How To Buy Rental Property With An LLC: Steps & Financing

Buying rental property in your personal name might seem like the straightforward path, but it leaves your personal assets exposed to lawsuits, tenant disputes, and unexpected liabilities. Learning how to buy rental property with an LLC creates a legal barrier between your investments and everything else you own, your home, savings, and other assets stay protected if something goes wrong with a property.

The process involves more than just filing paperwork with your state. You'll need to structure your LLC correctly, secure the right financing, and understand how lenders evaluate LLC-owned properties differently than personal purchases. Many investors stumble at the financing stage because traditional banks often shy away from LLC borrowers or demand personal guarantees that defeat the purpose of the structure.

With over 25 years funding real estate investments and more than $150 million in closed deals, I've helped hundreds of investors navigate LLC purchases using DSCR loans, commercial financing, and other investor-focused products. This guide breaks down every step, from formation to funding to closing, so you can build your rental portfolio with proper protection in place.

When buying in an LLC makes sense

You don't need an LLC for your first rental property if you're buying a single-family home with a traditional mortgage. The liability protection becomes valuable when your portfolio grows beyond two properties or when you're purchasing higher-risk property types like multi-unit buildings, commercial space, or properties requiring significant renovation work.

Protection thresholds that justify the structure

Most investors consider LLC ownership once they reach three or more rental properties because a lawsuit against one property could threaten the equity in all others. If you own $500,000 in equity across multiple rentals in your personal name, a tenant injury or property damage claim could put all that wealth at risk. Each LLC you create isolates risk to the assets held within that specific entity, so a problem with Property A doesn't expose Property B and C to the same legal claim.

An LLC creates a legal firewall between your rental properties and your personal assets, keeping lawsuits contained within the entity.

Property types with higher lawsuit exposure make the strongest case for LLC ownership. Commercial properties, short-term vacation rentals, and buildings with common areas or pools face more liability exposure than standard residential rentals. You should also prioritize LLC ownership if you're using leverage aggressively, because properties with 80% loan-to-value ratios or higher concentrate your personal financial risk.

Multi-property investors who want operational flexibility

Understanding how to buy rental property with an LLC becomes important when you plan to scale beyond casual landlording. Investors who intend to build a portfolio of five or more properties benefit from the credibility and structure that comes with LLC ownership. Banks and private lenders take you more seriously when you operate through a business entity, especially if you're pursuing commercial loans or portfolio financing products.

LLCs also simplify partnership structures when you're buying with other investors. Operating agreements define ownership percentages, profit distributions, and decision-making authority without the complexity of joint tenancy or tenancy-in-common arrangements. You can add or remove members, transfer ownership interests, and maintain clean accounting records that separate business finances from personal spending.

When personal ownership works better

Skip the LLC structure if you're buying your first or second property with conventional financing. Most traditional lenders offer better rates and terms for personal purchases, and the underwriting process moves faster when you're not dealing with business entity verification. You can always transfer properties into an LLC later through a quit-claim deed, though some lenders include due-on-sale clauses that technically allow them to call the loan due upon transfer.

