FHA Loan Limits Explained: 2026 Floor, Ceiling, And Counties

Every FHA borrower hits the same question early in the process: how much can I actually borrow? The answer depends on where you're buying, what type of property you're financing, and which year's limits apply. This guide covers FHA loan limits explained for 2026, including the national floor, the ceiling for high-cost areas, and how to look up the specific cap for your county.

FHA loan limits change annually based on home price data, and the 2026 numbers reflect another round of adjustments. If you're buying a single-family home in a mid-range market, your borrowing cap will look very different from someone purchasing a fourplex in a high-cost metro. Understanding these tiers matters because exceeding your county's limit means you'll either need to bring more cash to closing or explore a different loan program. Getting this right upfront saves you from chasing properties you can't finance under FHA guidelines.

At David Roa, we've closed over $150 million in funded loans across FHA, VA, Jumbo, DSCR, and dozens of other programs over 25+ years. FHA loans remain one of the most accessible paths to homeownership, especially for first-time buyers and borrowers working with tighter down payments. We walk clients through these details daily, not just the numbers, but what they mean for your specific purchase. Below, you'll find a clear breakdown of 2026 FHA loan limits, how they're calculated, and exactly how to find the figures for your area.

Why FHA loan limits matter

FHA loan limits matter because they define the maximum loan amount the federal government will insure for a mortgage in your county. The FHA does not lend money directly; it insures loans, which reduces risk for lenders and allows them to offer lower down payments and more flexible credit requirements. Once a loan amount crosses the county cap, the FHA will not insure it, and most lenders will not write it as an FHA product.

Your county's FHA limit is a hard ceiling: exceeding it means FHA insurance does not apply, and you will need to qualify under a different program entirely.

When the limit shapes your property search

Knowing your county limit before you start shopping changes how you approach the entire buying process. If your target area has a limit of $524,225 and you're looking at homes priced at $550,000, you already know you'll need to cover the gap with a larger down payment or pivot to a conventional loan. Without this information upfront, you risk spending weeks touring homes and negotiating deals that cannot close under FHA terms.

Your county limit also interacts directly with property type. A single-family home carries a different cap than a two-unit, three-unit, or four-unit property. If you plan to buy a duplex and rent the second unit to offset your mortgage payment, the higher multi-unit limit may give you more purchasing room than you expected. Running these numbers before you tour properties keeps your search focused on homes where FHA financing is actually viable.

When prices run ahead of the limit

In competitive markets, home prices sometimes outpace the county FHA cap. This is especially common in suburban markets that sit just outside a high-cost metro designation. You may be shopping in a county where the limit held at the national floor while nearby home values climbed. When that happens, your effective purchase price ceiling is lower than the market reflects, and you need to plan accordingly.

This is where getting fha loan limits explained in full detail pays off. Knowing your county's specific number lets you filter your property search accurately, set realistic expectations with your real estate agent, and avoid financing surprises late in the transaction.

How FHA loan limits are calculated each year

The Federal Housing Administration ties its limits directly to conforming loan limits set by the Federal Housing Finance Agency. Each fall, the FHFA updates those conforming limits based on changes in average home prices nationwide, and FHA limits adjust accordingly.

