How Does Refinancing a Mortgage Work? Steps, Costs & Timing

Refinancing replaces your current mortgage with a new one, different rate, different terms, sometimes a different loan amount entirely. That's the short answer to how does refinancing a mortgage work. But the real question most homeowners have isn't about the definition. It's about whether refinancing actually makes sense for their situation, what the process looks like from application to closing, and how much it's going to cost them upfront versus what they'll save over time.

After funding over $150 million in loans across residential, commercial, and investment properties, I've walked thousands of borrowers through refinance decisions. Some saved hundreds per month. Others realized the timing wasn't right and held off. Both outcomes count as wins because refinancing only works when the numbers back it up. At David Roa, we treat every refinance conversation the same way, starting with your actual financials, not a sales pitch.

This guide breaks down each step of the refinancing process, from evaluating your current loan to closing on the new one. You'll learn what lenders look at, what fees to expect, and how to figure out whether refinancing puts you ahead or behind. No guesswork, just the information you need to make a confident decision.

What refinancing is and what changes

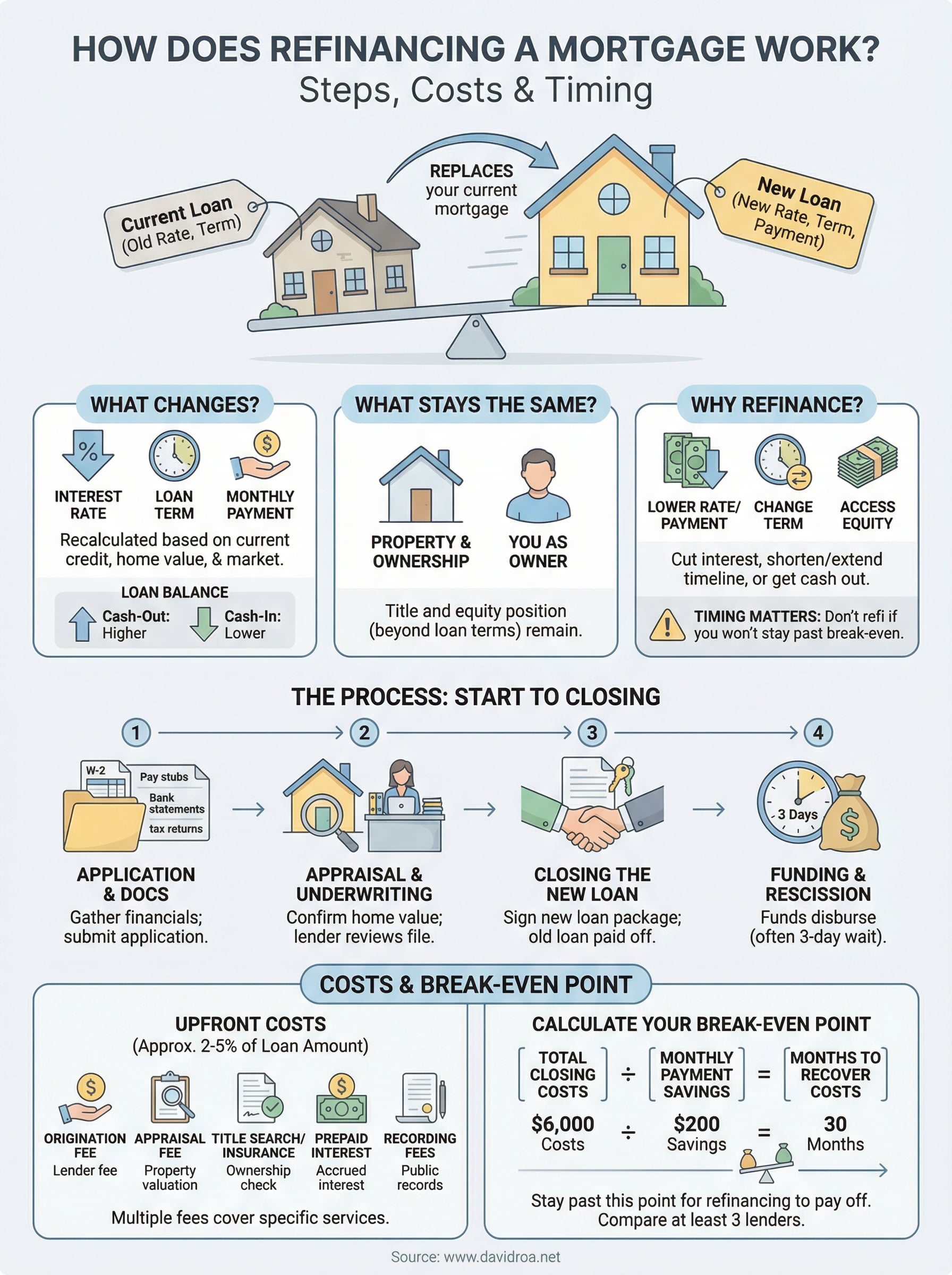

When you refinance, your current mortgage gets paid off and a completely new loan takes its place. You're not modifying your existing loan or renegotiating terms with your current servicer. You go through a full loan application, just like when you first bought the home, and the proceeds from the new loan pay off the old balance. That's the foundation of how does refinancing a mortgage work: one loan closes, a new one opens, and the slate resets based on where you stand today financially.

The loan that replaces your current one

The new loan comes from a lender, which can be your current one or a completely different institution. Your original loan closes permanently, and you begin making payments on the new one. The new loan carries its own interest rate, its own term length, and its own monthly payment. None of those figures carry over from the old loan automatically. Every detail gets recalculated based on your current credit profile, your home's appraised value, and the rate environment at the time you apply.

The rate you locked in years ago has no bearing on what you'll get today. Your new loan gets priced entirely on current market conditions and your current financial standing.

Lenders pull your credit, order a new appraisal, verify your income, and underwrite the loan from scratch. You don't get automatic approval as a reward for years of on-time payments. Those payments do show up as positive credit history, which can strengthen your score and support your application, but the underwriting process treats this as a brand-new loan regardless.

What actually changes on your mortgage