Step 1. Form the LLC and set up clean finances

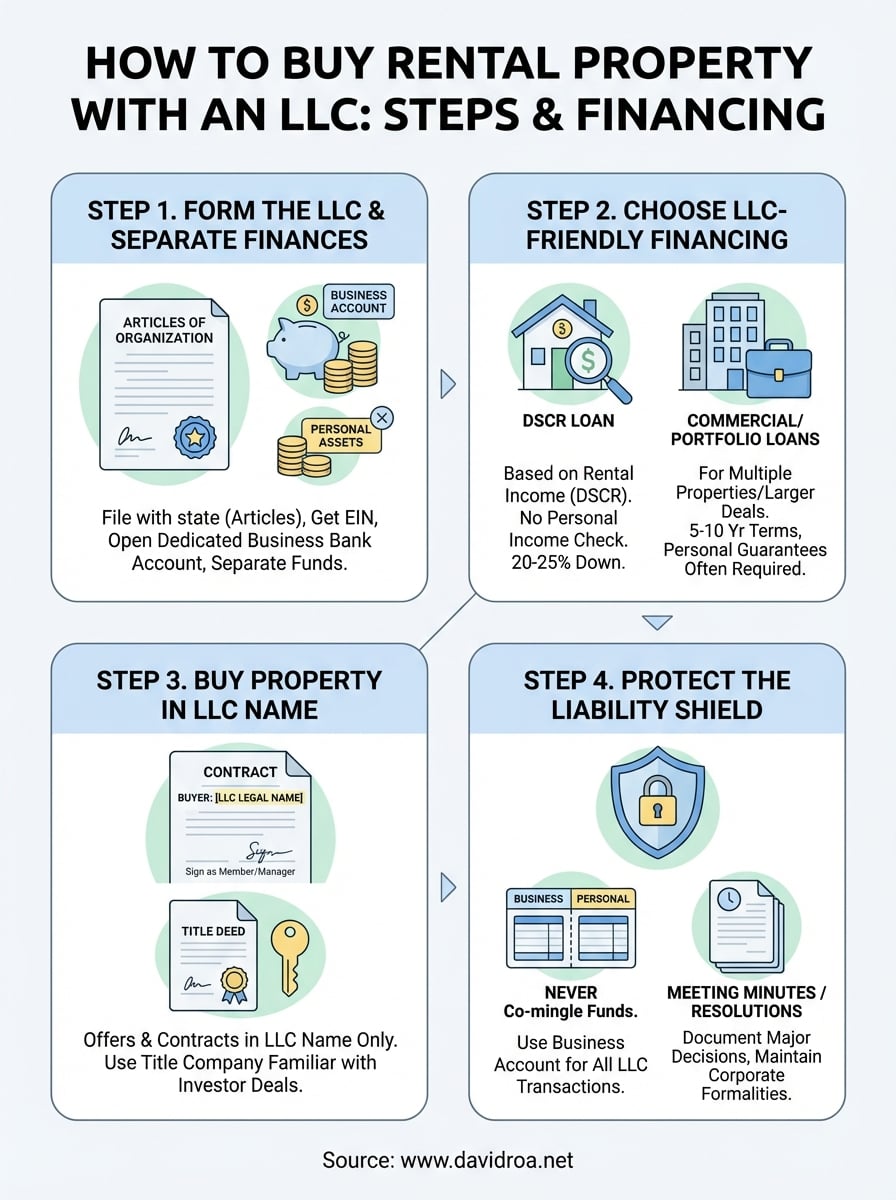

You need to establish your LLC as a separate legal entity before you start shopping for properties. The formation process takes 7 to 14 business days in most states, and you'll want clean financial separation in place before you approach lenders or make offers. Mixing personal and business finances destroys the liability protection an LLC provides, so proper setup matters from day one.

File articles of organization in your state

Start by filing articles of organization with your state's business registration office, usually the Secretary of State. You'll need to choose a unique business name that includes "LLC" and designate a registered agent who can receive legal documents on behalf of the company. Most states charge $50 to $500 in filing fees, with processing times ranging from immediate approval to three weeks depending on your location.

Draft an operating agreement even if your state doesn't require one. This document defines ownership percentages, profit distributions, and management responsibilities. Single-member LLCs still benefit from operating agreements because they demonstrate to courts that you're treating the LLC as a legitimate business entity rather than an alter ego.

Proper LLC documentation proves to lenders and courts that your business operates as a genuine separate entity.

Open a business bank account immediately

Apply for an Employer Identification Number (EIN) from the IRS before you contact banks. You can get an EIN online in minutes at no cost, and most banks require it to open business accounts. Use the EIN and your articles of organization to open a dedicated business checking account that you'll use exclusively for property transactions, rent collection, and operating expenses.

Deposit enough working capital to cover earnest money deposits and initial property expenses. Understanding how to buy rental property with an LLC means keeping $5,000 to $10,000 available for offers, inspections, and closing costs before financing arrives.

Step 2. Choose the right financing for an LLC purchase

Traditional lenders avoid LLC purchases because they can't rely on personal income verification or standard underwriting guidelines. You'll need financing products designed for business entities, which typically focus on the property's cash flow rather than your personal W-2 income. The right loan structure depends on your property type, down payment availability, and whether you're willing to sign personal guarantees.

DSCR loans eliminate personal income requirements

Debt Service Coverage Ratio (DSCR) loans evaluate the property's rental income against the mortgage payment instead of reviewing your tax returns or pay stubs. Lenders approve you based on whether the monthly rent covers 1.0x to 1.25x the principal, interest, taxes, and insurance payment. You'll need 20% to 25% down payment and solid credit scores above 660, but your personal employment history stays irrelevant.