The floor, ceiling, and county calculation

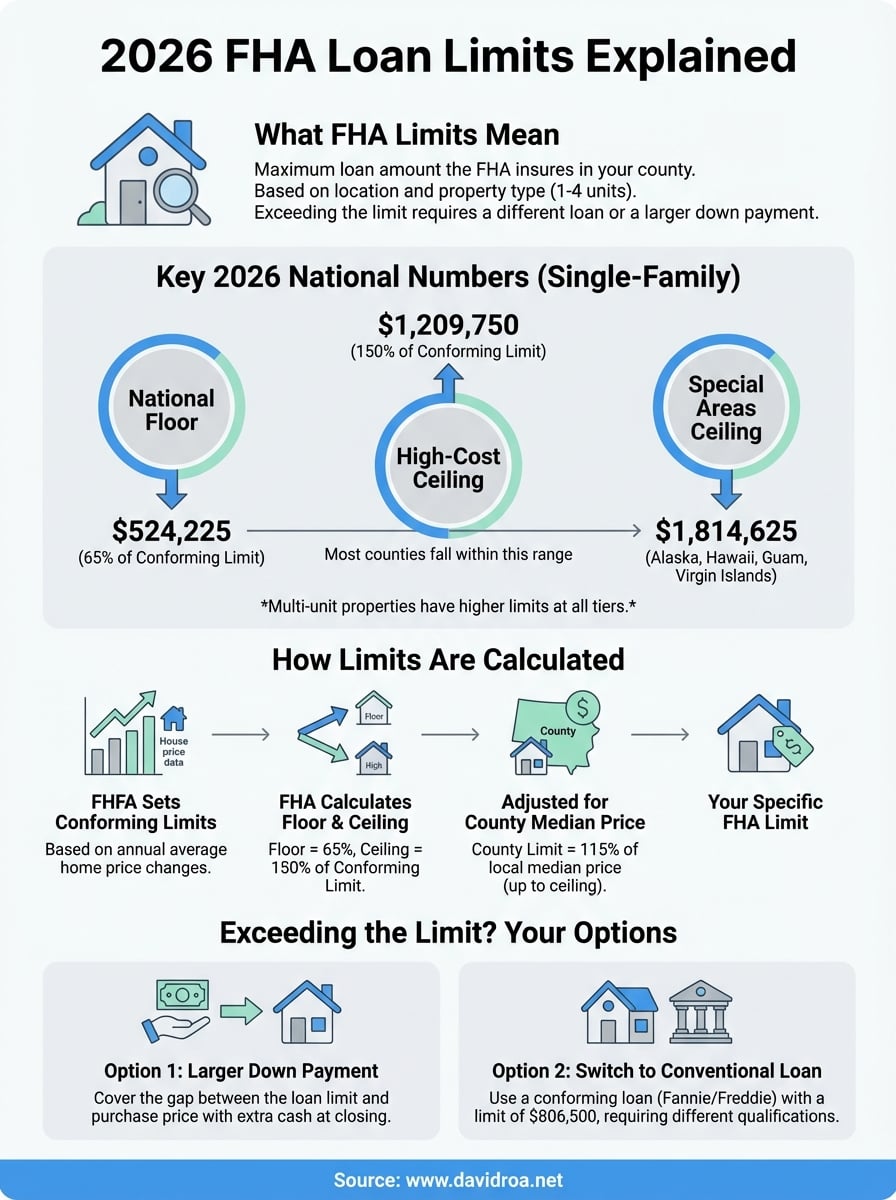

FHA sets the floor at 65% of the national conforming loan limit, while the ceiling for high-cost areas sits at 150% of that same number. For 2026, the conforming loan limit for a single-family property is $806,500, which produces a floor of $524,225 and a ceiling of $1,209,750.

The floor and ceiling both move with the conforming loan limit each year, so a strong home price report from the FHFA directly raises the maximum you can borrow under FHA.

Any county where 115% of the local median home price falls between the floor and the ceiling receives its own unique limit. Counties at or below the floor get the national minimum; counties in high-cost metros can reach the full ceiling.

Local median prices and your county cap

HUD calculates each county's limit using local median home price data. If 115% of the median price in your county exceeds the national floor, your county gets a higher limit up to the ceiling cap. Two counties sitting side by side can carry different FHA caps if their median home prices differ significantly.

Getting fha loan limits explained accurately means recognizing that your specific county number reflects local market conditions, not a single national figure applied uniformly across the country.

2026 FHA loan limits: floor, ceiling, special areas

For 2026, the national floor for a single-family home is $524,225, and the high-cost area ceiling reaches $1,209,750. These two numbers define the range within which most county limits fall. Getting fha loan limits explained with the right context means understanding that your actual borrowing cap depends on which tier your county falls into, and which property type you're financing.

