The Complete Guide to Investing in Multifamily Properties

Most real estate investors start with single-family homes. It makes sense, one property, one tenant, one mortgage payment to track. But at some point, the math stops adding up. You're spending just as much time managing a duplex as you would a small apartment building, yet the cash flow from a single unit caps your growth. That's when investing in multifamily properties becomes more than an option; it becomes a logical next step.

Multifamily real estate, buildings with two or more units, offers something single-family rentals can't: scalable income under one roof. Instead of acquiring ten separate properties to generate meaningful cash flow, you can consolidate your efforts into one asset that houses multiple rent-paying tenants. The economies of scale are real. So are the risks if you don't understand how to evaluate deals, structure financing, or manage operations.

This guide covers what you need to know before buying your first (or next) multifamily property. We'll break down the benefits and potential pitfalls, walk through the financial metrics that separate good deals from bad ones, and outline practical steps for acquisition and management. Whether you're eyeing a small triplex or a 20-unit apartment building, the fundamentals apply.

At David Roa, we've helped investors secure financing for multifamily acquisitions through DSCR loans, conventional investment mortgages, and commercial lending programs. With over $150 million funded and 25+ years in the industry, we've seen what works, and what doesn't, when investors make the jump to multiple units. This guide reflects that experience.

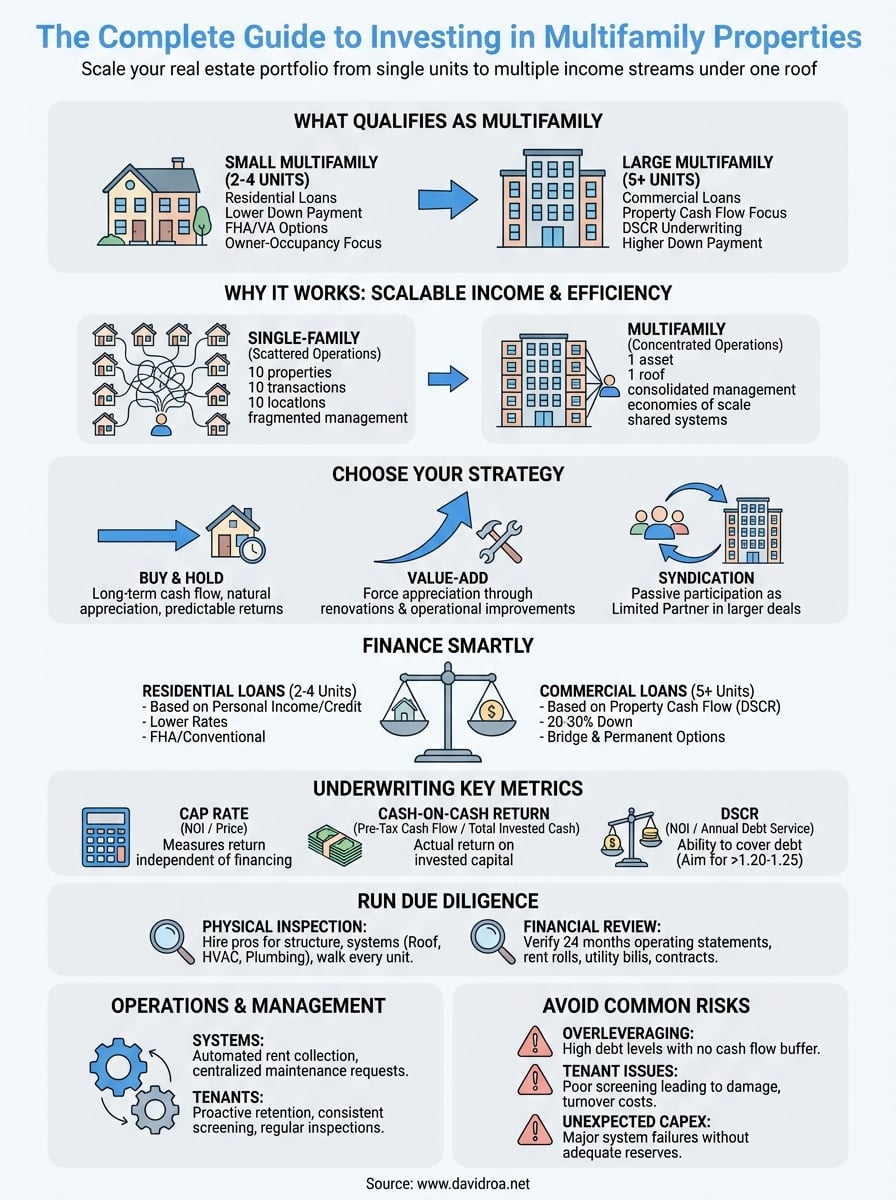

What qualifies as a multifamily property

A multifamily property is any residential building designed to house two or more separate living units under one roof or on a single parcel. Each unit has its own entrance, kitchen, bathroom, and living space, allowing multiple tenants or families to live independently within the same structure. The definition sounds simple, but the classification carries real weight. It determines how lenders view your purchase, what financing options you can access, and which property management strategies work best.

