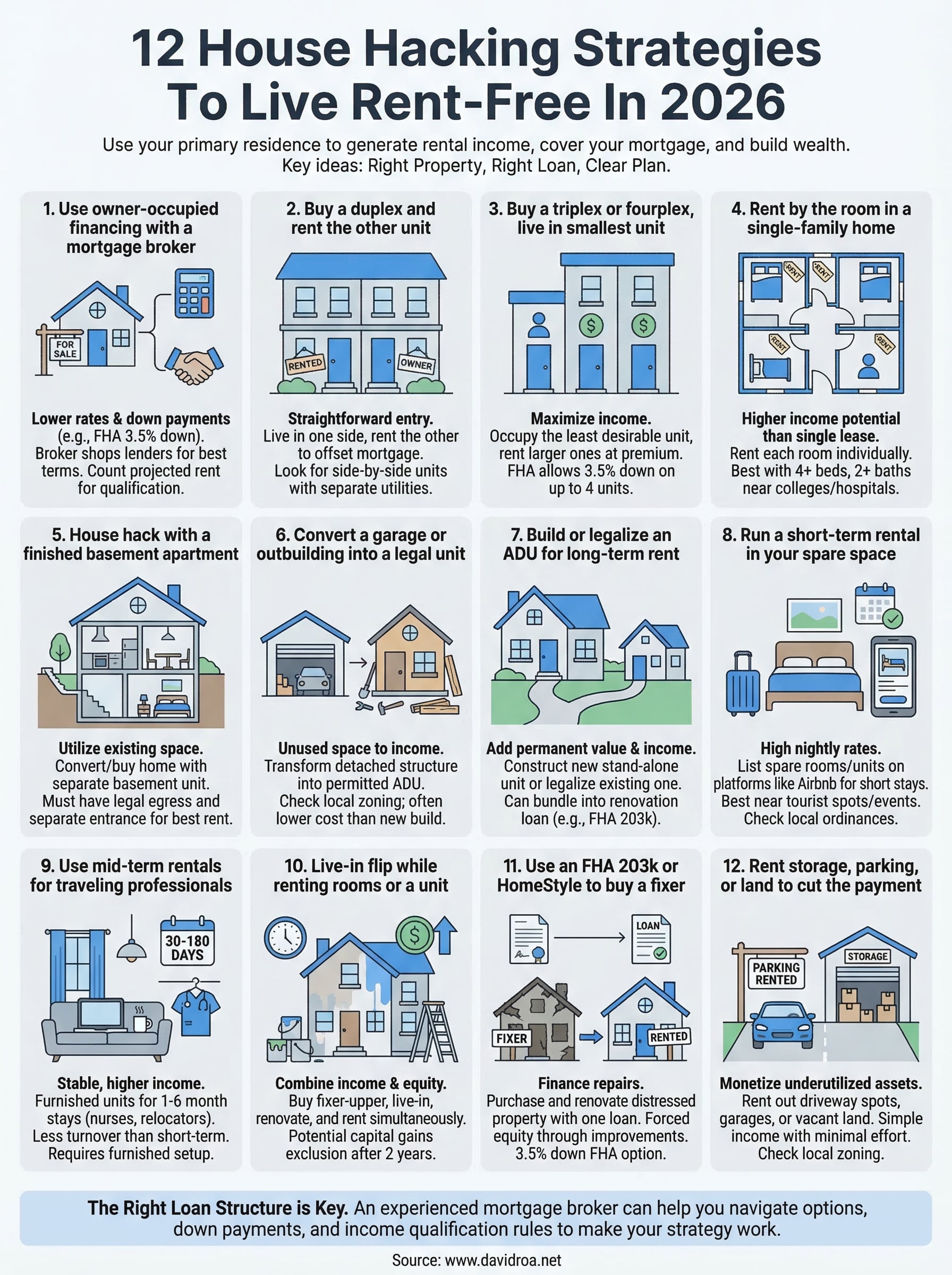

12 House Hacking Strategies To Live Rent-Free In 2026

Most people hand over 30% or more of their income to housing costs every single month. But what if your home actually paid you back? That's the core idea behind house hacking strategies, using your primary residence to generate rental income that covers your mortgage, and sometimes puts extra cash in your pocket.

