8 Pros And Cons Of Investing In Commercial Real Estate

Commercial real estate can generate serious wealth, but it can also drain your capital if you go in unprepared. Understanding the pros and cons of investing in commercial real estate is the difference between building a portfolio that works for you and getting stuck with a property that bleeds money. With over 25 years in mortgage lending and hands-on experience as a real estate investor myself, I've seen both outcomes play out hundreds of times.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment properties. That volume gives us a front-row seat to what separates successful commercial investors from those who struggle, and it almost always comes down to how well they understood the full picture before signing on the dotted line.

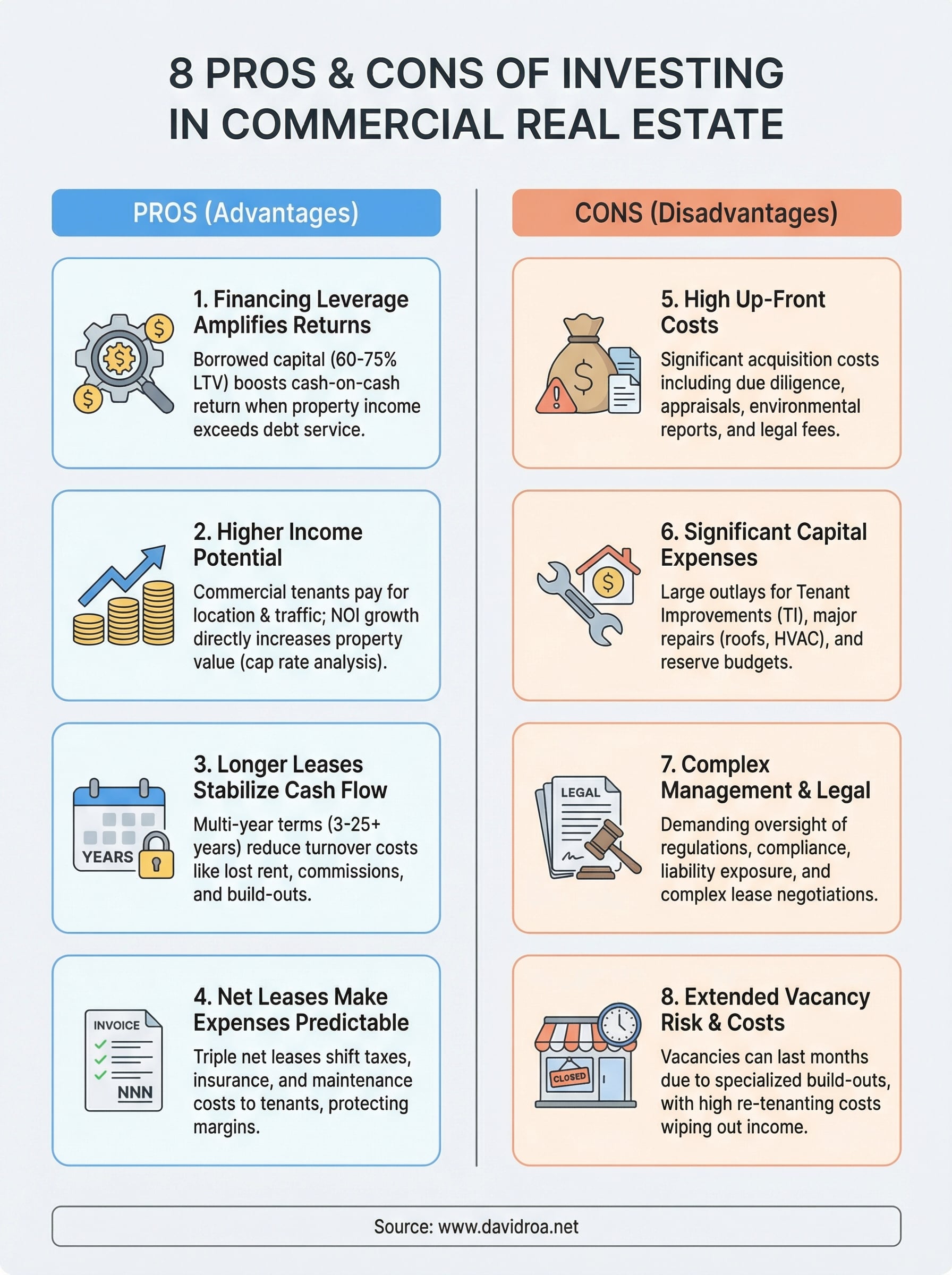

This article breaks down four major advantages and four real disadvantages of commercial real estate investing. No sugarcoating, no hype, just a straight breakdown based on what I've seen work (and fail) across SBA-backed acquisitions, mixed-use deals, and everything in between. By the end, you'll have a clear framework to decide whether commercial property belongs in your investment strategy.

1. Financing leverage can amplify returns

Leverage is one of the most powerful tools in commercial real estate investing, and it works differently here than in residential markets. When you use borrowed capital to acquire a property, your cash-on-cash return can far exceed what you'd earn if you paid all cash. The key is understanding how leverage actually functions before you put it to work.

What this means in commercial real estate

In commercial real estate, lenders typically finance 60% to 75% of a property's value, which means you bring 25% to 40% as a down payment. Your total return on equity is measured against what you put in, not the full purchase price. If a property generates $100,000 in net operating income and you financed 70% of a $1 million purchase, you're measuring that return against your $300,000 equity contribution, not the full $1M cost.

Leverage doesn't create returns, it amplifies returns that already exist in the deal, which means a bad deal gets worse, not better, with more debt on it.

When leverage becomes a real advantage

Leverage works best when your property's income significantly exceeds your debt service. That spread is your cushion against vacancies, repairs, and rate changes. If you're buying a stabilized asset with strong tenants and a debt service coverage ratio (DSCR) above 1.25, leverage can meaningfully accelerate your wealth-building timeline without putting the asset at serious risk.

