FHA Loan Property Requirements: Minimum Standards Checklist

You found a home you love, got pre-approved for an FHA loan, and now you're wondering if the property will actually qualify. Here's the reality: FHA loan property requirements exist to protect you from purchasing a home with serious safety or structural problems. The FHA won't insure a mortgage on just any property, minimum standards for health, safety, and livability must be met before your loan gets final approval.

After funding over $150 million in residential mortgages across 25+ years, I've watched deals fall apart because buyers didn't understand what the FHA appraiser would flag during inspection. A cracked foundation, peeling paint on a pre-1978 home, or a faulty electrical panel can stop your closing in its tracks. The good news? Most issues are fixable once you know what to look for.

This guide gives you a clear checklist of every property standard the FHA requires, from roof condition to water heater safety. Whether you're a first-time homebuyer using traditional FHA financing or an ITIN borrower working through alternative documentation, understanding these requirements upfront helps you spot problems early and negotiate repairs before they become deal-breakers.

Why FHA property requirements matter

The FHA doesn't inspect properties to annoy you or slow down your closing. These standards exist because the government insures your lender against default, and they won't back a loan on a home that could become a money pit or safety hazard. When you apply for an FHA loan, the property itself becomes part of the underwriting process, not just your credit score and income. Every home must meet baseline safety standards before the FHA will approve your mortgage.

Protection from costly mistakes

You're about to make the largest purchase of your life, and FHA loan property requirements act as a mandatory safety net. I've seen buyers fall in love with a home only to discover $30,000 in foundation repairs or a failing septic system after closing. The FHA appraisal catches these problems upfront, giving you leverage to negotiate repairs or walk away without losing thousands. Pre-1978 homes with peeling paint trigger mandatory lead-based paint remediation, which protects your family from toxic exposure that most conventional inspections might overlook.

FHA standards prevent you from financing a property that could drain your savings or put your health at risk before you even move in.

Loan approval depends on it

Your pre-approval means nothing if the property fails inspection. The FHA appraiser must certify the home meets minimum standards before your lender releases funds, which means a cracked foundation, exposed wiring, or a damaged roof can kill your deal instantly. Unlike conventional loans where some lenders might overlook cosmetic issues, FHA financing requires documented compliance with every safety standard on their checklist. I've watched buyers lose earnest money because they waived inspection contingencies, assuming their FHA approval guaranteed closing. The property has to qualify just as much as you do, and that two-step approval process protects both your investment and the government's financial risk.