Multi-unit property limits at the floor and ceiling

The floor and ceiling figures apply specifically to single-family homes. Multi-unit properties carry higher limits at every tier. For 2026, the floor for a two-unit property is $671,200, a three-unit property hits $811,275, and a four-unit property reaches $1,008,300. At the high-cost ceiling, those numbers scale up proportionally, giving investors and house-hackers significantly more room to borrow under FHA terms.

If you plan to live in one unit and rent the others, the multi-unit FHA limits may open up properties you assumed were out of reach.

Special geographic areas and their elevated caps

Alaska, Hawaii, Guam, and the U.S. Virgin Islands operate under a separate, higher tier because of elevated construction and land costs specific to those locations. In 2026, the single-family ceiling for these special areas is $1,814,625, well above the standard high-cost ceiling. Multi-unit properties in these areas carry proportionally higher caps. If you're buying in one of these locations, your FHA borrowing ceiling extends significantly beyond what most mainland buyers will encounter.

How to find your county FHA limit on HUD

HUD maintains a public lookup tool that gives you the exact FHA limit for your county without any calculations on your end. The tool updates annually after FHFA releases the new conforming limits, so the numbers you pull directly from HUD reflect the current year's official caps for your specific location and property type.

Using the HUD mortgage limits tool

The HUD Mortgage Limits lookup page lets you search by state, county, and metropolitan statistical area. You select your state and county from dropdown menus, hit search, and the tool returns the FHA limits for all four property types in your area. The process takes under two minutes and requires no account or login.

Bookmark the HUD lookup page so you can recheck limits quickly when you're comparing counties or tracking year-over-year changes.

Here's what to enter:

- State: Select your state from the dropdown

- County: Select the specific county where the property sits

- Limits Year: Confirm you're viewing the current year's figures

Reading your county results

Once the results load, you'll see a table showing limits for one-unit through four-unit properties. The one-unit row applies to standard single-family homes. If you're purchasing a multi-unit property, read across to the correct column.

Getting fha loan limits explained through the actual HUD data is the most reliable approach because it removes any guesswork about whether your source reflects the current year's official figures.

What to do if the home price exceeds the limit

When a home's purchase price pushes above your county's FHA cap, you still have real options worth evaluating before walking away from the property. The key is knowing which path fits your financial position. Getting fha loan limits explained fully means understanding not just the cap itself, but what happens when your target property crosses it.

Bring a larger down payment to cover the gap

You can still use FHA financing on a higher-priced property by increasing your down payment to bring the loan amount down to or below the county limit. If the purchase price is $560,000 and your county limit is $524,225, you need to cover the $35,775 difference out of pocket in addition to your standard FHA minimum down payment. This approach works well if you have the cash reserves but want to keep the FHA's flexible credit requirements and lower mortgage insurance structure.

Run this calculation early so you know exactly how much cash you need at closing before you make an offer.

Switch to a conventional loan program

A conventional loan removes the FHA cap entirely, since Fannie Mae and Freddie Mac conforming limits sit at $806,500 for 2026. If your credit score and debt-to-income ratio qualify, conventional financing may carry comparable or better terms depending on your down payment size. For higher credit profiles, conventional loans also allow private mortgage insurance cancellation once you reach 20% equity, which FHA loans do not offer on the same terms. Comparing both paths with your loan officer before you make an offer keeps your options open.

Next steps for your FHA loan plan

Now that you have fha loan limits explained from floor to ceiling, the next step is applying these numbers to your specific situation. Pull your county's 2026 limit from the HUD tool, match it against your target price range, and confirm which property type you're financing. This groundwork takes less than an hour and eliminates the most common cause of deal surprises: discovering too late that your loan amount exceeds what FHA will insure.

From there, connect with a loan officer who handles FHA deals daily, not one who treats them as an afterthought. With over 25 years of experience and more than $150 million funded across FHA and other programs, David Roa's lending team can walk you through your county limit, your qualification picture, and the best loan structure for your purchase. Getting started with the right guidance makes the whole process faster and cleaner.