Refinance Mortgage To Remove PMI: Steps, Costs, Break-Even

PMI adds hundreds of dollars to your monthly mortgage payment, and once you've built enough equity, there's no reason to keep paying it. If you're exploring whether to refinance mortgage to remove PMI, you're asking the right question, but the answer depends on your current loan balance, home value, and how long you plan to stay in the property. Not every homeowner should refinance to drop PMI, because closing costs can eat into the savings if the math doesn't work in your favor.

That's exactly where a clear breakdown of the process helps. You need to know what lenders require, how much equity triggers PMI removal, and whether a refinance actually saves you more than simply requesting cancellation from your current servicer. The break-even point, the moment your monthly savings outweigh the cost of refinancing, is the number that matters most.

With over 25 years in mortgage lending and more than $150 million funded, I've walked hundreds of borrowers through this exact decision at David Roa. Below, I'll cover the steps, costs, and calculations so you can determine whether refinancing out of PMI is worth it, or if there's a better path.

When refinancing removes PMI and when it won't

The short answer: a refinance removes PMI when your new loan-to-value (LTV) ratio comes in at 80% or below based on a new appraisal. If your home has appreciated or you've paid down the balance enough to hit that threshold, the lender will issue the new loan without PMI attached. But whether refinancing is the right tool depends heavily on your loan type and current interest rate environment, so it's worth understanding the scenarios before you start the application process.

When a refinance successfully removes PMI

A conventional loan borrower with 20% or more equity is the clearest candidate. If your home's value has risen since you bought it, a new appraisal can confirm a lower LTV and qualify you for a PMI-free conventional refinance. For example, if you bought a home for $300,000 with 5% down and the balance is now around $270,000, but the home appraised at $380,000, your LTV sits at roughly 71%, which comfortably clears the 80% mark.

FHA borrowers face a different situation entirely. The FHA's mortgage insurance premium (MIP) does not automatically cancel on loans originated after June 2013, regardless of how much equity you build. Paying down the balance won't trigger removal the way it does on a conventional loan.

The only path to eliminating MIP on a post-2013 FHA loan is to refinance mortgage to remove PMI by converting to a conventional loan with enough equity to avoid new PMI.

This distinction changes the entire cost analysis. You're not just refinancing to drop a line item on your statement; you're switching loan products entirely. That means comparing MIP rates against conventional PMI rates, evaluating closing costs, and deciding whether the new interest rate makes the move worthwhile over your remaining time in the home.

When refinancing won't remove PMI or isn't worth it

Refinancing won't solve your problem if your LTV is still above 80% after a new appraisal. If home values in your area have stayed flat or declined, you may not have built enough equity yet, and a refinance will attach new PMI to the replacement loan. That means paying closing costs to end up in the same position.

Refinancing also becomes a costly mistake when your current rate is significantly lower than today's market rates. If you locked in at 3.5% and current rates are in the 7% range, the extra interest you'd pay over the life of the loan would far exceed the total cost of PMI. In that case, your better alternatives are requesting cancellation directly from your servicer once you reach 20% equity or waiting for automatic termination at 22% equity, which is your legal right under the Homeowners Protection Act.