DSCR loans let your LLC qualify based on property performance, not your personal income documentation.

These loans work perfectly when learning how to buy rental property with an LLC because they're designed for business entity ownership. Rates typically run 0.5% to 1.5% higher than conventional mortgages, but you avoid the complications of transferring personally-financed properties into your LLC after closing.

Commercial loans for larger portfolios

Commercial real estate loans and portfolio financing products serve investors buying multiple properties or buildings above four units. Banks structure these as business loans with 5 to 10-year terms and 25-year amortization schedules. You'll face balloon payments at term end, requiring refinancing or sale, but you get better pricing on larger deals above $500,000.

Most commercial lenders require personal guarantees regardless of LLC ownership, which reduces but doesn't eliminate your liability protection.

Step 3. Buy the property in the LLC name

Your offers and purchase contracts must list the LLC as the buyer, not your personal name. This step requires coordination with real estate agents, title companies, and lenders who understand business entity purchases. Missing this detail creates ownership confusion and potentially invalidates your liability protection before you even close the deal.

Make offers using your LLC legal name

Write offers with your complete LLC legal name exactly as it appears on your articles of organization, including the state designation like "ABC Rentals LLC, an Illinois Limited Liability Company." Sign documents as yourself followed by your title: "John Smith, Member" or "John Smith, Manager." Real estate agents unfamiliar with understanding how to buy rental property with an LLC might try to add your personal name as a co-buyer, which defeats the entire purpose of the structure.

Your signature block should always identify you as acting on behalf of the LLC, not as an individual buyer.

Work with a title company that handles investor transactions

Title companies verify ownership chains and issue insurance policies that protect against defects. Business entity purchases require additional documentation like operating agreements and certificates of good standing from your state. Request a title officer experienced with LLC closings because they'll catch issues like incorrect vesting or missing corporate resolutions that standard residential closers overlook.

Lenders funding your purchase will require the LLC listed as the mortgagor on loan documents. Your DSCR lender or commercial bank structures the note with the LLC as borrower, keeping ownership and financing aligned within the same entity from day one.

Step 4. Protect the liability shield after closing

Your LLC ownership becomes worthless if you treat the business like a personal piggy bank or ignore basic corporate formalities after closing. Courts can "pierce the corporate veil" and hold you personally liable when you fail to maintain separation between the LLC and your personal affairs. This step requires ongoing discipline rather than one-time paperwork, and most investors skip these protections until they face their first lawsuit.

Maintain separate records and bank accounts

Never pay personal expenses from your LLC bank account or deposit rental income into personal accounts. Every transaction flows through the business checking account you established in Step 1, from mortgage payments to maintenance costs to rent collection. You can pay yourself through documented distributions or management fees, but you record these transfers with proper accounting entries that show business-to-personal movement rather than commingled funds.

Mixing personal and business finances gives courts the evidence they need to disregard your LLC protection.

Keep separate credit cards for LLC expenses and save all receipts in digital or physical files organized by property and tax year. Understanding how to buy rental property with an LLC includes building systems that prove you operate as a legitimate business entity.

Document major decisions in writing

Record significant business decisions in meeting minutes or written resolutions even if you're the only member. Purchase agreements, refinancing decisions, and major capital improvements deserve documentation that shows your LLC made these choices through proper business processes. Store these records with your operating agreement and annual state filings so you can prove corporate formality if someone challenges your liability shield in court.

Where to go from here

You now understand how to buy rental property with an LLC, from formation through closing and ongoing protection. Start by forming your LLC in your state and opening that dedicated business bank account before you make your first offer. Your financing choice matters most after structure, so decide whether DSCR loans or commercial products fit your down payment availability and property type.

Most investors stumble on financing because they approach traditional lenders who don't understand business entity purchases. Connect with lenders who specialize in investor transactions and can underwrite based on property performance rather than personal income verification. Your LLC protection only works when you pair proper structure with the right loan product from day one.

Ready to secure financing for your LLC property purchase? Contact me directly to discuss DSCR loans, commercial financing options, and portfolio strategies that protect your assets while building rental income. I've closed over $150 million in investor deals and can guide you through the entire LLC purchase process with financing that actually works for business entities.