Small multifamily properties (2-4 units)

Properties with two to four units fall into what the lending industry calls "small multifamily" or "residential multifamily." This category includes duplexes, triplexes, and fourplexes. Banks and mortgage lenders treat these properties differently than larger apartment buildings because they still qualify for residential financing programs. You can often secure a conventional mortgage, FHA loan, or VA loan (if you're a veteran) as long as you plan to occupy one of the units as your primary residence.

The owner-occupancy option makes small multifamily properties attractive for investors just starting out. You live in one unit while tenants in the other units cover most or all of your mortgage payment. This strategy, often called "house hacking," lets you build equity and rental income simultaneously. Even if you don't occupy the property, residential loan terms typically offer lower down payments and better interest rates than commercial financing.

Small multifamily properties bridge the gap between homeownership and full-scale real estate investing, giving you income without forcing you into commercial loan territory.

Large multifamily properties (5+ units)

Once a building crosses the five-unit threshold, it enters commercial real estate classification. Apartment buildings with five units or more, mid-rise complexes, and large residential developments all fall under this category. The shift matters because lenders no longer evaluate these properties based on your personal income. Instead, they focus on the property's cash flow and ability to service debt through rental income.

Commercial multifamily loans use different underwriting standards. Lenders calculate the debt service coverage ratio (DSCR), a metric that compares the property's net operating income to its annual debt obligations. You need a DSCR above 1.0 for most lenders, though many prefer 1.25 or higher. The property itself becomes the primary factor in loan approval, not your W-2 or tax returns. This opens doors for investors with strong deal analysis skills but limited personal income documentation.

Classification matters for financing and strategy

Understanding where your target property falls in the classification system shapes your entire approach to investing in multifamily properties. Small multifamily deals (2-4 units) allow you to use conventional mortgage products, often with down payments as low as 15% for investment properties or 3.5% for FHA owner-occupied purchases. You'll face residential appraisal standards, which focus on comparable sales rather than income potential.

Large multifamily properties (5+ units) require commercial financing, which typically demands 20-30% down payments and focuses heavily on the property's operating performance. Lenders want to see rent rolls, expense histories, and profit-and-loss statements. The due diligence process becomes more complex, but the potential returns scale faster when you control dozens of units instead of just three or four.

The classification also affects your property management decisions. Small multifamily buildings can sometimes be self-managed if you live nearby, while larger properties usually require professional management companies to handle tenant issues, maintenance requests, and lease renewals. Your time investment shifts from hands-on landlording to asset oversight and financial analysis as the unit count increases.

Why multifamily investing works for many investors

Most investors choose multifamily properties because the numbers make more sense than chasing individual houses across town. You collect rent from multiple tenants each month instead of relying on a single source of income. When one unit sits vacant, the others still generate cash flow to cover your mortgage payment, property taxes, and operating expenses. This built-in buffer gives you more financial stability than single-family rentals, where a vacancy means zero income until you find a replacement tenant.

Cash flow scales faster with multiple units

A fourplex with four tenants paying $1,200 each produces $4,800 in monthly gross rent from one acquisition. You'd need four separate single-family homes to match that income, which means four closings, four inspections, four insurance policies, and four property tax bills to manage. The transaction costs alone, buying and financing four properties versus one, eat into your profits before you collect a dollar in rent. Multifamily properties let you scale your portfolio without multiplying your workload or closing costs proportionally.

The efficiency extends to property improvements too. Installing a new roof on a fourplex costs more than roofing a single house, but you're protecting four income streams with one project. Landscaping, exterior maintenance, and common area upgrades serve multiple units simultaneously. Your cost per unit drops as the building size increases, which directly improves your profit margins and return on investment.