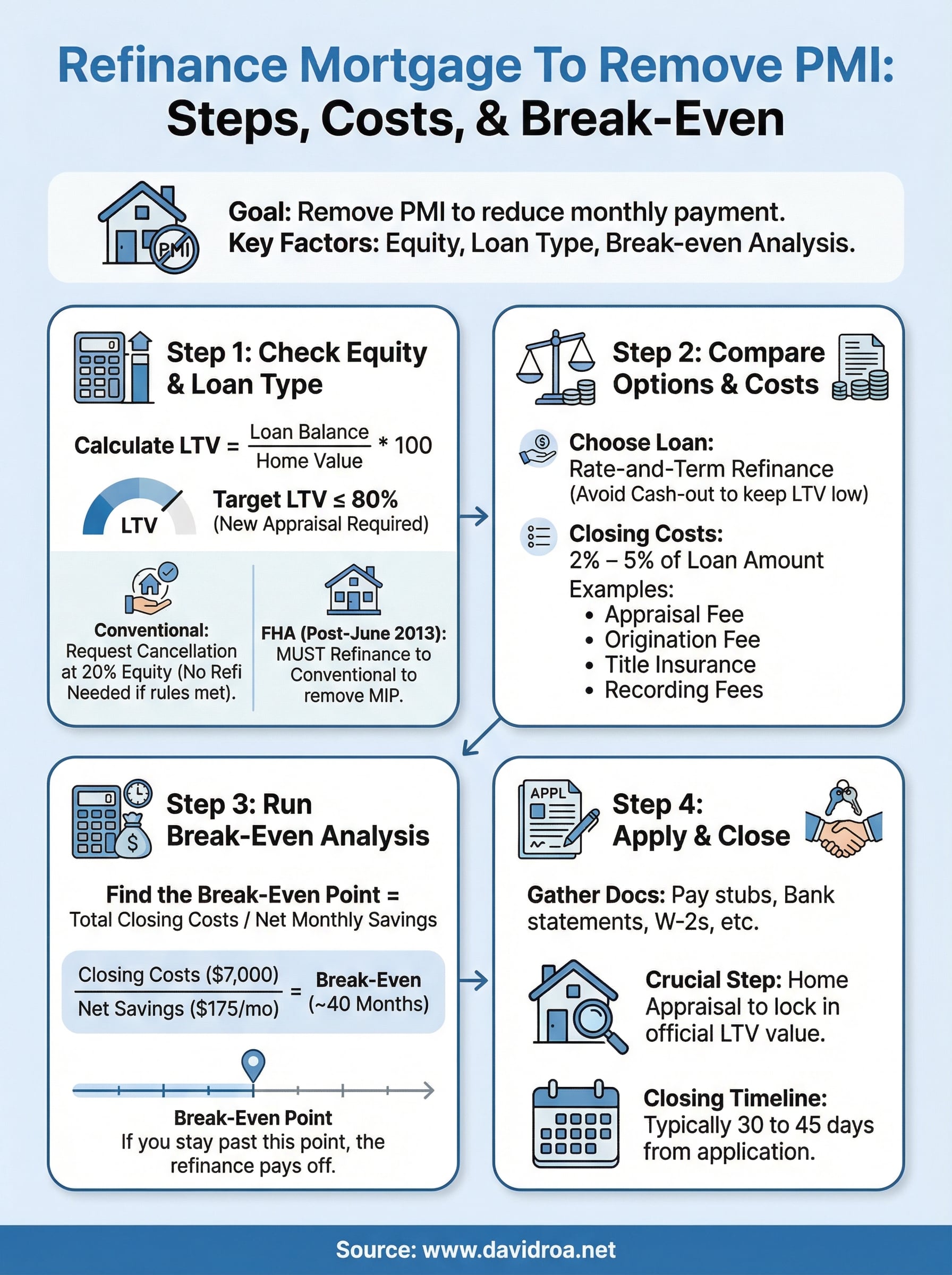

Step 1. Check your equity and loan type

Before you contact a lender or request an appraisal, you need two numbers: your current loan balance and your home's estimated market value. Pull your most recent mortgage statement for the balance, then research comparable recent sales in your neighborhood to get a rough value estimate. This initial check tells you whether a refinance to remove PMI is even in range, or whether you should hold off and wait for more equity to accumulate.

Calculate your current LTV

Your loan-to-value ratio is the figure that determines everything. Divide your remaining loan balance by your home's estimated value, then multiply by 100. If your balance is $220,000 and your home is worth $290,000, your LTV is roughly 75.8%, which clears the 80% threshold lenders require to issue a conventional loan without PMI.

If your LTV sits between 80% and 85%, you may be close enough that a formal appraisal, which often comes in slightly higher than informal estimates, could push you over the line.

Here's a quick reference for what different LTV ranges mean for your options:

| LTV Range | PMI Removal Path |

|---|---|

| Below 80% | Refinance or cancellation request qualifies |

| 80% to 85% | Formal appraisal may confirm eligibility |

| 85% to 90% | Continue paying down balance; monitor home value |

| Above 90% | Refinancing now adds new PMI; wait for more equity |

Identify your loan type

Conventional and FHA loans follow completely different rules, so knowing which one you have changes your next move entirely. On a conventional loan, you can request PMI cancellation without refinancing once you hit 20% equity. With an FHA loan originated after June 2013, the only way to eliminate MIP is to refinance mortgage to remove PMI by switching to a conventional product. Check your loan documents or call your servicer to confirm the loan type before taking any further steps.

Step 2. Compare refinance options and costs

Once you confirm you have enough equity, the next step is getting loan estimates from multiple lenders and building a complete picture of what the refinance will actually cost you. Most borrowers focus only on the new interest rate, but closing costs and loan structure matter just as much when your primary goal is eliminating PMI.