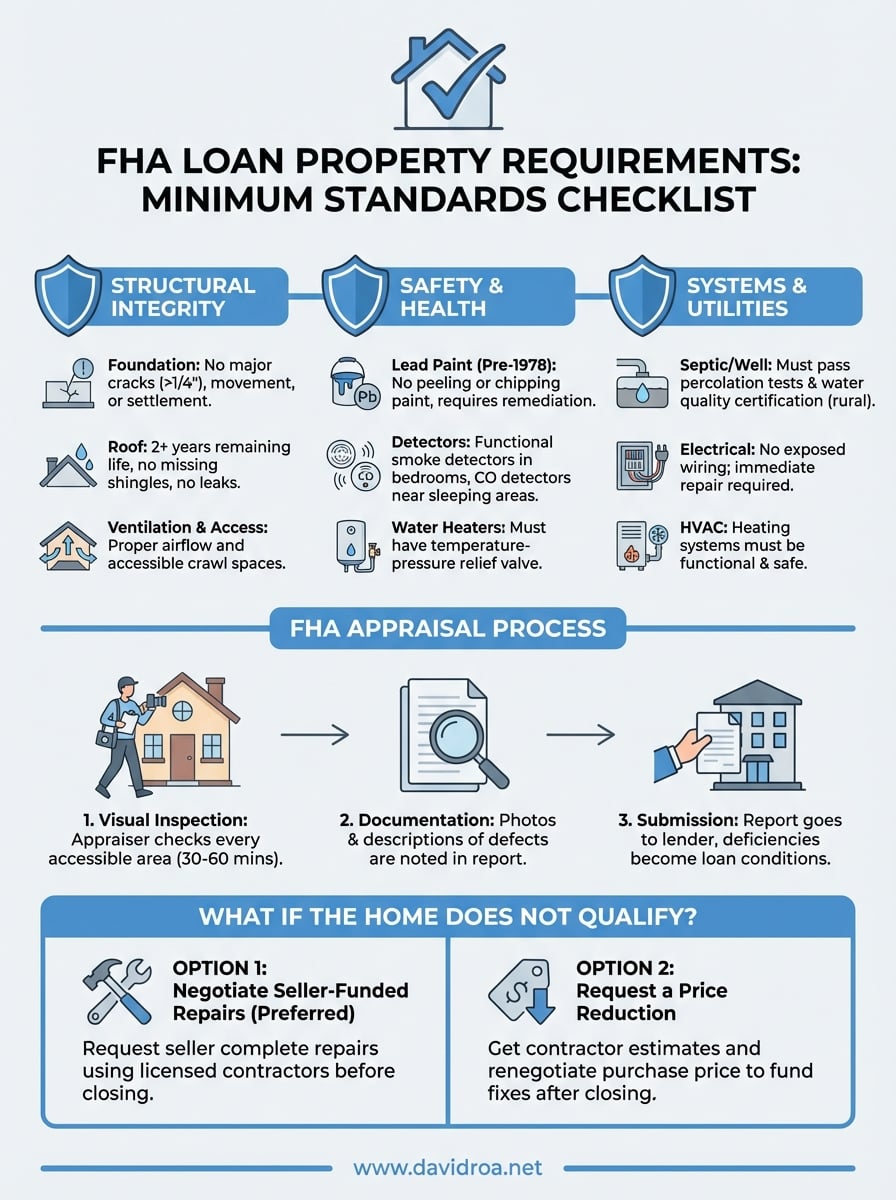

FHA minimum property standards checklist

The FHA divides their property requirements into three core categories that every home must pass before your loan closes. Every single item on this checklist gets inspected during your appraisal, and failure in any area requires repairs or a loan denial. Understanding these FHA loan property requirements upfront helps you evaluate properties before making an offer, saving time and money on homes that won't qualify.

Structural integrity requirements

Your home's foundation, roof, and framing must meet specific safety standards. Foundation cracks wider than 1/4 inch require engineering evaluation, and any visible structural movement or settlement needs documentation from a licensed professional. The roof must have at least two years of remaining life with no missing shingles, water damage, or sagging areas. Attics need proper ventilation, and crawl spaces require adequate access for inspection. Any structural repairs identified by the appraiser become mandatory conditions before closing.

Safety and health standards

Peeling paint on homes built before 1978 triggers lead-based paint testing and certified remediation. Your property must have safe access and egress from all habitable rooms, functional smoke detectors in every bedroom, and carbon monoxide detectors near sleeping areas. Water heaters need temperature-pressure relief valves, and any exposed electrical wiring requires immediate repair.

FHA appraisers will fail your loan if they spot safety hazards that could injure occupants or cause property damage.

Septic systems must pass percolation tests, and wells need water quality certification in rural areas.

How the FHA appraisal checks the property

The FHA appraisal is not a traditional home inspection that crawls through every closet and tests every outlet. Your appraiser arrives with a specific checklist tied to HUD's Minimum Property Standards, and their job focuses on three things: property value, safety hazards, and structural soundness. This inspection typically takes 30 to 60 minutes, depending on the home's size and condition, and the appraiser submits their findings directly to your lender within a few days.

The inspection process

Your appraiser walks through every accessible area of the property, including the attic, basement, and exterior grounds. They photograph defects, measure the home's square footage, and compare recent sales in your neighborhood to determine market value. Unlike a home inspector who you hire for detailed analysis, the FHA appraiser works independently and owes no loyalty to either buyer or seller. Their report goes straight to the lender, and any noted deficiencies become loan conditions that must be resolved before closing.

