203k Loan Requirements: Credit Score, Down Payment, Docs

Buying a home that needs work can be a smart move, if you can finance both the purchase and the renovations without draining your savings. That's exactly what an FHA 203(k) loan is designed to do. But before you start picking out countertops, you need to understand the 203k loan requirements that determine whether you actually qualify. Credit score thresholds, down payment minimums, property standards, and paperwork all play a role, and missing even one requirement can stall your approval.

At David Roa, we've helped borrowers navigate 203(k) loans for over 25 years, closing on renovations that range from minor cosmetic updates to full structural rehabs. With more than $150 million funded across residential and investment lending, we've seen firsthand where applicants get tripped up and what it takes to get these loans across the finish line. Our team handles both Standard and Limited 203(k) programs, so we know the specific criteria lenders look for at every level.

This guide breaks down every requirement you'll need to meet in 2026: credit scores, down payments, debt-to-income ratios, property eligibility, contractor rules, and the full list of documents you should have ready. Whether you're a first-time buyer eyeing a fixer-upper or a homeowner planning a major renovation, you'll walk away knowing exactly where you stand and what steps to take next.

Why 203k loan requirements matter

The 203k loan requirements exist because this program is more complex than a standard mortgage. You're not just borrowing money to buy a home; you're financing a purchase and a renovation under a single loan, which means the lender, the FHA, your contractor, and sometimes a HUD consultant all need to be aligned. Missing one eligibility criterion can delay your closing by weeks or, in a worst-case scenario, cost you the deal entirely. Understanding what the program demands upfront is the most practical way to protect your time and your money.

The FHA 203(k) program is government-backed, meaning lenders follow strict guidelines set by the U.S. Department of Housing and Urban Development, not just their own internal policies.

Two loan programs, two sets of rules

The FHA offers two versions of this product, and which one you qualify for depends on the scope of your renovation. The Limited 203(k) caps renovation costs at $75,000 and covers non-structural repairs like updating kitchens, replacing flooring, or improving energy efficiency. The Standard 203(k) handles larger projects, including structural repairs, room additions, and full rehabilitation work, and it requires a HUD-approved 203(k) consultant to oversee the entire renovation process from bid to completion.

Choosing the wrong version creates avoidable setbacks. If you apply for a Limited 203(k) but your project actually requires structural work, your lender will redirect you to the Standard program, which brings additional documentation and third-party oversight. Identifying your correct program track before you apply saves you a full round of rework and keeps your closing timeline on track.

The real cost of skipping the details

Many borrowers approach renovation loans the same way they handle a conventional purchase mortgage, and that assumption creates problems. The requirements include property standards, contractor approvals, and draw schedules that simply don't apply to a standard home loan. If your contractor isn't on the approved list or your property fails FHA minimum property standards, you'll face delays that push back your closing date and put pressure on your purchase contract.

Lenders also scrutinize renovation budgets carefully. Cost overruns during the project are not automatically rolled into the loan, so if your contractor's final costs exceed the approved amount, you cover the difference out of pocket. Getting the requirements right from the beginning means building a realistic budget, selecting a qualified contractor early, and having your paperwork organized before you submit a single form. The borrowers who close fastest are the ones who treat the documentation process with the same attention they give to the renovation plan itself.

Credit score and down payment requirements

The 203k loan requirements around credit and down payment are more accessible than most borrowers expect, but they're still firm. Your credit score directly controls both your eligibility and the size of your required down payment, so knowing exactly where you stand before you apply saves you from surprises at the lender's desk.