Types of refinance loans to consider

Two products dominate this decision: a rate-and-term refinance and a cash-out refinance. A rate-and-term refinance replaces your existing loan with a new one at a different rate or term without pulling cash out of your equity. This is the cleaner option when you want to refinance mortgage to remove PMI and potentially lower your monthly payment at the same time. A cash-out refinance pulls equity out as cash, which raises your loan balance and can push your LTV back above 80%, reattaching PMI to the new loan and canceling out the benefit.

Stick with a rate-and-term refinance when your goal is PMI removal; a cash-out option introduces new risk and often defeats the purpose entirely.

What closing costs to expect

Closing costs on a refinance typically run 2% to 5% of the loan amount. On a $250,000 loan, that's $5,000 to $12,500 out of pocket or rolled into the new balance. Here's a breakdown of the standard line items you'll see on a loan estimate:

| Cost Item | Typical Range |

|---|---|

| Appraisal fee | $400 to $700 |

| Origination fee | 0.5% to 1% of loan amount |

| Title insurance | $500 to $1,500 |

| Recording fees | $100 to $300 |

| Prepaid interest | Varies by closing date |

Request loan estimates from at least three lenders and compare them line by line, not just the advertised rate. Submit all applications within a 14-day window so the credit inquiries bundle together as a single hard pull on your credit report, protecting your score during the shopping process.

Step 3. Run a break-even calculation

The break-even calculation answers one straightforward question: how many months until your monthly savings cover the full cost of refinancing? If you plan to stay in the home beyond that point, the refinance makes financial sense. If you're likely to sell or refinance again before then, you'll pay closing costs without recovering them, and the move costs you money.

Calculate your monthly savings

Your monthly savings come from two sources: eliminating PMI and any reduction in your interest rate. Subtract your new projected monthly payment from your current monthly payment to get the total monthly benefit. If your current payment is $1,850 with PMI and your new payment would be $1,680 without PMI at the new rate, your net monthly savings equal $170.

Be careful when your new interest rate is higher than your current one. In that scenario, the rate increase partially offsets the PMI elimination, and your real monthly savings are smaller than the PMI amount alone. Run both numbers separately so you see the complete picture before making a decision.

