How To Do A 1031 Exchange: IRS Rules, Timelines & Steps

Selling an investment property often means watching a significant portion of your profits disappear to capital gains taxes. But there's a legal strategy that lets you defer those taxes indefinitely, if you know how to do a 1031 exchange correctly. Miss a single deadline or break one IRS rule, and you could lose the entire tax benefit.

After 25 years helping real estate investors secure financing and structure deals, I've seen too many people stumble through this process without fully understanding what's at stake. A 1031 exchange isn't overly complicated, but it is unforgiving when it comes to timelines. The IRS gives you exactly 45 days to identify replacement properties and 180 days to close, no extensions, no exceptions.

This guide breaks down the exact steps you need to take, the IRS rules you must follow, and the critical deadlines that determine whether your exchange succeeds. Whether you're rolling over a single rental or repositioning an entire portfolio, you'll have a clear roadmap to defer your capital gains and keep more of your money working for you.

What a 1031 exchange is and who qualifies

A 1031 exchange lets you sell an investment property and reinvest the proceeds into a new property without paying capital gains taxes immediately. Named after Section 1031 of the Internal Revenue Code, this provision allows you to defer taxes indefinitely as long as you continue rolling your equity from one property to another. The IRS treats the sale and purchase as a single transaction, which means your tax liability gets pushed to a future date when you eventually cash out.

You don't literally swap properties with another owner. Instead, you sell your current property, place the proceeds with a qualified intermediary, and use those funds to purchase replacement property within strict IRS timelines. The qualified intermediary holds your money to prevent you from taking constructive receipt of the funds, which would immediately trigger tax liability and disqualify the entire exchange.

The basic mechanics of the exchange

The process requires three critical components: a qualified intermediary to hold your sale proceeds, like-kind replacement property to reinvest into, and strict adherence to IRS deadlines. Your intermediary creates an exchange agreement before you close on your relinquished property, then receives and holds the funds in a segregated account. You never touch the money directly.

The moment you receive sale proceeds directly, you lose the tax deferral and owe capital gains taxes on the entire transaction.

Who qualifies for a 1031 exchange

You must hold both your relinquished property and replacement property for investment or business purposes. Personal residences, vacation homes you primarily use yourself, and properties you flip within short timeframes typically don't qualify. The IRS looks at your intent and usage pattern, not just what you claim on paper.

Both properties must be like-kind, which for real estate means almost any type of investment real estate can exchange for another. You can trade a single-family rental for an apartment building, raw land for a commercial warehouse, or a strip mall for farmland. The IRS defines like-kind broadly for real estate, but you cannot exchange U.S. properties for foreign properties or swap real estate for personal property like equipment or vehicles.

