compare APRs alongside interest rates when reviewing Bankrate's tables, since two lenders can post the same rate while charging very different fees.

Who this fits best

Bankrate works best if you're in early research mode and want a broad read on the market before committing to any lender. It's most relevant for borrowers with standard financial documentation who are refinancing a straightforward primary residence.

Complex scenarios, such as self-employment income, ITIN documentation, or investment property refinances, fall outside what Bankrate's rate tables can meaningfully address for you.

What Bankrate includes in its averages

The platform pulls rates from lenders who pay to be listed, so the data reflects a curated sample rather than the full market. Most rate assumptions on Bankrate require a credit score of 740 or higher and clean, traditionally documented income.

Fees, points, and closing costs to expect

Bankrate displays APR alongside the interest rate on most listings, which helps you spot lenders loading costs into discount points. The actual closing cost breakdown depends entirely on the lender you select and will only appear in a formal Loan Estimate after you apply.

How to use Bankrate to shop lenders

Use Bankrate's rate tables as a market benchmark, not a final answer. Once you identify a realistic rate range, bring that data to specific lenders and request formal Loan Estimates you can compare directly, including fees, points, and total cost over your expected hold period.

3. U.S. Bank jumbo refinance

U.S. Bank is one of the larger national lenders that actively prices jumbo loan refinance rates through both its branch network and online application system. For borrowers with strong credit and standard documentation, it offers a direct path to refinancing a high-balance loan without needing to go through a broker.

Rate snapshot and APR notes

As of April 2026, U.S. Bank's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

The APR will exceed the note rate on every product because it spreads origination charges and prepaid costs across the full loan term. Rate assumptions typically require a credit score of 740 or higher.

Check U.S. Bank's online rate tool for current figures, since posted rates update daily based on market movement.

Who this fits best

U.S. Bank suits W-2 borrowers with clean income documentation who prefer the security of a large institutional lender. It's a reliable option for refinancing a primary residence or second home when your financial profile fits standard underwriting guidelines without exceptions.

Self-employed borrowers or investors with non-traditional income structures will likely find U.S. Bank's guidelines too rigid and should compare alternative lenders before applying.

Typical jumbo refinance requirements

U.S. Bank generally requires a minimum credit score of 720, a DTI at or below 43%, and at least 12 months of cash reserves after closing. Your LTV must stay at or below 80% to avoid additional pricing adjustments on most jumbo products.

Fees, points, and closing costs to expect

Closing costs at U.S. Bank typically run between 2% and 3% of the loan amount. Paying discount points to reduce your rate makes financial sense only if you plan to hold the loan for seven or more years.

How to get a quote with U.S. Bank

You can start a rate inquiry on the U.S. Bank website by entering your loan amount, property type, and credit range. A formal application triggers a Loan Estimate within three business days, which gives you the full cost breakdown needed for a real comparison.

4. Navy Federal Credit Union jumbo refinance

Navy Federal Credit Union offers jumbo mortgage refinancing exclusively to its members, which includes active duty military, veterans, Department of Defense employees, and their immediate family members. If you qualify for membership, Navy Federal is worth a close look because it consistently prices jumbo loan refinance rates competitively against larger retail banks.

Rate snapshot and APR notes

As of April 2026, Navy Federal's jumbo refinance rates for well-qualified members are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 6.875% to 7.375% |

| 15-year fixed jumbo | 6.375% to 6.875% |

Your APR will run above the stated interest rate because it folds in origination charges and prepaid costs across the full loan term. Navy Federal members with strong credit and significant reserves tend to see the most favorable pricing.

Always request a formal Loan Estimate from Navy Federal to compare total costs, not just the advertised rate.

Who this fits best

Navy Federal is the right call if you're a military borrower or qualifying family member refinancing a primary residence or second home. Its underwriting tends to be more flexible than big commercial banks for members with non-standard service income situations.

Typical jumbo refinance requirements

Navy Federal generally expects a minimum credit score around 700, a DTI at or below 43%, and solid post-closing reserves. Your LTV should stay at or below 80% to avoid rate adjustments on most jumbo products.

Fees, points, and closing costs to expect

Closing costs typically fall between 2% and 3% of the loan amount. Navy Federal sometimes runs promotions that reduce origination fees for qualifying members, so ask directly when you request a quote.

How to get a quote with Navy Federal

You can start your refinance inquiry through Navy Federal's online member portal or by calling their mortgage team directly. Membership verification is the first step before any rate discussion begins.

