What Is A Hard Money Loan? How It Works, Rates, Pros & Cons

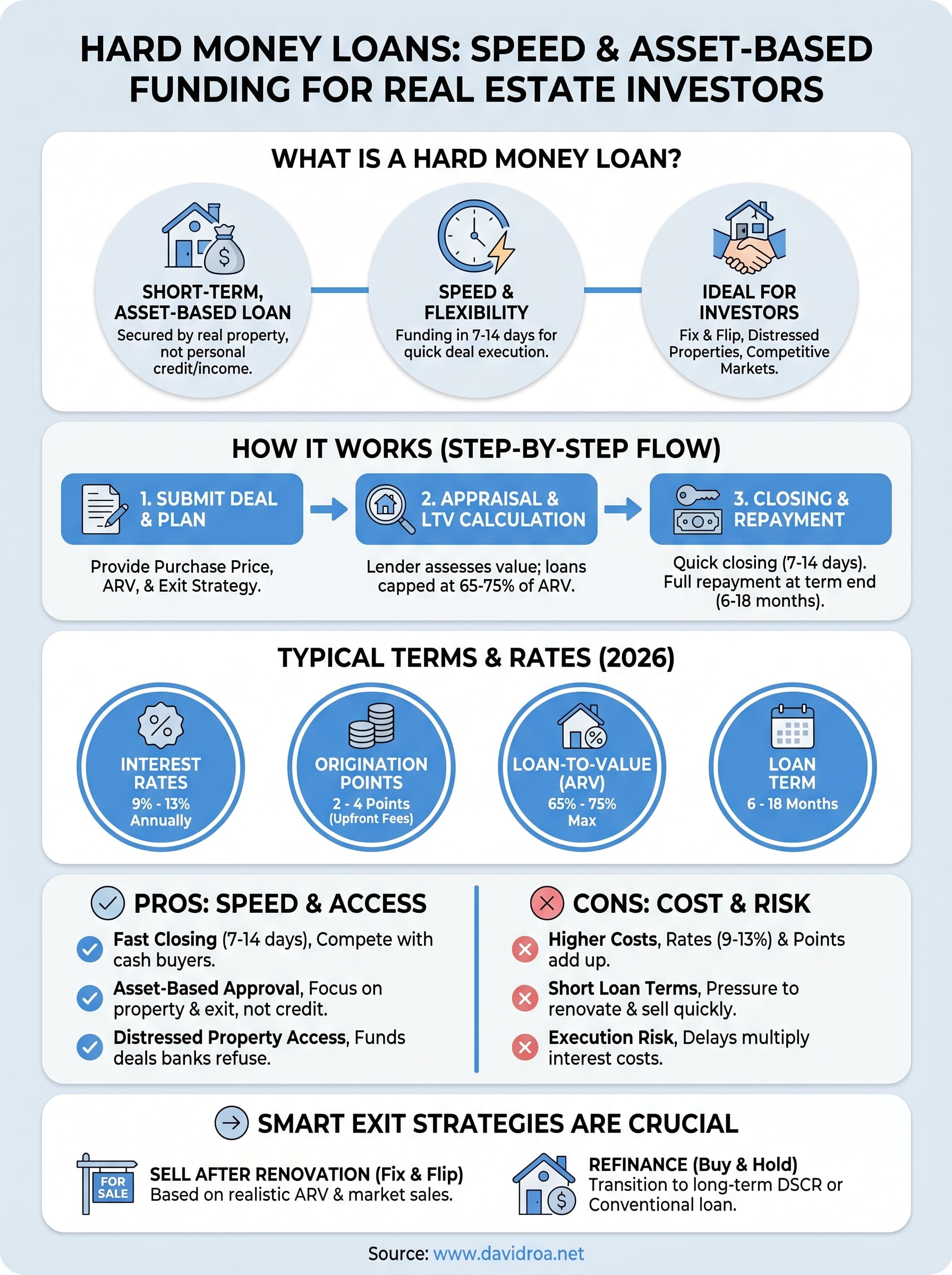

A hard money loan is a short-term, asset-based loan secured by real property, and it works nothing like a conventional mortgage. Instead of weighing your credit score and income history, hard money lenders focus on the property itself: its current value, its after-repair value, and how quickly you can execute your plan. For real estate investors who need to move fast on a deal, this distinction changes everything.

But speed and flexibility come with trade-offs. Interest rates are higher, loan terms are shorter, and the stakes feel different when a physical asset is on the line. Understanding exactly how hard money works, the mechanics, the costs, the risks, is what separates a smart investment from an expensive mistake. Knowing when to use this tool matters just as much as knowing what it is.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment deals over 25+ years. Hard money lending is one of the core products we offer real estate investors, whether they're flipping properties in the Chicago area or building rental portfolios nationwide. This article breaks down how hard money loans actually work, what rates and terms to expect, and the real pros and cons you should weigh before signing anything.

