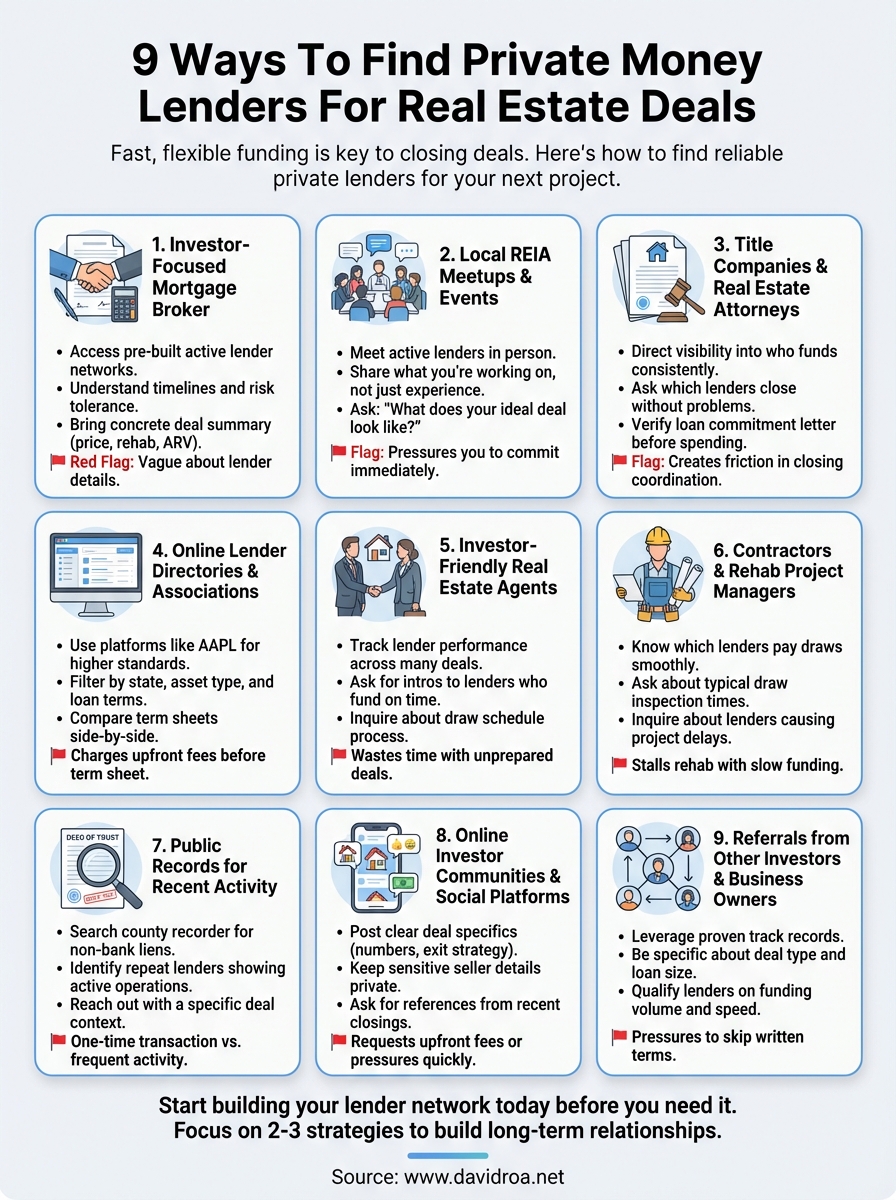

9 Ways To Find Private Money Lenders For Real Estate Deals

Most real estate deals don't fall apart because of bad numbers. They fall apart because the financing takes too long or never comes through at all. That's exactly why private money lenders for real estate have become a go-to funding source for investors who need speed, flexibility, and fewer hoops to jump through. But finding the right one? That's where most people get stuck.

With over 25 years in the lending business and more than $150 million funded, I've worked both sides of this equation, as a mortgage broker owner helping investors close deals and as an active real estate flipper myself. I know firsthand what makes a private lending relationship work and what red flags to watch for. At David Roa, we connect investors with financing solutions including hard money, DSCR loans, and fix-and-flip capital built around real deal timelines.

Below, I'm breaking down nine practical ways to find reliable private money lenders so you can fund your next real estate project with confidence. Whether you're sourcing your first deal or scaling a portfolio, these strategies work across experience levels, and I've seen each one play out in the field.

