Understanding Hard Money Loans: Terms, Process, Pros & Cons

You've found the perfect investment property. The numbers work, the location is right, and you can already see the profit potential. There's just one problem: traditional banks move too slowly, and the deal won't wait. This is exactly where understanding hard money loans becomes essential for real estate investors who need to act fast and close with confidence.

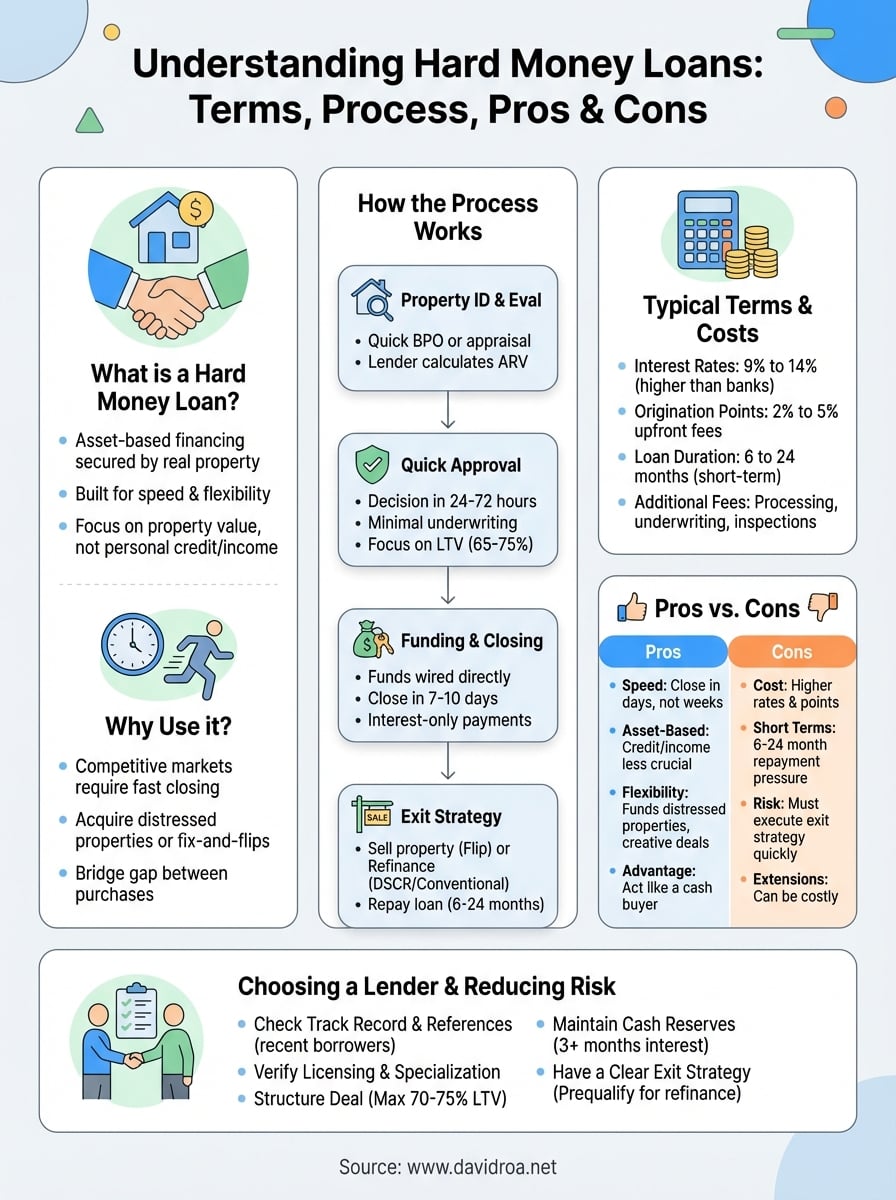

Hard money loans are asset-based financing solutions secured by real property rather than your personal credit history or income documentation. They're built for speed and flexibility, two things conventional lenders rarely offer. Whether you're flipping houses, acquiring rental properties, or bridging the gap between purchases, hard money can be the tool that makes your deal possible when banks say no or take too long.