The three things that shift most often when you refinance are your interest rate, your loan term, and your monthly payment. Sometimes all three change, sometimes just one or two, depending on your goal. If you refinance from a 30-year loan at year 10 into a new 30-year loan, you reset your payoff timeline by another decade. If you move into a 15-year term instead, you shorten the payoff window but will likely see a higher monthly payment even at a lower rate.

Your loan balance can also change. A cash-out refinance lets you borrow more than you currently owe and receive the difference in cash. In that scenario, your new loan amount is higher than your current payoff balance. Conversely, if you bring cash to closing to reduce your balance or buy down your rate, your new loan amount comes in lower than what you owed before.

What stays the same

Your property and your ownership don't change. Refinancing has no effect on the title to your home or your equity position beyond what the new loan terms create. Your home is still yours, and you remain the owner of record. The lien on the property gets updated to reflect the new lender, but no ownership clock resets.

The basic structure of how you pay stays the same as well. You still make one monthly payment that covers principal and interest. Your escrow account for property taxes and homeowners insurance typically transfers to the new servicer or gets re-established at closing. The mechanics of homeownership don't change, only the loan terms behind it do.

Why people refinance and when it makes sense

Most refinances come down to one of three goals: lower your rate, change your loan term, or pull cash out of your equity. Understanding which goal applies to your situation is the first step before you look at current rates or talk to a lender. Refinancing for the wrong reason, or at the wrong time, can cost you more than staying put.

Lowering your rate and monthly payment

The most common reason people refinance is to cut their interest rate and reduce what they pay each month. If rates drop significantly after you close on your original loan, refinancing lets you capture that lower rate on your remaining balance. Even a reduction of 0.75 to 1 percentage point can translate to meaningful savings over the life of the loan, depending on your balance and remaining term.

The savings from a lower rate only matter if you stay in the home long enough to recover the closing costs you paid upfront to get there.

Borrowers who bought homes when rates spiked often refinance as soon as conditions improve. If your financial profile has also strengthened since you first got your loan, meaning a higher credit score or lower debt load, you may qualify for an even better rate than market averages suggest.

Changing your loan term or accessing equity

Some borrowers refinance not to lower their payment but to shorten their payoff timeline. Moving from a 30-year to a 15-year loan costs more per month but cuts the total interest you pay significantly. Other borrowers extend their term to reduce monthly cash obligations during a period of financial pressure, freeing up cash flow even if it means paying longer.