Whether you're buying a duplex and renting out the other unit, converting a basement into an Airbnb, or getting creative with a multi-unit property, house hacking remains one of the most accessible paths into real estate investing. The best part? You don't need a massive portfolio or years of experience to start. You need the right property, the right loan, and a clear plan.

At David Roa, we've helped borrowers finance exactly these kinds of deals, from FHA purchases on multi-family homes to DSCR loans for investor-minded buyers, with over $150 million funded and 25+ years in the lending business. We see firsthand how the right financing turns a house hack from an idea into a wealth-building machine.

Below, you'll find 12 proven house hacking strategies you can use in 2026 to reduce or eliminate your housing costs, along with practical tips on financing, tenant management, and scaling your portfolio. Let's get into it.

1. Use owner-occupied financing with a mortgage broker

The single biggest advantage available to any house hacker is owner-occupied loan pricing. When you buy a property as your primary residence, lenders treat you as a lower-risk borrower, which means lower interest rates, smaller down payments, and easier qualification compared to a straight investment property purchase. Pairing that advantage with a knowledgeable mortgage broker turns financing into one of your sharpest tools.

How it works

You purchase a home, a single-family, duplex, triplex, or fourplex, and declare it as your primary residence. In exchange, you get access to loan programs that investors purchasing non-owner-occupied properties simply cannot use. These include FHA loans with as little as 3.5% down, conventional loans starting at 5% down on multi-family properties, and VA loans with zero down for eligible veterans. A mortgage broker shops those programs across multiple lenders to find the best rate and terms for your specific situation, something a single bank cannot do.

Working with a broker instead of going directly to one bank can save you thousands over the life of the loan, especially on a multi-unit property where every basis point matters.

Best property setup

The ideal setup for this house hacking strategy is a 2-to-4 unit multi-family property where you occupy one unit and rent the others. Single-family homes with an accessory dwelling unit (ADU) or a rentable basement also qualify. The key is that the property must be your legitimate primary residence, meaning you actually live there, not a secondary property you're pretending to occupy.

Financing and underwriting notes

Lenders allow you to use projected rental income from the other units to help qualify for the loan. On FHA loans for multi-family properties, lenders typically count 75% of the market rent on non-owner units toward your qualifying income. For conventional loans, the rules vary by lender, which is exactly why a broker can make a material difference. Your debt-to-income ratio (DTI) and credit score still matter, but the rental offset often makes it possible to qualify for a larger purchase than you could on your own income alone.

Numbers to run before you buy

Before you commit to a property, run a simple break-even analysis. Take your total monthly mortgage payment (principal, interest, taxes, insurance, and any HOA dues) and compare it against the realistic rent you can collect from the other units. Factor in a 5-10% vacancy rate and budget roughly 10-15% of gross rent for maintenance and repairs. If the rental income covers 80% or more of your payment from day one, you're looking at a strong candidate.

Risks, rules, and execution tips

The primary risk is an owner-occupancy requirement: most loan programs require you to move in within 60 days of closing and stay for at least 12 months. Violating that is loan fraud. Beyond that, screen tenants carefully, since they're living next door to you, and document everything in writing from day one. Work with a local real estate attorney to make sure your lease agreements comply with state and local landlord-tenant laws before you hand over a single key.

2. Buy a duplex and rent the other unit

Among all house hacking strategies, buying a duplex is the most straightforward entry point. You purchase a two-unit property, move into one side, and rent out the other. Your tenant's rent directly offsets your mortgage payment, and in many markets, it covers it entirely.

How it works

You own both units under one roof and one loan. The rental income from the vacant unit flows to you as the landlord-owner, and you apply it against your monthly housing costs. Because you live on-site, you also manage the property more easily than a remote landlord ever could.

Best property setup

Look for a duplex with two similarly sized units so you can switch which side you occupy if needed, or rent both when you eventually move out. Side-by-side layouts tend to appeal to better tenants than stacked units because each unit feels more like a standalone home. Separate entrances, separate utilities, and good soundproofing all increase what you can charge for rent.

