Can You Rent Out an FHA Home? Rules, Timing, Exceptions

You bought your home with an FHA loan, and now circumstances have changed. Maybe you got a job offer in another city, or you're ready to move into a bigger place. Either way, you're wondering: can you rent out an FHA home without breaking the rules? The short answer is yes, but the timing and conditions matter more than most borrowers realize.

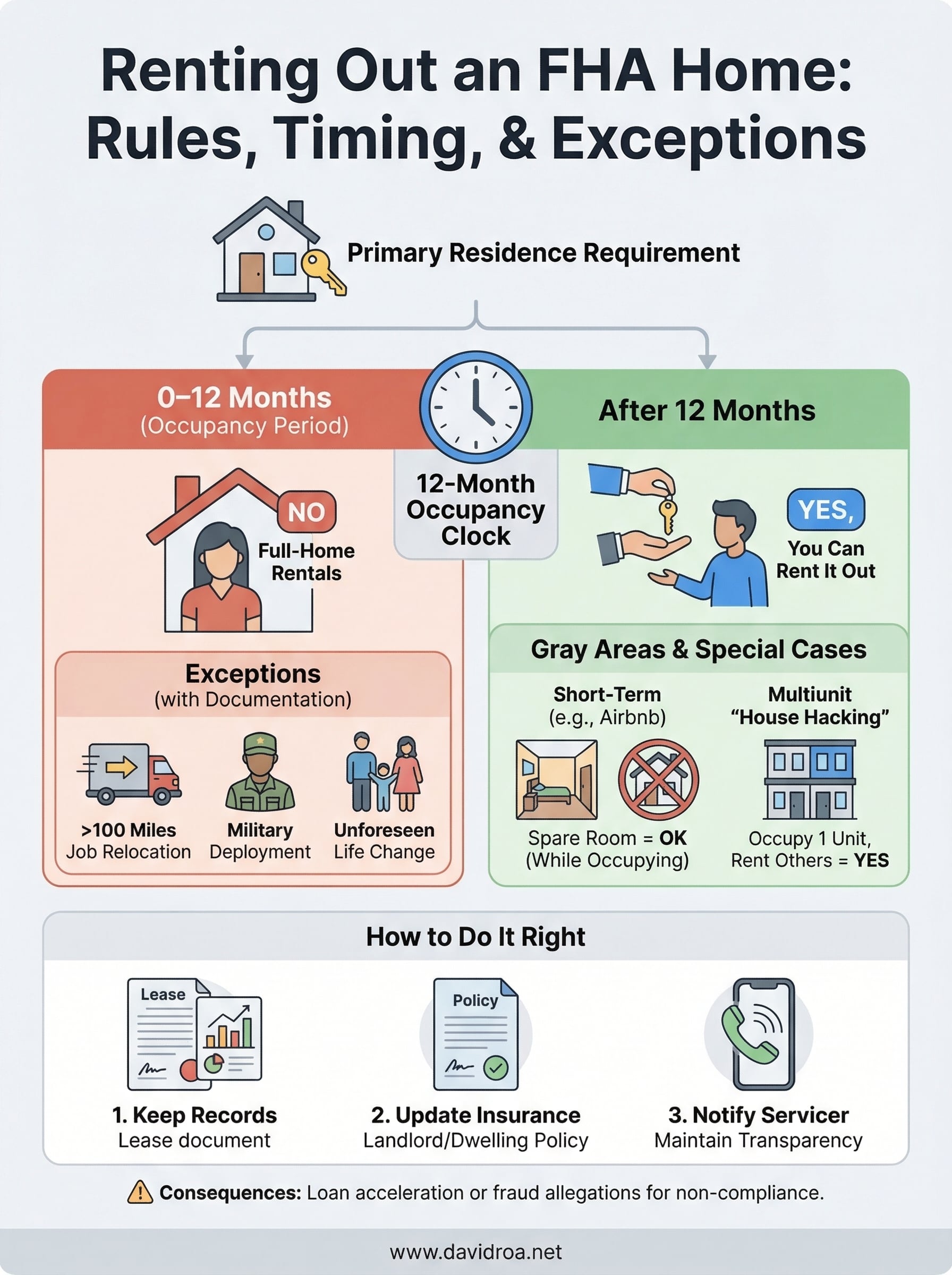

FHA loans come with a primary residence occupancy requirement that you need to satisfy before converting the property to a rental. Ignore this requirement, and you could face serious consequences, including loan acceleration or fraud allegations. The good news is that HUD provides clear guidelines on when and how you can legally make the switch.