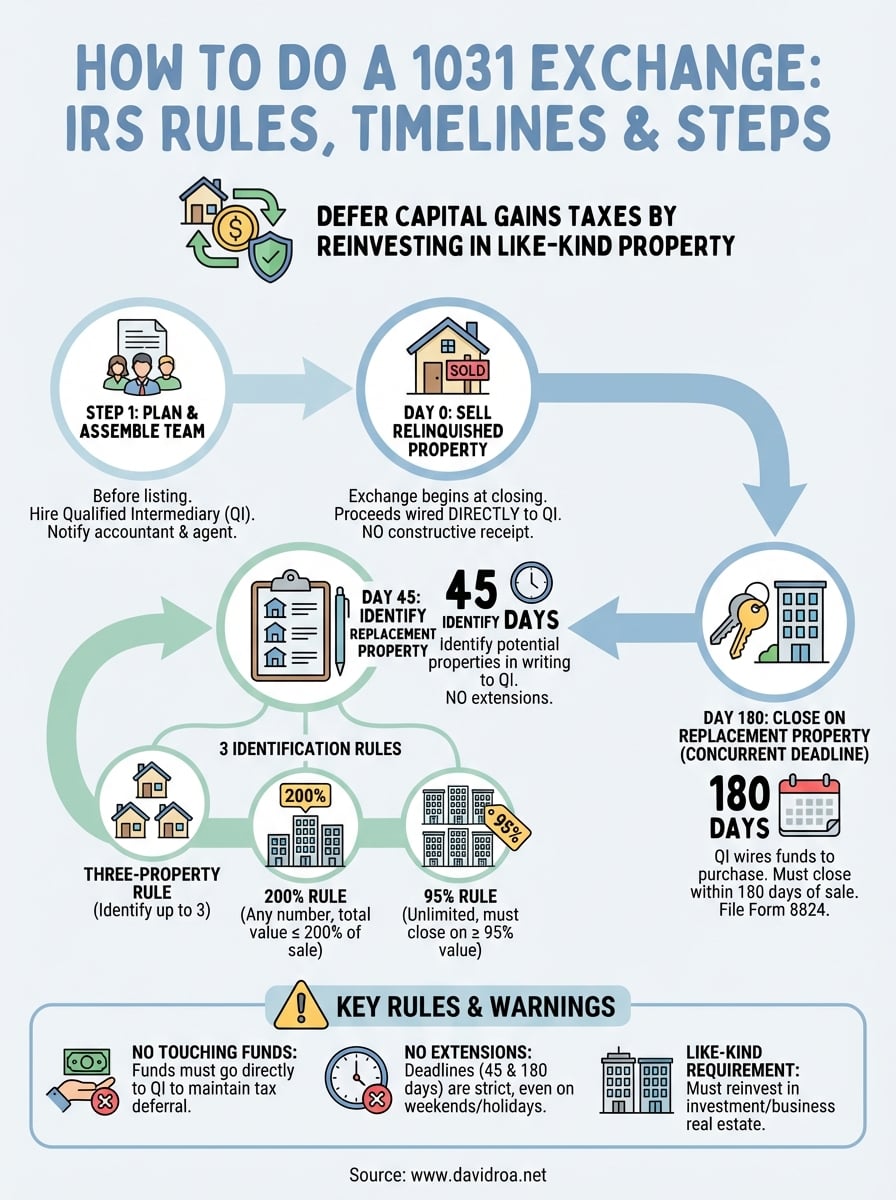

Step 1. Line up your team and plan the exchange

You need to assemble your exchange team before you list your relinquished property for sale. The most critical hire is your qualified intermediary, who must be in place before closing. Wait too long to bring them in, and you risk disqualifying the entire exchange. This planning phase also involves notifying your accountant, real estate agent, and closing attorney about your intent to execute a 1031 exchange.

Find a qualified intermediary

Your qualified intermediary holds your sale proceeds and facilitates the exchange process. Choose someone with verifiable experience and adequate errors and omissions insurance to protect your funds. Ask for references from real estate investors who have completed multiple exchanges, and verify the intermediary maintains segregated accounts for client funds rather than commingling them with business operating accounts.

The IRS prohibits you from using relatives, employees, or anyone who has provided you services in the past two years as your qualified intermediary.

Most qualified intermediaries charge between $800 and $1,500 for standard exchanges. Interview at least three candidates and confirm they provide written exchange agreements that outline their responsibilities and your deadlines.

Notify relevant parties

Inform your real estate agent that you plan to execute a 1031 exchange when they list your property. This helps them structure offers correctly and communicate requirements to potential buyers. Your accountant needs advance notice to prepare Form 8824 and calculate your adjusted basis for the replacement property. The closing attorney or escrow officer must also know upfront because they work directly with your qualified intermediary to wire funds properly at closing.

Step 2. Sell the relinquished property and fund escrow

Your exchange officially begins when you close on your relinquished property. The closing statement must explicitly identify the transaction as part of a 1031 exchange, and your qualified intermediary needs to receive the proceeds directly from escrow. This step determines whether you maintain the tax deferral, so proper coordination between your closing agent and intermediary is non-negotiable.

Include exchange language in the purchase agreement

Add a 1031 exchange cooperation clause to your purchase agreement before the buyer signs. This clause notifies the buyer that you're executing an exchange and requires their cooperation in assigning the contract to your qualified intermediary. Most buyers readily agree because the clause doesn't affect their rights or obligations, but you need it documented upfront to satisfy IRS requirements.