Numbers to review before you borrow

Before you commit to any financing structure, review these figures carefully:

- Loan-to-value (LTV): Most commercial lenders cap this at 65-75%

- DSCR: Lenders typically require 1.20-1.35x; higher gives you more breathing room

- Interest rate type: Fixed vs. variable directly changes your long-term exposure

- Amortization and balloon terms: 20-25 year amortization with 5-10 year balloon periods is standard in commercial lending

Common financing pitfalls to avoid

One of the most common mistakes investors make is over-leveraging a deal to minimize their down payment, only to find the property barely covers its debt service. Another is ignoring balloon payment schedules, which are standard in commercial loans and can force a refinance at an unfavorable rate environment. Always stress-test your deal at a rate 2% higher than your current quote before you sign anything.

2. Income potential can beat residential rentals

One major advantage in the pros and cons of investing in commercial real estate is raw income potential. Commercial properties typically generate higher gross rents per square foot than residential rentals, and that gap can widen significantly depending on location and property type.

Why commercial rents can run higher

Commercial tenants pay for location, foot traffic, and business infrastructure, not just four walls and a roof. That economic dependency on the space means they're willing to pay more for it. Consider the income sources available to you on a single strip retail property:

- Anchor tenants who draw customer traffic and command longer terms

- Smaller inline tenants who pay a premium to benefit from that traffic

- Signage and common area rights that generate additional revenue streams

How NOI drives your real return

Net operating income (NOI) is the number that matters most to your investment performance. It equals gross income minus operating expenses, excluding debt service. Your lender and any future buyer will use NOI to assess your property's value through cap rate analysis, which means improving NOI directly increases what your asset is worth.

A 10% increase in NOI can translate into a substantial jump in appraised value, a dynamic that simply doesn't exist in residential real estate.

Metrics to compare deals apples-to-apples

Your three core benchmarks for comparing commercial income deals are cap rate (NOI divided by purchase price), cash-on-cash return (pre-tax cash flow divided by cash invested), and price per square foot within the same market and property class.