With over 25 years in the mortgage and lending industry and more than $150 million funded, I've helped countless investors navigate financing options that fit their specific situations. As someone who actively flips properties myself, I understand the real-world pressure of time-sensitive deals and why hard money exists as a legitimate strategy, not a last resort.

This guide breaks down how hard money loans actually work, what terms you can expect, and the advantages and drawbacks compared to traditional financing. By the end, you'll have the clarity to decide whether hard money fits your next investment move.

Why hard money loans matter in real estate deals

Real estate moves fast, and the investors who win are the ones who can close quickly. Hard money loans exist because traditional financing doesn't match the pace of competitive markets. When you spot a distressed property at 30% below market value or face multiple offers on a rental unit, waiting 30 to 45 days for bank approval means you lose the deal to someone with cash or faster funding.

Speed closes deals that banks can't

Banks require extensive documentation, appraisals, underwriting reviews, and committee approvals. Hard money lenders skip most of that. You can get approved in days and funded within a week, sometimes faster. This speed gives you the power to act like a cash buyer, which sellers and listing agents heavily favor. Properties in probate sales, foreclosure auctions, or time-sensitive estate situations won't wait for conventional loan processes.

The ability to close in 7 to 10 days instead of 30 to 45 days can be the difference between securing a profitable investment and watching someone else take it.

Understanding hard money loans means recognizing that flexibility and timing create value in ways banks simply cannot provide. I've seen investors double their portfolio in a year solely because they could move when opportunities appeared, not when a loan officer finally returned their call.

Asset value matters more than credit scores

Traditional lenders focus on your W-2 income, tax returns, debt-to-income ratios, and credit history. Hard money lenders care about one thing above all: the property's value and equity position. If you're buying a property worth $300,000 for $200,000, the lender sees built-in protection through that $100,000 equity cushion.

This shift changes everything for investors who don't fit the conventional borrower profile. Maybe you're self-employed with irregular income documentation. Perhaps you've already maxed out conventional loan limits across your portfolio. Hard money doesn't penalize you for these situations because the real estate itself secures the loan, not your personal financial history. The property's potential return drives the approval, which aligns perfectly with how real investors actually operate.

How hard money loans work from application to payoff

The process starts with property identification and evaluation, not credit checks or income verification. You bring a deal to the lender, who assesses the property's current value and after-repair value (ARV) to determine loan eligibility. Most hard money lenders fund 65% to 75% of the property's purchase price or current value, sometimes adding rehab costs into the loan amount for fix-and-flip projects.

Property evaluation and quick approval

Hard money lenders order a broker price opinion (BPO) or quick appraisal rather than the full appraisal traditional lenders require. This cuts approval time dramatically. You'll submit basic information: the property address, purchase price, estimated repair costs, and your exit strategy (flip, refinance, or rental). The lender focuses on whether the numbers support the loan, not your employment history or tax returns.

Approval typically happens within 24 to 72 hours because there's minimal underwriting. The lender calculates loan-to-value (LTV) ratios and confirms the property provides adequate collateral. Once approved, you move to closing within days, not weeks.

Funding, closing, and exit strategies

You close with a title company just like any real estate transaction, but with far less documentation. The lender wires funds directly to escrow, and you take possession. Repayment terms usually run 6 to 24 months, giving you time to complete renovations and sell or refinance into permanent financing.

Understanding hard money loans means knowing your exit strategy before you borrow, because these are short-term tools designed for specific investment scenarios.

Most investors either flip the property and pay off the loan from sale proceeds, or refinance into a conventional mortgage or DSCR loan once the property is stabilized and rented.

Typical hard money loan terms, rates, and fees

Hard money costs more than conventional financing because you're paying for speed, flexibility, and asset-based approval. Interest rates typically range from 9% to 14%, sometimes higher for riskier deals or borrowers with limited experience. These rates reflect the lender's higher risk and shorter loan duration compared to traditional 30-year mortgages.

Interest rates and points

Beyond the interest rate, you'll pay origination points, typically 2 to 5 points of the total loan amount. If you borrow $200,000, expect to pay $4,000 to $10,000 in upfront fees just to secure the loan. These points compensate lenders for the quick underwriting and the risk they assume by lending based on property value rather than your credit profile.

