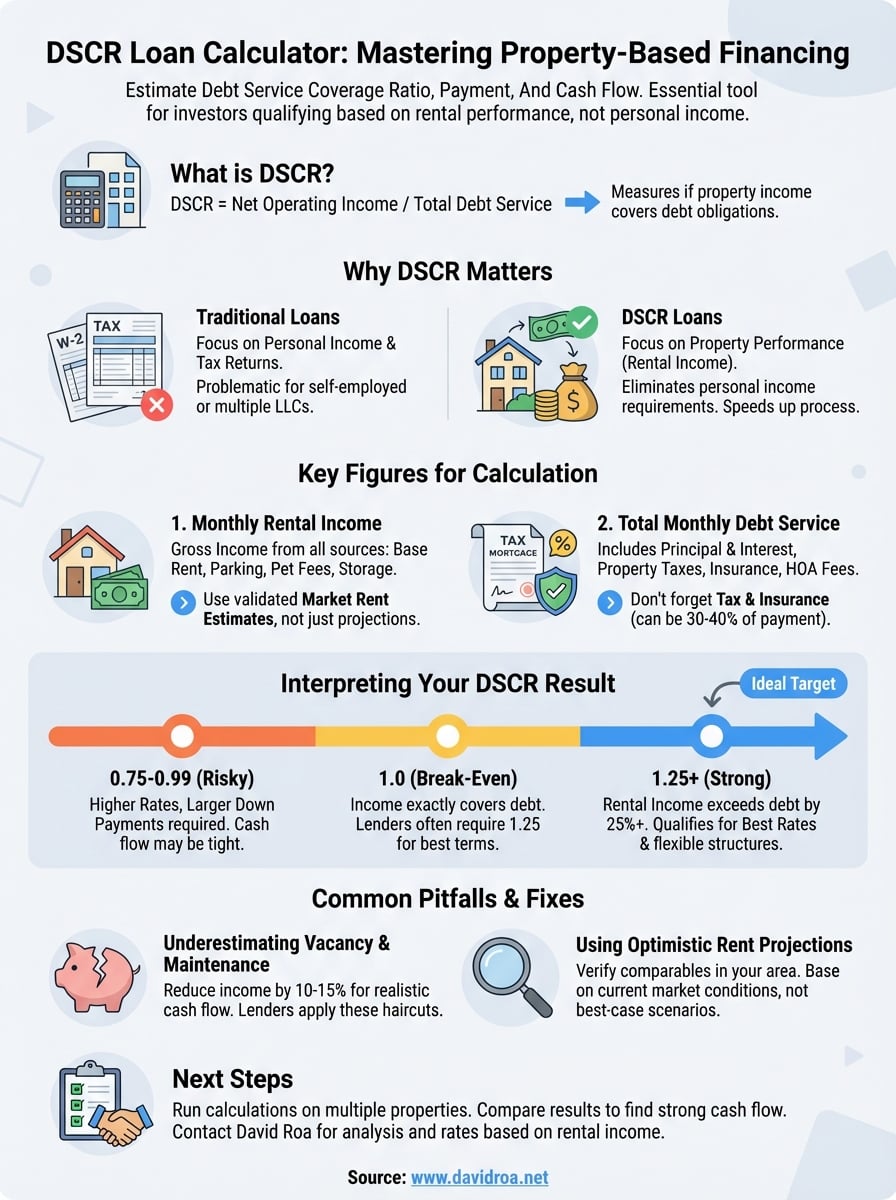

DSCR Loan Calculator: Estimate DSCR, Payment, And Cash Flow

Real estate investors know that qualifying for a loan based on personal income can be frustrating, especially when your properties generate strong rental cash flow. That's where a DSCR loan calculator becomes essential. This tool helps you estimate whether a property's income can cover its debt obligations, which is exactly what lenders evaluate when approving Debt Service Coverage Ratio loans.

At David Roa, we've funded over $150 million in loans, including DSCR financing for investors who prefer qualification based on property performance rather than personal tax returns. Whether you're expanding your rental portfolio or acquiring your first investment property, understanding your DSCR before applying saves time and sets realistic expectations.

This guide walks you through how to use a DSCR calculator, what the numbers actually mean, and how to strengthen your ratio if it falls short of lender requirements.

Why DSCR matters for investor loans

Traditional lenders base loan approval on your personal tax returns, W-2s, and employment history. That creates a problem when you're self-employed, earning income through multiple LLCs, or writing off legitimate business expenses that lower your taxable income. Your debt-to-income ratio may look weak on paper even when your rental properties generate strong positive cash flow.