1. Work with an investor-focused mortgage broker

An investor-focused mortgage broker is one of the fastest entry points into the world of private money lenders for real estate. Unlike retail loan officers who work primarily with W-2 borrowers, these brokers maintain active lender networks built specifically around investment property financing, including fix-and-flip, bridge, and DSCR loans.

Why brokers can unlock private money faster

Brokers who specialize in investment deals have pre-built relationships with lenders who fund these loans regularly. They know which lenders close in 7 days and which ones routinely take 30, so you skip the trial-and-error process entirely. Speed and certainty are what separate deals that close from deals that fall through, and the right broker gives you both.

A broker who has personally closed investor deals understands your timeline and risk tolerance in a way a generalist lender simply won't.

How to vet a broker's lender network

Ask the broker how many private lenders they actively work with and how many investor transactions they closed in the last 12 months. A strong broker can name specific lenders and describe each one's niche. Vague or evasive answers at this stage are a clear signal to keep looking.

What to bring to the first call

Come prepared with your property address or deal summary, estimated purchase price, rehab budget, and after-repair value. If you have a track record of previous deals, bring documentation of those closings. Brokers move faster when you hand them something concrete from the start rather than a rough idea.

Questions to ask before you share a deal

Before sharing your deal details, ask the broker who they're submitting to and whether they shop your deal to multiple lenders at the same time. Also confirm whether they use a formal confidentiality process. Your deal structure is proprietary information, and you want it handled carefully, not circulated without your knowledge.

Typical costs and how brokers get paid

Most investor-focused brokers earn 1 to 2 origination points paid at closing, though some also charge a processing fee upfront. Always request a written fee disclosure before moving forward. Knowing the full cost structure early keeps the relationship straightforward and removes surprises from your closing statement.

2. Go to local REIA meetups and investor events

Real Estate Investor Association (REIA) meetups put you in the same room as active private money lenders for real estate, people who are already looking for deals to fund. These events happen in most major cities on a monthly basis and cost little to nothing to attend, which makes them one of the most accessible starting points for any investor.

Where to find legit events in your market

Search National REIA's chapter directory or look for local investor groups in your area through community forums and social platforms. Established clubs that have been running for at least two years tend to attract more serious participants, including lenders with real capital to deploy.

How to introduce yourself without sounding new

Lead with what you're working on, not your experience level. Say something like "I'm sourcing a fix-and-flip in [neighborhood] and looking to connect with lenders who fund rehab deals." That framing signals deal activity and draws the right people toward you naturally.

The goal at any event isn't to close a loan on the spot. It's to collect one or two solid contacts worth following up with.

A simple script that gets lenders talking

Ask lenders: "What does your ideal deal look like right now?" That question lets them talk about their own criteria, and their answer tells you everything about their speed, flexibility, and minimum requirements.

How to follow up and move to a term sheet

Send a brief email within 24 hours that includes your deal summary and a one-line recap of your conversation. Specificity keeps you memorable and moves the conversation forward.

Common red flags at in-person events

Avoid anyone who pressures you to commit the same night or refuses to put terms in writing before you proceed. Legitimate lenders welcome due diligence and will not rush you into a decision.

3. Ask title companies and real estate attorneys for intros

Title companies and real estate attorneys sit at the closing table for nearly every transaction in your market. That position gives them direct visibility into who is funding deals and how reliably those lenders perform when it counts.

Why these pros know who actually funds deals

These professionals see private money lenders for real estate in action on a regular basis. They know which lenders fund on time, which ones create last-minute headaches, and which ones show up consistently across multiple deal types.

A title company that closes 10 investor deals per month has better lender intelligence than most online directories ever will.

How to request referrals the right way

Call or visit in person and be direct. Tell them you are actively sourcing investment deals and ask which lenders they see close the most transactions without problems. That framing respects their time and gets you a useful answer.

What to verify about the lender's process

Ask the referred lender how they handle title reviews and closing coordination. A lender who works smoothly with title companies speeds up your timeline. One who creates friction there will slow down every deal you bring them.

How to protect yourself with the right paperwork

Always request a loan commitment letter before you spend money on inspections or appraisals. This document outlines the lender's terms in writing and gives you legal standing if anything changes before closing.

