DSCR Loans For Short Term Rentals: Qualifying Rules & Rates

Short-term rentals generate serious cash flow, but getting a mortgage for one can be frustrating when lenders want to see W-2s, tax returns, and two years of personal income history. That's exactly where DSCR loans for short term rentals come in. These loans qualify based on the property's projected rental income, not yours, which makes them one of the most practical financing tools available to Airbnb and vacation rental investors.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment properties, and DSCR financing is one of the products our investor clients use most. With more than 25 years as a senior loan officer and active real estate investor myself, I've seen firsthand how these loans remove the biggest bottleneck standing between investors and their next deal.

This guide breaks down how DSCR loans work for short-term rentals, what lenders look for when calculating your ratio, current rate expectations, and the qualifying rules you need to know before applying. Whether you're buying your first Airbnb property or scaling a portfolio, this is the roadmap to get there with the right financing in place.

What DSCR loans cover for short-term rentals

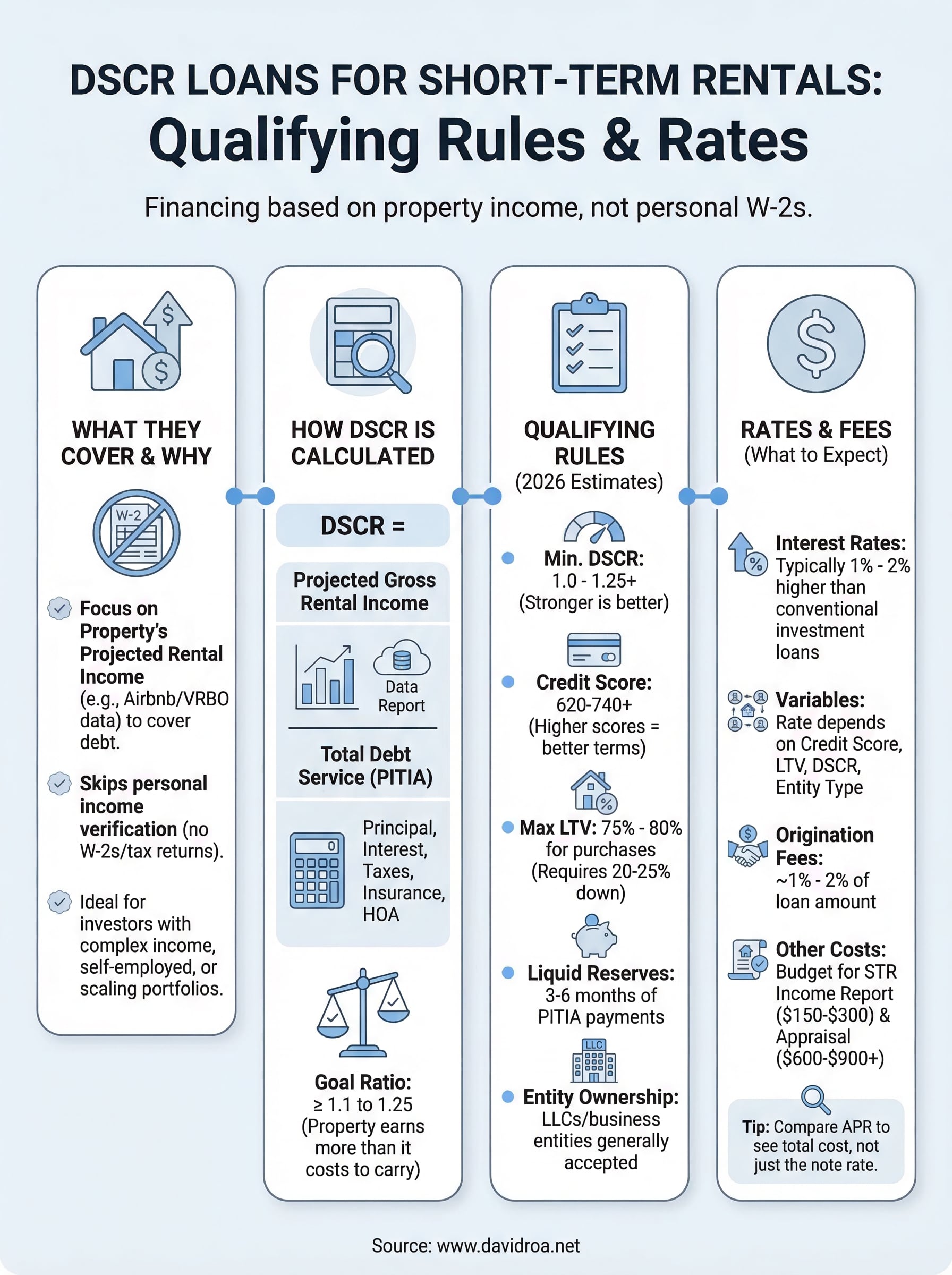

A DSCR loan is a non-QM (non-qualified mortgage) product built specifically for investment properties. Unlike conventional loans, the lender skips personal income verification entirely and focuses instead on whether the property generates enough rental revenue to cover its own debt payments. For short-term rentals, this means projected income from platforms like Airbnb or VRBO is what drives your approval, not your W-2 or a two-year history of personal tax returns. That single shift in underwriting logic changes everything for investors who are self-employed, own multiple properties, or have income that doesn't show up cleanly on paper.

