Conventional Loan Vs FHA Loan: Pros, Cons, And Requirements

Choosing between a conventional loan vs FHA loan is one of the first real decisions you'll face as a homebuyer, and it's one that directly affects your down payment, monthly costs, and long-term equity. Both options can get you into a home, but they work differently under the hood. The right pick depends on your credit profile, savings, and financial goals, not on which one sounds better on paper.

After more than 25 years as a mortgage broker and senior loan officer, and having funded over $150 million in loans, I've walked thousands of buyers through this exact comparison. At David Roa, we work with both conventional and FHA products daily, so we see firsthand how each one plays out for different borrower situations, from first-time buyers with limited savings to experienced homeowners looking to optimize their terms.

This article breaks down the pros, cons, and requirements of each loan type side by side. By the end, you'll have a clear understanding of which option aligns with your finances and what to expect during the approval process, no guesswork involved.

Why the FHA vs conventional choice matters

The loan type you choose does more than determine your interest rate. It shapes your entire borrowing experience, from how much you bring to closing to how long you pay for mortgage insurance. Most buyers focus on the monthly payment, but the conventional loan vs fha loan decision reaches deeper than that. It determines what properties you can buy, how your credit score is weighted, and how much flexibility you have when your financial situation shifts down the road. Getting this choice right from the start saves you real money and frustration later.