How DSCR loans eliminate personal income requirements

DSCR loans shift the focus entirely to property performance. Lenders evaluate whether the rental income covers the mortgage payment, taxes, insurance, and HOA fees. You don't submit tax returns or employment verification, which speeds up the process and removes barriers for investors with complex income structures or high write-offs. A dscr loan calculator shows you in minutes whether your property meets the typical 1.0 to 1.25 ratio threshold that most lenders require.

If your property generates $2,500 in monthly rent and your total debt service is $2,000, you have a DSCR of 1.25, which qualifies you for favorable rates.

Why portfolio growth depends on DSCR qualification

When you scale your portfolio, applying for conventional loans becomes impractical because most lenders cap you at 10 financed properties. DSCR loans don't count toward that limit since they're underwritten as investment products rather than consumer mortgages. This structure allows you to acquire properties faster without hitting regulatory restrictions. Investors who understand how to calculate and improve their DSCR can leverage rental income to fund additional acquisitions, creating a sustainable growth strategy that doesn't rely on personal income verification or employment stability.

What numbers you need to calculate DSCR

You need two primary figures to use any dscr loan calculator: monthly rental income and total monthly debt service. The calculation divides gross rental income by all monthly property obligations to determine whether cash flow justifies the loan. Most calculators require you to input actual or projected rent along with your proposed mortgage payment, property taxes, insurance, and HOA fees if applicable.

Monthly rental income sources

Your gross rental income includes all money the property generates before expenses. This covers base rent, parking fees, pet rent, storage unit income, and any other tenant-paid amounts. Lenders typically use market rent estimates from appraisals rather than your optimistic projections, so you should verify comparable rental rates in your area before running calculations. A property with multiple units requires you to add all rent streams together for the total monthly figure.

Total monthly debt service

Debt service includes your principal and interest payment, property taxes, homeowner's insurance, and any HOA or condo fees. Most borrowers underestimate this number by forgetting tax and insurance costs, which can represent 30 to 40 percent of your total payment. You calculate this figure by adding your proposed mortgage payment to monthly property tax (annual tax divided by 12), monthly insurance premium, and monthly HOA if the property has one.

Lenders count every recurring monthly obligation tied to the property, not just your mortgage payment.