Cash-out refinancing serves a different purpose entirely. If your home has appreciated and you've built substantial equity, you can borrow more than your current payoff balance and receive the difference as cash. Homeowners use those funds for renovations, business capital, or consolidating higher-interest debt.

When the numbers actually support refinancing

Refinancing carries closing costs that typically run 2 to 5 percent of the loan amount. That upfront expense means refinancing isn't automatically a good move just because rates dropped. You need to calculate your break-even point: how many months of payment savings it takes to recover what you spent at closing.

If you plan to sell or move within two to three years, the math rarely works in your favor. That's the timing filter most homeowners skip, and it's one of the most important steps in understanding how does refinancing a mortgage work in practice.

Types of mortgage refinances

Not every refinance works the same way, and choosing the wrong type can cost you money even when rates move in your favor. Understanding how does refinancing a mortgage work across different loan structures helps you match the right program to your actual goal before you contact a lender or pull your credit.

Rate-and-term refinance

A rate-and-term refinance changes your interest rate, your loan term, or both, without significantly altering your loan balance. The new loan pays off your existing mortgage, and you start fresh with better terms. This is the most common refinance type, and it's what most borrowers pursue when they want to reduce their monthly payment or shorten the payoff timeline. Your equity position stays roughly intact, and the purpose is straightforward: improve the terms without changing how much you owe.

Rate-and-term refinances also cover switching from an adjustable-rate mortgage to a fixed-rate loan. If you bought with an ARM and rates have risen since closing, locking in a fixed rate through a refinance protects your payment from future adjustments and brings predictability back to your monthly budget.

Cash-out refinance

A cash-out refinance lets you borrow more than your current payoff balance and collect the difference as cash at closing. If you owe $180,000 on a home worth $300,000, you could refinance into a $230,000 loan and receive $50,000 at close. Homeowners direct those funds toward renovations, paying down higher-interest debt, or investing in a business or additional property. Your loan balance increases, so expect your monthly payment to climb even if you secure a lower rate.

Cash-out refinancing works best when the asset or expense you're funding generates savings or returns that outpace the added interest cost on the larger balance.

Streamline and cash-in refinances

Government-backed loans like FHA and VA mortgages include streamline refinance programs that cut documentation requirements and processing time. You skip the full appraisal in many cases, and underwriting moves faster because you stay within the same loan program. A cash-in refinance runs in the opposite direction: you bring funds to closing to reduce your balance, lower your loan-to-value ratio, and either qualify for a better rate or remove private mortgage insurance from your payment. Both tools serve specific situations and won't apply to every borrower.

Steps in the refinance process from start to closing

Understanding how does refinancing a mortgage work in practice means knowing what happens between the day you contact a lender and the day you sign at the closing table. The process mirrors a purchase loan application in most ways, but the timeline moves faster if your financial documents are organized and your home appraises without issues.

Application and document gathering

Your refinance begins the moment you submit a formal application with a lender. From there, expect to pull together pay stubs, W-2s, tax returns from the last two years, bank statements, and your current mortgage statement. Self-employed borrowers and investors using DSCR loans may need additional items like business returns or rental lease agreements to verify income.

Getting your documents ready before you apply cuts processing time and reduces the chance of delays once underwriting starts.

Here's what lenders typically request at application:

- Last 30 days of pay stubs or proof of income

- Two years of W-2s or federal tax returns

- Two to three months of bank statements

- Current mortgage statement showing your payoff balance

- Homeowners insurance declarations page

Appraisal and underwriting

Once your application is in, the lender orders a home appraisal to confirm your property's current market value. That appraised value sets your loan-to-value ratio, which affects the rate you qualify for and determines whether a cash-out refinance is even on the table. Streamline programs through FHA or VA loans sometimes waive the appraisal, but most conventional refinances require one.

Underwriting follows the appraisal. The underwriter reviews your entire financial file, including credit history, income documentation, and the appraisal report. Expect requests for additional items called conditions before the lender issues final approval. Responding to those requests quickly keeps your closing date from slipping.

Closing on the new loan

Closing a refinance works similarly to a purchase closing. You review and sign a new loan package, and the lender funds the loan, which pays off your existing mortgage directly. Most refinances on a primary residence include a three-day rescission period, meaning funds don't disburse until three business days after you sign.