5. PNC Bank jumbo mortgage refinance

PNC Bank operates across roughly 50 markets nationwide and offers jumbo mortgage refinancing as part of a broader suite of home lending products. For borrowers looking to compare jumbo loan refinance rates from a large regional bank with a full-service branch presence, PNC is a solid option worth including in your search.

Rate snapshot and APR notes

PNC's jumbo refinance rates for well-qualified borrowers are running in these general ranges as of April 2026:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will exceed the stated note rate because it factors in origination charges and prepaid costs spread across the loan term.

Request a formal Loan Estimate from PNC to see the full fee breakdown before comparing it against other lenders.

Who this fits best

PNC works well for borrowers with W-2 income and traditional documentation who want a direct relationship with a bank that handles the loan in-house. It suits refinances on primary residences and second homes where the financial profile is straightforward.

Typical jumbo refinance requirements

PNC generally requires a minimum credit score of 720 for jumbo refinances, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid pricing adjustments on most products.

Fees, points, and closing costs to expect

Closing costs at PNC typically fall between 2% and 3% of the loan amount, covering origination, title, and prepaid items. Discount points are available if you want to buy down your rate, but run the break-even math first to confirm it makes financial sense for your hold period.

How to get a quote with PNC

You can start a refinance inquiry directly on PNC's website by entering your loan details and property information. A formal application triggers a Loan Estimate within three business days, giving you the real numbers needed for an accurate comparison.

6. Chase jumbo refinance

Chase is one of the largest mortgage lenders in the country and offers jumbo loan refinancing as a core product through both its branch network and digital application platform. For borrowers who value working with a nationally recognized institution and want access to relationship banking perks, Chase is a competitive option when you're shopping jumbo loan refinance rates.

Rate snapshot and APR notes

Chase's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges as of April 2026:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will run above the stated note rate because it incorporates origination charges and prepaid costs spread across the full loan term.

Existing Chase Private Client customers sometimes receive rate discounts, so ask your banker directly whether any relationship pricing applies before you apply.

Who this fits best

Chase suits borrowers with W-2 income and clean documentation who already hold a significant banking relationship with the institution. It works well for refinancing a primary residence or second home where your financial profile fits standard jumbo underwriting guidelines without exceptions. Self-employed borrowers with complex income structures will likely find Chase's guidelines less flexible than portfolio lenders or broker options.

Typical jumbo refinance requirements

Chase generally expects a minimum credit score of 720 for jumbo refinance approvals, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid pricing adjustments on most products.

Fees, points, and closing costs to expect

Closing costs at Chase typically run between 2% and 3% of the loan amount, covering origination, title, appraisal, and prepaid items. Discount points are available if you want to reduce your note rate, but calculate your break-even timeline first.

How to get a quote with Chase

You can start a refinance inquiry on Chase's website by entering your property details and loan amount. A formal application generates a Loan Estimate within three business days, giving you the full cost breakdown needed for an accurate comparison against other lenders.

7. Rate.com jumbo mortgage rates

Rate.com, formerly known as Guaranteed Rate, operates as one of the larger independent mortgage lenders in the country and prices jumbo loan refinance rates competitively through its online application platform. It combines a digital-first application experience with access to human loan officers, making it a reasonable option for borrowers who want speed without losing direct support.

Rate snapshot and APR notes

As of April 2026, Rate.com's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will run above the stated note rate because it incorporates origination charges and prepaid costs distributed across the full loan term. Rate assumptions on Rate.com's platform typically require a credit score of 740 or higher to hit the advertised figures.

Confirm whether any advertised rate includes discount points before you use it as a benchmark against other lenders.

Who this fits best

Rate.com works best for borrowers with traditional W-2 income who want a streamlined digital process and are refinancing a primary residence or second home. Its underwriting guidelines follow standard jumbo criteria, so borrowers with complex income documentation or non-traditional financial profiles will likely find better flexibility elsewhere.

Typical jumbo refinance requirements

Rate.com generally expects a minimum credit score of 720, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid additional pricing adjustments on most jumbo products.

Fees, points, and closing costs to expect

Closing costs at Rate.com typically run between 2% and 3% of the loan amount, covering origination, title, and prepaid items. Discount points are available, but calculate your break-even timeline before committing.

How to get a quote with Rate.com

You can start a refinance inquiry directly on Rate.com's website by entering your loan amount and property details. A formal application generates a Loan Estimate within three business days, giving you the real numbers needed for a side-by-side comparison.