One property means concentrated operations

Managing ten single-family rentals scattered across different neighborhoods turns property management into a logistics puzzle. You drive to multiple locations for inspections, deal with ten different sets of neighbors, and coordinate repairs across various zip codes. A ten-unit apartment building puts all your tenants in one physical location. You handle maintenance requests more efficiently, conduct property walks in minutes instead of hours, and build relationships with local contractors who become familiar with your building's systems.

Concentrated operations reduce the time you spend on property management tasks, letting you focus on deal analysis and portfolio growth instead of driving between scattered houses.

This geographic consolidation also improves your tenant screening and lease enforcement. You establish consistent standards across all units because they exist under the same roof, governed by the same lease terms. When issues arise, you address them immediately rather than scheduling visits days out because a property sits forty minutes away.

Compare multifamily vs single-family investing

The choice between multifamily and single-family investing shapes your cash flow potential, risk exposure, and time commitment from day one. Single-family homes appeal to new investors because they're familiar. You understand how houses work, what tenants expect, and how neighborhoods affect property values. Multifamily properties introduce complexity, more units to fill, higher purchase prices, and commercial financing requirements, but they also deliver advantages that single-family rentals can't match at scale.

Risk distribution works differently

A vacancy in a single-family rental stops 100% of your income immediately. You still owe the mortgage, property taxes, insurance, and maintenance costs, but nothing comes in until you find another tenant. That gap can stretch for weeks or months depending on your market. With multifamily properties, a vacant unit in a fourplex drops your income by 25%, not 100%. The other three tenants keep paying rent while you search for a replacement, so your mortgage payment stays covered.

This risk buffer matters more as your portfolio grows. If you own four single-family homes and one sits vacant, you've lost a quarter of your rental income just like the fourplex scenario. But you're managing four separate properties, dealing with four different neighborhoods, and coordinating repairs across multiple locations. The multifamily property concentrates the same income (or more) in one asset, giving you the same diversification benefit without the operational fragmentation.

Appreciation and equity building follow separate paths

Single-family homes typically appreciate based on comparable sales in the surrounding neighborhood. When similar houses sell for higher prices, your property value increases. You have limited control over this process beyond basic maintenance and cosmetic improvements. Market forces, school quality, and neighborhood trends drive your property's value more than anything you do as an owner.

Multifamily properties gain value through income generation, meaning you directly control appreciation by raising rents, cutting expenses, or improving operations.

Investing in multifamily properties lets you force appreciation through strategic management. Increase the net operating income by $10,000 annually, and you might add $100,000 to the property's value (assuming a 10% cap rate). You control rent rates, negotiate better insurance premiums, reduce vacancy through tenant retention, and implement energy-efficient upgrades that lower utility costs. Every operational improvement flows straight to your bottom line and property valuation.

Management intensity scales differently

You might self-manage one or two single-family rentals without much trouble. Answer occasional maintenance calls, collect rent checks, handle lease renewals once a year. Add ten single-family properties to your portfolio, and you're running a full-time operation. Each property needs individual attention, separate vendor relationships, and location-specific problem-solving.

A ten-unit multifamily building demands professional management in most cases, but the per-unit effort drops significantly. One property manager oversees all ten units, contractors become familiar with the building's systems, and you build operational efficiencies that single-family investors never achieve at the same scale.

Choose a strategy that fits your goals

Your investment strategy determines which properties you target, how you finance them, and what returns you can expect. Some investors prioritize steady monthly income and hold properties for decades, while others buy distressed buildings, improve operations, and sell within three to five years. A third group participates passively through syndication deals, contributing capital without managing day-to-day operations. Each approach requires different skills, capital reserves, and time commitments. Match your strategy to your financial goals, available resources, and comfort level with active management.

Buy and hold for long-term cash flow

This strategy focuses on consistent rental income that covers your mortgage and operating expenses while generating monthly profit. You purchase stabilized properties with tenants already in place, maintain solid occupancy rates, and collect rent checks for years or decades. The property appreciates naturally over time as market values increase and you pay down the mortgage principal with tenant dollars.

Buy and hold works best when you want predictable returns without major renovation projects. You screen quality tenants, keep the property well-maintained, and raise rents gradually to match market rates. Your wealth builds through cash flow accumulation and mortgage paydown rather than quick flips or major repositioning efforts. This approach requires patience but delivers stable income that can fund your lifestyle or reinvest into additional properties.

Value-add and force appreciation

Value-add investing targets properties with operational problems or deferred maintenance that suppress rental income. You might buy a building with below-market rents, high vacancy rates, or outdated units that tenants avoid. After closing, you implement improvements such as unit renovations, better property management, or expense reduction strategies that boost the net operating income.