With over 25 years in mortgage lending and more than $150 million funded, I've walked hundreds of FHA borrowers through exactly this question at David Roa. As someone who also invests in real estate myself, I understand the pull to turn a property into an income-producing asset. Below, I'll break down the occupancy rules, timing thresholds, and recognized exceptions that determine whether you can rent out your FHA-financed home, and how to do it the right way.

What FHA rules say about renting

The FHA loan program exists to help people buy primary residences, not investment properties. When you close on an FHA loan, you sign a certification stating that you intend to occupy the property as your principal residence within 60 days of closing and continue living there for at least one year. That commitment is the foundation of every rule that follows when you ask whether you can rent out an FHA home legally. Skipping past that foundation without understanding it creates real legal and financial exposure.

HUD Handbook 4000.1 defines owner-occupancy as a core requirement that must be satisfied before any rental arrangement becomes permissible under the FHA loan program.

The owner-occupancy requirement explained

This rule comes directly from HUD Handbook 4000.1, the official FHA Single Family Housing Policy Handbook. It states that a borrower must occupy the property as their principal residence for a minimum of 12 months after closing. During that period, you cannot legally convert the home into a full rental. The lender, the FHA, and HUD all rely on your signed occupancy certification to verify your intent at the time of purchase, and that certification carries legal weight.

Lenders treat this requirement seriously because FHA loans carry government-backed mortgage insurance through the Federal Housing Administration. That insurance program is designed specifically for owner-occupants, not landlords or investors. If you misrepresent your occupancy intent at closing to secure the lower down payment and favorable rates that FHA loans offer, that misrepresentation qualifies as mortgage fraud under federal law and can result in the lender demanding immediate repayment of the full loan balance.

What "principal residence" actually means

Your principal residence is the address where you live most of the year, receive mail, file your taxes, and conduct your daily life. HUD does not interpret this loosely. The agency expects you to demonstrate that the FHA-financed property is genuinely where you live, not a property you planned to convert into a rental from day one. Living there means using it as your actual home, not just maintaining a nominal presence to satisfy paperwork.

Lenders and underwriters watch for occupancy red flags that suggest a borrower never intended to live in the home. These include purchasing a property far from your current workplace, buying a home that far exceeds your household size, or applying for an FHA loan while already owning a nearby comparable property. Any of these patterns can trigger a deeper review of your occupancy intent both before and after closing.

Why the rules exist and who enforces them

The FHA program lowers the barrier to homeownership by offering low down payments and flexible credit requirements, but those benefits come with conditions. HUD designed them for buyers who need affordable housing, not for investors looking to use government-backed financing as a cheaper path to building a rental portfolio. This is why HUD and your mortgage servicer can request occupancy verification at any point during the loan term, and why inconsistencies between your stated intent and actual behavior draw scrutiny from auditors and lenders alike.

When you can rent out an FHA home

The clearest answer to can you rent out an FHA home is this: after you've lived in the property as your primary residence for at least 12 months, you can rent it out without violating FHA rules. Once you satisfy that one-year threshold, you're free to lease the home to tenants, move into a new property, and even pursue another FHA loan under certain conditions.

After the 12-month occupancy period

Once 12 months of owner-occupancy have passed, nothing in the FHA loan program prevents you from converting the property to a rental. You don't need to refinance out of the FHA loan first, and you don't need to notify your servicer before signing a lease. Your mortgage terms stay in place, and you simply transition from owner-occupant to landlord. At that point, the rental income can also help you qualify for a new mortgage if you document it properly with a signed lease agreement and evidence of security deposit receipt.

Your lender will want to see at least a one-year signed lease before counting rental income toward a new loan application, so organize your paperwork before you apply.

When a legitimate life change forces you to move early

Sometimes life moves faster than a 12-month clock. A job relocation, a family emergency, or a major household change can force you out of the home before you hit the one-year mark. HUD recognizes that circumstances change, and lenders can grant exceptions when you document a genuine, unforeseen reason for the move.

The key word is documentation. You need to show your servicer a clear paper trail, whether that's a job transfer letter, a divorce decree, or a physician's statement, that explains why you couldn't maintain the occupancy requirement you committed to at closing. Without that evidence, your lender has no basis to approve the early transition.

Exceptions and gray areas lenders watch

Even after you understand the 12-month rule, edge cases and gray areas can complicate whether you can rent out an FHA home legally. Lenders and HUD auditors don't just look at the calendar; they examine your intent at the time of closing and your behavior after you moved in. Knowing where lenders draw the line helps you stay on the right side of it.