Why hard money loans exist

Hard money loans exist because conventional lending systems were built around a specific borrower profile: stable W-2 income, strong credit history, and properties in move-in condition. That profile fits a lot of homebuyers, but it excludes a substantial portion of the real estate investment market. When you're an investor trying to close on a distressed property in 10 days, a bank's 45-to-60-day approval process doesn't just slow you down. It kills the deal entirely.

The gap conventional lenders create

Banks and traditional mortgage lenders operate under federal regulatory frameworks that require thorough income verification, debt-to-income analysis, and strict property condition standards. Fannie Mae and Freddie Mac guidelines, for example, won't allow financing on properties that lack functioning utilities or have significant structural damage. If you're targeting a fixer-upper to flip, the property you most want to buy is often the exact property a conventional lender will refuse to finance. This gap is where hard money lending was built to operate.

The property you most want to buy is often the one a conventional lender refuses to touch.

That restriction creates a concrete problem for investors. Fix and flip investors need to purchase properties precisely because they're distressed and underpriced. Waiting for a bank to approve a loan on a property that fails standard appraisal conditions isn't a realistic strategy. Hard money lenders fill that void by evaluating the deal on its actual merits, including the after-repair value (ARV), rather than the property's current condition.

Why timing matters more than you think

Real estate markets move fast, especially when you're competing against other investors or dealing with motivated sellers who need a quick close. Cash buyers regularly dominate competitive investment markets, and a buyer who can close in two weeks consistently beats one who needs 60 days. Hard money loans give you a way to compete at that speed without liquidating your own capital.

This is part of why, when people ask what is a hard money loan, the answer connects directly to timing. It's short-term capital deployed quickly against the value of an asset, designed for situations where conventional financing is either too slow or structurally unavailable.

When your financial profile creates obstacles

Traditional lenders also struggle with non-traditional borrower profiles. Self-employed investors, those operating through multiple LLCs, or borrowers who take aggressive depreciation on rental properties often show low taxable income on paper even when their actual cash flow is strong. A bank sees that low income figure and declines the loan. Hard money lenders evaluate the situation differently. They focus on the asset value and your exit plan, which opens financing doors that conventional underwriting keeps shut regardless of how successful you actually are.

How hard money loans work step by step

The process moves faster than most borrowers expect. When you pursue a hard money loan, the entire transaction centers on the property's value and your exit strategy, not a lengthy review of your personal financial history. Most deals go from application to funded in 7 to 14 days, sometimes faster, which is exactly why investors reach for this tool when speed determines whether they win or lose a deal. Understanding what is a hard money loan really comes down to understanding this property-first underwriting process.

Submitting the deal

You start by bringing the lender a specific property with a clear plan. Hard money lenders want to know the purchase price, the estimated after-repair value (ARV), and how you intend to exit, whether that means selling after renovation or refinancing into a longer-term product. Unlike a bank, the lender is not building a thick file around your tax returns. They are evaluating whether the deal itself makes financial sense on its own merits.

The appraisal and loan-to-value calculation

Once the lender reviews your deal, they order an appraisal or conduct their own property assessment to establish value. Most hard money lenders cap their loan at 65% to 75% of the ARV, which protects them if the project stalls or the market shifts. That loan-to-value ratio determines exactly how much capital you can access, so knowing your ARV before you approach a lender puts you in a stronger negotiating position.

Your ARV estimate is the single number that determines how much a hard money lender will put on the table.

Closing and repayment

After the lender approves the loan, closing happens quickly, often within a week. You receive the funds, execute your renovation or acquisition plan, and then repay the full loan balance at the end of the term, typically 6 to 18 months out. That repayment usually comes from either selling the property or refinancing into a conventional loan.

Typical terms, rates, and fees in 2026

When you ask what is a hard money loan in practical terms, the numbers tell the real story. Hard money loans carry significantly higher costs than conventional mortgages, and those costs are structured differently. You pay for speed, flexibility, and access, and you need to factor every line item into your deal analysis before you commit to anything.

Interest rates in today's market

Hard money interest rates in 2026 typically run between 9% and 13% per year, depending on your lender, the property type, and your experience as a borrower. Some deals with stronger equity positions land closer to 9%, while higher-risk projects or less-experienced borrowers can push toward 13% or above. Because these are short-term loans, the annualized rate matters less than your total interest cost over the specific hold period, so calculate that number against your projected profit margin before you move forward.

A hard money loan that costs you $15,000 in interest on a deal netting $60,000 in profit is a better outcome than a missed deal that costs you nothing.