How this decision affects your total loan cost

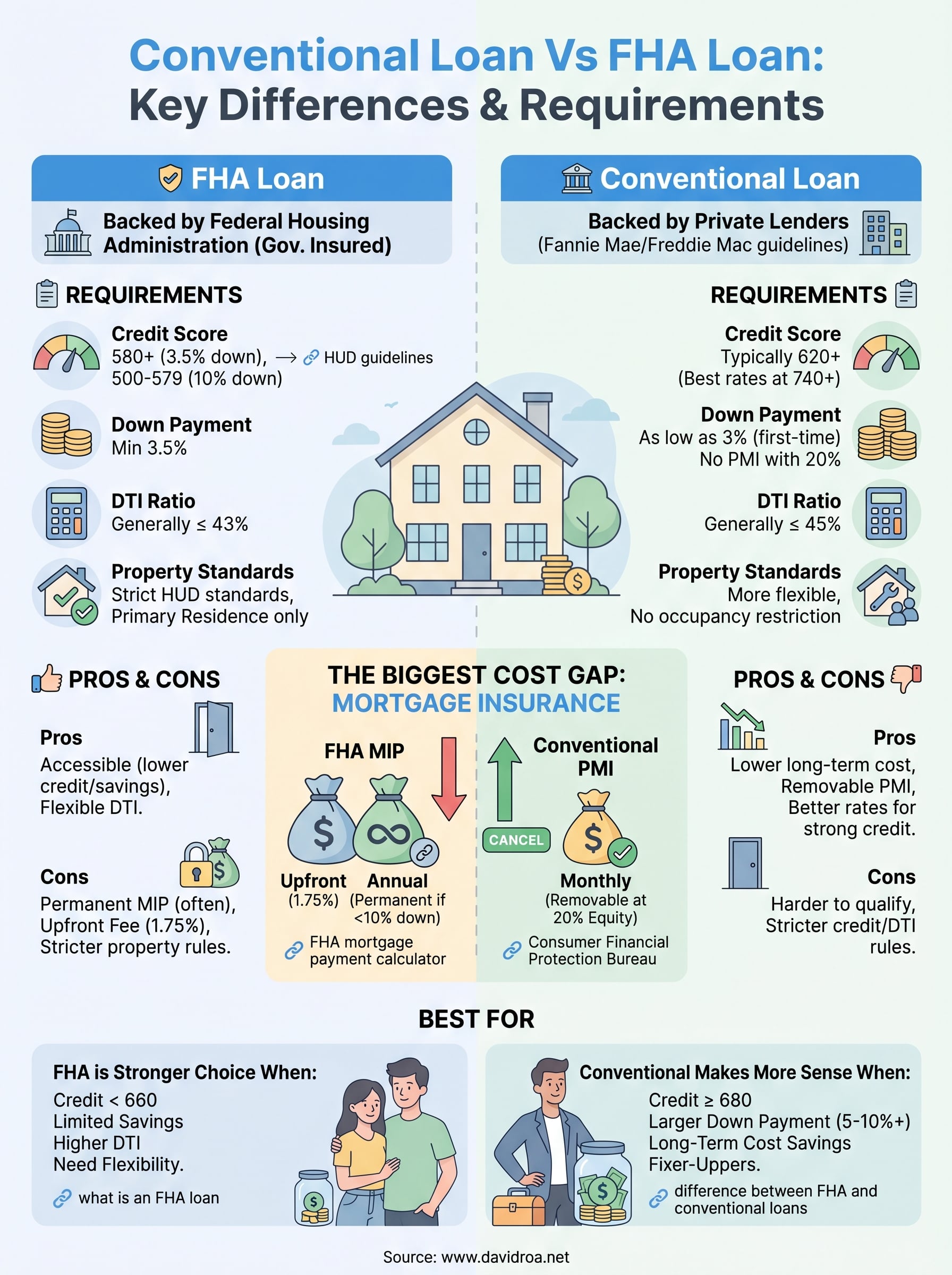

Your loan type directly controls several cost layers that stack up over the life of the loan. FHA loans carry a mandatory mortgage insurance premium (MIP) that includes an upfront charge of 1.75% of the loan amount at closing, plus an annual premium rolled into your monthly payment. In most cases, that annual MIP stays for the entire life of the loan if your down payment is under 10%. Conventional loans require private mortgage insurance (PMI) only when your down payment falls below 20%, and once you reach 20% equity in your home, you can request its removal.

Choosing FHA when you actually qualify for conventional could cost you thousands in insurance premiums that never go away.

Consider a buyer purchasing a $350,000 home with 3.5% down on an FHA loan. They pay the upfront MIP at closing and then carry monthly premiums for the full 30-year term. That same buyer with a 720 credit score using a 3% down conventional loan may pay a lower PMI rate with a clear path to canceling it once equity builds. The exact numbers shift based on your credit profile and lender, but the structure of each program determines your long-term cost exposure in ways the interest rate alone does not show you.

The impact on your eligibility and options

Your credit score and debt-to-income ratio determine which loan you can actually access, not just which one looks better on paper. FHA loans accept lower credit scores, starting at 580 with 3.5% down and going as low as 500 with a 10% down payment, according to HUD guidelines. Conventional loans typically require a minimum score of 620, and the best pricing becomes available as your score climbs toward 740 and above. If your credit has taken some hits, FHA gives you a way in. If your credit is strong, conventional usually rewards you for it.

Loan limits also shape your options. The Federal Housing Finance Agency sets conforming loan limits each year for conventional loans. For 2025, the baseline limit is $806,500 for a single-family home in most U.S. counties. FHA has its own county-level limits as well. If you are buying in a higher-cost market or targeting a more expensive property, these caps directly affect which program works for your purchase.

Property condition is a factor many buyers overlook. FHA loans require the home to meet minimum property standards set by HUD, which means a distressed property or one needing significant repairs may not qualify. Conventional loans carry more flexible property standards in most cases, giving you more room if you are targeting a fixer-upper or a property in a non-standard condition. Knowing these constraints before you start making offers prevents deals from falling apart late in the process.

FHA loan requirements, pros, and cons

FHA loans are backed by the Federal Housing Administration, which means the government insures the lender against default. That guarantee is what allows lenders to approve borrowers with lower credit scores and smaller down payments than they would typically accept on conventional products. If your credit history has gaps or your savings are limited, FHA is often the program that gets you to the closing table when other options would not.