The core premise: DSCR loans qualify the asset, not the borrower's personal income, which is a major advantage for investors who write off income aggressively or hold properties through an LLC.

Property types that qualify

When it comes to dscr loans for short term rentals, most lenders accept a wide range of residential investment property types. Single-family homes, condos, townhomes, and 2-4 unit properties are standard across nearly every DSCR program available today. Many lenders also extend financing to vacation homes, cabins, and lake houses that generate short-term rental income through Airbnb, VRBO, or similar booking platforms. The property must be classified as non-owner-occupied, meaning you're buying it strictly as an investment, not as your primary or secondary residence.

Not every property type qualifies automatically. Condotels, fractional ownership properties, and units inside buildings with complex shared rental management agreements often face additional lender scrutiny or outright exclusions from DSCR programs. Before you make an offer, confirm with your loan officer that the specific property you're targeting meets the lender's program guidelines, since discovering a conflict after you're under contract creates unnecessary delays at underwriting.

What the loan funds

DSCR loans cover the same core transaction types you'd expect from a conventional investment property mortgage. You can use them to purchase a new short-term rental, rate-and-term refinance an existing one, or execute a cash-out refinance to pull equity and fund your next acquisition. That transaction flexibility is a primary reason investors use them to grow rental portfolios without running into the income documentation barriers that conventional lenders put in place.

Loan amounts typically range from $100,000 up to $3 million or more, depending on the lender, property location, and the strength of your DSCR ratio. Most programs allow you to hold the property in your personal name or inside an LLC, which matters for both asset protection and tax strategy. If you operate your rentals through a business entity, DSCR financing is one of the few mortgage products that accommodates that ownership structure without requiring you to verify personal W-2 income on your application.

Why STR investors use DSCR loans

Short-term rental investors run into a specific problem with conventional financing: their actual income looks worse on paper than their real cash flow suggests. Heavy depreciation write-offs, business deductions, and income routed through LLCs all reduce the taxable income that conventional lenders use to calculate your debt-to-income ratio. DSCR loans sidestep that problem entirely by measuring what actually matters, which is whether the property earns enough to cover its own debt payments.

Income documentation is no longer the barrier

When you apply for a DSCR loan, your lender asks for the property's projected rental income, not your W-2 or two years of personal tax returns. That shift removes the single biggest obstacle most active real estate investors face. Self-employed borrowers, full-time investors, and high-net-worth individuals who optimize their taxes aggressively can all qualify based on how the property performs, not how their personal returns look.

For investors who reduce taxable income heavily through depreciation or business expenses, DSCR financing is often the only loan type that reflects their real financial position accurately.

This is why dscr loans for short term rentals have become the go-to product for Airbnb investors who want to grow without restructuring their financial profile to satisfy a bank's income requirements.

Portfolio scaling without hitting income limits

Conventional lenders cap the number of financed properties you can carry, typically at ten, and they count each new mortgage payment against your personal debt-to-income ratio. DSCR loans operate outside that framework entirely. Each property gets evaluated on its own rental income, which means you can keep adding units to your portfolio as long as each one carries itself financially. That structure makes DSCR programs a natural fit for investors building long-term rental income at scale, rather than stopping at one or two properties because a bank's DTI calculation runs out of room.

How DSCR is calculated for Airbnb income

The DSCR formula itself is straightforward: gross rental income divided by total debt service. A ratio of 1.0 means the property breaks even, covering its own payments exactly. Most lenders want to see a ratio of 1.1 to 1.25 or higher, which signals the property earns meaningfully more than it costs to carry. Where things get more specific for short-term rentals is in how lenders determine what counts as "income" when you're running an Airbnb rather than a long-term lease.

Because short-term rentals don't have a signed lease to verify income, lenders rely on third-party market data to estimate what the property will realistically earn.

How lenders estimate short-term rental income

For dscr loans for short term rentals, lenders typically order a short-term rental income report from a data provider that analyzes comparable properties in your market. These reports pull booking rates, occupancy trends, and average nightly rates from platforms like Airbnb and VRBO to produce a projected annual gross income figure for your specific property. That projected number is what feeds into your DSCR calculation, replacing the lease agreement a long-term rental investor would submit.