What it should cost to close a private loan

Expect to pay 2 to 4 points in origination fees plus standard closing costs. If a lender quoted through a title referral is asking for significantly more, request an itemized fee breakdown before you proceed.

4. Use private lender directories and associations

Online directories dedicated to investment lending give you a structured way to search for private money lenders for real estate without cold-calling or attending events. These platforms aggregate lender profiles across states and loan types, so you can build a shortlist before you pick up the phone.

Which directories tend to be more reliable

Industry associations like the American Association of Private Lenders (AAPL) maintain member directories with higher accountability standards than general listing sites. Members agree to a code of ethics, which filters out many of the less legitimate operators you might encounter elsewhere.

How to filter lenders by state and asset type

Use the directory's filter tools to narrow results by your target state and property type. A lender who funds residential fix-and-flips in Illinois operates very differently from one focused on commercial deals in Texas, so precise filtering saves you time upfront.

What to look for on a lender profile

Check how long the lender has been active, how many loans they list as funded, and whether they publish their standard loan terms. Profiles that lack basic details like minimum loan amounts or property types are not worth your time.

A lender with a complete, transparent profile signals professionalism before you ever speak to them.

How to compare term sheets apples to apples

Request term sheets from at least three lenders and line up the key variables side by side before deciding:

- Interest rate and whether it is fixed or variable

- Origination points and total closing costs

- Loan-to-value ratio and draw schedule structure

Red flags in online listings

Avoid lenders who charge upfront fees before issuing a term sheet or whose profiles show no verifiable transaction history. Both patterns suggest the listing is not backed by a legitimate, active lending operation.

5. Tap real estate agents who work with investors

Real estate agents who specialize in investment properties close deals alongside private money lenders for real estate on a regular basis. These agents have a direct view into which lenders actually perform when a closing is on the line.

Why investor agents know who closes on time

Investor-focused agents track lender performance across multiple deals, not just one or two. When a lender funds consistently and on time, agents keep working with them. That pattern gives you a reliable, field-tested shortlist before you make a single call.

An agent who has watched a lender fund 20 deals in your market is a better source than any directory.

How to ask for lender intros without wasting time

Be specific when you approach an agent. Tell them your deal type, target market, and loan size. That precision helps them connect you with the right lender rather than sending a generic referral you still have to vet from scratch.

What agents can tell you about draw schedules

Ask the agent how draw inspections and funding timelines worked on past deals with the lender. Rehab projects stall when draws are delayed, and agents who have experienced that firsthand will tell you exactly which lenders keep projects moving.

How to keep the agent in the loop on financing

Update the agent when you submit your loan application and when you receive a commitment letter. Keeping them informed builds trust and makes them more likely to send you stronger referrals on future deals.

Mistakes that scare off lender referrals

Agents stop making introductions when investors waste a lender's time with deals that aren't ready. Before you ask for a referral, have your deal summary, budget, and exit strategy prepared so the introduction reflects well on everyone involved.

6. Network with contractors and rehab project managers

Contractors and rehab project managers work directly inside renovation projects funded by private money lenders for real estate. That proximity gives them real insight into which lenders pay draws on time and which ones create problems that slow down the job site.

Why contractors know who funds rehab draws

Contractors see lender behavior up close on every project they touch. When a draw gets delayed, they're the ones waiting to pay their crew. Over dozens of projects, they build a mental list of which lenders run a smooth process and which ones stall for no clear reason.

A contractor who has worked on 30 funded rehabs in your market carries better lender intelligence than most published reviews ever will.

How to ask without putting them in a bad spot

Frame the request around your shared interest in a smooth project. Ask which lenders they've worked with that funded draws without friction. That question keeps the conversation practical and avoids putting them in the position of recommending someone they're not fully confident in.

What to ask about inspections and draw timing

Ask the contractor how long draw inspections typically take with lenders they've worked with before. Some lenders fund within 48 hours of an inspection, while others take two weeks. That gap directly affects your project timeline and carrying costs.

How to avoid lenders that stall your rehab

Ask contractors directly which lenders they've seen cause project delays. Slow draw funding is one of the most common ways a rehab goes over budget.

Signs a lender understands renovations

Lenders who understand rehab projects ask detailed questions about your scope of work upfront and structure draws around project milestones rather than fixed calendar dates.

