Equipment Financing Calculator: Estimate Payments & Compare

Before you sign a financing agreement or lease contract for business equipment, you need to know what you're actually committing to. An equipment financing calculator gives you that clarity, breaking down your estimated payments based on the loan amount, interest rate, and term length so you can plan with real numbers instead of guesswork.

Whether you're looking at a $30,000 commercial oven or a $500,000 piece of construction machinery, the difference between buying and leasing, and the difference between a 5-year term and a 7-year term, can shift your monthly cash flow by hundreds or even thousands of dollars. Getting those estimates upfront helps you walk into conversations with lenders already knowing what fits your budget.

At David Roa, we've helped business owners secure equipment financing as part of our broader commercial and SBA lending services, backed by over 25 years of experience and more than $150 million funded. This guide walks you through how equipment financing calculators work, what inputs matter most, and how to compare your options so you can make the smartest move for your business.

What an equipment financing calculator should cover

A basic payment calculator only tells part of the story. A solid equipment financing calculator accounts for both loan and lease scenarios, because the inputs and outputs differ significantly between the two. Before you trust any estimate, confirm the tool you're using captures all the variables that actually drive your payment, not just the sticker price of the equipment.

Core loan inputs

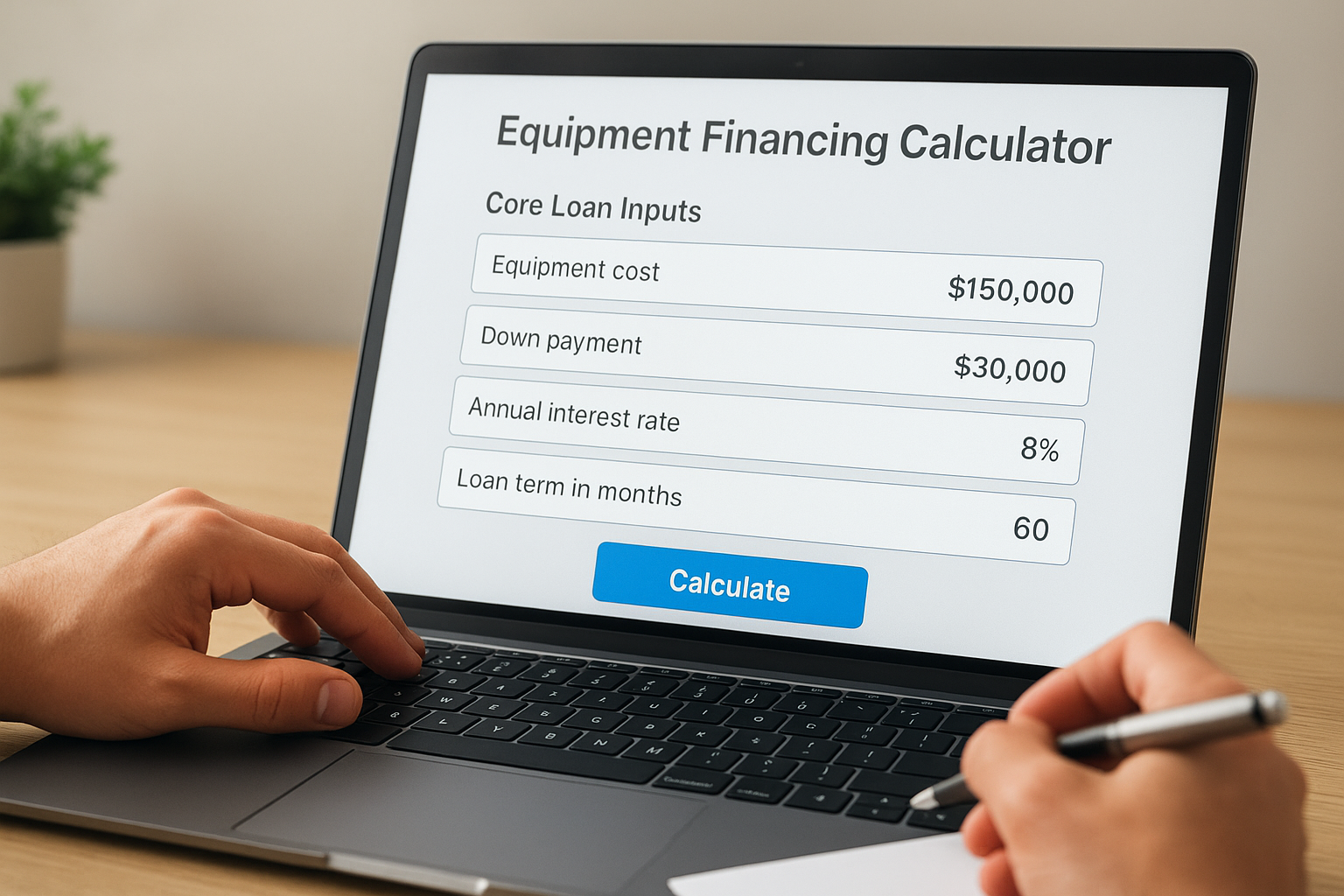

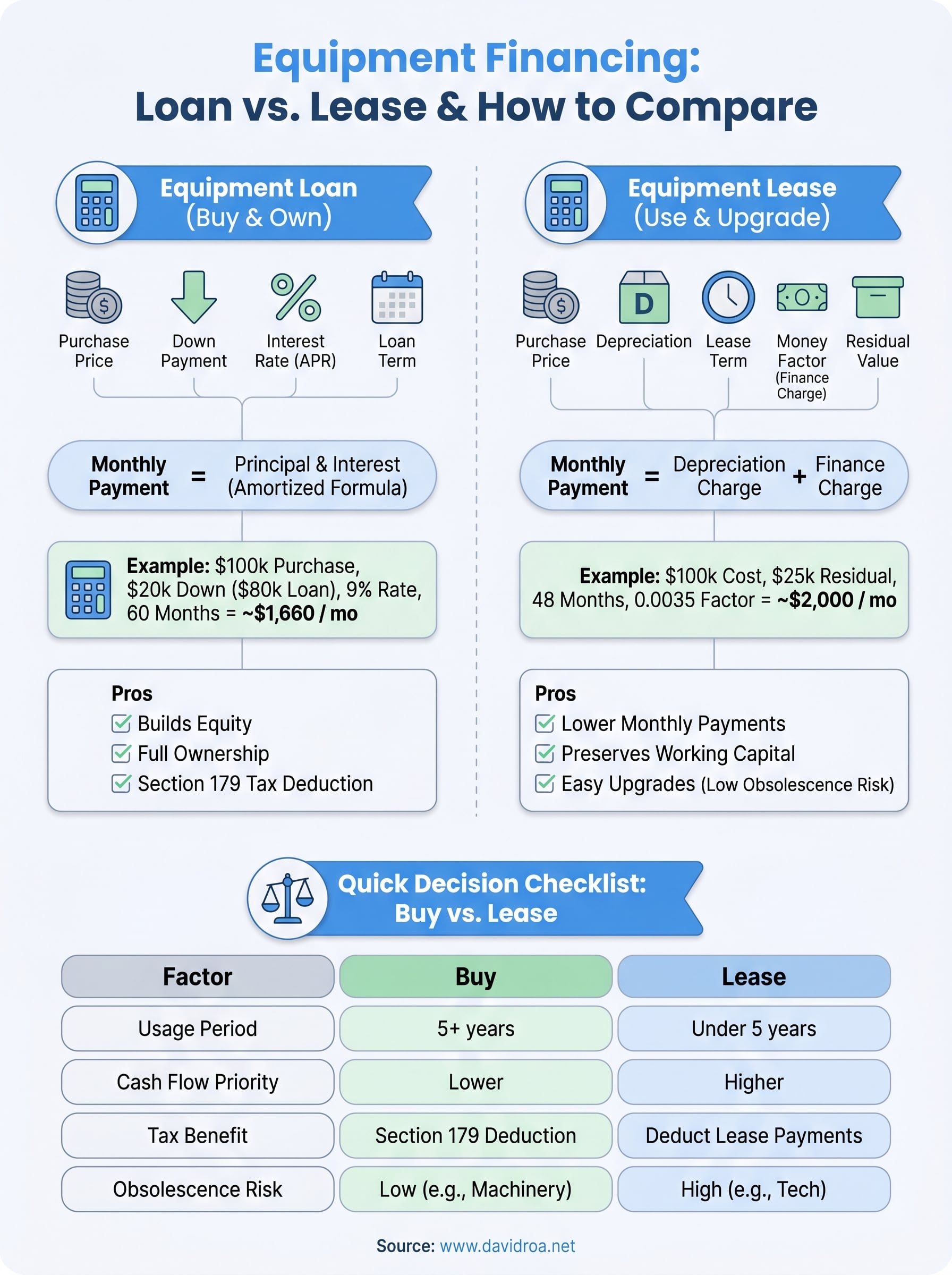

For a standard equipment loan, the calculator needs three numbers to produce an accurate monthly payment estimate: the loan amount (principal), the annual interest rate (APR), and the loan term in months. Equipment loan terms typically run 24 to 84 months, and a rate shift of even one to two percentage points can change your monthly payment noticeably on larger purchases.

If you finance $150,000 at 8% over 60 months, your estimated monthly payment lands around $3,042. At 10%, that same loan runs about $3,187 per month, a difference of $145 every single month.