What you need to qualify for an FHA loan

The minimum credit score to qualify with a 3.5% down payment is 580, according to HUD guidelines. If your score falls between 500 and 579, you can still qualify but the required down payment jumps to 10%. Your debt-to-income ratio generally needs to stay at or below 43%, though some lenders will go higher with compensating factors like strong cash reserves or a larger down payment.

Beyond your credit and income profile, FHA has a few structural requirements most buyers don't expect. The property you're purchasing must meet HUD's minimum property standards, so homes with structural issues, safety hazards, or significant deferred maintenance may not clear the appraisal. You are also required to occupy the property as your primary residence, which rules out FHA for investment properties or vacation homes.

Pros and cons of FHA loans

When comparing a conventional loan vs FHA loan, the biggest draw of FHA is accessibility. Lower credit thresholds and the 3.5% down payment requirement open the door for buyers who would otherwise need years more of credit rebuilding or saving. Lenders also tend to be more flexible on debt-to-income ratios, which helps buyers carrying student loans or other recurring obligations.

The accessibility FHA offers at the front end often comes with a real cost you carry for the full loan term.

The main drawback is mortgage insurance. You pay an upfront MIP of 1.75% at closing, and if your down payment is under 10%, the annual premium stays on your loan for its entire life. There is no automatic removal tied to equity the way PMI works on conventional loans. That permanent insurance cost is what makes FHA the right fit for some borrowers and the wrong call for others, and it is worth running the numbers before you commit.

Conventional loan requirements, pros, and cons

Conventional loans are not backed by any government agency. Private lenders issue them, and they follow guidelines set by Fannie Mae and Freddie Mac. Because there is no government guarantee behind the loan, lenders set stricter eligibility standards than FHA programs typically require. That higher bar is exactly what makes conventional loans more rewarding for borrowers who meet it.

What you need to qualify for a conventional loan

Your credit score is the first filter a conventional lender runs. Most programs start at a minimum of 620, but your actual pricing improves significantly as your score moves higher. Borrowers with scores at 740 or above typically access the best interest rates and lowest PMI tiers available. If your score sits below 700, you will still qualify, but expect higher costs built into your rate or insurance.

Your debt-to-income ratio generally needs to stay at or below 45%, though some automated underwriting approvals will go slightly higher depending on your full financial picture. Lenders also look at your employment history, income documentation, and reserves. For down payment, conventional loans accept as little as 3% down for first-time buyers through certain programs, though putting down 20% eliminates private mortgage insurance entirely. One structural advantage over FHA is that conventional loans place no occupancy restriction tied to government insurance rules, which gives investors and multi-unit buyers more flexibility depending on the loan product.

If your credit is strong and you have at least 5% to 10% to put down, conventional is almost always worth running the numbers on first.

Pros and cons of conventional loans

When you stack up the conventional loan vs fha loan comparison, the primary advantage of conventional is the long-term cost structure. PMI on a conventional loan is not permanent. Once your loan-to-value ratio drops to 80%, you can request removal, and lenders are required to cancel it automatically at 78% based on the original amortization schedule under the Homeowners Protection Act, as outlined by the Consumer Financial Protection Bureau. That exit path from insurance costs saves real money over time.

The tradeoff is that qualifying is harder. Borrowers with recent credit problems, limited credit history, or higher debt loads will find conventional guidelines less forgiving. FHA exists specifically to serve those situations, but if your profile is clean, conventional gives you more favorable long-term terms with a clear path to eliminating extra monthly costs.

Cost differences that change your monthly payment

When you compare a conventional loan vs FHA loan, the interest rate gets most of the attention, but it is rarely the number that causes the biggest difference in your monthly payment. The real gap lives in mortgage insurance, loan structure, and how your credit score affects pricing across both programs. Understanding where each dollar goes helps you make a comparison that reflects your actual costs, not just the rate on the term sheet.

