SBA Lender Match Tool: How It Works And How To Apply Online

Finding the right lender for an SBA loan can feel like a guessing game, especially when you're a business owner with limited time and a long list of requirements. That's exactly the problem the SBA Lender Match tool was built to solve. It's a free, government-backed platform that connects you with SBA-approved lenders based on your specific financing needs, and it does so within 48 hours of submitting your information.

But like most government tools, there's a gap between what it promises and what actually happens once you hit "submit." Some borrowers get matched quickly and move forward. Others hear from lenders who aren't a great fit, or don't hear back at all. Understanding how the tool works before you use it gives you a real advantage in the process and helps you avoid wasting time on dead-end conversations.

At David Roa, we handle SBA 7(a) and 504 loans as part of our commercial financing services, backed by over 25 years of lending experience and more than $150 million funded. This article breaks down exactly how the SBA Lender Match tool works, what you need to apply, and how to use it strategically, whether you go through the platform alone or work directly with an experienced lender from the start.

What the SBA Lender Match tool is

The SBA Lender Match tool is a free online resource built and maintained by the U.S. Small Business Administration. It acts as a bridge between small business owners and SBA-approved lenders across the country. Instead of cold-calling banks or spending hours researching who participates in SBA loan programs, you fill out a short form describing your business and financing needs, and the platform surfaces lenders who may be interested in working with you.

The SBA does not lend money directly to businesses. It guarantees a portion of loans made by approved lenders, which is why finding the right participating lender is the critical first step.

What the tool does and doesn't do

The Lender Match platform collects your basic business information and sends it to lenders in its network who match your profile. Within roughly 48 hours, interested lenders can contact you directly with details about their programs and next steps. What the tool does not do is approve your loan, lock in rates, or guarantee you'll receive funding. It simply connects you with potential lenders who have expressed interest based on what you submitted.

Think of it as a referral service, not an application portal. You still need to go through each lender's individual underwriting and qualification process after the initial match.

Who runs the tool

The U.S. Small Business Administration operates Lender Match as part of its broader effort to expand access to capital for small businesses. It lives on the official SBA.gov website, which means there's no cost to use it and no third-party organization is involved in collecting your information at that stage. The SBA built this platform to reduce the friction business owners face when trying to identify qualified lending partners without an existing banking relationship.

Why the tool matters for SBA loan shopping

Finding an SBA-approved lender on your own is harder than it sounds. The SBA works with thousands of lenders nationwide, and not every bank or credit union participates in every SBA loan program. Without a starting point, you can spend weeks calling institutions, filling out pre-qualification forms, and still end up talking to lenders who don't serve your industry or loan size. The SBA Lender Match tool cuts that process down significantly by pre-filtering the lender pool for you.

The access problem it solves

Many business owners, especially those without an established banking relationship, struggle to even get a conversation started with a lender. Traditional banks often prioritize existing customers when reviewing SBA applications, which puts newer businesses or those with non-traditional financials at a disadvantage.

The Lender Match platform levels the field by letting lenders review your profile and reach out to you, rather than requiring you to know the right person at the right institution.

The tool is particularly valuable if you're exploring multiple SBA loan types, such as a 7(a) loan for working capital versus a 504 loan for real estate or equipment. Different lenders specialize in different programs, and the platform helps surface those specializations without requiring you to research each institution individually.