The goal is to increase property value significantly within two to five years, then either refinance to pull cash out or sell at a profit. This strategy demands more capital upfront for renovations and carries higher risk if your improvements don't attract tenants at projected rent rates. You need construction management skills, market knowledge to price rents correctly, and financial reserves to handle unexpected costs during the value-add period.

Value-add strategies let you create equity through operational improvements rather than waiting for market appreciation, but they require hands-on involvement and renovation capital.

Syndication for passive participation

Real estate syndication pools money from multiple investors to purchase larger multifamily properties that individual buyers couldn't afford alone. You contribute capital as a limited partner while experienced operators (general partners) handle property acquisition, management, and eventual sale. Your returns come from quarterly or annual distributions plus a share of profits when the property sells.

Syndication allows you to participate in investing in multifamily properties without finding deals, securing financing, or managing tenants yourself. You gain exposure to larger assets (50+ units) with professional management teams. The tradeoff is less control over decisions and dependence on the general partner's expertise and integrity.

Finance a multifamily purchase the smart way

Financing determines whether a deal works or falls apart before you close. You can find the perfect property with strong rent rolls and solid cash flow projections, but without the right loan structure, your returns evaporate under high interest rates or unfavorable terms. The financing landscape for multifamily properties splits into distinct categories based on unit count, occupancy plans, and your investor profile. Understanding which programs fit your situation saves you months of frustration and potentially thousands in closing costs.

Understand how property size affects your loan options

Properties with two to four units qualify for residential financing programs that typically offer better terms than commercial loans. You can secure conventional mortgages with down payments as low as 15% for investment properties or access FHA loans with 3.5% down if you plan to occupy one unit. These residential loans evaluate your personal income and credit score more than the property's cash flow, which works well if you have strong W-2 income but limited real estate experience.

Once you target buildings with five or more units, lenders shift to commercial financing standards. Banks focus on the property's ability to generate income through debt service coverage ratio (DSCR) calculations rather than your personal tax returns. Commercial loans typically require 20-30% down payments and carry shorter amortization periods, but they let you scale faster because your borrowing capacity grows with each property's performance rather than hitting personal income limits.

Match financing to your investment strategy

DSCR loans work particularly well when investing in multifamily properties because underwriters approve you based on rental income rather than employment documentation. You submit rent rolls and operating statements instead of tax returns, which benefits self-employed investors or those with complex income structures. The property needs to generate enough net operating income to cover 1.2 to 1.25 times the annual debt payment, depending on the lender's requirements.

DSCR financing lets the property qualify itself through cash flow, removing personal income limitations that cap your portfolio growth with conventional loans.

Bridge loans provide short-term capital for value-add projects where you plan to renovate units and increase rents within 12 to 24 months. These loans carry higher interest rates but offer flexibility during the improvement period. You transition to permanent financing through a cash-out refinance once you stabilize operations and boost the property's value through strategic improvements.

Prepare your financial profile for lenders

Lenders want to see substantial cash reserves equal to six months of mortgage payments and operating expenses, particularly for larger properties. Your credit score should exceed 680 for competitive rates, though some programs accept scores as low as 620 with compensating factors like larger down payments. Gather 24 months of property tax returns, current rent rolls, and profit-and-loss statements before approaching lenders to demonstrate you understand the asset's financial performance beyond surface-level numbers.

Underwrite deals with the key multifamily metrics

Numbers tell you whether a deal makes sense before you commit capital. You can't rely on seller claims about income potential or rough estimates from property listings. Real underwriting requires calculating specific financial metrics that reveal cash flow potential, risk levels, and return expectations. These calculations separate properties that generate wealth from those that drain your bank account month after month. Master these core metrics before you write an offer, and you'll avoid deals that look attractive on the surface but collapse under basic financial scrutiny.

Calculate the capitalization rate

The capitalization rate, or cap rate, measures a property's annual net operating income against its purchase price. You divide the NOI by the property price to get this percentage, which tells you what return the property generates independent of financing. A building producing $80,000 in annual NOI with a $1,000,000 price tag delivers an 8% cap rate. Higher cap rates generally indicate higher returns but often come with increased risk, lower-quality properties, or less desirable markets.

Cap rates let you compare properties across different markets and price points using a standardized metric. You evaluate a 10-unit building in one neighborhood against a 20-unit building across town by examining their respective cap rates. Properties in stable, high-demand areas typically trade at lower cap rates (4-6%) while secondary markets or value-add opportunities might offer 8-10% or higher. Understanding local market cap rates prevents you from overpaying or missing opportunities when investing in multifamily properties.