FHA appraisers focus on habitability and safety, not cosmetic issues like outdated kitchens or worn carpeting.

What gets documented

Every flagged issue lands in the appraisal report under "Subject To" or "Required Repairs" sections. Structural problems, safety violations, and any item affecting the home's livability get documented with photos and detailed descriptions. The appraiser also notes whether deficiencies require licensed contractor repairs or simple maintenance fixes, which determines your next steps after receiving the report.

Common issues that fail an FHA appraisal

Most FHA appraisals fail for preventable reasons that sellers could have fixed before listing. Roughly 15 to 20 percent of FHA appraisals require repair conditions before closing, and the most common failures involve safety hazards and deferred maintenance. Understanding these frequent problems helps you spot red flags during property tours, and you'll save time by avoiding homes that clearly violate FHA loan property requirements before making an offer.

Structural and exterior problems

Foundation cracks, roof damage, and peeling exterior paint trigger immediate repair requirements. Appraisers fail homes with water stains in attics or ceilings, missing handrails on stairs with four or more steps, and damaged siding that exposes wood framing. Properties built before 1978 face automatic scrutiny for any peeling or chipping paint, which requires certified lead remediation regardless of location. Drainage issues causing water to pool near the foundation or broken gutters also create appraisal conditions.

Exterior defects are the number one reason FHA loans stall during the appraisal phase.

Interior deficiencies

Non-functional appliances included in the sale, broken windows, and cracked floor tiles all require repair documentation before closing. Your appraiser will flag homes with missing smoke or carbon monoxide detectors, exposed electrical wiring, or plumbing leaks under sinks. Missing outlet covers, holes in walls larger than your fist, and any evidence of active pest infestation become mandatory repair conditions that halt your loan approval.

What to do if the home does not qualify

Your appraisal came back with repair conditions, and now you're stuck deciding whether to move forward or walk away. Most FHA loan property requirements can be resolved through seller-funded repairs or price adjustments, but you need to act quickly once deficiencies appear in the appraisal report. Your purchase contract likely includes an appraisal contingency that protects your earnest money if the property fails inspection, giving you three clear options depending on the severity of issues and seller cooperation.

Negotiate seller-funded repairs

Your first move should be requesting the seller complete all required repairs before closing. Present the FHA appraisal report to the seller's agent and ask for documented fixes from licensed contractors where required. Most sellers prefer making repairs over losing a buyer, especially if they've already accepted your offer and taken the property off market. Foundation issues, roof replacements, and lead paint remediation typically need contractor certification, while minor fixes like installing smoke detectors or repairing handrails can be seller-completed tasks.

Sellers who refuse repairs often face the same issues with the next FHA buyer, making cooperation their best financial option.

Request a price reduction instead

Sellers unwilling to handle repairs might agree to reduce the purchase price, letting you fund fixes after closing. Calculate repair estimates from licensed contractors and present documented quotes during renegotiation. You'll need enough cash reserves beyond your down payment to cover immediate repairs, and your lender must approve the reduced price before proceeding.

Quick recap and next steps

Understanding fha loan property requirements before making an offer saves you from deal-killing surprises during the appraisal process. Every FHA-financed home must meet minimum safety and structural standards, from foundation integrity to lead paint remediation, and your loan won't close until all deficiencies get resolved. Most issues are fixable through seller-funded repairs or price reductions, but you need to spot red flags early and negotiate repair contingencies into your purchase contract.

Your next move depends on where you are in the buying process. Start by touring properties with this checklist in mind, avoiding homes with obvious structural problems or deferred maintenance. Once you find a qualifying property, work with an experienced loan officer who understands how to navigate FHA appraisal conditions and coordinate repairs before closing. Get personalized guidance on FHA financing and property requirements to ensure your dream home meets every standard and your closing stays on track.