Jumbo Loan Requirements: Credit Down Payment DTI & Reserves

When the home you want exceeds conforming loan limits, you're in jumbo territory, and the rules change. Jumbo loan requirements are stricter than what you'll find with conventional financing because lenders take on more risk without government backing. That means higher standards for credit, income, assets, and down payment before you'll get approved.

For 2026, any mortgage above $806,500 in most U.S. counties (or $1,209,750 in designated high-cost areas) qualifies as a jumbo loan. If you're shopping for property in that range, you need to know exactly where the bar is set, not a vague overview, but the actual numbers lenders use to make decisions.

That's what this guide covers. You'll get a clear breakdown of minimum credit scores, debt-to-income ratio limits, down payment expectations, and the cash reserve requirements that trip up even well-qualified borrowers. Each section reflects what we see daily at David Roa, where we've helped borrowers close on over $150 million in funded loans across residential, investment, and commercial deals over 25+ years. Jumbo loans are a regular part of that work, and the qualification process doesn't have to be a guessing game when you understand what's required upfront.

What counts as a jumbo loan in 2026

A jumbo loan is any mortgage that exceeds the conforming loan limit set by the Federal Housing Finance Agency (FHFA). That limit defines the maximum loan size Fannie Mae and Freddie Mac will purchase from lenders. When your loan goes above that ceiling, it no longer qualifies for those government-sponsored programs, so lenders hold the risk on their own books. That's exactly why jumbo loan requirements sit in a different category from standard conventional financing.