Measure cash-on-cash return

Cash-on-cash return shows what percentage return you earn on your actual invested capital after factoring in mortgage payments. You calculate this by dividing your annual pre-tax cash flow by the total cash you invested (down payment, closing costs, and initial reserves). A property generating $15,000 in annual cash flow after debt service, with $150,000 invested, delivers a 10% cash-on-cash return.

This metric matters more than cap rate for leveraged purchases because it accounts for financing costs that directly impact your wallet. A property with a strong cap rate might produce weak cash-on-cash returns if you secure poor loan terms or overleverage the purchase.

Cash-on-cash return reveals your true profitability after mortgage payments, showing whether borrowed money amplifies or diminishes your investment returns.

Verify debt service coverage ratio

DSCR measures whether rental income covers your debt obligations with a safety buffer. Lenders calculate this by dividing net operating income by annual debt service. A property generating $100,000 in NOI with $80,000 in annual mortgage payments has a 1.25 DSCR. Most commercial lenders require 1.20 to 1.30 minimum, ensuring the property generates enough income to handle debt payments even during minor occupancy dips or expense increases.

Run due diligence before you close

Due diligence protects your investment by uncovering problems the seller might hide or genuinely not know exist. You move beyond the numbers you used for initial underwriting and verify that physical conditions, financial records, and tenant situations match what the seller represented. This inspection period, typically 30 to 45 days after going under contract, gives you the legal right to walk away if you discover deal-breaking issues. Most purchase agreements make your deposit refundable during this window, so use every day to investigate the property thoroughly.

Inspect the physical property thoroughly

Hire licensed inspectors to evaluate the building's structural integrity, mechanical systems, and code compliance. You need separate inspections for the roof, HVAC units, plumbing, electrical systems, and foundation. General home inspectors miss issues that specialized commercial property inspectors catch, particularly in older buildings with deferred maintenance problems. Request inspection reports from the seller if recent ones exist, but always commission your own rather than trusting documents provided by someone motivated to close the sale.

Walk every unit personally, even occupied ones (with proper tenant notice). Look for water damage, pest infestations, mold growth, and structural issues that affect habitability. Document everything with photos and notes. The condition of occupied units tells you how current tenants treat the property and what turnover costs you'll face when they move out.

Review financial records and rent rolls

Demand at least 24 months of operating statements, including income and expense reports that show the property's true financial performance. Compare these documents against tax returns the seller filed, watching for discrepancies that suggest inflated income or hidden expenses. Request copies of all utility bills, insurance policies, property tax statements, and service contracts to verify the seller's expense claims match reality when investing in multifamily properties.

Sellers sometimes inflate projected rents or hide recurring maintenance costs, making detailed financial verification the difference between a profitable deal and a cash-draining mistake.

Analyze the rent roll for lease terms, security deposits, and tenant payment histories. Properties with multiple month-to-month tenants carry higher risk than buildings with signed annual leases. Check for unusually low rents that suggest deferred increases or below-market pricing you'll struggle to raise without losing tenants.

Operate and manage the property day to day

Daily operations determine whether your multifamily investment generates the returns you projected or bleeds cash through poor execution. You purchased based on financial projections, but those numbers only materialize through consistent management of rent collection, maintenance requests, and tenant relationships. Properties don't run themselves. You need systems that handle routine tasks efficiently while giving you visibility into problems before they become expensive crises. Whether you self-manage or hire a property manager, understanding operational fundamentals keeps your investment on track.

Establish clear systems for rent collection and maintenance

Set up automated rent collection through ACH transfers or online payment platforms that eliminate manual check handling. You reduce late payments when tenants can pay instantly through their phones instead of mailing checks or dropping off cash. Send payment reminders three days before the due date and assess late fees consistently according to your lease terms. Inconsistent enforcement trains tenants to ignore deadlines because they know you won't follow through.

Maintenance requests need a centralized tracking system whether you manage the property yourself or hire professionals. Tenants submit requests through a portal or dedicated phone line, and you log each issue with dates, descriptions, and resolution timelines. Response speed affects tenant retention directly. Handle emergency repairs (burst pipes, heating failures, security issues) within 24 hours and schedule non-urgent requests within 48 to 72 hours.

Handle tenant relationships proactively

Regular property inspections, quarterly or semi-annually, catch problems before tenants report them and show you care about property conditions. You document unit conditions with photos, verify lease compliance, and identify maintenance needs during these walks. Tenants who feel heard and see responsive management stay longer, reducing your turnover costs and vacancy periods when investing in multifamily properties.