Here are the core inputs a loan calculator should include:

- Equipment cost (purchase price)

- Down payment or trade-in value

- Annual interest rate (APR)

- Loan term (in months)

- Residual or balloon payment (if applicable)

Lease-specific variables

Lease calculations work differently because you're financing the depreciation of the equipment, not its full purchase price. The calculator needs your equipment cost, the money factor (the lease equivalent of an interest rate), the lease term, and the estimated residual value at the end of the term. Without that residual value input, the payment estimate will be inaccurate.

Your lease payment covers the gap between the equipment's current value and its projected residual value at lease end, plus the financing cost. Two pieces of equipment at the same purchase price can carry very different lease payments depending on how well each holds its value over time.

Step 1. Gather the numbers before you calculate

Running any equipment financing calculator without accurate inputs gives you meaningless output. Before you open a calculator, pull together the exact figures for your equipment purchase so every estimate you get reflects your actual situation, not a rough guess.

The numbers you need

Collecting the right data upfront takes five minutes and saves you from recalculating multiple times. Here are the specific numbers you need before you start:

- Equipment purchase price (get a formal quote from the vendor)

- Down payment amount (typically 10% to 20% of the purchase price)

- Expected loan or lease term (24, 36, 48, 60, or 84 months)

- Annual interest rate or money factor (ask your lender for a rate estimate)

- Residual value (for leases, ask the vendor for the equipment's projected value at lease end)

If you don't have a rate yet, use a realistic range: equipment loan rates typically fall between 6% and 30% depending on your credit profile, time in business, and equipment type.

Your credit score and business revenue also influence the rate a lender will offer you, so have those figures ready before you contact anyone.

Step 2. Estimate payments for an equipment loan

With your numbers ready, you can calculate your estimated monthly payment using the standard amortizing loan formula. This formula breaks your total loan into equal monthly payments that cover both principal and interest over the full term.

The loan payment formula

The formula for a fixed monthly payment is:

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Where:

- M = Monthly payment

- P = Loan principal (equipment cost minus down payment)

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of monthly payments

Running this formula manually or inside any equipment financing calculator gives you a reliable baseline before you sit down with a lender.

A worked example

Say you're financing $80,000 after a $20,000 down payment on a $100,000 purchase. At a 9% annual rate over 60 months, your monthly interest rate is 0.75% (9% ÷ 12). Plugging those figures in:

- P = $80,000

- r = 0.0075

- n = 60

Your estimated monthly payment lands at approximately $1,660. Over the full 60-month term, you pay roughly $99,600 total, meaning about $19,600 goes toward interest charges alone.

Step 3. Estimate payments for an equipment lease

Lease payments work differently from loan payments. Instead of paying off the full purchase price, you're covering the depreciation of the equipment over the lease term plus a financing charge applied to the combined cost. Running this through an equipment financing calculator shows you exactly how much the residual value drives your monthly number.

