Conventional Loan Vs Jumbo Loan: Limits, Rates, And Rules

When you're shopping for a home above a certain price point, the type of mortgage you qualify for changes, and so do the rules. The conventional loan vs jumbo loan distinction matters more than most buyers realize because it affects your interest rate, your down payment, and the documentation you'll need to close. Getting this wrong can cost you thousands over the life of your loan or, worse, stall your purchase entirely.

The short answer: conventional conforming loans follow limits set by the Federal Housing Finance Agency (FHFA), while jumbo loans exceed those limits and come with stricter qualification standards. But the real differences go deeper than dollar amounts. Credit score thresholds, reserve requirements, and rate structures all shift depending on which category your loan falls into. With over 25 years in mortgage lending and more than $150 million funded, I've walked buyers through both sides of this decision hundreds of times at David Roa, and the right choice always depends on your specific numbers and goals.

This guide breaks down the limits, rates, and qualification rules for both loan types so you can determine which one fits your situation before you start making offers.

Why the conventional vs jumbo choice matters

The loan category you land in shapes nearly every financial detail of your mortgage. Whether you're buying a primary home, a vacation property, or an investment asset, the conventional loan vs jumbo loan distinction influences what you pay each month, how much you need to bring to closing, and how long your approval process takes. Most buyers focus on the home price and interest rate, but the loan type sitting underneath those numbers controls far more than they expect.

Your purchase price sets the stage

Your home's price tag is the first signal that tells lenders which category you fall into. If your loan amount stays under the FHFA conforming limit for your county, you're looking at a conventional conforming mortgage. Cross that threshold and you enter jumbo territory automatically, regardless of your credit score or income. Many buyers in higher-cost markets like Chicago or coastal cities get pushed into jumbo status without planning for it, which creates real surprises at the application stage.

The loan limit, not the home price, determines whether your mortgage is conventional or jumbo, so always check current FHFA limits before you start making offers.

This matters because lenders treat these two categories very differently from the moment they receive your file. Conventional conforming loans get packaged and sold to Fannie Mae or Freddie Mac, which lets lenders price them more competitively. Jumbo loans stay on the lender's own balance sheet, so those lenders set stricter internal rules to manage their exposure.

The ripple effect on your finances

When your loan shifts from conventional to jumbo, the financial impact shows up in several places at once. Your required down payment often increases, your credit score benchmark rises, and lenders typically want to see larger cash reserves sitting in your account after closing. None of these changes are impossible to meet, but they require you to plan ahead rather than scramble once you're already under contract.

Your debt-to-income ratio also gets scrutinized more tightly on a jumbo application. Conventional conforming loans allow DTI ratios up to 50% in some scenarios. Jumbo lenders often cap that ratio at 43% or lower, depending on the loan size and their internal risk appetite. If your income picture is complicated, such as self-employment or multiple income streams, that tighter threshold can directly affect whether you get approved.