8. Rocket Mortgage jumbo refinance

Rocket Mortgage is one of the most recognized online lenders in the country and offers jumbo loan refinancing through a fully digital application process. If you're comparing jumbo loan refinance rates across multiple platforms, Rocket gives you a fast way to get a rate quote without scheduling a branch visit or waiting for a callback.

Rate snapshot and APR notes

As of April 2026, Rocket Mortgage's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will run above the stated note rate because it spreads origination charges and prepaid costs across the full loan term. Rate assumptions on Rocket's platform typically require a credit score of 740 or higher to match advertised figures.

Confirm whether any rate you see from Rocket includes discount points before using it as a comparison benchmark against other lenders.

Who this fits best

Rocket Mortgage works well for W-2 borrowers with standard documentation who want a fast, tech-driven experience and are refinancing a primary residence. Its process favors borrowers with clean financial profiles and limited complexity in their income structure.

Typical jumbo refinance requirements

For a jumbo refinance, Rocket generally expects a minimum credit score of 720, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid pricing adjustments on most jumbo products.

Fees, points, and closing costs to expect

Closing costs at Rocket typically run between 2% and 3% of the loan amount, covering origination, title, and prepaid items. Discount points are available, but run your break-even calculation before committing to buying down the rate.

How to get a quote with Rocket Mortgage

You can start a refinance inquiry on Rocket's website by creating an account and entering your property and loan details. A formal application generates a Loan Estimate within three business days, giving you the full cost breakdown for a real comparison.

9. Mortgage News Daily jumbo rate index

Mortgage News Daily publishes a daily rate index that tracks average mortgage rates across a wide range of loan products, including jumbo mortgages. It's one of the most frequently cited sources for understanding real-time rate movement, and many loan officers and borrowers use it as a daily benchmark when timing a refinance.

Rate snapshot and APR notes

As of April 2026, the Mortgage News Daily jumbo rate index is showing 30-year fixed jumbo rates in the 7.00% to 7.50% range for well-qualified borrowers. The index updates each business day, so the figures can shift meaningfully within a single week depending on economic data releases and Federal Reserve commentary.

The index reflects average rates based on lender surveys, not guaranteed quotes, so treat it as a directional signal rather than a number you can lock.

Who this fits best

Mortgage News Daily's index is most useful for borrowers who are actively tracking rate trends over days or weeks to identify a favorable window to lock. It gives you context for whether rates are moving up, down, or holding steady, which helps you decide when to act rather than just who to call.

What the index measures and what it misses

The index aggregates data from a network of mortgage professionals who report daily rate observations, giving it a real-market feel compared to some other benchmark sources. What it misses is personalization. It cannot account for your specific credit profile, loan amount, or property type, so the rate you actually receive from a lender will differ based on your individual scenario.

Fees, points, and closing costs to expect

The index does not include fee or cost data, so you won't find any APR figures or closing cost estimates here. It tracks interest rates only.

How to use the index when rate shopping

Use Mortgage News Daily as a daily market pulse while you're actively comparing jumbo loan refinance rates across lenders. When the index shows rates dropping, that's your signal to accelerate conversations with lenders and push toward a rate lock before conditions reverse.

10. Star One Credit Union jumbo mortgages

Star One Credit Union is a member-owned institution based in Silicon Valley that offers jumbo mortgage refinancing at rates that frequently undercut major retail banks. Because it operates as a credit union rather than a for-profit lender, it can pass more savings to members, which makes it worth a look if you qualify for membership.

Rate snapshot and APR notes

As of April 2026, Star One's jumbo refinance rates for well-qualified members are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 6.75% to 7.25% |

| 15-year fixed jumbo | 6.25% to 6.75% |

| 5/1 ARM jumbo | 6.125% to 6.625% |

Your APR will exceed the stated note rate because it incorporates origination charges and prepaid costs spread across the full loan term.

Star One's pricing can sit notably below national averages for jumbo loan refinance rates, but you must meet membership eligibility before you can access any of these products.

Who this fits best

Star One is built for technology industry professionals and employees of companies located in or affiliated with Santa Clara County. If you work for a qualifying employer in Silicon Valley and hold a high-balance mortgage on a primary residence or second home, this credit union gives you access to below-average jumbo pricing that most borrowers can't reach through retail banks.

Typical jumbo refinance requirements

Star One generally expects a minimum credit score of 720, a DTI at or below 43%, and solid post-closing cash reserves. Your LTV should stay at or below 80% to qualify for standard jumbo refinance pricing without adjustments.