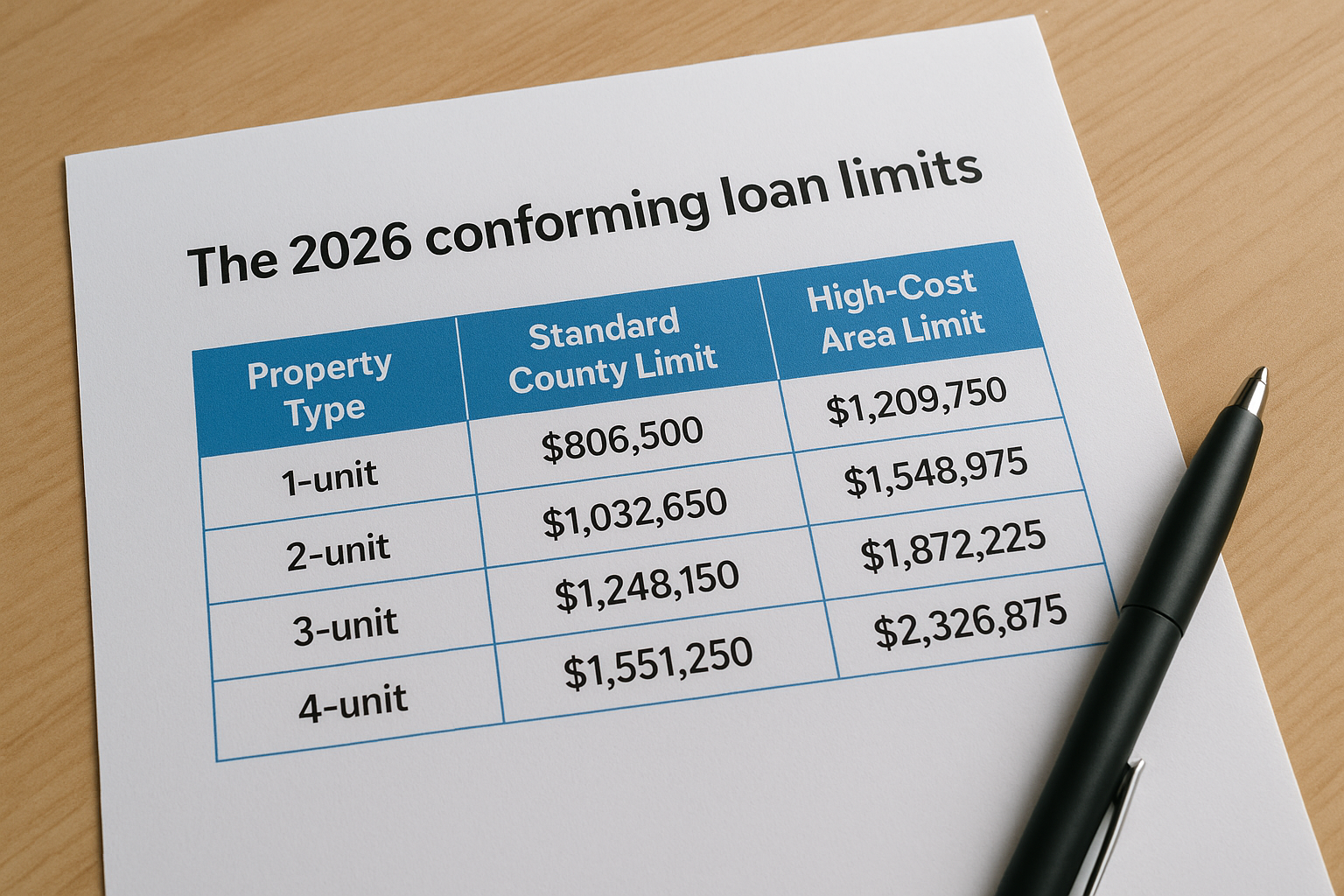

The 2026 conforming loan limits

For 2026, the baseline conforming loan limit is $806,500 for a single-unit property in most U.S. counties. Any loan request above that number puts you in jumbo territory. The FHFA adjusts these limits annually based on national home price data, and the 2026 figure reflects continued appreciation in property values across most markets.

| Property Type | Standard County Limit | High-Cost Area Limit |

|---|---|---|

| 1-unit | $806,500 | $1,209,750 |

| 2-unit | $1,032,650 | $1,548,975 |

| 3-unit | $1,248,150 | $1,872,225 |

| 4-unit | $1,551,250 | $2,326,875 |

If your loan amount lands above the limit in your specific county, you face a full jumbo underwriting review, regardless of how close to the threshold you are.

High-cost area exceptions

Counties with significantly higher median home prices receive elevated conforming limits set at up to 150% of the baseline. In these designated high-cost areas, the ceiling rises to $1,209,750 for a single-unit property. Major metros like San Francisco, Los Angeles, New York City, and Honolulu fall into this category, which means buyers in those markets can borrow more before triggering jumbo status.

Your specific county's limit is published and updated by the FHFA each year. In the Chicago metropolitan area, most counties use the standard baseline, so any purchase requiring financing above $806,500 moves into jumbo underwriting. Confirming your county's exact threshold before you start shopping saves you from surprises mid-process.

Multi-unit properties and the jumbo threshold

The limits scale upward based on the number of units in the property. A 2-unit property in a standard county carries a conforming ceiling of $1,032,650, while a 4-unit property reaches $1,551,250 before crossing into jumbo territory. For investors financing duplexes or small multifamily properties, this distinction matters because qualifying under conforming limits opens up more flexible underwriting paths with lower reserve requirements.

Your down payment affects your loan amount, but it does not change the loan type classification on its own. If you're purchasing a property at $900,000 with 10% down, your loan amount lands at $810,000, which is still above the standard single-unit limit and still requires jumbo financing. The only number that determines classification is your final loan amount compared to the applicable county limit for your property type.