Situations where the income story breaks

Income projections fall apart fast when your vacancy rate climbs or a major tenant exits. A single-tenant property where the occupying business closes can drop from strong monthly cash flow to zero without warning, which is why tenant credit quality matters as much as the lease itself.

3. Longer leases can stabilize cash flow

Lease duration is one of the most overlooked factors when evaluating the pros and cons of investing in commercial real estate. Unlike residential rentals where tenants typically sign 12-month leases, commercial tenants commit to terms that can run years or even decades, which fundamentally changes how predictably your income flows.

Typical lease lengths by property type

Commercial lease terms vary widely depending on what you own. Office and retail properties often carry three to ten year leases, while industrial tenants and anchor retailers may sign 15 to 25 year agreements. Net lease properties with nationally recognized tenants frequently run 10 to 20 years with built-in options to extend.

Why lower turnover matters to investors

Every time a tenant vacates, you absorb real costs: lost rent, broker commissions, and often a full build-out for the next occupant. A tenant locked into a five-year lease represents five years of predictable income without the re-tenanting cycle that eats into residential landlords' margins constantly.

Long-term leases reduce your operating uncertainty and give lenders confidence in your property's income stream, which directly affects the financing terms you can secure.

Rent escalations and renewal options to watch

Strong leases include annual rent bumps, either fixed (2-3% per year) or tied to CPI. Review every renewal option clause carefully because tenants locking in below-market rents for another five years at their discretion can cap your upside significantly.

Red flags in tenant financial strength

A long lease only protects you if the tenant can actually pay. Request financial statements or review publicly available data for corporate tenants. A struggling business on a seven-year lease can default halfway through, leaving you with a long vacancy and a costly re-tenanting process.

4. Net leases can make expenses more predictable

Net leases shift operating costs from you to the tenant, which fundamentally changes how predictably you can plan your cash flow. Understanding these lease structures is one of the most practical parts of evaluating the pros and cons of investing in commercial real estate.