Fees, points, and closing costs to expect

Closing costs at Star One typically run between 2% and 3% of the loan amount, covering origination, title, and prepaid items. Discount point options are available for borrowers who plan to hold the loan long-term.

How to get a quote with Star One

You can start a refinance inquiry through Star One's online portal after confirming your membership eligibility. Request a formal Loan Estimate to get the complete fee and rate breakdown before comparing it against other lenders.

11. Wells Fargo jumbo refinance

Wells Fargo is one of the largest home lenders in the country and offers jumbo loan refinancing through both its branch network and online application platform. For borrowers who already have a banking relationship with Wells Fargo, it can be a natural first stop when comparing jumbo loan refinance rates across major institutions.

Rate snapshot and APR notes

As of April 2026, Wells Fargo's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will run above the stated note rate because it folds origination charges and prepaid costs across the full loan term. Rate assumptions typically require a credit score of 740 or higher to match any advertised figure.

Existing Wells Fargo banking customers may qualify for a relationship discount on their rate, so ask your banker directly before submitting a formal application.

Who this fits best

Wells Fargo suits borrowers with clean W-2 income and standard documentation who prefer refinancing with a large bank that handles the loan in-house. It works best for a primary residence or second home with a straightforward financial profile and no complex income variables.

Typical jumbo refinance requirements

Wells Fargo generally expects a minimum credit score of 720 for jumbo refinance approvals, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid pricing adjustments.

Fees, points, and closing costs to expect

Closing costs at Wells Fargo typically run between 2% and 3% of the loan amount, covering origination, title, appraisal, and prepaid items. Discount points are available, but calculate your break-even timeline before buying down the rate.

How to get a quote with Wells Fargo

You can start a refinance inquiry on Wells Fargo's website by entering your property details and loan amount. A formal application generates a Loan Estimate within three business days, giving you the full cost breakdown needed for a real comparison.

12. Guaranteed Rate jumbo refinance

Guaranteed Rate is one of the most widely recognized independent mortgage lenders in the country and has built a strong reputation for competitive pricing on jumbo loan refinance rates across its digital platform. Note that the company now operates under the brand Rate.com for most consumer-facing transactions, but its underwriting capabilities and product lineup remain the same as the legacy Guaranteed Rate platform.

Rate snapshot and APR notes

As of April 2026, Guaranteed Rate's jumbo refinance rates for well-qualified borrowers are generally landing in these ranges:

| Product | Approximate Rate Range |

|---|---|

| 30-year fixed jumbo | 7.00% to 7.50% |

| 15-year fixed jumbo | 6.50% to 7.00% |

| 7/1 ARM jumbo | 6.375% to 6.875% |

Your APR will run above the stated note rate because it distributes origination charges and prepaid costs across the full loan term. Rate assumptions typically require a credit score of 740 or higher to match any advertised figure.

Always confirm whether a quoted rate includes discount points before using it as a benchmark against competing lenders.

Who this fits best

Guaranteed Rate works best for W-2 borrowers with standard income documentation who want a digital-forward experience backed by licensed loan officers. It suits refinances on a primary residence or second home with a clean financial profile and no complex income variables.

Typical jumbo refinance requirements

You'll generally need a minimum credit score of 720, a DTI at or below 43%, and at least 12 months of verified cash reserves after closing. Your LTV should stay at or below 80% to avoid pricing adjustments on most jumbo products.

Fees, points, and closing costs to expect

Closing costs typically fall between 2% and 3% of the loan amount, covering origination, title, and prepaid items. Discount points are available if you want to reduce your long-term interest expense, but calculate your break-even timeline before committing.

How to get a quote with Guaranteed Rate

You can start a refinance inquiry directly on the Guaranteed Rate website by entering your loan amount and property details. A formal application generates a Loan Estimate within three business days, giving you the full breakdown needed for a real side-by-side comparison.

Next steps

You now have a clear picture of where jumbo loan refinance rates stand across 12 of the leading lenders in 2026. The differences between them are real, and the right match depends on your credit profile, income documentation, property type, and how much complexity your scenario carries. Most borrowers benefit from comparing at least three lenders before locking, because even a quarter-point difference on a high-balance loan can move your monthly payment by hundreds of dollars.

If your situation has any complexity to it, whether you're self-employed, investing in real estate, or working with non-traditional income, a broker with direct lender relationships will save you time and money. David Roa has spent over 25 years placing borrowers with the right lender for their specific scenario. Start your refinance by visiting davidroa.net and getting a real rate comparison across multiple lenders at once, so you can move forward with confidence.