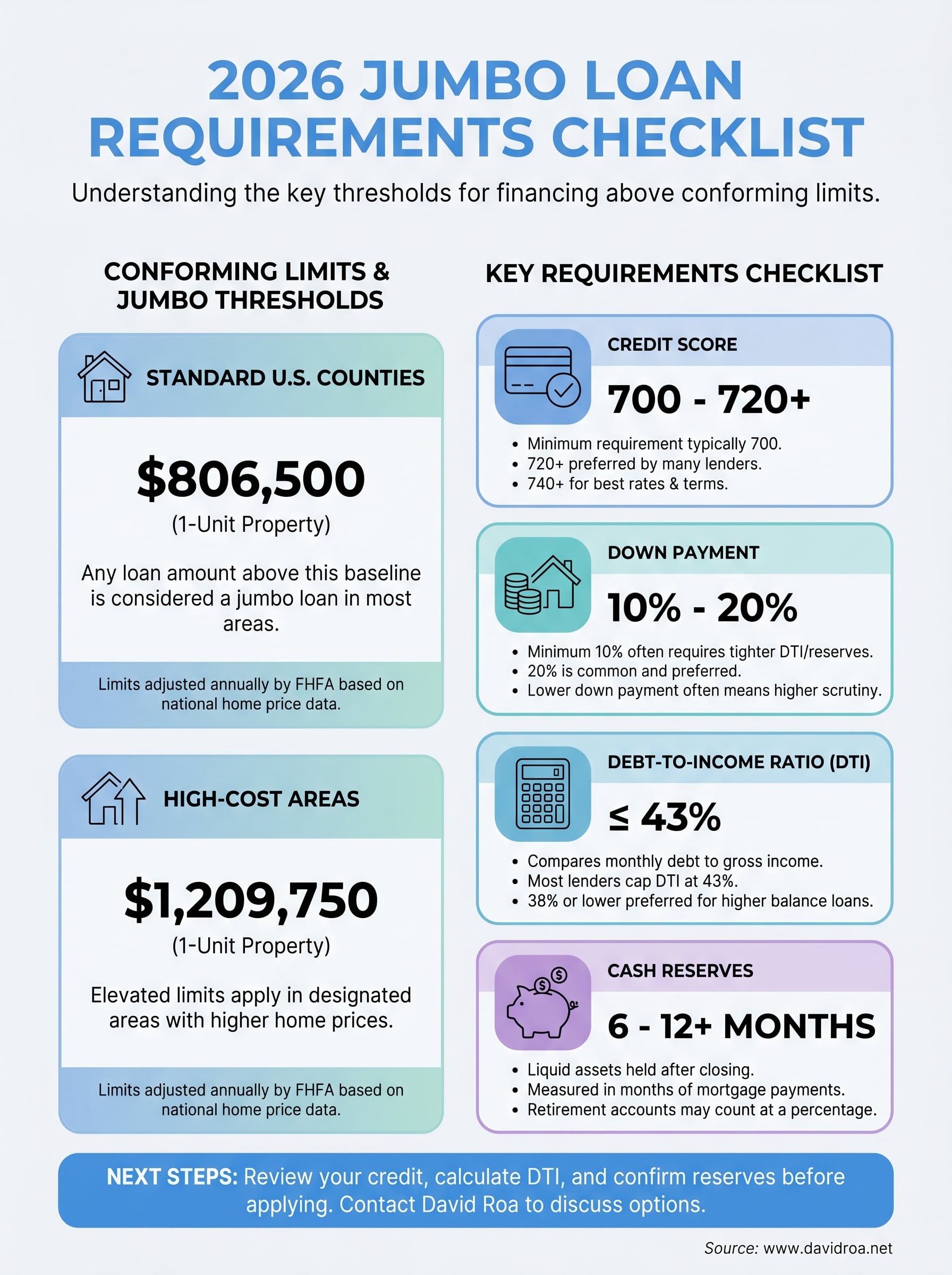

Jumbo loan requirements checklist

The four areas every lender examines when reviewing a jumbo application are credit score, down payment, debt-to-income ratio, and cash reserves. Meeting the minimum on any single factor isn't enough; you need to clear all four thresholds simultaneously. Understanding where each bar sits lets you prepare before you apply rather than scrambling to fix issues during underwriting.

Credit score

Jumbo lenders typically require a minimum credit score of 700, though many set the floor at 720 or higher, especially for larger loan amounts. A score of 740 or above puts you in the best position for competitive rates and less restrictive reserve requirements. Unlike FHA or VA loans, there's no government floor here, so each lender sets its own standard.

Down payment

Most jumbo programs require a minimum down payment of 10%, but 20% is far more common among lenders. Putting down less than 20% typically means higher rates, additional scrutiny, and stricter reserve requirements. On a $1,000,000 purchase, a 20% down payment means bringing $200,000 to the table before closing costs.

Lenders offering 10% down jumbo programs often offset that risk with tighter DTI limits and larger reserve requirements, so a lower down payment doesn't simplify the overall process.

Debt-to-income ratio

Your DTI ratio compares your monthly debt obligations to your gross monthly income. Most jumbo lenders cap DTI at 43%, and many prefer to see it at 38% or lower. Higher-balance loans or borrowers with layered risk factors such as lower credit or a smaller down payment will face tighter DTI ceilings.

Cash reserves

Cash reserves are liquid assets you hold after closing, measured in months of mortgage payments. Jumbo loan requirements for reserves typically range from 6 to 12 months, and some lenders ask for up to 18 months on loans above $1.5 million. Retirement accounts often count at a percentage of their value, but lenders want to see accessible funds rather than money tied up in illiquid investments.

How to qualify for a jumbo loan step by step

Qualifying for a jumbo loan works best when you approach it in a deliberate sequence rather than applying and hoping for the best. Each step builds on the previous one, and identifying weak spots early gives you time to correct them before a lender sees your file. The following process mirrors how an experienced loan officer walks a borrower through jumbo loan requirements before submitting an application.

Step 1: Pull and review your credit report

Start by pulling your credit reports from all three bureaus: Equifax, Experian, and TransUnion. Review every account for errors, late payments, or collections that could drag your score below the 700-720 threshold most jumbo lenders require. Dispute inaccuracies before you apply because the correction process takes time, and lenders use the middle score across all three bureaus to make their decision.

Paying down revolving balances to below 30% of your credit limit is one of the fastest ways to move your score upward before applying.

Step 2: Calculate your debt-to-income ratio

Add up your total monthly debt payments, including your projected new mortgage, property taxes, insurance, car loans, student loans, and minimum credit card payments. Divide that total by your gross monthly income to get your DTI. If that number sits above 43%, you either need to reduce existing debt or document additional income sources before moving forward with a jumbo application.