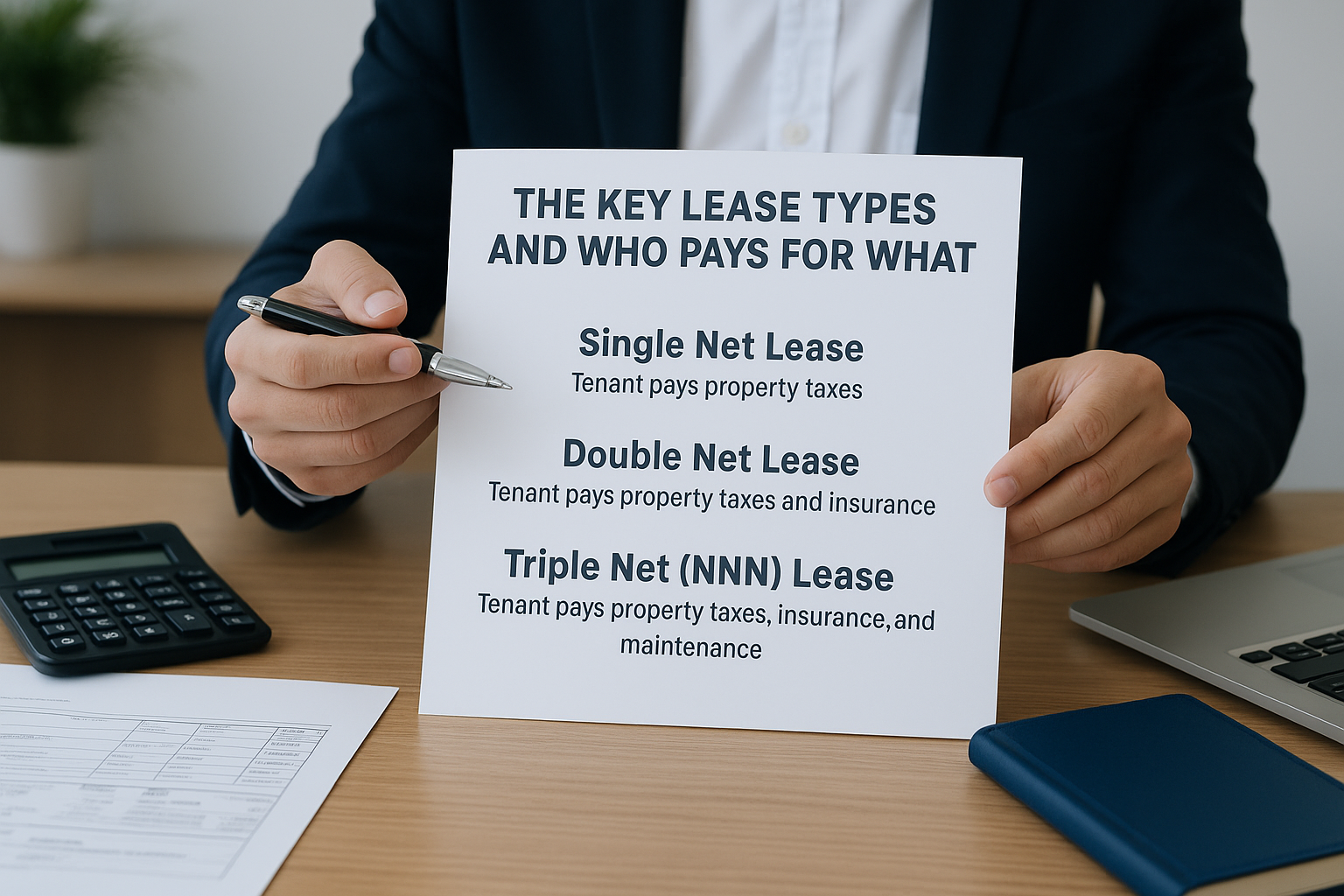

The key lease types and who pays for what

Commercial leases come in several forms, and each one defines who covers which expenses. A single net lease requires the tenant to pay property taxes in addition to base rent. A double net lease adds insurance to that responsibility. A triple net (NNN) lease places taxes, insurance, and maintenance on the tenant, making your income highly predictable month to month.

How pass-throughs can protect your margins

When expenses pass through to the tenant, your net income stays closer to what you projected when you underwrote the deal. Rising property taxes or insurance premiums no longer erode your returns the way they would under a gross lease.

Triple net leases are especially valuable during inflationary periods when operating costs climb faster than expected.

What to verify in CAM, tax, and insurance billing

CAM charges, tax reconciliations, and insurance billings require annual audits to confirm tenants are being billed correctly. Errors in CAM calculations are common and can cost you real money if you don't catch them during reconciliation.

Risks of relying on a single lease structure

Building your entire portfolio around NNN properties creates concentration risk. If market conditions shift or your tenant base changes, a single lease structure may leave you overexposed at the wrong time.

5. Up-front costs and capital expenses can be huge

One of the sharpest disadvantages in the pros and cons of investing in commercial real estate is how much capital you need before you collect your first dollar of income. Down payments, closing costs, inspections, and environmental assessments can easily push your initial outlay well past what most residential investors expect.

Where the big checks show up in CRE

Acquisition costs in commercial real estate extend far beyond the down payment. Before closing, you're also covering a stack of required due diligence expenses that add up fast:

- Commercial appraisal: $2,000 to $10,000+

- Phase I environmental report: $1,500 to $5,000

- Phase II environmental (if triggered): $10,000 to $50,000+

- Legal fees and title insurance: $5,000 to $20,000+

Tenant improvements and leasing commissions explained

When you sign a new tenant, tenant improvement (TI) allowances often run $30 to $75 per square foot or more for office and retail spaces. On top of that, leasing commissions to brokers typically range from 3% to 6% of the total lease value, and those costs land on you upfront, not spread over the lease term.

The combination of TI costs and leasing commissions on a single new tenant can easily equal six to twelve months of that tenant's rent.