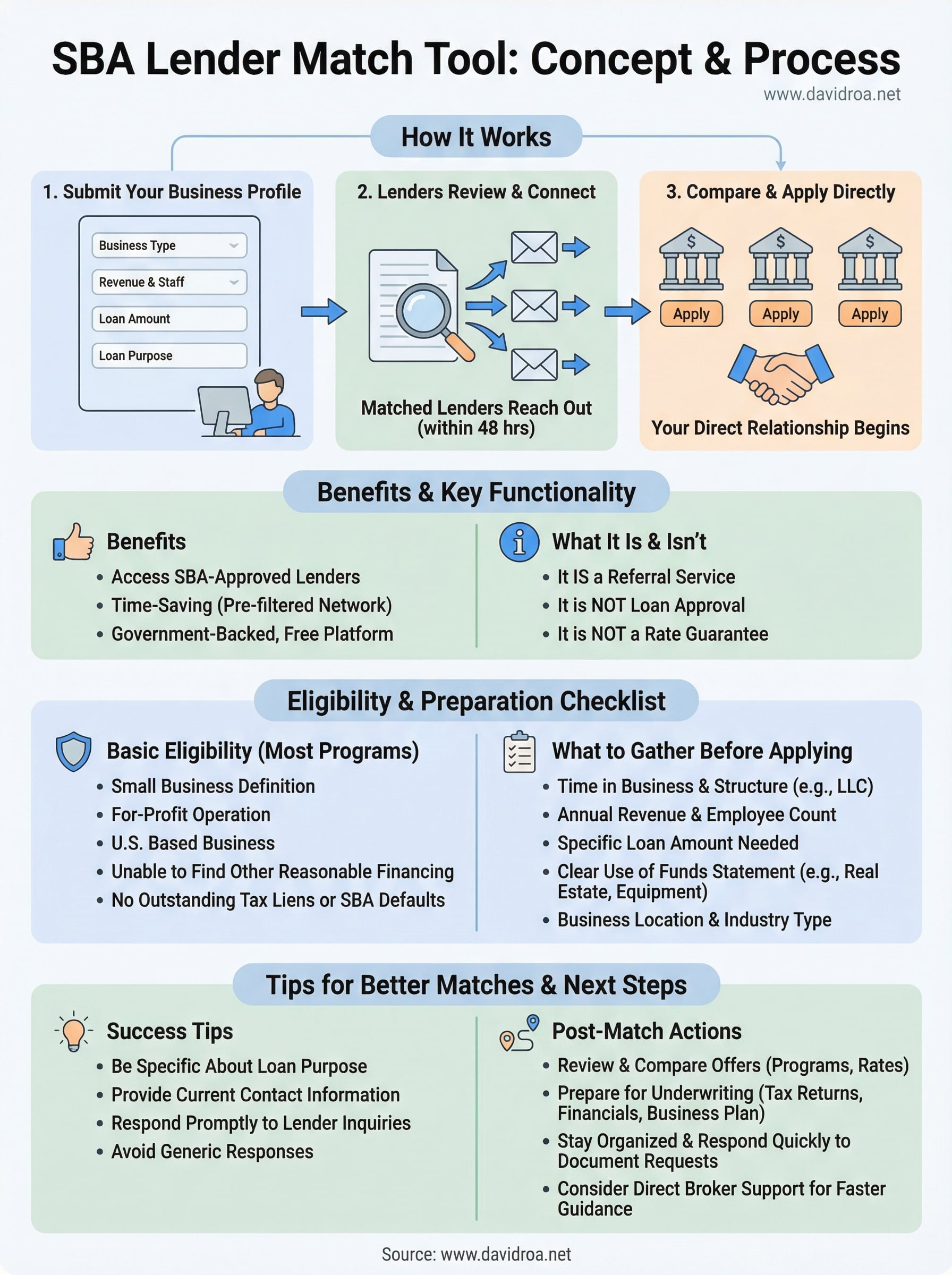

How SBA Lender Match works step by step

The SBA Lender Match tool follows a straightforward process, but knowing what happens at each stage helps you prepare the right information and set realistic expectations before you start.

Step 1: Fill out the intake form

You visit SBA.gov and complete a short questionnaire covering your business type, how long you've been operating, the amount you want to borrow, and what you plan to use the funds for. The form takes about five to ten minutes. You also provide your contact information so lenders can reach you after reviewing your profile.

Step 2: Lenders review your profile

After you submit, the platform shares your information with SBA-approved lenders in its network whose programs align with what you described. Lenders then decide whether to reach out based on your loan purpose, amount, and business profile.

Most borrowers hear from interested lenders within 48 hours, though response volume varies based on your loan size and location.

Step 3: Review and respond to lender outreach

You receive emails from lenders who expressed interest and can review each one to compare programs, rates, and terms. From there, you choose who to continue conversations with and begin each lender's individual application process. The platform's job ends here; the rest depends on your direct relationship with each lender.

Eligibility and info you need before you start

Before you open the SBA Lender Match tool, it helps to know whether your business qualifies for SBA financing in the first place. The platform won't screen you out during the form, but lenders will review your profile and pass on it quickly if you don't meet basic program requirements.

Basic eligibility requirements

Your business needs to meet the SBA's definition of a small business, operate for profit, and be based in the United States. Most SBA loan programs also require that you've already sought financing elsewhere and couldn't secure it on reasonable terms, which is a standard SBA condition most lenders will ask about.

If your business has an outstanding tax lien or a prior SBA loan default, most lenders in the network will decline to reach out, regardless of your current financials.

Information to gather before you submit

Walking into the form prepared speeds up the entire matching process and makes your profile more credible to lenders reviewing it. Before you start, collect the following:

- Time in business and legal business structure (LLC, S-Corp, sole proprietor, etc.)

- Estimated annual revenue and current employee count

- The specific loan amount you need and a clear use of funds statement

- Your business location and industry type

Having these details ready lets you fill out the form accurately and gives lenders the context they need to take your profile seriously.

Tips to get better lender matches and replies

Your intake form is the only thing lenders see before deciding whether to contact you. Vague or incomplete answers reduce your chances of hearing back, while a clear and specific profile attracts lenders who are actually positioned to help. A few deliberate adjustments to how you fill out the form can make a real difference in the quality and volume of responses you receive.

Be specific about your loan purpose

Generic use-of-funds statements like "business expansion" or "working capital" don't give lenders enough to work with. Describe exactly what you need the money for, such as purchasing equipment, hiring staff, or acquiring commercial property. Lenders want to see that you've thought through the capital use before they commit time to reviewing your file.

The more specific your loan purpose, the easier it is for lenders to match their programs to your actual need.

Keep your contact information current

After you submit through the SBA Lender Match tool, lenders reach out by email within 48 hours. Respond to every inquiry promptly, even while you're still comparing options. Use these habits to stay on top of replies:

- Check the inbox tied to your submission every day

- Reply within 24 hours to keep lenders engaged

- Avoid generic responses; reference what each lender mentioned to show you reviewed their message

Next steps after you get matched

Once lenders respond to your SBA Lender Match tool submission, the work shifts from form-filling to decision-making. Review each lender's message carefully and compare their loan programs, rates, and documentation requirements before committing to one. Not every response will be the right fit, and that's fine. Prioritize lenders who specialize in the loan type you need, ask about their average closing timelines, and request a clear list of what they need from you upfront.

From there, you move into formal underwriting, which means submitting tax returns, financial statements, and a business plan depending on the program. Stay organized and respond quickly to document requests, since delays on your end slow the entire process down. If the matched lenders aren't a strong fit or you want a faster path to funding, working directly with an experienced broker cuts through the back-and-forth. Connect with David Roa to get expert guidance on SBA financing and find the right loan for your situation.