Costs, break-even point, and who pays

Refinancing isn't free, and understanding what you'll spend upfront is just as important as knowing what you'll save each month. Most homeowners focus on the new rate and ignore the cost side of the equation, which is exactly how does refinancing a mortgage work against you if the timing is off. Closing costs on a refinance typically run 2 to 5 percent of the loan amount, so on a $250,000 loan, expect to pay somewhere between $5,000 and $12,500 before you see a single dollar in savings.

What closing costs cover

Refinance closing costs aren't one single fee. They're a collection of charges from multiple parties, each covering a specific service in the transaction. Knowing where each dollar goes helps you evaluate lender estimates and spot any fees that seem out of line.

Common refinance closing costs include:

- Origination fee: Charged by the lender for processing the loan, usually 0.5 to 1 percent of the loan amount

- Appraisal fee: Typically $300 to $600 depending on your property and location

- Title search and title insurance: Confirms clean ownership and protects the lender's interest in the property

- Prepaid interest: Covers the interest that accrues between your closing date and your first payment due date

- Recording fees: Paid to the county or municipality to update public records with the new lien

Calculating your break-even point

Your break-even point is the number of months it takes for your monthly savings to cover what you paid at closing. Divide your total closing costs by your monthly payment reduction, and the result tells you how long you need to stay in the home before refinancing actually pays off.

If your break-even point is 36 months and you plan to sell in two years, refinancing costs you money rather than saves it.

Running this calculation before you apply is one of the most practical steps you can take. If you're not certain how long you'll hold the property, a lender can help you model different scenarios based on your actual payoff balance and current rate options.

Rolling costs into the loan

Some lenders offer a no-closing-cost refinance, which wraps your fees into the loan balance or offsets them through a slightly higher interest rate. You avoid a large upfront payment, but you pay for those costs over time through a higher balance or a higher rate. This option works well if you're short on cash at closing or expect to refinance again in a few years before the cost difference compounds.

Timing, credit impact, and common refinance mistakes

Knowing how does refinancing a mortgage work on paper doesn't automatically tell you when the right moment is to pull the trigger. Timing a refinance poorly can erase the savings you're chasing before you ever see them, and a few common mistakes accelerate that outcome faster than most borrowers expect.

When to refinance and when to wait

The best time to refinance is when your monthly savings clearly outpace your closing costs within a timeframe that matches how long you plan to keep the property. Rate drops alone don't make refinancing smart. You also need to account for how much principal you've already paid down, since resetting to a new 30-year term late in your existing loan means restarting the interest-heavy years of amortization even at a lower rate.

Refinancing in year 22 of a 30-year mortgage into another 30-year loan can cost you more in total interest than simply finishing your original loan at the higher rate.

How refinancing affects your credit

Applying for a refinance triggers a hard credit inquiry, which can lower your score by a few points temporarily. Shopping multiple lenders within a 14 to 45-day window limits the damage because FICO scoring models treat those inquiries as a single event. Once the new loan opens, your credit history length and your payment record on the new account both factor into your score going forward, so on-time payments rebuild any small dip faster than most borrowers expect.

Mistakes that cost you money

Refinancing without comparing at least three lender estimates is one of the most expensive shortcuts borrowers take. Rates and fees vary more than most people realize, and the lender with the lowest advertised rate doesn't always offer the best deal once origination fees and points are factored in. Skipping the break-even calculation is another costly error. Borrowers who move forward without confirming they'll stay in the home long enough to recover their closing costs often end up worse off than if they had done nothing, so running the math before you apply protects your long-term financial position.

Next steps

Now that you understand how does refinancing a mortgage work from application through closing, the next move is running your own numbers. Pull your current mortgage statement, note your remaining balance and interest rate, and calculate how much your monthly payment would change under today's rate environment. Then estimate your break-even point using your projected closing costs divided by your monthly savings. That single calculation tells you more than any general advice can.

Refinancing rewards borrowers who prepare before they apply. Organized financial documents, a clear goal, and a firm timeline for how long you plan to hold the property give you a stronger position when you sit down with a lender. If the math works and the timing fits, refinancing can meaningfully reduce what you spend over the life of your loan.

Connect with David Roa to review your current loan and find out whether refinancing puts real money back in your pocket.