Financing and underwriting notes

A duplex with an owner-occupant qualifies for FHA financing at 3.5% down and conventional loans starting at 5% down. Lenders will count 75% of the market rent on the vacant unit toward your qualifying income on FHA loans, which can meaningfully increase your purchase power. A mortgage broker can compare programs across multiple lenders to find the best fit for your credit profile and income situation.

The ability to use future rental income to qualify is one of the biggest financial advantages of buying a duplex as your primary residence.

Numbers to run before you buy

Pull comparable rental listings in the immediate area to estimate realistic rent for the vacant unit. Subtract a 7% vacancy allowance and 10% for maintenance, then compare the net figure to your total housing payment. If that number gets you to 50% or more coverage, the deal is worth serious consideration.

Risks, rules, and execution tips

Your biggest exposure is a vacancy or non-paying tenant, since you're living right next door. Screen applicants thoroughly, verify income at 3x the monthly rent, and use a written lease that complies with your state's landlord-tenant statutes. Keep a three-month cash reserve so a single vacancy doesn't put your mortgage at risk.

3. Buy a triplex or fourplex and live in the smallest unit

Scaling up from a duplex to a triplex or fourplex is one of the most powerful house hacking strategies available to owner-occupants. With two or three income-producing units working alongside your own, it becomes genuinely possible to cover your entire mortgage payment and still have cash left over each month.

How it works

You purchase a 3-to-4 unit residential property, move into one unit as your primary residence, and rent out the remaining units to tenants. The combined rental income from those units offsets your mortgage, and in high-rent markets, it often exceeds your total monthly payment. You're building equity while other people's rent pays the bill.

Best property setup

The smartest move is to occupy the smallest or least desirable unit and rent out the larger, more attractive units at premium rates. Ground-floor units near parking, units with private outdoor space, or those with updated kitchens command the highest rents. Keeping your own space modest maximizes the income you collect and lowers your personal cost basis.

On a well-purchased fourplex, three renting tenants can cover 100% of your housing costs while you build equity from day one.

Financing and underwriting notes

A fourplex is the largest property you can finance with an FHA or conventional owner-occupied loan. FHA allows as little as 3.5% down on a four-unit property, and lenders can count 75% of the projected rents from the other three units toward your qualifying income. Once you move to a five-unit building, you cross into commercial financing territory, so a fourplex sits at the sweet spot for owner-occupant buyers.

Numbers to run before you buy

Add up the gross market rent for all non-owner units, apply a 8% vacancy factor, subtract 12% for maintenance and management, then compare the result to your full mortgage payment. On a solid fourplex, that net income number should cover 90% to 110% of your payment.

Risks, rules, and execution tips

Managing three tenants simultaneously while living on the property demands solid systems from day one. Use a standardized lease, collect separate security deposits for each unit, and set up a dedicated landlord bank account to track income and expenses cleanly. Keep a reserve equal to two months of gross rent to handle simultaneous vacancies without stress.

4. Rent by the room in a single-family home

Renting by the room turns a standard single-family home into a multi-income property without the complexity of buying a multi-unit building. Instead of renting to one household, you rent each bedroom individually, often generating 30 to 50% more income than a single-family rental would produce under a traditional lease.

How it works

You purchase a single-family home, move into one bedroom as your primary residence, and rent out the remaining bedrooms to separate tenants. Each tenant signs their own individual room rental agreement, pays their own rent, and shares common areas like the kitchen, living room, and bathrooms. Because each room generates its own income stream, your total rental revenue often covers most or all of your mortgage payment.

Best property setup

A home with four or more bedrooms and at least two full bathrooms produces the best results. More bathrooms reduce friction between tenants and allow you to charge higher per-room rents. Look for properties with good natural separation between bedrooms, solid closet space in every room, and proximity to universities, hospitals, or downtown employment corridors where demand for single-room rentals stays consistently high.

Markets near colleges or major medical centers often support room rents that far exceed what a single-family lease would generate from the same property.

Financing and underwriting notes

You finance this property as a standard owner-occupied purchase, which gives you access to FHA, conventional, and VA loan programs. Lenders underwrite the loan based on your personal income since there is no established rental history on the rooms yet. A mortgage broker can help you structure the loan correctly from the start so you're not locked out of better programs later.