Origination points and other fees

Lenders typically charge 2 to 4 origination points up front, where one point equals 1% of the loan amount. On a $300,000 loan, that puts your origination cost between $6,000 and $12,000 at closing. Beyond points, you should also budget for appraisal fees, title insurance, and extension fees if your project runs longer than the original loan term, since extensions are common and cost real money.

Here is a quick reference for typical 2026 hard money loan terms:

| Term | Typical Range |

|---|---|

| Interest rate | 9% to 13% annually |

| Origination points | 2 to 4 points |

| Loan-to-value (based on ARV) | 65% to 75% |

| Loan term | 6 to 18 months |

| Closing timeline | 7 to 14 days |

Understanding these numbers upfront lets you build a deal that actually works rather than discovering a margin problem after you've already committed.

Pros, cons, and when they make sense

Understanding what is a hard money loan means weighing both sides of the equation with clear eyes. This product solves real problems for real estate investors, but it introduces costs and risks that can damage your returns if you use it in the wrong scenario. The decision always comes back to one question: does the deal justify the price of the capital?

Where hard money gives you a real edge

Hard money loans deliver advantages that no conventional mortgage product can match in competitive investment situations. The core benefits are straightforward.

- Speed: You can close in 7 to 14 days, which lets you compete directly with cash buyers.

- Asset-based approval: Your credit score and tax returns take a back seat to the property's value and your exit plan.

- Distressed property access: Lenders fund properties that conventional financing won't touch, which opens up the deals with the strongest margins.

- Flexible structures: Terms get negotiated deal by deal, giving you options that a bank's standardized products rarely allow.

Where hard money creates real risk

The cost structure and compressed timeline are where investors run into trouble. Interest rates between 9% and 13%, plus origination points, stack up fast if your project runs long.

- Renovation delays extend your hold period and multiply your interest expense beyond your original projections.

- Over-estimating ARV reduces your profit margin and can leave you underwater on the exit.

- Short loan terms of 6 to 18 months create pressure that punishes slow execution.

The biggest hard money mistakes happen when investors underestimate renovation timelines and overestimate the sale price.

When hard money actually makes sense

This product fits a specific investor profile: you have a clear exit strategy, a realistic renovation budget, and a target ARV supported by comparable sales. Fix and flip deals, bridge financing between acquisitions, and distressed property purchases are the situations where hard money earns its cost. If your timeline is uncertain or your margins are thin, a different financing structure will serve you better.

Alternatives and smart exit strategies

Knowing what is a hard money loan also means knowing when a different product serves your goals better. Hard money is a high-cost tool built for specific scenarios, and using it outside those scenarios will compress your margins or create unnecessary pressure on your timeline. Before you commit, compare it against the alternatives that might fit your situation more cleanly.

When a DSCR loan is a better fit

If you are buying a rental property rather than flipping one, a DSCR (Debt Service Coverage Ratio) loan gives you a longer timeline and lower rates without requiring traditional income documentation. Lenders qualify you based on the property's rental income relative to its debt obligations, not your W-2 or tax returns. For buy-and-hold investors, this structure removes the pressure of a short repayment window and lets you carry the asset profitably from day one.

A DSCR loan rewards you for buying cash-flowing properties, while a hard money loan rewards you for executing fast renovations.

Bridge loans are another option worth considering if you need short-term capital between transactions but want slightly more favorable terms than a traditional hard money product. Some lenders offer bridge products designed specifically for investors transitioning between a sale and a new acquisition.

Planning your exit before you borrow

Your exit strategy is not an afterthought. Lenders expect you to articulate it clearly before they fund the deal, and you should have it mapped out with specific numbers before you even apply. If your plan is to sell after renovation, anchor your ARV to recent comparable sales within the last 90 days in the same submarket, not wishful projections.

If your plan is to refinance into a conventional or DSCR loan after the renovation, confirm your eligibility for that product before closing on the hard money loan. Entering a deal without a confirmed exit is one of the fastest ways to lose money in real estate investing.

Next steps

You now have a complete picture of what is a hard money loan, including how it works, what it costs, and exactly when it makes sense versus when it doesn't. The decision to use hard money should always start with your deal's numbers: ARV, renovation budget, hold period, and exit strategy. If those numbers support the cost of the capital, this tool gives you access and speed that no conventional product can match.

Before you pursue your next deal, get those projections locked down and talk to a lender who understands investment-focused financing from the inside out. David Roa has spent over 25 years funding real estate investors across residential, commercial, and hard money products, with more than $150 million closed. If you have a deal in front of you and need to move fast, connect with David Roa and get a straight answer on what your financing options actually look like.