7. Search public records for recent private loan activity

County recorder and assessor offices document every loan attached to a property, including those from private money lenders for real estate. This public data gives you a direct path to lenders who are already active in your target market, without relying on anyone's referral.

How to spot private lenders in county records

Search your county recorder's website for deed of trust or mortgage filings where the lender listed is an individual or a private LLC rather than a bank. Those filings identify real lenders who funded real deals in your area recently.

What lien details tell you about terms and speed

Each recorded lien shows the loan amount, origination date, and lender name. A lender who closed multiple deals within a short window is actively deploying capital, which tells you they can move fast when the right deal comes in.

Repeat lenders in public records are the clearest signal that someone has both the capital and the process to close consistently.

How to build a shortlist from repeat lenders

Filter your search to lenders who appear more than twice in the last 12 months. Frequency indicates an active operation, not a one-time transaction from a private individual.

How to approach a lender you found in records

Reach out directly with a brief message that references a specific deal type they funded and explains your current project. That context earns a faster response than a cold pitch with no connection.

Legal and privacy boundaries to respect

Public records are legally accessible to anyone, but use the information professionally. Treat every outreach as a business introduction and never misrepresent how you found the contact.

8. Use online investor communities and social platforms

Online investor forums and social platforms have become active sourcing grounds for private money lenders for real estate. Facebook groups, BiggerPockets forums, and LinkedIn communities all host lenders who are actively looking for qualified borrowers with fundable deals rather than waiting for borrowers to find them through traditional channels.

Where private lenders actually look for deals

Lenders with capital to deploy participate in investment-focused Facebook groups and LinkedIn communities because deal flow surfaces quickly there. Search for groups specific to your market or property type and join the ones with consistent, deal-related activity rather than promotional clutter.

How to write a post lenders respond to

Lead your post with the deal specifics: location, purchase price, rehab budget, ARV, and your exit strategy. A post structured around clear numbers gets a response from serious lenders far faster than a vague request for "funding sources."

Keep your post concise and fact-based. Lenders scroll past anything that reads like a help-wanted ad.

What to share and what to keep private

Share deal structure details openly, but keep your purchase contract and seller contact information private until you have a signed term sheet. Protecting those details prevents other buyers from approaching your seller directly.

How to vet lenders you meet online

Ask any online contact for references from recent closings and verify their funding history before sharing sensitive deal documents. A lender who refuses to provide references is not worth pursuing further.

Scams and patterns to watch for

Watch for lenders who request upfront fees before issuing any terms or who pressure you to act within hours. Legitimate lenders do not charge you to review a deal.

9. Get referrals from other investors and business owners

Other investors and business owners in your network already work with private money lenders for real estate and can point you toward their best contacts. A warm referral shortens your vetting process significantly because the lender already has a proven track record with someone you trust.

How to ask for intros that people will make

Be specific when you ask. Tell your contact the deal type and loan size you need so they can make a targeted introduction rather than a blind referral that wastes everyone's time.

What to offer in return without crossing lines

Offer to return the favor when you come across a lender that fits their deal type. Keep it informal and avoid any arrangement that resembles a referral fee, which can create legal complications.

The best referral networks run on genuine reciprocity, not transactional favors.

How to qualify a lender through one phone call

Ask the lender how many deals they funded in the last 90 days and what their typical closing timeline looks like. Those two questions separate active lenders from people who deploy capital only when conditions are perfect.

How to build long-term lender relationships

Update your lender contacts after each closing with deal results and a short summary of how the project performed. That transparency keeps you top of mind when they have capital ready to deploy.

When to walk away from a "friendly" loan

Walk away when a lender pressures you to skip written terms or standard closing documentation, even if the referral came from someone you trust. Friendship does not replace a signed loan agreement.

Next Steps

You now have nine proven ways to find private money lenders for real estate, each one tested in real deal environments rather than pulled from theory. The most important move you can make right now is to pick two or three of these strategies and start working them this week, before your next deal is under contract and time pressure forces a rushed decision.

Building lender relationships before you need them is what separates investors who close consistently from those who scramble at the last minute. Your lender network is a long-term asset, and every introduction you make today pays off on future deals as well. Start with the strategies that match where you are right now, whether that means attending a local REIA or reaching out to a broker directly.

If you want to skip the search and work with a lender who understands investor timelines, connect with David Roa to discuss your next project.