Some lenders also accept an appraiser's market rent analysis for short-term use, which factors in seasonal demand, local competition, and property-specific amenities. Either way, the income figure used is a projection, not a guarantee, so the property needs to show strong comparable performance in its market to support a favorable ratio.

What counts as debt service

Your total debt service includes principal, interest, property taxes, insurance, and HOA dues if applicable, commonly referred to as PITIA. Lenders use the full monthly PITIA payment as the denominator in your DSCR equation. A lower monthly payment or a higher projected income both improve your ratio, which is why loan amount, interest rate, and local tax burden all directly affect whether your deal qualifies.

Qualifying rules lenders use in 2026

DSCR programs have tightened in certain areas since rates climbed, but the core framework for dscr loans for short term rentals remains accessible for investors who understand what lenders actually evaluate. Most programs today set a minimum DSCR of 1.0 to 1.25, with the stronger ratios unlocking better rates and higher loan-to-value limits. A handful of lenders still approve ratios below 1.0, but you'll pay a pricing premium for that flexibility.

Credit score and loan-to-value thresholds

Lenders set minimum credit score requirements in the range of 620 to 680, with the most competitive programs starting at 700 or above. Your credit score directly controls both your rate tier and your maximum LTV, so a score above 740 gives you meaningful advantages on both fronts. Most programs cap LTV at 75 to 80 percent for purchases, which means you need a down payment of 20 to 25 percent at closing. Short-term rental properties often sit at the lower end of that LTV range because lenders treat them as higher-volatility assets compared to long-term leases.

Your credit profile still matters significantly in DSCR lending, even though personal income never enters the equation.

Reserves, entity ownership, and property condition

After closing, most lenders require you to hold three to six months of PITIA payments in verified liquid reserves. That reserve requirement protects both you and the lender against seasonal vacancy gaps, which are common with short-term rentals. Properties held inside an LLC or business entity are generally accepted, but some lenders add a small rate adjustment for entity-owned deals. The property itself must also meet standard condition requirements at appraisal. Lenders will not fund short-term rentals in poor or deferred-maintenance condition, so factor any needed repairs into your budget before you apply.

Rates, fees, and how to compare lenders

DSCR loans carry higher interest rates than conventional mortgages because lenders price in the additional risk of investment property and non-QM underwriting. For dscr loans for short term rentals specifically, expect rates to run roughly 1 to 2 percentage points above comparable conventional investment property rates, reflecting the added volatility lenders associate with short-term rental income versus a signed long-term lease.

What rates look like in 2026

Your rate depends on four primary variables: your credit score, your loan-to-value ratio, the property's DSCR, and whether the property is held in your name or an LLC. Borrowers with credit scores above 740, a DSCR above 1.25, and an LTV at or below 75 percent consistently receive the most competitive pricing. Short-term rental properties often receive a small rate add-on compared to long-term rental equivalents at the same program tier, so account for that when running your cash-flow projections before making an offer.

Getting quotes from at least three lenders lets you see the actual rate spread in your market rather than relying on advertised minimums that rarely reflect your specific scenario.

Fees and closing costs to budget for

Beyond the rate, origination fees on DSCR loans typically run 1 to 2 points, and you should also budget for the short-term rental income report ordered by the lender, which usually costs between $150 and $300. Appraisal fees on investment properties run higher than residential appraisals, often landing between $600 and $900 depending on the property type and location. Factor all of these into your total acquisition cost before comparing loan options.

How to compare lenders effectively

When you evaluate lenders, compare the Annual Percentage Rate (APR) rather than just the note rate, since APR captures origination fees and points inside a single number. Ask each lender how they source short-term rental income estimates, whether they use a third-party data report or an appraiser's market analysis, because that methodology directly affects the income figure driving your approval.

What to do next

You now have a complete picture of how dscr loans for short term rentals work, from how lenders calculate projected income to the credit, LTV, and reserve requirements that determine your approval. The next step is straightforward: run the numbers on your target property before you apply. Pull comparable short-term rental data for your market, estimate your PITIA payment at current rates, and check whether your projected DSCR clears the 1.25 threshold most lenders prefer.

If the ratio looks strong, you're in a position to move quickly. Working with an experienced loan officer who has funded DSCR deals across multiple property types makes a measurable difference in how smoothly your file moves through underwriting. At David Roa, we've helped investors close on Airbnb properties and rental portfolios across the country with financing built around property performance, not personal income. Get in touch with David Roa to discuss your deal and find the right program for your next acquisition.