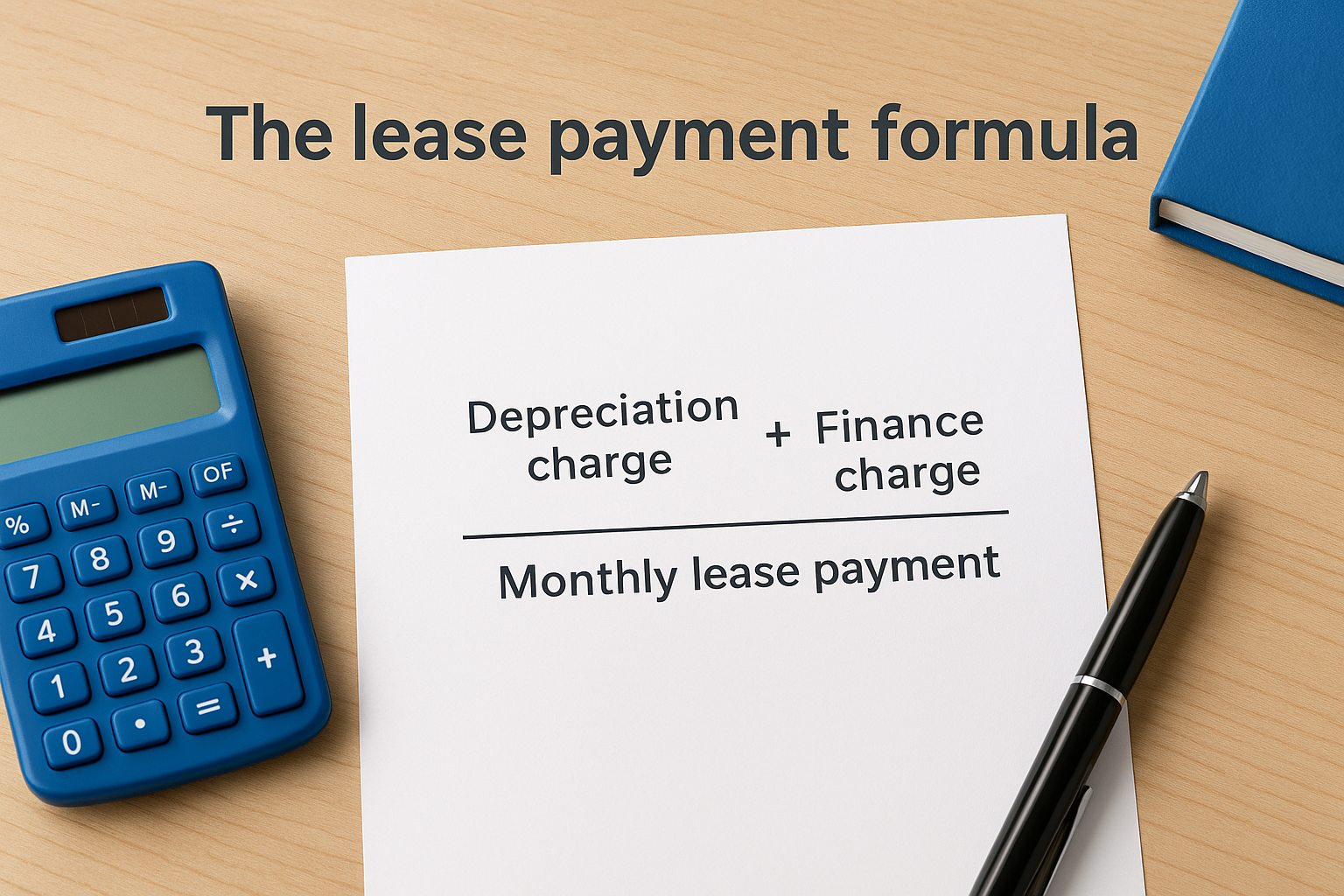

The lease payment formula

The monthly lease payment breaks into two parts: the depreciation charge and the finance charge. Add them together to get your total monthly obligation.

- Depreciation charge = (Equipment cost - Residual value) ÷ Lease term (months)

- Finance charge = (Equipment cost + Residual value) × Money factor

- Monthly lease payment = Depreciation charge + Finance charge

Convert the money factor to an approximate APR by multiplying it by 2,400, so you can compare it directly against loan interest rates.

A worked example

Take a $100,000 equipment lease with a $25,000 residual value, a 48-month term, and a money factor of 0.0035.

- Depreciation charge: ($100,000 - $25,000) ÷ 48 = $1,562.50

- Finance charge: ($100,000 + $25,000) × 0.0035 = $437.50

- Monthly lease payment: $1,562.50 + $437.50 = $2,000

Your monthly payment drops compared to financing the full purchase price, which makes leasing attractive for businesses managing tight cash flow without sacrificing access to necessary equipment.

Step 4. Compare buy vs lease with a clear checklist

Once you've run both sets of numbers through an equipment financing calculator, put them side by side before you commit. Buying builds equity and ends with full ownership, while leasing preserves working capital and keeps your equipment current. The right choice depends on your specific business priorities.

The option with the lower monthly payment isn't always the better deal; total cost of ownership over the full term tells the more complete story.

When buying makes more sense

Purchasing makes sense when you plan to use the equipment for five or more years and it holds its value well. You also benefit from the Section 179 tax deduction, which lets you deduct the full purchase price in the year you buy it.

- Long-useful-life equipment (machinery, vehicles)

- Strong cash reserves to cover the down payment

- Low obsolescence risk

When leasing makes more sense

Leasing fits best when cash flow is your top priority or when the equipment becomes outdated quickly. Technology-heavy assets like servers or diagnostic tools rarely make sense to own long-term.

- Limited upfront capital available

- Equipment upgrades needed every three to five years

- Preference for keeping assets off your balance sheet

Quick decision checklist

Use this table to match your situation to the right financing path:

| Factor | Buy | Lease |

|---|---|---|

| Usage period | 5+ years | Under 5 years |

| Cash flow priority | Lower | Higher |

| Tax benefit | Section 179 deduction | Deduct lease payments |

| Obsolescence risk | Low | High |

Next steps

You now have everything you need to run an equipment financing calculator with confidence and interpret what the numbers actually mean for your business. Start by pulling the exact figures from your vendor quote, then run both the loan and lease scenarios using the formulas in this guide. Comparing total cost over the full term, not just the monthly payment, gives you the clearest picture before you commit.

Once you have your estimates in hand, the next step is talking to a lender who understands your industry, your cash flow, and your growth goals. Equipment financing works best when the structure matches your specific situation, whether that's a fixed-rate loan with a Section 179 deduction or a short-term lease that keeps your capital free. If you're ready to move forward and want guidance from someone with over 25 years in commercial lending, connect with David Roa to review your options and find the right fit.