Numbers to run before you buy

Multiply your expected per-room rent by the number of rooms you plan to rent, then apply a 10% vacancy factor. Compare that net figure to your full monthly mortgage payment including taxes and insurance. If rented rooms cover 75% or more of your payment, the property is a strong candidate.

Risks, rules, and execution tips

Shared living arrangements require clear house rules in writing covering guests, quiet hours, kitchen use, and cleaning responsibilities. Check local ordinances before closing, since some cities cap the number of unrelated tenants per dwelling. Keep a written lease for every tenant, collect a separate security deposit from each, and screen all applicants with the same income and background criteria you would apply to any rental.

5. House hack with a finished basement apartment

A finished basement apartment is one of the most underrated house hacking strategies available to homeowners who already live in, or plan to buy, a single-family home. You gain a separate income-producing unit without purchasing a multi-family property or managing the added complexity of shared living spaces.

How it works

You convert or purchase a home that already has a finished basement unit with its own entrance, bathroom, and kitchen or kitchenette. You occupy the main floors and rent out the lower unit to a long-term tenant. Your tenant lives independently, you both access your own spaces separately, and their monthly rent payment directly reduces your housing cost.

Best property setup

Look for a home where the basement already has a walkout or exterior side entrance, separate electrical service, and ceiling heights of at least seven feet. Units with a full bathroom and a functional kitchen, even a compact one, command the highest rents. Properties in established neighborhoods close to public transit or employment centers attract reliable tenants who will stay long-term.

A basement unit with a private entrance rents significantly faster and at a higher rate than one that requires tenants to pass through shared interior space.

Financing and underwriting notes

You finance the home as a primary residence, which keeps your loan options wide open. If the basement unit has a separate entrance and is legally recognized as a rental unit in your county, some lenders will allow you to count 75% of the projected rent toward your qualifying income. A mortgage broker can identify which lenders apply that rental offset and structure your loan to take full advantage of it.

Numbers to run before you buy

Estimate realistic basement rent using active listings for comparable units in the same zip code. Subtract a 7% vacancy allowance and 10% for maintenance, then measure the net figure against your total monthly payment. If the basement rent covers 40% or more of your housing cost, the deal significantly improves your cash position.

Risks, rules, and execution tips

Check your local zoning code and building department before closing to confirm the basement unit is legally permitted as a rental. Unpermitted units can trigger fines or forced vacancy. Budget for a carbon monoxide detector, proper egress windows, and any required fire separation between floors to meet code and protect your tenant.

6. Convert a garage or outbuilding into a legal unit

A detached garage, carriage house, or outbuilding already sitting on your property is unused square footage with real income potential. Converting it into a legal rental unit is one of the more hands-on house hacking strategies available to existing homeowners, and it also works well for buyers who specifically target properties with convertible structures already on site.

How it works

You transform an existing non-residential structure into a permitted, habitable rental unit by adding insulation, HVAC, plumbing, electrical service, and proper egress. Once the local building department inspects and signs off on the work, you can rent the unit at market rate while you continue to occupy the main house. The conversion often costs less than a ground-up ADU build because the foundation and framing already exist.

Best property setup

Target properties with a detached garage of at least 400 square feet, or a carriage house, barn, or workshop already on the lot. A single-story detached structure with existing electrical service reduces your conversion costs significantly. Properties in areas with consistent demand for small studio or one-bedroom units produce the fastest payback on the conversion investment.

A permitted conversion commands much higher rents and protects you legally compared to renting an unpermitted space.

Financing and underwriting notes

You purchase the property as a primary residence and retain all the standard loan options that come with it, including FHA, conventional, and VA programs. If you need to finance the conversion itself, a renovation loan such as the FHA 203k can bundle the purchase price and construction costs into one mortgage, which avoids a second loan at a higher rate.

Numbers to run before you buy

Get two or three contractor bids on the conversion before you close so you understand your total project cost. Divide that number by the expected monthly rental income to calculate your payback period. A $40,000 conversion that produces $1,200 per month in rent pays back in roughly 33 months.