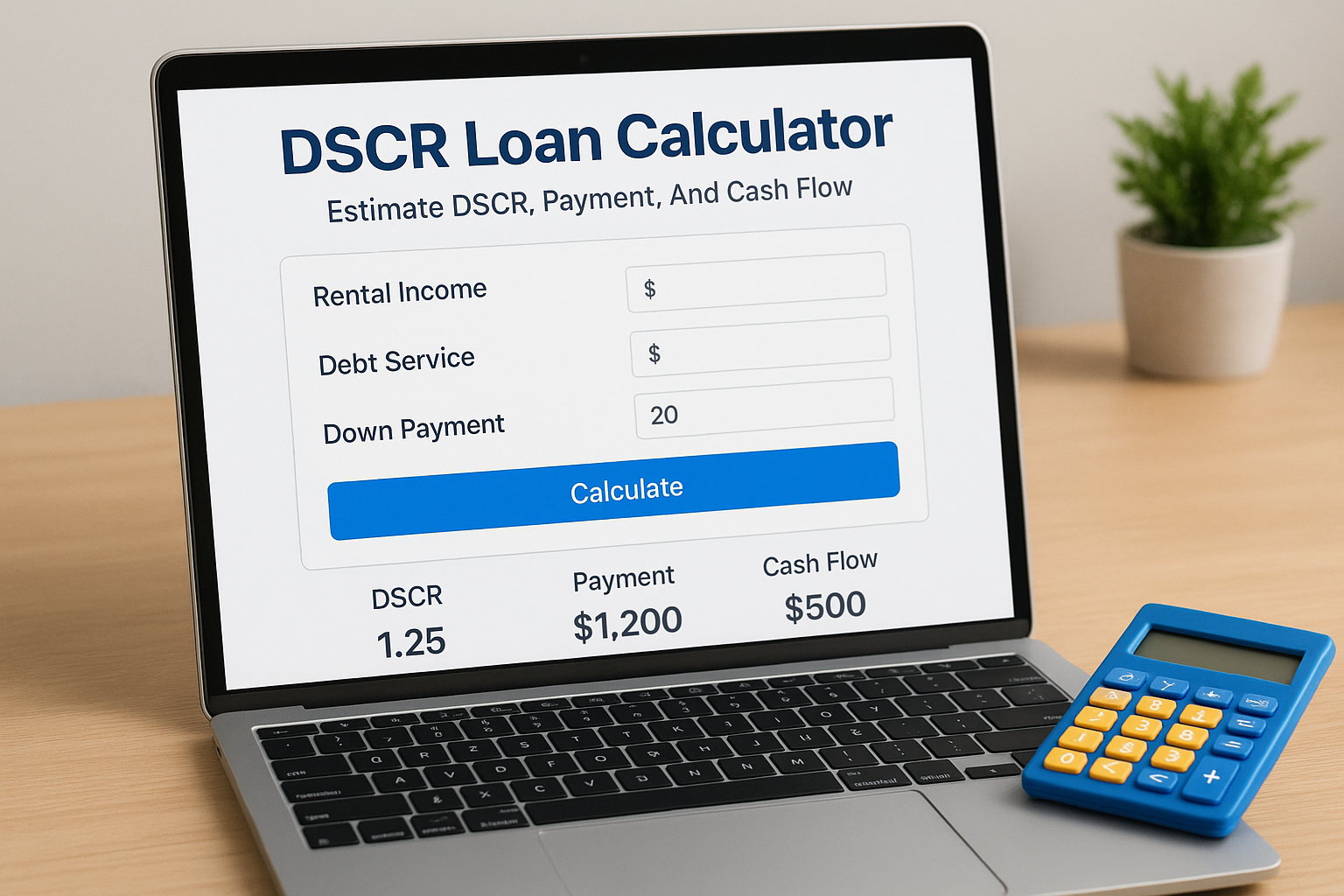

How to use a DSCR loan calculator

Most DSCR calculators follow a straightforward process. You enter your property's monthly rental income and then input your proposed loan amount, interest rate, and term. The calculator automatically adds estimated property taxes, insurance, and HOA fees based on either your input or standard percentages. Some advanced tools let you adjust these figures manually for greater accuracy.

Input your property details

You start by entering your total monthly rent from all income sources tied to the property. Next, you input your purchase price or loan amount, the interest rate you expect to receive, and your loan term (typically 30 years for investment properties). Most calculators require you to specify whether you plan to make a 20, 25, or 30 percent down payment since that affects your loan amount and monthly payment. Property tax rates and insurance costs usually auto-populate based on the property location you enter.

Review your DSCR result

The calculator displays your debt service coverage ratio along with your monthly cash flow after all obligations. A result of 1.25 means your rental income exceeds debt service by 25 percent, which qualifies you for standard rates.

Most lenders require a minimum DSCR of 1.0 to 1.25, though some accept 0.75 with larger down payments.

How lenders interpret DSCR and set terms

Your DSCR number determines both approval and pricing. Lenders use this ratio as their primary risk assessment tool because it shows whether the property generates enough income to sustain the loan. A higher ratio signals lower risk, which translates to better interest rates and more flexible loan structures. Understanding these thresholds before you shop for financing helps you target properties that match your capital and income strategy.