Understanding hard money loans means recognizing that higher costs are the tradeoff for accessing capital that traditional lenders won't provide on your timeline.

Some lenders charge additional fees for processing, underwriting, or property inspections, which can add another $1,000 to $3,000 to your total costs. Always ask for a complete fee breakdown before committing to any lender.

Loan duration and repayment structure

Most hard money loans run 6 to 24 months, with 12 months being the most common term. You'll typically make interest-only monthly payments, with the full principal due at the end of the term through a balloon payment. This structure keeps your monthly expenses low while you complete renovations or stabilize the property for refinancing.

Extension options exist if your project takes longer than expected, but lenders charge additional points or higher interest rates for extensions. Plan your exit strategy carefully to avoid these extra costs.

Pros and cons compared to traditional financing

Hard money loans and traditional bank financing serve different purposes, and understanding hard money loans means recognizing when each option makes sense for your investment strategy. Traditional mortgages offer lower rates and longer terms, but they sacrifice speed and flexibility. Hard money delivers immediate capital and asset-based approval, but you pay premium costs for those advantages.

Advantages of hard money financing

Speed gives you the biggest competitive edge. You can close in 7 to 10 days versus 30 to 45 days with banks, which means you win time-sensitive deals that other investors miss. Credit history and income documentation become irrelevant since lenders focus on property value, not your W-2s or tax returns. This opens opportunities for self-employed investors, those with multiple properties, or anyone who doesn't fit conventional lending boxes.

Hard money lets you act like a cash buyer without liquidating assets, giving you purchasing power that traditional financing simply cannot match on short notice.

Flexibility extends to property condition as well. Banks won't lend on properties needing major repairs, but hard money lenders fund distressed properties that you plan to renovate and flip or refinance.

Disadvantages to consider

Cost represents the primary drawback. Interest rates of 9% to 14% plus 2 to 5 points upfront mean you're paying significantly more than conventional loans at 6% to 7%. Short repayment terms of 6 to 24 months create pressure to execute your exit strategy quickly, whether that's selling or refinancing. If your project takes longer than expected or market conditions shift, you may face extension fees or forced sales at unfavorable prices.

How to choose a lender and reduce risk

Choosing the right hard money lender protects your investment and prevents costly mistakes that can derail profitable deals. Start by vetting lenders based on their track record in your specific market and property type. Ask for references from recent borrowers who completed similar projects. Understanding hard money loans includes knowing that not all lenders operate with the same standards, so due diligence on the lender matters as much as the property itself.

Check lender track record and references

Request references from at least three recent borrowers who closed deals in the past six months. Ask those borrowers about communication quality, hidden fees, and whether the lender funded on time. Experienced lenders who specialize in your property type (fix-and-flip, rental acquisitions, or commercial) will understand your project's unique challenges and structure loans accordingly. Verify the lender maintains proper licensing in your state and check for complaints with local real estate investor groups.

The lender's ability to close on schedule matters more than a slightly lower rate, because missed deadlines cost you the entire deal.

Structure the deal to protect your equity

Never borrow more than 70% to 75% loan-to-value unless the deal's profit margins justify higher leverage. Keep enough cash reserves to cover at least three months of interest payments plus unexpected repair costs. This cushion prevents forced sales if your timeline extends. Request clear written terms that outline all fees, extension options, and prepayment penalties before signing. Lock in your exit strategy by pre-qualifying for refinancing or confirming buyer demand through local market analysis before you commit to the hard money loan.

Wrap-up and next steps

Understanding hard money loans gives you the power to compete in fast-moving real estate markets where traditional financing falls short. You've learned how these asset-based loans prioritize property value over credit scores, deliver funding in days instead of weeks, and provide flexibility that banks simply cannot match. The tradeoff comes through higher interest rates and shorter terms, but for time-sensitive deals or properties needing renovation, those costs often represent a smart investment rather than an obstacle.

Your next step depends on your current situation. If you're evaluating a specific property, calculate the total cost of hard money financing against your projected profit to confirm the numbers work. For investors building their portfolio, reach out to David Roa to discuss whether hard money fits your strategy or if alternative financing options like DSCR loans or commercial products better serve your goals. The right funding source transforms opportunities into closed deals and profitable investments.