Reserve planning for roofs, HVAC, and parking lots

Capital reserve budgets protect you when major systems fail. Commercial roofs, HVAC units, and parking lots carry significant replacement costs that can run from $50,000 to several hundred thousand dollars depending on building size.

How investors stress-test CapEx risk

Before closing, run a thorough property condition assessment to identify near-term capital needs. Build your CapEx reserves into your underwriting model from day one so a surprise replacement doesn't wipe out your cash flow position.

6. Management and legal complexity runs higher

One disadvantage that shows up consistently in the pros and cons of investing in commercial real estate is how much more demanding the management side becomes. Commercial properties carry regulatory requirements, tenant relationships, and legal structures that residential investors rarely encounter, and underestimating that complexity leads to costly mistakes.

What gets more complicated than residential

Commercial property management involves tracking multiple lease agreements, coordinating vendor contracts, and monitoring compliance across local, state, and federal regulations simultaneously. Unlike residential rentals, where your obligations are relatively straightforward, commercial buildings demand ongoing attention to zoning laws, building codes, and permitted-use clauses that can shift as your tenants' businesses evolve.

Compliance, safety, and liability exposure

Your liability exposure in commercial real estate extends well beyond basic maintenance. ADA compliance, fire safety inspections, environmental regulations, and occupancy requirements all fall on you as the property owner. Failing any of these audits can result in fines, forced closures, or litigation that wipes out your cash flow far faster than any vacancy would.

A single compliance violation on a commercial property can cost more than an entire year of net operating income.

Why leases require more negotiation and oversight

Commercial leases routinely run 20 to 50 pages and contain clauses covering exclusivity rights, permitted use, subletting, co-tenancy, and assignment. Each clause carries real financial consequences if you sign without fully understanding what you are agreeing to.

When to hire a property manager and attorney

Budget for a qualified commercial property manager and a real estate attorney before you close on any deal. Their fees are modest compared to the cost of a disputed lease clause or a missed compliance deadline.

7. Vacancy risk and re-tenanting costs can hit hard

Vacancy is one of the most damaging variables in the pros and cons of investing in commercial real estate. Unlike residential rentals where a new tenant can be placed within weeks, commercial vacancies can stretch for months or years depending on market conditions and property type.

Why vacancies last longer in many CRE markets

Commercial spaces require specialized build-outs and attract a narrower pool of prospective tenants than apartments or single-family homes. Your property may sit empty for six to eighteen months while you negotiate a deal, complete a build-out, and wait for the new tenant to open for business.

Tenant concentration and co-tenancy ripple effects

When one major tenant vacates a multi-tenant property, smaller tenants sometimes exercise co-tenancy clauses that allow them to reduce rent or exit their leases entirely. Your single largest tenant leaving can trigger a chain reaction that drops occupancy and income simultaneously.

Losing an anchor tenant in a retail center can cut your property's market value by 20% to 40% before you sign a replacement.

The real cost of downtime and build-outs

Every month of vacancy represents lost rent plus continued mortgage payments, taxes, insurance, and maintenance costs. Add a $40 to $80 per square foot tenant improvement allowance for the next tenant, and the total cost of one vacancy cycle can easily exceed a full year of gross income.

How to underwrite vacancy and protect downside

Model a 10% to 15% vacancy rate into your pro forma before you close any commercial deal. Holding six to twelve months of operating reserves gives you the runway to re-tenant without being forced into a bad lease just to cover debt service.

Your next steps

The pros and cons of investing in commercial real estate come down to one core question: does your deal generate enough income and stability to justify the complexity and capital it demands? Commercial real estate can absolutely outperform residential investing, but only when you go in with clear underwriting, realistic reserves, and a solid financing structure behind you.

Every advantage covered in this article, from leverage and long-term leases to net lease pass-throughs, depends on getting your financing terms right from the start. The disadvantages, from vacancy risk to capital expenses, become far more manageable when you work with a lender who understands commercial deals rather than one learning on your transaction.

If you're ready to move forward on a commercial acquisition, a mixed-use property, or an investment that needs specialized financing, connect with David Roa to review your options with someone who has funded these deals firsthand.