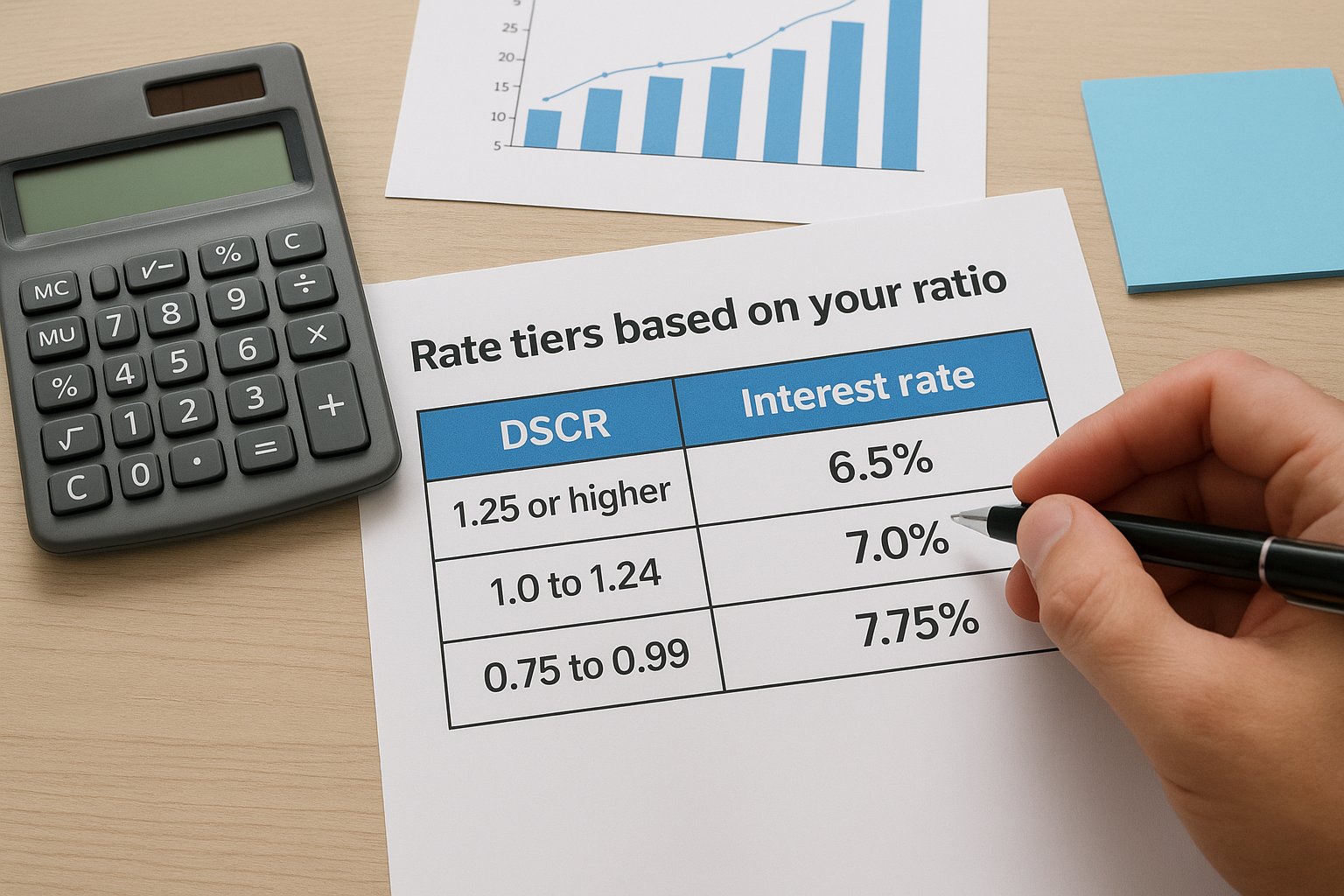

Rate tiers based on your ratio

Lenders typically offer their best rates at 1.25 DSCR or higher, viewing these deals as strong cash flow opportunities with minimal default risk. You'll see rates increase by 0.25 to 0.50 percent when your ratio drops to 1.0 to 1.24, and some lenders charge an additional premium for ratios below 1.0. Properties with 0.75 to 0.99 DSCR still qualify but require larger down payments and accept higher interest costs. Running scenarios through a dscr loan calculator before making offers shows you exactly where your deal falls on the rate spectrum.

A 1.30 DSCR property might qualify at 6.5 percent while a 0.85 DSCR property gets quoted at 7.75 percent with the same down payment.

Common pitfalls and quick fixes

Most investors make calculation errors that artificially inflate their DSCR, leading to surprise rejections or weaker cash flow than expected. The most common mistake involves using gross rental income without accounting for vacancy periods, maintenance reserves, or property management fees. A dscr loan calculator shows your ratio based on full occupancy, but lenders expect you to maintain positive cash flow even during tenant turnover or unexpected repairs.

Underestimating vacancy and maintenance costs

You should reduce your rental income figure by 10 to 15 percent to account for realistic vacancy rates and ongoing maintenance. A property renting for $2,500 monthly actually generates $2,125 to $2,250 in reliable annual average income when you factor in turnover periods and repair costs. Lenders who conduct detailed underwriting often apply these haircuts automatically, so your approval depends on the adjusted figure rather than your optimistic projections.

Using optimistic rent projections

Your market rent estimate must reflect actual comparable properties in your area, not aspirational pricing. Pull recent rental data from properties with similar square footage, condition, and location before running your calculations. Appraisers verify these figures during underwriting, and inflated projections cause delays or denials when the final valuation comes back lower than expected.

Base your DSCR on conservative rent estimates that match current market conditions, not best-case scenarios.

Next steps for your property analysis

You now understand how a dscr loan calculator works and what adjustments improve your ratio before applying. Your next move should focus on running calculations on multiple properties in your target market rather than falling in love with a single deal. Compare DSCR results across different price points and rental income levels to identify which properties offer the strongest cash flow and approval odds.

Start by pulling accurate market rent data from at least three comparable properties within a half-mile radius of your target acquisition. Input conservative figures that account for vacancy and maintenance costs, then adjust your down payment percentage until you reach a 1.25 DSCR or higher. This exercise shows you exactly what capital you need to secure favorable loan terms.

Ready to move forward with DSCR financing? Contact David Roa to discuss your property analysis and lock in rates based on your rental income rather than personal tax returns.