Tenant retention saves more money than aggressive rent increases because turnover costs, from advertising to unit preparation, typically equal one to two months of rent per unit.

Screen tenant complaints carefully to separate legitimate issues from chronic complainers. Address valid concerns promptly while documenting patterns of unreasonable demands that might justify non-renewal decisions later.

Track expenses and optimize operations monthly

Review your profit and loss statements monthly rather than waiting for year-end summaries. Compare actual expenses against your underwriting projections to spot budget overruns in utilities, repairs, or property management fees. Small expense creep, $200 extra here, $300 there, accumulates into thousands annually that erode your cash flow without obvious warning signs.

Negotiate service contracts annually for landscaping, snow removal, pest control, and trash collection. Vendors rarely reduce prices voluntarily, but shopping quotes from competitors gives you leverage to reduce recurring costs by 10 to 20 percent without sacrificing service quality.

Avoid the most common multifamily investing risks

Risk management separates successful investors from those who lose their properties to foreclosure or sell at a loss after years of frustration. Every multifamily deal carries inherent risks, but the most destructive ones follow predictable patterns. You can't eliminate uncertainty completely, but you can identify and mitigate the specific threats that sink deals most often. Understanding where investors typically fail protects your capital investment and prevents problems that force distressed sales or drain your reserves when investing in multifamily properties.

Watch for overleveraging and cash flow gaps

Excessive debt loads kill deals that should work financially. You might secure favorable terms that keep your debt service coverage ratio barely above lender minimums, but any small disruption in income or unexpected expense increase pushes you underwater. Properties financed at 90% loan-to-value leave no room for error. A single month of higher-than-expected vacancy can force you to inject personal capital just to cover the mortgage payment.

Calculate your cash flow assuming 5% lower occupancy than current levels and 10% higher operating expenses than the seller claims. Your deal should still generate positive cash flow under these conservative assumptions. Properties that only work with perfect conditions and maximum leverage fail when reality introduces normal business fluctuations like tenant turnover or maintenance emergencies.

Conservative underwriting with adequate cash reserves protects you when markets soften or properties underperform projections, letting you survive temporary setbacks instead of facing foreclosure.

Protect against poor tenant quality and high turnover

Low-quality tenants destroy property value through damage, late payments, and the costs associated with evictions. Screening applicants with criminal background checks, income verification, and rental history reviews costs money upfront but saves multiples in avoided damages and legal fees. Setting minimum credit scores and income requirements (typically 2.5 to 3 times monthly rent) filters out tenants likely to default.

Turnover costs extend beyond lost rent during vacancy periods. You spend on advertising, unit cleaning, repairs, and potential rent concessions to attract new tenants quickly. Factor $2,000 to $4,000 per unit for turnover expenses when evaluating deals, and prioritize tenant retention strategies that reduce this recurring drain on profitability.

Account for capital expenditures you can't predict

Major system failures, roof replacements, parking lot resurfacing, and building envelope repairs arrive without warning and cost tens of thousands. Reserve at least $250 to $500 per unit annually for capital expenditures separate from your maintenance budget. You might not spend these reserves every year, but the fund grows to handle inevitable large-scale replacements that operating cash flow can't absorb.

Properties with aging mechanical systems or deferred maintenance require higher reserve levels. Budget for complete HVAC replacement ($5,000 to $8,000 per unit), roof replacement ($15,000 to $25,000 for smaller buildings), and plumbing updates that older buildings demand.

Bring it all together and plan your first deal

Start with a small multifamily property (2-4 units) if you're new to this asset class. These buildings qualify for residential financing with lower down payments and let you learn operational fundamentals without the complexity of larger commercial deals. You can secure conventional or FHA financing, analyze rent rolls from just a few tenants, and manage the property yourself initially to understand how systems work before scaling up.

Calculate your numbers conservatively during underwriting. Use cap rates from comparable sales in your target market, assume 5% lower occupancy than current levels, and budget for capital reserves you'll need when systems fail. Properties that barely work on paper with perfect assumptions fail in reality. Your first deal should generate positive cash flow even under stressed scenarios, giving you breathing room to handle mistakes and unexpected costs while learning the business of investing in multifamily properties.

Contact David Roa if you need financing for your acquisition. We specialize in DSCR loans and investment property mortgages that let the property qualify itself through cash flow rather than limiting your growth with personal income requirements.