Job relocation and military deployment

HUD formally recognizes certain qualifying events that allow you to vacate the property before completing 12 months of occupancy without triggering a fraud finding. A documented job transfer more than 100 miles from the property and active military deployment orders are two of the strongest grounds for an early exception. If either applies to you, contact your servicer immediately, provide the required documentation, and get written confirmation before you sign any lease.

Keep copies of every document you submit to your servicer when requesting an occupancy exception, because gaps in your paper trail can become costly problems during an audit.

An unexpected household change, such as a sudden increase in family size that makes the property genuinely insufficient, can also support an early approved departure. However, servicers evaluate each case individually, and no exception is automatically granted without clear evidence that the move was unplanned and unavoidable.

When intent becomes the issue

The gray area lenders watch most closely involves borrower intent at closing. If you buy a home with an FHA loan and rent it out within weeks, your lender may flag the transaction as an occupancy misrepresentation regardless of how you explain it afterward. Patterns like purchasing far from your workplace, buying a property that exceeds your household size, or showing no utility activity at the address after closing all signal intent problems that can expose you to a formal investigation and loan acceleration.

Short-term rentals and multiunit house hacking

Two scenarios come up frequently when borrowers ask can you rent out an FHA home: renting through short-term platforms like Airbnb and using an FHA loan on a multiunit property to cover your mortgage costs. Both strategies are possible under FHA rules, but each comes with specific conditions you need to understand before you list a room or sign a lease.

Short-term rentals and the occupancy line

Short-term rental platforms present a real gray area. Renting the entire home on a short-term basis while you live elsewhere violates your occupancy commitment, full stop. However, renting a spare room while you continue living in the property as your primary residence is generally acceptable because you're still occupying the home. HUD's concern is whether the property functions as your actual residence, not whether a guest occasionally uses a room.

Once you move out and convert the home entirely to a short-term rental, you face the same 12-month occupancy requirement that applies to any other rental arrangement.

Your mortgage servicer may not audit your short-term rental activity directly, but inconsistencies like utility records showing minimal personal use or a business address registered at the property can raise occupancy red flags during a routine review.

Multiunit properties and house hacking

FHA loans allow you to purchase a property with up to four units, as long as you occupy one of those units as your primary residence. This makes FHA financing one of the most accessible tools for house hacking because you can collect rent from the other units from day one without any conflict with your occupancy requirement. Your rental income from the non-owner-occupied units can even help you qualify for the loan during underwriting.

With this approach, you reduce your monthly housing cost while building equity in an income-producing property, all with a down payment as low as 3.5 percent.

How to rent your FHA home the right way

Once you confirm you can rent out an FHA home legally, the next step is executing the transition cleanly. Cutting corners on documentation or skipping important notifications creates liability that can surface months later when you least expect it. Doing this right the first time protects your loan status and positions you as a credible landlord from day one.

Keep your paperwork in order

Your signed lease agreement is the most important document in this process. Before you accept any tenant, make sure the lease reflects the full rental term, the monthly rent amount, and the security deposit collected. Lenders reviewing a future mortgage application will request this documentation to count your rental income, so gaps or informal arrangements work against you.

Store your lease, security deposit receipt, and any occupancy exception correspondence in one place so you can produce them quickly if your servicer requests verification.

Beyond the lease, track your rental income and expenses carefully from the start. The IRS treats rental income as taxable, and maintaining clear records simplifies your tax filing while also demonstrating to future lenders that the property functions as a legitimate income-producing asset.

Notify your insurance provider and servicer

Your homeowner's insurance policy was written for an owner-occupant, not a landlord. Once you move out and rent the property, you need to switch to a landlord or dwelling policy that covers tenant-related risks and liability. Failing to update your coverage means your current policy could deny a claim after the rental begins.

Contact your mortgage servicer as well, not because FHA requires formal approval after the 12-month period, but because some servicer agreements include notification clauses. A quick call or written notice keeps the relationship transparent and prevents any confusion about occupancy status down the line.

Final takeaways

So, can you rent out an FHA home? Yes, once you've lived in the property as your primary residence for at least 12 months, you can rent it out without violating FHA rules. Life changes like job relocations or military deployments can justify an earlier move, but you need clear documentation to support any exception request. Multiunit properties let you collect rent from day one as long as you occupy one unit yourself, and renting a spare room while you remain in the home stays within your occupancy commitment.

The biggest mistakes happen when borrowers move too fast or skip the paperwork. Updating your insurance, organizing your lease documents, and tracking rental income from the start keeps your loan in good standing and positions you well for your next purchase. If you want to talk through your specific situation, reach out to David Roa for direct, experience-backed guidance.