Mortgage insurance: the biggest cost gap

FHA mortgage insurance hits you twice. You pay an upfront premium of 1.75% of the loan amount at closing, which on a $300,000 loan adds $5,250 to your costs before your first payment. Then you carry an annual premium that typically runs between 0.45% and 1.05% depending on your loan term and down payment, and it stays on your loan for the full term if you put down less than 10%.

On a 30-year FHA loan with less than 10% down, you could pay mortgage insurance for the entire life of the loan with no ability to remove it early.

Conventional PMI works differently. The rate varies by lender and credit score, typically ranging from 0.2% to 2% annually, and you can request removal once you hit 20% equity. At 78% loan-to-value based on the original amortization schedule, your lender must cancel it automatically under the Homeowners Protection Act, as detailed by the Consumer Financial Protection Bureau. That built-in exit makes conventional insurance far less expensive over time for buyers who build equity at a steady pace.

Interest rate and down payment tradeoffs

Credit score tiers shape your conventional interest rate more aggressively than they affect FHA pricing. FHA rates tend to stay relatively flat across a wider score range because the government guarantee absorbs more of the lender's risk. With conventional loans, your rate can shift meaningfully between a 680 and a 740 score, sometimes enough to offset the PMI savings if your score sits in the lower ranges.

Your down payment also changes the cost math in both directions. Putting down more on a conventional loan lowers your PMI rate and can improve your interest tier. On FHA, a larger down payment reduces your annual MIP rate slightly, but it does not eliminate the upfront premium or give you an early exit from ongoing insurance unless you put down at least 10%, which extends the MIP removal to 11 years rather than the full loan term.

How to choose the right loan for your situation

There is no single answer that works for every buyer in the conventional loan vs FHA loan comparison. The right choice depends on where you stand today with your credit score, savings, and income, and what your financial picture looks like over the next five to ten years. Running both scenarios with actual numbers for your specific situation will tell you more than any general rule of thumb.

When FHA is the stronger choice

FHA makes the most sense when your credit score falls below 660 or when you have limited savings and need the lowest possible down payment to get into a home. If your score sits in the 580 to 620 range, conventional lenders will either decline your application or price the loan at a level that wipes out any insurance savings. FHA gives you stable, government-backed access to financing at a rate structure that does not punish lower credit tiers as severely.

If you are early in your credit journey or recovering from a financial setback, FHA often gets you into a home years sooner than waiting to qualify for conventional.

FHA also works well when your debt-to-income ratio is higher than 43% and you have compensating factors a lender can document, such as strong cash reserves or a co-borrower. Buyers who plan to refinance within five to seven years can use FHA to get in now and exit the mortgage insurance requirement later by refinancing into a conventional loan once their equity and credit score improve.

When conventional makes more sense

Conventional becomes the smarter option when your credit score is 680 or higher and you can put at least 5% to 10% down. At that threshold, your PMI rate will likely be lower than FHA's annual premium, and you have a clear path to canceling it once you build equity. Borrowers with scores above 740 typically see the most dramatic cost advantage over FHA because conventional pricing rewards strong credit directly through better rate tiers.

You should also lean toward conventional if you are buying a property that needs work or one that might not meet FHA's minimum property standards. Conventional appraisals carry fewer property condition requirements, which gives you more flexibility when the home is not move-in ready.

Next steps

The conventional loan vs FHA loan decision comes down to your specific numbers, not a general preference. If your credit score is strong and you have some savings to put down, conventional typically delivers lower long-term costs with a clear exit from mortgage insurance. If your score needs work or your savings are limited, FHA gives you a reliable path to homeownership without waiting years to qualify for stricter programs.

Before you apply for either product, pull your credit report, calculate your debt-to-income ratio, and get a realistic picture of what you can bring to closing. Those three numbers will narrow your options fast and tell you where to focus your preparation.

Ready to run the actual numbers on your situation? Work with a mortgage expert at David Roa to compare both loan types side by side and find the option that fits your financial goals and timeline.