Step 3: Verify your down payment and reserve funds

Confirm that your down payment funds have been seasoned in your account for at least 60 days. Lenders will request bank statements covering that period and flag any large deposits that lack a clear paper trail. After accounting for your down payment and closing costs, you also need to show 6 to 12 months of liquid reserves remaining in accessible accounts.

Step 4: Organize your documentation

Jumbo underwriting requires more documentation than a standard conventional loan. Prepare the following before your application:

- Two years of tax returns and W-2s (or 1099s if self-employed)

- Two months of bank and investment account statements

- Pay stubs covering the most recent 30-day period

- Documentation for any other income sources such as rental income or business distributions

Common jumbo loan roadblocks and fixes

Even well-prepared borrowers run into issues during the approval process. The problems that stall applications aren't always obvious upfront, but they follow predictable patterns tied directly to jumbo loan requirements around income, assets, and debt. Knowing what flags lenders and how to address it before you apply keeps your timeline intact.

Self-employed income and documentation gaps

Self-employed borrowers face more scrutiny in jumbo underwriting because lenders average two years of net income from tax returns rather than relying on a pay stub. If your most recent year shows a significant drop from the prior year, lenders use the lower figure, which can reduce your qualifying income even if your cash flow is strong. Bank statement loan programs exist as an alternative for borrowers who write off large business expenses, but those carry their own rate premiums and stricter asset requirements.

Reserve shortfalls after closing

Many borrowers focus entirely on saving for the down payment and overlook post-closing reserve requirements. After your down payment and closing costs clear, you still need to show 6 to 12 months of liquid reserves sitting in accessible accounts. If your savings run thin after closing, moving funds from a retirement account into a liquid account early gives the balance time to season and provides the paper trail lenders require.

Retirement accounts typically count at 60 to 70 percent of their vested value toward reserve calculations, so factor that discount into your planning.

DTI sitting above the limit

A debt-to-income ratio above 43% is one of the most common reasons jumbo applications stall. Paying off installment debt like car loans or personal loans before you apply directly reduces your DTI and is the fastest path to clearing that threshold. If payoff isn't realistic in your timeline, documenting additional income sources such as rental income, investment distributions, or a second job can raise your qualifying income and bring your ratio into an acceptable range.

Alternatives to a jumbo loan

Not every high-value purchase has to go through jumbo underwriting. If you're close to the conforming limit or want to avoid the stricter jumbo loan requirements around reserves and credit, a few alternative financing structures can reduce that friction. Each option involves real tradeoffs, so understanding how each path works helps you pick the right one before you commit to a strategy.

Piggyback loan strategy

A piggyback loan splits your financing into two separate loans to keep each one below the conforming limit. The most common structure is an 80-10-10: an 80% first mortgage, a 10% second mortgage (typically a home equity loan or line of credit), and a 10% down payment from you. Both loans stay within conforming guidelines, which often means more flexible approval criteria and more competitive rates than a single jumbo loan.

This structure works best when you have strong credit and enough reserves to support two separate monthly payments rather than one.

Conforming loan with a larger down payment

If your purchase price sits just above the conforming limit, putting more money down can bring your loan amount back below the threshold entirely. On a $900,000 purchase in a standard county, a down payment of roughly 11% drops your loan below $806,500 and removes the jumbo classification. You trade a larger upfront cash outlay for a smoother qualification process and access to standard conventional underwriting standards without the additional scrutiny.

Portfolio loans

Portfolio lenders hold loans on their own balance sheets rather than selling them to Fannie Mae or Freddie Mac. Because they set their own underwriting criteria, they can offer more flexible terms for borrowers with unusual income documentation, higher DTI ratios, or non-traditional assets. These loans often carry slightly higher rates than standard jumbo products, but they open a realistic path for borrowers who don't qualify under conventional guidelines. Self-employed buyers and investors with multiple financed properties frequently find portfolio lending to be a practical route worth exploring.

Next steps

You now have the actual numbers behind jumbo loan requirements: a credit score of 700 or higher, a down payment of at least 10 to 20 percent, a DTI ratio at or below 43 percent, and 6 to 12 months of liquid reserves after closing. Those four criteria, taken together, determine whether your application moves forward or stalls.

Before you apply, pull your credit reports, calculate your current DTI, and confirm your reserve funds will clear the post-closing threshold. Catching a shortfall now is far easier than addressing it mid-underwriting when your rate lock is ticking and your purchase contract has a deadline.

Working with an experienced loan officer makes that preparation faster and more targeted. David Roa's team has closed over $150 million in loans, including complex jumbo deals that required creative structuring across credit, income, and asset documentation. Contact David Roa to discuss your jumbo loan options and get a clear picture of where you stand before you apply.