Minimum credit score thresholds

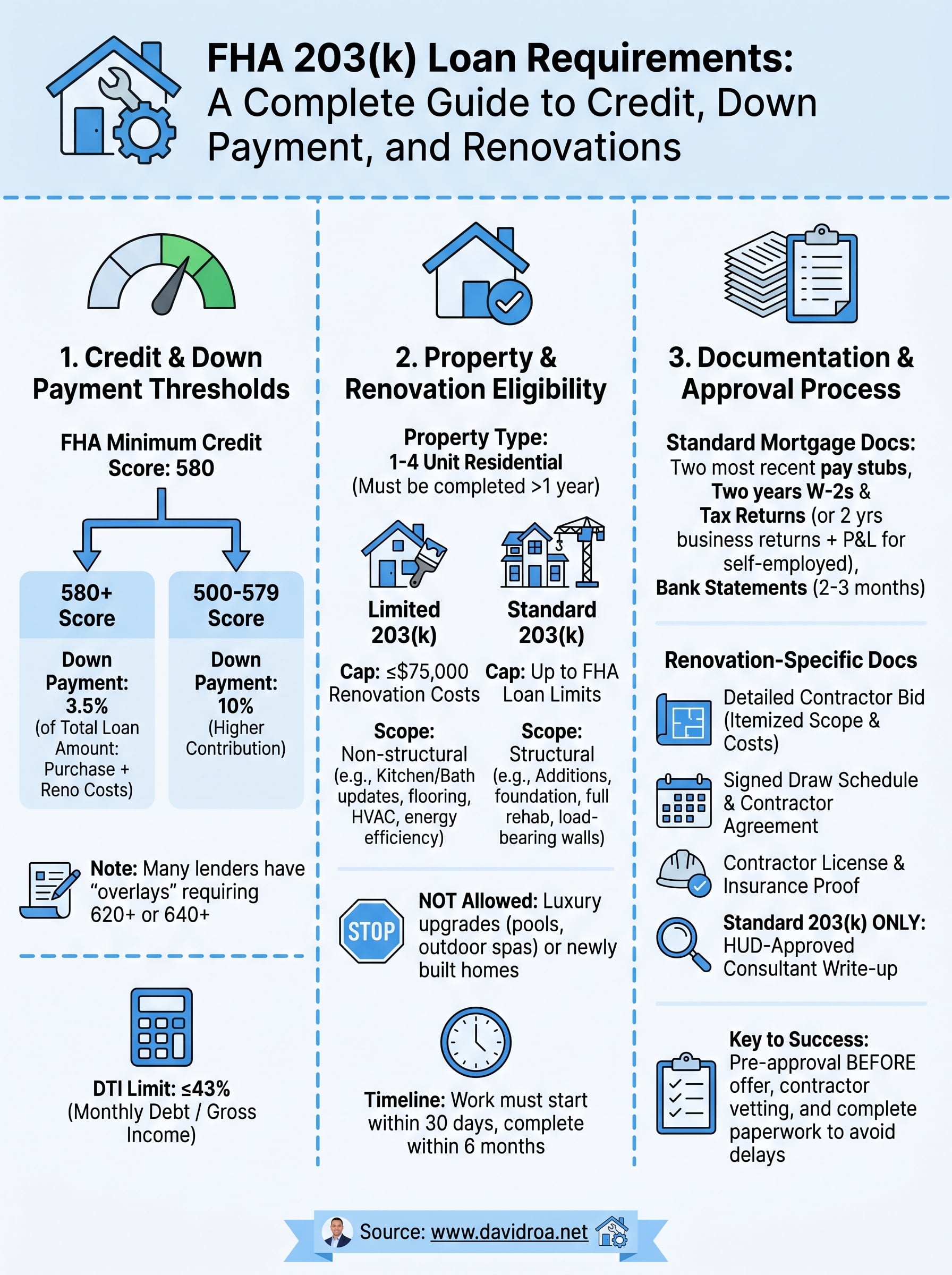

FHA sets a minimum credit score of 580 to qualify for the standard 3.5% down payment on a 203(k) loan. If your score falls between 500 and 579, you're still eligible under FHA guidelines, but your required down payment jumps to 10%. Most lenders who offer 203(k) loans apply their own overlays on top of FHA minimums, which means many require a 620 or 640 score in practice, even though FHA allows 580.

If your credit score is below 620, contact a lender before you find a property. Knowing your actual approval threshold upfront lets you plan your timeline and avoid wasted steps.

You should pull your credit report from AnnualCreditReport.com before you apply. Disputed accounts, collections, and high credit utilization can each drag your score down in ways that are fixable with a few weeks of attention.

Down payment and DTI limits

At a 580 or higher credit score, your minimum down payment is 3.5% of the total loan amount, which includes both the purchase price and the estimated renovation costs combined. On a $250,000 acquisition with $50,000 in renovation work, that means you need $10,500 minimum to close, not counting closing costs.

Your debt-to-income ratio must stay at or below 43% in most cases, though some lenders allow up to 50% with strong compensating factors like significant cash reserves. Monthly obligations including the new mortgage payment, renovation escrow, car loans, and credit card minimums all count toward that number, so calculate your full picture before you apply.

Property and renovation rules for 203k loans

Not every home and not every renovation project qualifies under this program. The 203k loan requirements include specific standards for both the property you're buying and the work you plan to complete, and understanding these rules before you make an offer protects you from locking into a deal that the program won't support.

Which properties qualify

The home must be a one-to-four-unit residential property that has been completed for at least one year. Single-family homes, townhouses, and eligible condominiums all qualify, but the condo must be in an FHA-approved project. You cannot use a 203(k) loan on a newly built home or a commercial property.

If you're purchasing a mixed-use building where the commercial portion is small and the primary use is residential, talk to your lender before assuming the property is ineligible.