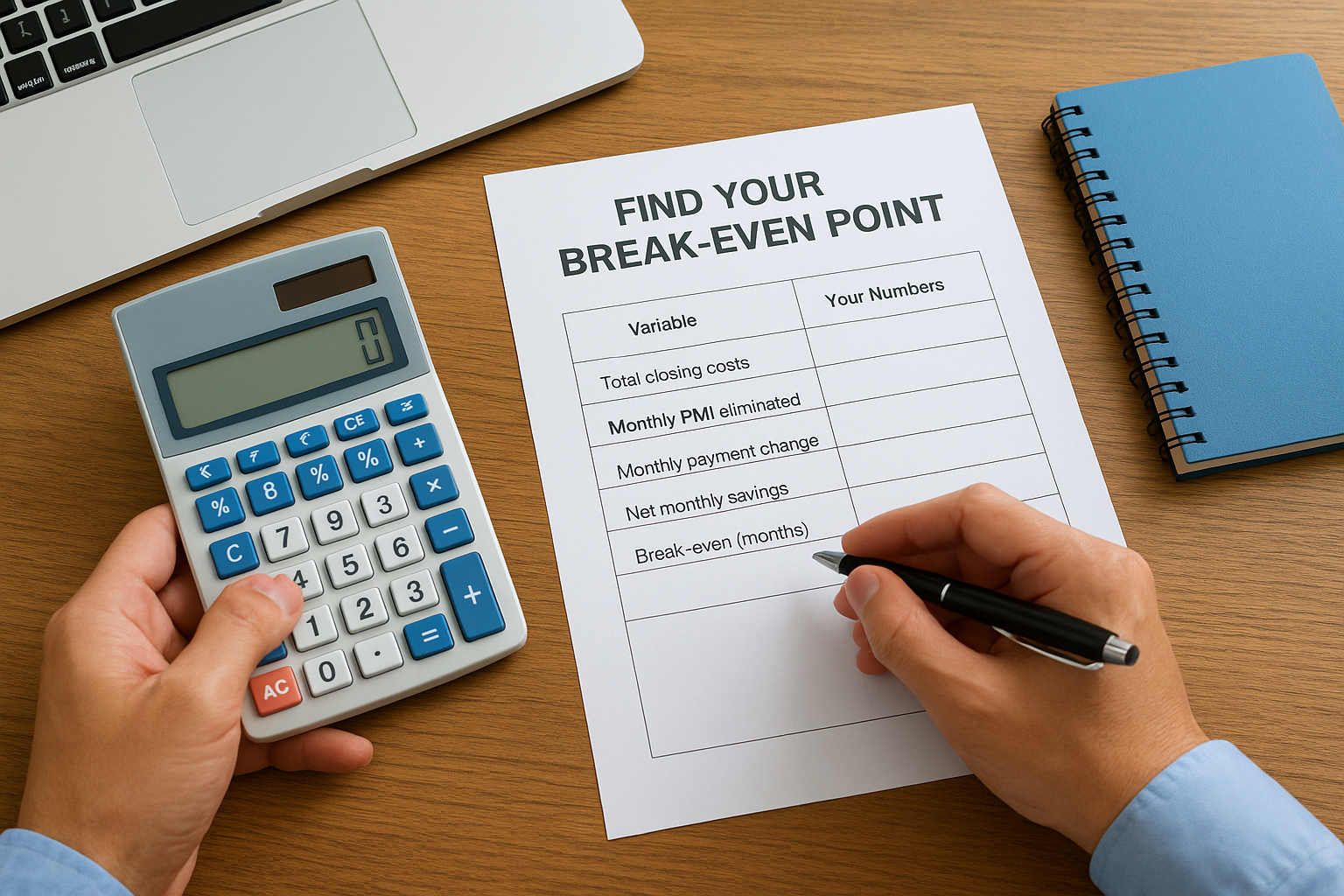

Find your break-even point

Divide your total closing costs by your monthly savings to get the break-even timeline in months. Use this template with your own numbers:

| Variable | Your Numbers |

|---|---|

| Total closing costs | $_______ |

| Monthly PMI eliminated | $_______ |

| Monthly payment change from rate | $_______ |

| Net monthly savings | $_______ |

| Break-even (months) | Closing costs / Net savings |

For example, if your closing costs are $7,000 and your net monthly savings are $175, your break-even lands at 40 months, roughly 3.3 years. If you plan to stay in the home longer, the decision to refinance mortgage to remove pmi puts real money back in your pocket over time.

Run this calculation before you apply, because it's the clearest indicator of whether the refinance actually benefits you financially.

Step 4. Apply and close the refinance

Once your break-even math confirms the refinance makes sense, the process moves quickly if you come prepared. Most refinances close in 30 to 45 days from application, and the biggest delays come from missing documents or an appraisal that comes in lower than expected. Knowing what to expect at each stage helps you move faster and avoid surprises.

Submit your application and gather documents

You'll submit a formal loan application with the lender who offered the best terms in your comparison. The lender will order a home appraisal, which is the most critical step when your goal is to refinance mortgage to remove PMI, because the appraised value locks in your official LTV. Prepare your documents before you apply so you can respond to requests the same day they arrive.

Here's a checklist of what most lenders require:

- Two most recent pay stubs (or two years of tax returns if self-employed)

- Two most recent bank statements for all accounts

- Two years of W-2 forms

- Most recent mortgage statement

- Homeowners insurance declarations page

- Photo ID and Social Security number

Responding to lender document requests within 24 hours is one of the fastest ways to shorten your closing timeline.

What to expect at closing

Your lender will send a Closing Disclosure at least three business days before your closing date. Review it line by line against the loan estimate you received earlier and flag any fees that changed without explanation. You have the right to ask for clarification on every line item before you sign.

At closing, you'll sign the final loan documents, pay any closing costs not rolled into the loan balance, and the new loan pays off the old one. PMI drops off immediately because the new loan is issued without it from day one.

Next steps

You now have a complete framework for deciding whether to refinance mortgage to remove PMI: check your equity, compare loan options, run the break-even math, and move through the application with your documents ready. If your LTV clears 80% and your monthly savings outpace closing costs within a timeline that matches how long you plan to stay in the home, refinancing is a straightforward financial win. If the numbers don't support it yet, your clearest path forward is paying down the balance and requesting cancellation once you hit 20% equity.

Every borrower's situation is different, and the right move depends on your loan type, current rate, and home value. Getting a second opinion from an experienced lender costs you nothing and can prevent a costly mistake. If you want to run through your specific numbers with someone who has helped borrowers close over $150 million in loans, reach out to David Roa to start the conversation.