Your qualified intermediary provides template language for the assignment clause. Include it in the initial offer or add it as an addendum before closing.

Direct all proceeds to your intermediary

The closing agent wires your sale proceeds directly to your qualified intermediary's account at closing. You never receive the funds personally, not even temporarily. Your intermediary holds the money in a segregated escrow account until you're ready to purchase replacement property.

If you receive any portion of the sale proceeds directly, even by mistake, the IRS considers you in constructive receipt and the entire exchange fails immediately.

Review the closing statement before signing to confirm the wire instructions route funds to your intermediary, not your personal or business accounts. One wire sent to the wrong account destroys months of planning and triggers immediate tax liability on your gains.

Step 3. Identify replacement property within 45 days

You have exactly 45 days from closing on your relinquished property to identify potential replacement properties in writing to your qualified intermediary. This deadline falls on a calendar day, not a business day, which means if day 45 lands on a weekend or holiday, you don't get an extension. The IRS counts every single day, and missing this deadline by even one day disqualifies your entire exchange and triggers immediate tax liability.

The three identification rules

The IRS gives you three options for identifying replacement properties. Under the three-property rule, you can identify up to three properties of any value and close on one or more of them. This rule works for most investors because you have flexibility in which property you ultimately purchase.

The 200% rule lets you identify any number of properties as long as their total combined fair market value doesn't exceed 200% of your relinquished property's sale price. If you sold a property for $500,000, you can identify properties totaling up to $1,000,000 in value.

The 95% rule removes all limits on the number or value of properties you identify, but you must close on properties representing at least 95% of the total value you listed. This rule carries significant risk because failing to close on 95% of the identified value disqualifies your exchange.

The 45-day identification deadline is absolute. The IRS does not grant extensions for any reason, including natural disasters, illness, or administrative errors.

Submit written identification to your intermediary

Send your written identification to your qualified intermediary before midnight on day 45. Include the complete street address and legal description for each property. Email or fax works, but confirm your intermediary received it before the deadline expires. Understanding how to do a 1031 exchange means treating these deadlines as immovable constraints on your entire transaction timeline.

Step 4. Close within 180 days and file Form 8824

You have 180 days from the closing of your relinquished property to complete the purchase of your replacement property. This deadline runs concurrently with your 45-day identification period, not after it. Your qualified intermediary wires the funds they've been holding directly to the closing agent when you purchase your replacement property, completing the exchange transaction.

Complete the purchase of replacement property

Your purchase agreement for the replacement property must assign your rights to your qualified intermediary, just like you did when selling your relinquished property. The closing statement needs to show your intermediary as the buyer, with you listed as the beneficial owner. This structure maintains the proper chain of custody for your exchange funds and satisfies IRS documentation requirements.

Coordinate closely with your closing agent to ensure they receive wire instructions directly from your qualified intermediary. Your intermediary releases the held funds to cover your down payment and closing costs on the replacement property. If the replacement property costs more than your sale proceeds, you'll need to bring additional cash to closing from your own accounts.

The 180-day deadline includes weekends and holidays, with no extensions available except in presidentially declared disaster areas.

File Form 8824 with your tax return

You must file Form 8824 (Like-Kind Exchanges) with your tax return for the year you completed the exchange. This form reports both the relinquished property sale and replacement property purchase, documenting your deferred gain and establishing your new basis in the replacement property. Your accountant needs closing statements from both transactions to complete the form accurately and calculate your adjusted basis going forward.

Keep your exchange compliant

Knowing how to do a 1031 exchange successfully comes down to respecting the IRS deadlines and following the qualified intermediary protocol without exception. The most common failures happen when investors try to access their sale proceeds before closing on replacement property, or miss the 45-day identification deadline thinking they can negotiate an extension. Neither mistake is fixable once it happens.

Document everything throughout the process. Keep copies of all correspondence with your qualified intermediary, closing statements from both transactions, and proof of your written identification submitted before day 45. These records protect you during an audit and help your accountant complete Form 8824 accurately when tax season arrives.

If you're ready to sell an investment property and need financing for your replacement property, connect with an experienced lender who understands exchange timelines and can close quickly within your 180-day window.