2026 loan limits and what makes a loan jumbo

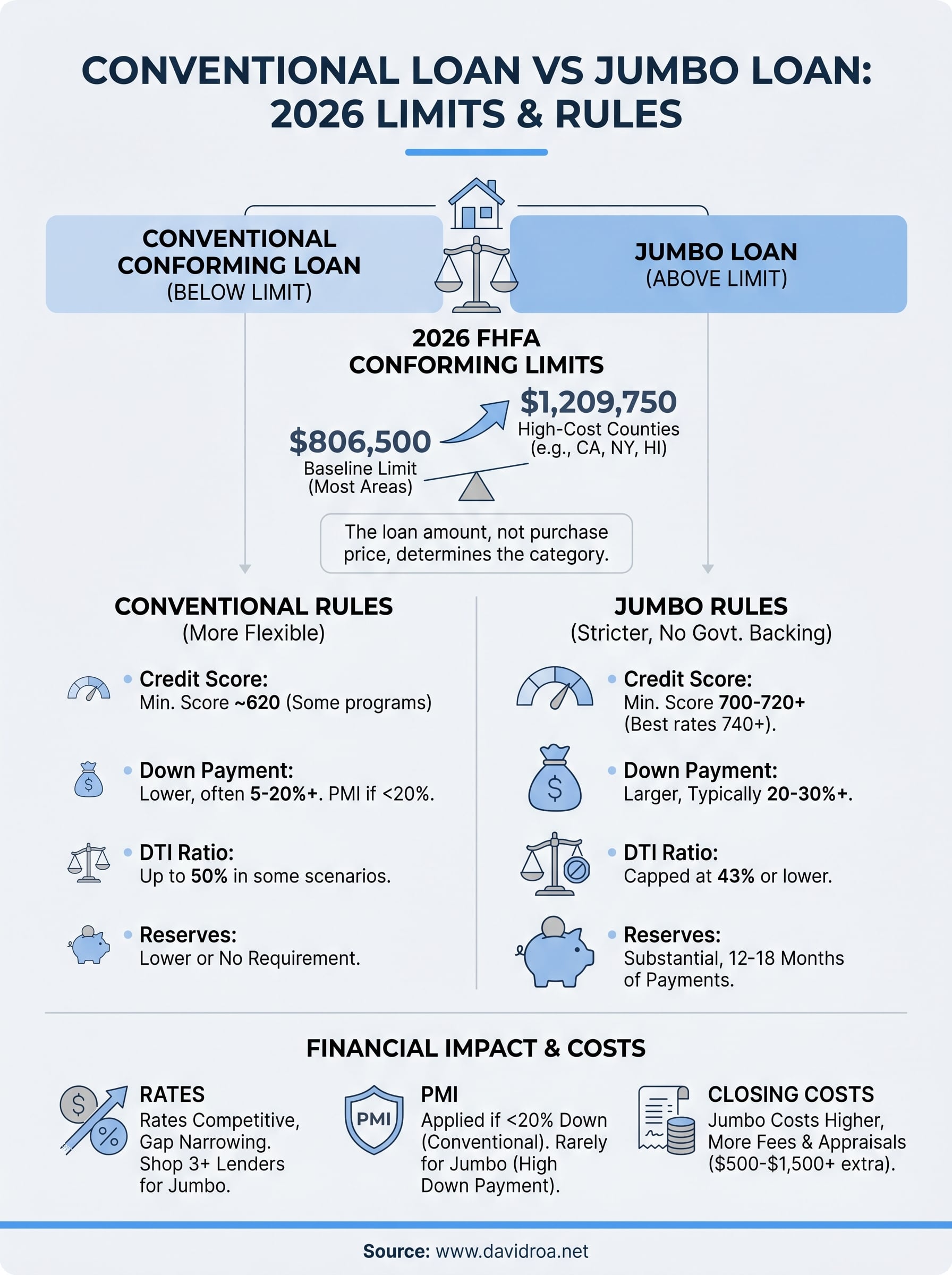

The FHFA adjusts conforming loan limits each year based on average home price movement. For 2026, the baseline conforming loan limit sits at $806,500 for a single-unit property in most U.S. counties. Any mortgage that exceeds this figure crosses into jumbo territory automatically, regardless of your credit profile or down payment size.

The 2026 baseline limit

That $806,500 threshold is the line that separates conventional conforming loans from jumbo loans for standard-cost markets. When your loan amount stays at or below this figure, your lender can sell the loan to Fannie Mae or Freddie Mac. Once you go above it, the lender holds that loan on their own books, which is exactly why the conventional loan vs jumbo loan distinction carries significant financial weight for both buyers and lenders.

Knowing this number matters because many buyers don't realize they've crossed into jumbo territory until they're already in the application process. Checking the limit before you set your purchase budget saves you from unexpected documentation requirements and down payment surprises later.

High-cost county adjustments

Some counties qualify for higher conforming limits because local home values consistently exceed the national average. In designated high-cost areas, the 2026 ceiling reaches $1,209,750 for a single-unit property. Markets like parts of California, New York, Hawaii, and certain metro regions fall into this category.

Always verify your county's exact 2026 limit through the FHFA's official lookup before assuming your loan needs to be jumbo.

Multi-unit properties also carry separate, higher limits at each tier, so investors buying small multi-family properties need to check the unit-specific threshold rather than relying on the single-unit baseline.

Rates, PMI, and closing cost differences

The conventional loan vs jumbo loan comparison gets particularly important when you look at the actual cost of borrowing. These two loan types price differently, carry different mortgage insurance rules, and generate different closing cost structures. Understanding each one before you apply gives you a clearer picture of your true monthly payment and total upfront costs.

How interest rates compare

Jumbo loans historically carried higher interest rates than conventional conforming loans because lenders absorbed more risk by keeping them on their books. That gap has narrowed in recent years, and in some market conditions, competitive jumbo lenders have offered rates that match or slightly beat conforming loans on larger balances. Still, your credit score, loan size, and lender relationship all influence where your rate lands, so getting multiple quotes matters more on a jumbo than on a conforming loan.