Risks, rules, and execution tips

Your local zoning and building department controls whether a garage conversion is permitted on your specific lot. Some municipalities prohibit them entirely, while others require minimum lot sizes. Pull the zoning rules before you close, not after. Also budget for unexpected costs like adding a sewer lateral or upgrading your electrical panel, both of which can significantly increase your project cost.

7. Build or legalize an ADU for long-term rent

An accessory dwelling unit (ADU) is a self-contained residential unit built on the same lot as your primary home. Unlike a garage conversion, you're either constructing a new structure from scratch or bringing an existing unpermitted unit up to code. Either path adds permanent, appraised value to your property while generating steady long-term rental income.

How it works

You add a permitted, stand-alone unit to your lot, either a detached backyard cottage, an attached addition, or a unit above a garage, and rent it to a long-term tenant. The tenant lives completely independently from you with their own entrance, kitchen, and bathroom. That monthly rent then works directly against your mortgage payment, which is the core goal of most house hacking strategies.

Best property setup

Properties with larger lots and rear-yard setbacks that meet local ADU ordinances work best. A minimum lot size of 6,000 square feet gives you room to build a detached unit without crowding the main structure. Areas with strong rental demand and limited housing inventory, like urban infill neighborhoods, tend to support the highest ADU rents.

A permitted ADU adds measurable appraised value to your home and strengthens your refinance options down the road.

Financing and underwriting notes

You can bundle a new ADU build into a renovation loan such as the FHA 203k or Fannie Mae HomeStyle, which rolls construction costs into your primary mortgage. This avoids taking out a high-rate construction loan separately. A mortgage broker can compare both programs and match you with the lender that applies the best rental income offset to your qualifying income.

Numbers to run before you buy

Get firm contractor bids before you close or commit to the build. Divide your total ADU construction cost by the expected monthly rent to find your payback period. A $60,000 build renting at $1,400 per month pays back in roughly 43 months.

Risks, rules, and execution tips

State and local governments set ADU permitting rules, and they vary widely by jurisdiction. California, for example, has streamlined ADU approval, while other states add significant restrictions. Confirm utility connection requirements and impact fees before you finalize your budget, since those costs catch many first-time builders off guard.

8. Run a short-term rental in your spare space

Short-term rentals on platforms like Airbnb let you monetize spare bedrooms, a finished basement, or a detached unit without committing to a long-term tenant. This approach works especially well in markets with strong tourism, business travel, or event-driven demand, and it sits among the highest-earning house hacking strategies on a per-night basis.

How it works

You list one or more rooms, or a separate unit on your property, on a short-term rental platform and host guests for stays typically ranging from one night to a few weeks. Guests pay a nightly rate that often exceeds what a long-term tenant would pay for the same space on a monthly basis. The income you collect each month goes directly toward reducing your housing payment, and in strong markets it can cover the entire mortgage.

Short-term rental rates in high-demand markets can run two to three times what the same space would earn under a standard 12-month lease.

Best property setup

Properties near tourist attractions, convention centers, airports, or major universities consistently outperform those in isolated residential neighborhoods. A private entrance for the rental space, a dedicated bathroom, and in-unit laundry all command higher nightly rates and better reviews, which drives more bookings over time.

Financing and underwriting notes

You purchase the property as a primary residence, which gives you access to conventional, FHA, and VA loan programs. Lenders underwrite the loan on your personal income since short-term rental income lacks the documented history most lenders require at origination. A mortgage broker can identify lenders who apply the most favorable terms for your income profile.

Numbers to run before you buy

Research active listings in the same zip code using publicly available occupancy and rate data. Multiply your expected nightly rate by a realistic 60% occupancy figure to get a conservative monthly income estimate, then compare that number to your total monthly mortgage payment.

Risks, rules, and execution tips

Many cities have passed short-term rental ordinances that require permits, cap the number of rental nights per year, or ban them in certain zones entirely. Check your local regulations before you close, not after you've already bought the property. Also review your homeowner's insurance policy, since standard policies typically do not cover short-term rental activity without a specific rider.