The property also must meet FHA minimum property standards after all renovations are complete. That means functional plumbing, electrical systems, roofing, and structural soundness. If the home can't meet those standards even after the planned work, the lender won't approve the loan.

What renovations are and aren't allowed

Your renovation scope depends on which program you're using. The Limited 203(k) covers non-structural improvements like HVAC replacement, kitchen updates, bathroom remodels, flooring, and energy-efficiency upgrades. The Standard 203(k) opens the door to structural repairs, room additions, foundation work, and full property rehabilitation.

Neither program allows luxury upgrades under FHA guidelines. Swimming pools, outdoor spas, and purely cosmetic features that don't contribute to the home's livability or habitability are off the table. All work must begin within 30 days of closing and be completed within six months of the loan closing date, so your contractor's timeline needs to be realistic from day one.

Documentation and underwriting requirements

The 203k loan requirements extend well beyond credit scores and property standards. Your documentation package needs to cover two distinct tracks: the standard mortgage underwriting file and a second layer of renovation-specific paperwork that a conventional purchase loan never touches. Getting both sets of documents organized before you submit your application is the single most effective way to avoid underwriting delays.

Income and asset documents

Your lender will verify income and assets using the same framework they apply to any FHA loan. You'll need your two most recent pay stubs, W-2s from the past two years, and federal tax returns for the same period. Self-employed borrowers need to provide two years of business returns along with a year-to-date profit and loss statement. Bank statements covering the last two to three months confirm that your down payment and cash reserves are sourced and seasoned.

If any large deposits appear in your bank statements, have a written explanation and supporting documentation ready before your lender asks for it. Unexplained deposits slow underwriting down significantly.

Your debt obligations, including car loans, student loans, and credit card balances, all get factored into your DTI calculation, so your lender will pull a full credit report and may request explanation letters for any late payments, collections, or recent credit inquiries.

Renovation-specific paperwork

This is where the 203(k) documentation process separates itself from a standard purchase loan. You need a detailed contractor bid that itemizes every scope of work, including materials, labor costs, and a projected timeline. For the Standard 203(k), a HUD-approved consultant prepares a formal write-up of the work that both the lender and FHA review before approval. The Limited program skips the consultant but still requires a signed contractor agreement and a completed draw schedule before your loan can close.

Your contractor must also provide proof of licensing, insurance, and in many cases a signed borrower-contractor agreement that outlines payment terms tied directly to completed renovation milestones.

How to apply and avoid 203k loan delays

The application process for a 203(k) loan moves in a specific sequence, and skipping steps or submitting incomplete files is the most common reason closings get pushed back. Once you understand the order of operations, you can move through underwriting without stalling your renovation timeline.

Start with the right lender

Not every FHA-approved lender offers the 203(k) program. Your first step is finding a lender who actively originates these loans and has a recent track record of closing them, because inexperienced lenders create delays that aren't your fault but become your problem. Get your pre-approval letter before you make any offers, so you already know your credit score clears the threshold, your DTI falls within range, and your down payment is documented and ready.

Bringing a lender into the process before you find a property gives you a realistic renovation budget ceiling before you spend time writing offers on homes you can't finance.

Meeting the full list of 203k loan requirements is much smoother when your lender guides the process from the beginning rather than reacting to problems after the fact.

Keep your contractor on track

Contractor delays are the leading cause of 203(k) closings running over schedule after the loan is already approved. Before you submit your application, confirm that your contractor is licensed, insured, and willing to sign a borrower-contractor agreement tied to a draw schedule. For Standard 203(k) loans, your HUD consultant needs to sign off on every draw request, so your contractor must be prepared to document completed work at each phase.

Set a clear start date in your contractor agreement and confirm their availability before closing. Work must begin within 30 days of closing and finish within six months, so a contractor who is overextended can push you out of compliance even if your loan closes on time. Staying ahead of that timeline starts with the conversation you have before you submit a single document.

Next steps

You now have a complete picture of what the 203k loan requirements demand across every stage of the process: credit score minimums, down payment thresholds, property standards, renovation rules, documentation, and closing timelines. The borrowers who close fastest are the ones who get their lender, contractor, and paperwork aligned before they make an offer, not after.

Your next move is simple. Pull your credit report, calculate your debt-to-income ratio, and identify which program, Limited or Standard, matches your renovation scope. Once you have those answers, you're ready to have a real conversation with a lender who knows this program inside and out.

David Roa has spent over 25 years closing renovation loans for buyers and investors across the Chicago area and beyond. If you're ready to move forward, connect with David Roa and get your 203(k) pre-approval started today.