Shopping at least three lenders on a jumbo application can surface meaningful rate differences that directly affect your monthly payment by hundreds of dollars.

PMI rules by loan type

Private mortgage insurance applies to conventional conforming loans when your down payment falls below 20%. Once you reach 20% equity, you can request removal. Jumbo loans operate differently. Most jumbo lenders require a minimum of 20% down, which means PMI rarely enters the picture, but that larger down payment requirement increases the cash you need upfront.

What closing costs look like

Closing costs on jumbo loans typically run higher in absolute dollars because several fees scale with the loan amount. Appraisal fees also increase since jumbo properties often require two independent appraisals rather than one, adding $500 to $1,500 or more to your settlement statement.

Qualification rules lenders tighten on jumbo loans

The conventional loan vs jumbo loan divide becomes most visible when you look at how lenders evaluate your application. Jumbo loans carry no government backing, which means lenders set their own rules and protect themselves by demanding stronger financial profiles. Expect the qualification bar to sit noticeably higher than what you'd face on a conforming loan.

Credit score and down payment requirements

Conventional conforming loans will approve borrowers with credit scores as low as 620 in some programs. Jumbo lenders typically want to see a minimum of 700 to 720, with the best rates reserved for borrowers at 740 or above. Your credit score directly affects your rate tier on a jumbo loan far more aggressively than it does on a conforming one.

If your score falls between 680 and 700, improving it before applying for a jumbo loan can move you into a better rate bracket and save you a significant amount over the loan term.

Down payment expectations also shift. Most jumbo programs require at least 20% down, and some lenders push that to 25% or 30% on loan amounts above $1.5 million or for investment properties.

Reserve requirements and DTI limits

Jumbo lenders want to see substantial cash reserves remaining in your accounts after closing, often 12 to 18 months of mortgage payments. That reserve requirement protects the lender on a loan they're holding on their own books. Your debt-to-income ratio ceiling typically lands at 43%, compared to the 50% that conforming loan programs sometimes allow. Self-employed borrowers need to prepare two full years of tax returns alongside bank statements to document their income thoroughly.

How to pick the right loan for your purchase

Deciding between a conventional conforming loan and a jumbo loan comes down to three concrete factors: your loan amount relative to the 2026 FHFA limit, your financial profile, and your timeline. Most buyers can eliminate one option immediately just by checking whether their loan amount clears the $806,500 baseline for their county. From there, the decision narrows based on what your credit, income, and reserves actually support.

Start with your loan amount

Your first move is to calculate your expected loan amount, not your purchase price. Subtract your planned down payment from the purchase price and compare that number against your county's 2026 conforming limit. If you land under the limit, a conventional conforming loan is available to you, and you should explore it before assuming you need jumbo financing. Some buyers push their down payment slightly higher specifically to stay below the conforming ceiling and capture the easier qualification requirements that come with it.

If your loan amount sits within $50,000 of the conforming limit, run the numbers on a slightly larger down payment before defaulting to jumbo.

Factor in your financial profile

The conventional loan vs jumbo loan decision also depends on what your file looks like. If your credit score sits below 700 or your DTI runs above 43%, a conventional conforming loan gives you more room to qualify. If your score is strong, your reserves are solid, and your loan amount simply exceeds the limit, a well-priced jumbo from a competitive lender makes sense. Talk to a lender who handles both products so you get an honest comparison based on your actual numbers, not a pitch for whichever product serves the lender's interests.

Quick recap and next steps

The conventional loan vs jumbo loan decision starts with one number: your loan amount compared to your county's 2026 conforming limit. Conventional conforming loans cap at $806,500 in most areas (up to $1,209,750 in high-cost counties), carry lower credit score minimums, and allow higher debt-to-income ratios. Jumbo loans exceed those limits, require stronger credit, larger down payments, and substantial cash reserves, but they make higher-priced properties accessible when conforming programs simply cannot cover the purchase price.

Your next move is to calculate your actual loan amount and pull your current credit score before you talk to any lender. Getting both pieces of information upfront means you walk into the conversation knowing which product fits your situation, rather than relying on someone else to frame the decision. If you're ready to run the numbers on your specific purchase scenario, connect with David Roa and get a direct comparison built around your actual file.