9. Use mid-term rentals for traveling professionals

Mid-term rentals target a specific tenant type: traveling nurses, corporate relocators, remote workers, and contractors who need furnished housing for one to six months. These renters typically pay premium rates for furnished units and cause far less wear and tear than short-term guests, making this one of the more dependable house hacking strategies for homeowners who want steady income without constant turnover.

How it works

You furnish a spare room, basement unit, or separate living space on your property and list it on corporate housing platforms or networks that connect landlords with traveling professionals. Tenants sign fixed-term leases of 30 to 180 days, which keeps your space occupied for longer stretches while still allowing you to reset rates between stays.

Common tenant types for mid-term rentals include:

- Travel nurses on hospital assignments

- Corporate employees on temporary relocation

- Remote workers seeking furnished short-stay housing

- Contractors working local projects for several months

Best property setup

Properties near hospitals, large corporate campuses, or universities generate the most consistent mid-term demand. Your rental space needs a fully furnished bedroom, a functional kitchen or kitchenette, high-speed internet, and dedicated laundry access. Traveling professionals have high expectations for comfort, so updated finishes directly affect what you can charge.

Traveling nurses alone account for a significant share of mid-term rental demand, and that demand stays active year-round in markets with large hospital systems.

Financing and underwriting notes

You buy the property as a primary residence, which keeps FHA, conventional, and VA loan programs on the table. Lenders underwrite based on your documented personal income since mid-term rental history rarely exists at the time of purchase. A mortgage broker can compare lenders and find the program that best fits your income profile and down payment.

Numbers to run before you buy

Use a conservative 75% occupancy rate across 12 months to account for gaps between tenants. Multiply your expected monthly rental rate by nine months and compare that figure to your total annual housing cost including taxes and insurance.

Risks, rules, and execution tips

Check whether your city classifies stays under 30 days as short-term rentals, since that triggers different permit requirements. Budget for furniture replacement and deep cleaning costs between tenants, and always use a written lease that clearly defines the tenancy term, utilities included, and house rules.

10. Live-in flip while renting rooms or a unit

A live-in flip combines two profitable strategies at once: you buy a distressed property, move in as the owner-occupant, and renovate it over 12 to 24 months while collecting rent from spare rooms or a separate unit on the same property. The rental income reduces your holding costs while you systematically add value to the asset before you sell.

How it works

You purchase a fixer-upper as your primary residence, which qualifies you for owner-occupied loan pricing, then rent out bedrooms or a secondary unit while you renovate. When you sell after living there for at least two years, you may qualify for the IRS Section 121 capital gains exclusion, up to $250,000 for single filers and $500,000 for married couples filing jointly.

Combining rental income with a capital gains exclusion makes the live-in flip one of the most tax-efficient house hacking strategies available to owner-occupants.

Best property setup

Target three-to-four bedroom single-family homes or small multi-family properties in neighborhoods with measurable price appreciation. Properties with a rentable unit already in place reduce your time to the first rent check. Focus on cosmetic distress over structural problems to keep renovation costs manageable and your timeline realistic.

Financing and underwriting notes

You access standard owner-occupied loan programs since you intend to live in the property. A renovation loan such as the FHA 203k or Fannie Mae HomeStyle bundles your purchase price and repair budget into one mortgage, which keeps your financing costs lower than carrying a purchase loan and a separate construction loan at the same time.

Numbers to run before you buy

Run these figures before you commit to any live-in flip:

- Purchase price plus estimated renovation cost vs. projected after-repair value (ARV)

- Monthly rental income from rooms or a unit vs. your total mortgage payment

- Projected capital gains exclusion at sale based on your filing status

Risks, rules, and execution tips

Living through an active renovation is genuinely disruptive, so plan your project sequence to keep your personal living area functional throughout the work. The two-year residency requirement for the capital gains exclusion is firm, so document your occupancy carefully with utility bills and mail records from day one.

11. Use an FHA 203k or HomeStyle to buy a fixer

Renovation loans give you a path to buy a property that most buyers skip over because it needs work, and then fix it up using financing that's already built into your mortgage. This approach sits at the intersection of two powerful house hacking strategies: accessing owner-occupied loan pricing and forcing equity through targeted improvements that unlock higher rents.

How it works

You purchase a distressed or outdated property and roll the cost of repairs directly into one mortgage. The FHA 203k covers structural and cosmetic work, while the Fannie Mae HomeStyle loan allows a broader range of improvements including luxury upgrades. Both programs require you to occupy the property as your primary residence, so you keep your low down payment and favorable rate intact.

Renovation loans let you buy a property below market value, improve it with borrowed funds, and rent out units at post-renovation market rates, all under one mortgage payment.

Best property setup

Target multi-unit properties or single-family homes with a rentable unit that are priced low due to dated finishes, deferred maintenance, or an outdated layout. Properties that need cosmetic work, new kitchens, updated bathrooms, or fresh systems produce the best return on renovation dollars because costs stay predictable and timelines stay manageable.

Financing and underwriting notes

The FHA 203k requires a 3.5% down payment and a minimum 580 credit score for most lenders. The HomeStyle loan runs through conventional underwriting and allows up to 97% loan-to-value on a primary residence. A mortgage broker can compare both programs side by side and factor in projected post-renovation rent to strengthen your qualification.

Numbers to run before you buy

Calculate your total loan amount as purchase price plus renovation budget, then compare the resulting monthly payment against projected rent from the rentable unit. Your post-renovation rent should cover at least 50% of your total payment to make the deal financially sound.

Risks, rules, and execution tips

Both programs require you to work with approved contractors and follow a draw schedule managed through the lender, which adds administrative steps. Get detailed contractor bids in writing before closing and build a 10-15% contingency into your renovation budget to absorb unexpected costs without derailing your timeline.

12. Rent storage, parking, or land to cut the payment

Not every house hacking strategy requires a separate unit or a tenant living under your roof. Renting out unused space on your property, whether that's a detached garage, a driveway spot, an empty lot, or a storage shed, can generate reliable monthly income with almost no ongoing work on your part.

How it works

You identify underutilized space on your property and rent it directly to people who need it. A single parking spot in a dense urban neighborhood can rent for $100 to $400 per month. A detached garage used for storage can command even more. Land you're not actively using can be leased to neighboring businesses, gardeners, or event operators depending on your zoning.

In high-density urban markets, a single parking spot can generate enough monthly income to cover a meaningful portion of your mortgage payment.

Best property setup

Properties in dense urban or suburban areas where parking and storage are scarce produce the best results. A detached garage, a wide driveway, a vacant side yard, or a fenced rear lot all have income potential. Proximity to transit stations, sports venues, hospitals, or commercial districts increases demand significantly.

Financing and underwriting notes

You finance this property as a standard owner-occupied purchase, so all conventional, FHA, and VA loan programs remain available. Lenders do not typically count storage or parking income at origination since it has no lease history, so your personal income carries the full qualification weight. A mortgage broker can identify programs that offer the most flexibility for your financial profile.

Numbers to run before you buy

List every rentable asset on the property, assign a conservative monthly rate to each based on local comparables, and total the projected income. Subtract a 10% vacancy estimate, then compare the net figure against your total monthly housing payment to understand how much this income stream reduces your out-of-pocket cost.

Risks, rules, and execution tips

Check your local zoning ordinances before renting any space commercially, since some municipalities restrict paid parking or storage on residential lots. Use a simple written agreement for every rental arrangement, even informal ones, to protect yourself if a dispute arises.

Your next move

You now have 12 proven house hacking strategies to work with, from buying a fourplex with FHA financing to renting a parking spot in your driveway. The common thread across all of them is this: the right loan structure determines whether your strategy actually pencils out or falls apart before you close. Down payment requirements, rental income offsets, and qualification rules vary significantly by loan program, and choosing the wrong one can cost you thousands before you even hand over a key.

That's exactly where an experienced mortgage broker earns their value. At David Roa, we've spent 25 years and over $150 million funded helping buyers match the right loan to the right property, including multi-family purchases, renovation loans, and DSCR products for investors. If you're ready to run the numbers on a specific deal or just want to understand your options, reach out to David Roa and let's build a financing plan that makes your next property work for you.